I know most of my readers are experienced investors who already have a TreasuryDirect account. If you know a less-experienced investor who could use this information, please pass it along. Thanks …

By David Enna, Tipswatch.com

The news that U.S. Series I Savings Bonds are now paying 3.54%, annualized, for six months is drawing a lot of attention from new investors, people who a few months ago would have laughed off any talk of investing in savings bonds.

This is good. I love when people learn about I Bonds and EE Bonds and appreciate them as valuable and viable investments. Yes, they are “relics” from the past, but that relic status is what makes them so attractive: They have terms that create a flow of interest income much higher than you’d find with any other “modern” safe investment.

But then there is the obvious question: How do you invest in I Bonds? You could ask your broker, but don’t expect any help there. Your broker can’t sell you I Bonds, and can’t make money from advising you to buy them. You can’t buy them on the “open market.” There is only one place to purchase I Bonds, and that is the U.S. government’s site, TreasuryDirect.gov.

What do you need to open an account?

TreasuryDirect says you need these these things to open an individual account:

- A taxpayer identification number … in other words, a Social Security Number.

- A United States address of record. Do you need to be a U.S. citizen? No. Do you need to be living in the U.S.? No. But you need a U.S. address to register the account.

- Be at least 18 years old. A child cannot open a TreasuryDirect account. But a parent or other adult guardian can open an account for a child and link it to the adult’s account.

- A checking or savings account … this can be at a physical or online bank, or at brokerage, such as Fidelity or Vanguard. You will need to know your account and routing numbers.

- An email address.

- A web browser that supports 128-bit encryption. TreasuryDirect states that its site is “optimized for Internet Explorer,” which is classic government dumbness. IE has been replaced by Microsoft Edge and today has a market share of less than 1%. TreasuryDirect even provides “helpful” links to Windows XP service packs that have long-ago been discontinued. TreasuryDirect works fine with Firefox and Chrome browsers. I have tested it with Edge and Safari, too, and it seems to work fine.

When you get to the “Account Type” page, choose “Individual.” (You can also open an account in the name of a trust, but I have no idea how that works.)

A married couple must open two separate TreasuryDirect accounts if both spouses wish to purchase I Bonds. Each account is limited to purchasing $10,000 per person per calendar year, so if you want to purchase $20,000 in a year, you need two accounts.

(There are separate purchase caps for I Bonds and EE Bonds, so an individual can buy $10,000 of both, for a total of $20,000. EE Bonds, by the way, are also an excellent 20-year investment in today’s market. I wrote about that in September 2019.)

Once you get to TreasuryDirect’s “Individual Account Application” page, you’ll need to fill in a lot of personal information — see why you need that 128-bit encryption? — including your Social Security number, date of birth, state driver’s license number and expiration date, mailing address, email address, and bank information.

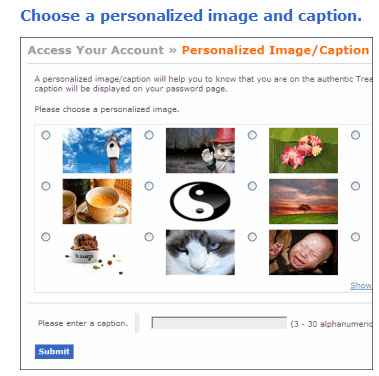

Then, TreasuryDirect will ask you to select a “personalized image and caption.” What’s this about? It is a safeguard against phishing attempts. If a scammer tries to get you to log into your TreasuryDirect account using a false address, you won’t see this image and caption. That’s a signal you are being scammed.

Next, you will choose your password. TreasuryDirect advises, “When selecting your password, avoid numbers, names and dates” that correspond to your personal information. I suggest creating a password that is UNIQUE to TreasuryDirect and not used elsewhere.

You’ll also be asked to answer three security questions, in case you forget your unique password. Favorite author? Favorite movie? And so on.

And that is it, on the last page of the account creation screens, you will be given your new account number (usually something like X-123-456-789). When you go to log later, you will be asked to provide your account number and password. As an additional security measure, you will be emailed a temporary security code to enter before you gain access to your account.

Registering your purchases

How you register a savings bond determines who owns the bond and who can cash it. The registration also determines what happens with the bond if the owner dies.

- One owner. Only one person is named as owner. Only that person can make transactions. If he or she dies, the bond becomes part of the estate.

- Owner and beneficiary. Only the owner can make transactions. If he or she dies, the beneficiary becomes the only owner. The beneficiary can’t be an entity. The registration says “PAYABLE ON DEATH,” or “POD.” Example of registration: JOHN DOE POD TO JANE DOE

- Two owners. For electronic bonds (the only option when buying through TreasuryDirect), the first-named owner is the primary owner; the second is secondary. The registration uses “WITH.” An example of this registration is JOHN DOE SSN 987-65-4321 WITH JANE DOE SSN 123-45-6789. If one owner dies, the other becomes sole owner. If one owner is a person, the other can’t be an entity like a trust.

These ownership rules throw a lot of investors for a loop, because they expect to see “Joint Ownership With Right of Survivorship” as an option. How is “with” ownership different from “joint ownership”? I don’t know, but for a married couple, I’d recommend using this “with” ownership, which should avoid issues after the primary owner’s death.

Using I Bonds for higher education

If you use interest from a Series I bond to pay for higher education, you may not have to pay federal tax on the interest. However:

- If you want to use the bond for your education, you must be the owner of the bond.

- If you want to use the bond for your child’s education, then you or your spouse, or both, must own the bond. Your child may be a beneficiary but not a co-owner.

- Your modified adjusted gross income has to be less than the cut-off amount set by the Internal Revenue Service. This amount typically changes every year. I believe the current caps are $84,950 for single taxpayers and $134,900 for married filing jointly, but a gradual phaseout of the benefit begins at lower income levels. See IRS Publication 970 “Tax Benefits for Education.”

Logging in for the first time

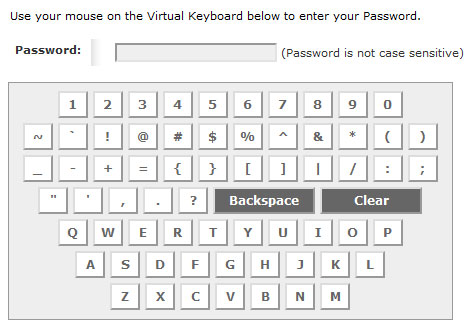

When you first log in, you will enter your account number (it looks something like X-123-456-789) and then you will get a notice that you must go to your connected email account for a one-time security code. Copy and paste that code into the box, submit, and you will come to the password entry page.

This is another security step. You enter your password using a virtual keyboard (it ignores upper and lower case). This security measure will keep keystroke-tracking viruses from learning your password. But you can see why you don’t want a 23-letter-long password. Keep it unique, and reasonable.

Here are the Treasury’s official password rules:

- Length. Use at least eight characters without spaces.

- Characters. Use at least one letter, one number, and one special character such as $ or %, but excluding “\”.

- Content. Avoid numbers, names, or dates that are significant to you. For example, your phone number, first name or date of birth. Try to choose a password based on a memory aid.

On this page, above the keyboard, you will also see the image and caption you selected in the registration pages.

Making your first purchase

After you complete the login process, you will see your account summary page, which should be pretty empty if this is your first purchase. Up in the top row of links, click on “BuyDirect” and you will go to the purchasing menu.

- Select Series I

- On the next page, your preferred registration should be filled in, such “Person1” or “Spouse1 WITH Spouse 2”

- Enter the purchase amount, up to $10,000 per account per calendar year.

- Select the source of funds, which should already be filled in once your link to your bank or brokerage is completed.

- If you select a single purchase, you can select the date for the purchase to be completed. I recommend setting a date near the end of the month, but on a weekday. For example, for this month, I’d probably select May 27, a Thursday. (An I Bond purchased late in a month earns a full’s month’s interest.)

- Submit.

At this point you should see a confirmation of your purchase, but since I’ve already purchased my 2021 allocation, I can’t complete the process to test it.

How do I track/sell my holdings?

TreasuryDirect isn’t really like a brokerage account where you can check the current value of your holdings on a simple “balances” page. When you go to the account summaries page, you will see a value listed, but it is actually the original value of the I Bonds you purchased. If you click on “Savings Bonds” on that list, you go to another page, where you can select “Series I Savings Bonds” and hit submit.

On the next page — titled “Current Holdings > Summary” — you can see a list of your holdings and the “issue date,” “interest rate” and “current value,” which reflects interest paid up to that point. If you click on an individual issue and “select,” you will see at the bottom a link to redeem that savings bond.

When you redeem, you can sell the full amount (including interest accrued), or a partial amount, and you designate the bank account that will receive the funds. TreasuryDirect says you should receive the money in two business days.

(Keep in mind that you must hold an I Bond for 12 months before redeeming, and if you redeem before 5 years you will forfeit the last three months of interest.)

The Treasury also provides a web-based Savings Bond Calculator that it says are for paper bonds only, but in actuality can be used to track and list the electronic version, too. Back in January 2018 I wrote a step-by-step guide to using this calculator. Hint: It’s clunky.

How secure is TreasuryDirect?

This is source of rather heated debates on the Bogleheads forums, because the Treasury makes no “stated” commitment to guarantee your account against hacking or theft. For that reason, some investors will not purchase any holdings in TreasuryDirect. And this debate has been going on for more than a decade.

While the Treasury seems to dodge the “security guarantee” question, I feel strongly that it would take responsibility for any errors/hacking that it caused. But if you fall for a clever phishing attack or have an evil relative, you could face losses. The system does send you email alerts for any account changes, such as in registrations or linked bank accounts, or even if the email address was changed.

The Treasury expects you to monitor your account and provide timely notice of any irregularities. I think the risk is extremely small, and I have not heard of anyone ever losing money through hacking or theft. The complex login system that TreasuryDirect uses, including the two-factor verification and virtual keyboard, add up to strong security.

As an added security feature, TreasuryDirect allows you to place a hold on your account. If you believe someone else has learned your account access information and you want to prevent unauthorized access, you can edit your Account Info in your primary account to place a Customer Hold. This action will prohibit all transactions associated with your primary and linked accounts. After you place your Customer Hold, you will not have access to your account until the hold is removed.

What happens at tax time?

Not much. TreasuryDirect doesn’t have a “user-friendly” attitude when it comes to tax documents. It may (or may not) send you an email reminder to log in and check your current documents. It will not physically mail you anything. When you locate your tax documents, you’ll find the format to be confusing and not-printer friendly.

Of course, with I Bonds, you won’t owe any federal taxes until you redeem a bond, and I Bond interest is exempt from state income taxes. So this isn’t a big deal for an I Bond investor. But if you redeem some bonds, you will have a tax obligation that year and you’ll need to track down the forms.

Conclusion

No one is going to extol TreasuryDirect for being “user friendly,” and some of the complexities arise because of the extra security steps it places in the way of logins. Can you open an account in 5 minutes? I’d bet against that. And there could be some time needed to verify your bank account before you can make a purchase.

If you have more questions, post them below. I might not be able to answer some of the more complex or legal issues, but possibly other readers have some experience in those areas.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

A quick question – my current treasurydirect account works. however, when I try to add “additional” bank/account, it seems working fine, then once I hit “submit”, it keeps saying “treasuarydirect is not available”, so how do I add secondary bank /account ?

It fools you into thinking you can manage bank accounts online. But one cannot. Now you will learn about the Medallion stamp fiasco!

Hello-I tried to open an account, but I had to print a form, go to the bank to get it signed and stamped, and send it by mail to get my account opened. I cannot believe they are taking the forms by mail and not through email or some type of electronic form. I am unsure why I had to jump through this annoying hoop (I am guessing it is because I am a teacher who lives on a campus, and the address comes up as a business address sometimes).

It looks like the time it takes for them to process the form I sent in is months…and I wanted to purchase the I bonds by the end of the year. I only recently learned of these bonds. Do you think there is any chance I get my account opened before the end of the year and can purchase the bonds? Is there any other way to expedite the process? I doubt it, but I figured it could not hurt to ask. Thank you!

I hate that you are having these issues. Many people are able to set up an account in a single day, but if your banking information causes a glitch, you can have these sorts of problems. Have you tried calling TreasuryDirect?

GOOD LUCK WHEN I TRIED CALLING 2 HOUR WAIT YOU WOULD THINK THEY WOULD HAVE A CALL BACK

Thanks for this. One quibble – says you need “A checking or savings account … this can be at a physical or online bank, or at brokerage, such as Fidelity or Vanguard. ” Apparently this is true of Fidelity, but not Vanguard – unlike Fidelity, Vanguard does not give brokerage accounts a routing/ABA number that allows “pulls” or withdrawals, the Vanguard setup is for deposits only.

Last night I tried to write this with links to sites saying this but your site rejected my comment with links with no chance to revise it, so I had to start over. Google a reddit thread on “Pull funds from Vanguard via ACH” for one example of such a site.

Vanguard did change its policy on withdrawals a few years ago. I moved my cash account to Fidelity. I don’t know for sure what the current policy is, or how it connects to TreasuryDirect.

I used my Treasurydirect account number (starts with a letter) and it said that account had been closed. So I tried to open a new account and it said there was already an account linked to that name. Then the message about emailing me a link never showed up in my inbox. I checked my spam folder- not there either. So what do I do now?

If you can straighten out the account, and get it reopened, you can still buy an I Bond allocation in 2022 and then another allocation in 2023. You’ll miss out on a couple percentage points for six months, but still a good investment.

Pingback: Intro to I Bonds October 2022 Edition - Milwaukee Financial & Retirement Advisors | Keil Financial

What is the trick for creating a password on Treasurydirect? I’ve used multiple browsers, have type all kinds of password and follow the rules, and it does not take anything I have tried.

Here are the rules, from TreasuryDirect:

Your password must be a minimum of eight (8) characters without spaces.

Your password is NOT case-sensitive.

Your password must contain at least one letter, one number, and one special character such as “$”, “%”, or “!”, but excluding “”.

You should avoid significant or meaningful numbers, names, or dates.

The actual password may not be used as the password reminder.

My Javascript was not enabled and I was not seeing the virtual keyboard. All good now.

I appear to have made an error in the bank account number or routing number when applying as it was rejected. It appears the only way to correct this is to do a couple pages of paper work, get it notarized , mail and they say it takes 12-13 weeks to process. Do you know of easier way?

Try calling them they will fix simple things. Bad news wait time is long!

Same problem, Phone wait time today is 2 hours. Give me a break! I’m afraid that after investing significant money with them, another snafu will arise and start the agony all over again.

Just opened an account for myself for Ibonds.

If I open gift accounts for my husband (10K) and 2 kids with 10K each (both over 18) and check mark as gifts (the advantage is not to create 4 different accounts till we decide to cash in, plus to fund everything from the same bank), is there any disadvantage vs opening 4 separate accounts?

Eventually, you will need to open accounts for each person to distribute the I Bonds in the future. So 4 separate accounts will be needed then. You and your husband can use the same bank account to fund these purchases, if it is a joint account, so you may want to go ahead and create his account now.

Estate planning question here. I established a Treasury Direct account and purchased I bonds. I registered them with a POD beneficiary so it would go directly to my wife if I die. I also established linked minor accounts for my children who are 12 and 9. I purchased bonds in their names and I am the custodian. My question is, if I were to pass away while my children are still young, would my wife become the new custodian of their bonds? I assume so but just looking for confirmation. Wait time to call Treasury Direct is over 2 hours so I thought I would try here. Thank you.

Sorry, I don’t have any expertise in this field, so I don’t know the answer.

I played with I Bonds and bought a $25.00 on July 19 just to get feel of system. Was getting ready to buy another for the max amount. Looked around to see if the $25.00 earned any interest and can’t see that it did. Question is when does it show any interest add to principal? I followed instructions and all the screens still shows $25.00. Also, didn’t show I could redeem, perhaps that don’t show up until the year anniversary?

This one of the quirks of TreasuryDirect. When you buy an I Bond, you can’t redeem it for one year and if you redeem before 5 years, you lose the last three months of interest. TD will not show your latest three months of interest until you have held the I Bond for 5 years. The I Bond is earning interest, but the TD site won’t show those last three months until 5 years.

So you gotta redeem it to see what is reall worth? After 5 yrs does the interest show up like we expect?

I am about ready to forget the I Bond. I think what is being said I would see one months of interest appear in month 4? That it is always 3 months behind until 5 years? Or maybe you see nothing until the 1 year or 5 year anniversary?

According to the TD website, interest is compounded semiannually. It says, “every six months from the bond’s issue date, interest the bond earned in the previous six months is added to the bond’s principal value; creating a new principal value. Interest is then earned on the new principal.”

This is correct. The interest is earned monthly and compounds semi-annually.

Yes, after 5 years TD will show the full interest earned.

Okay, I think I get it? Interest is earned monthly, but I won’t see that show up in the first few months. But at the 6 month anniversary of deposit, they will post the interest and it will be visible on my account. Then it will be another 6 months before I see another posting of interest which will be a compound interest. Sorry for being so slow at this, different than what use to at Credit Union that works monthly.

No, you will begin seeing interest after three months, but only one month at a time until you get to six months. Then you will see three months. After seven months, you will see four months. You won’t see the last three months of interest until you reach 5 years. The interest is compounded semiannually. However, I don’t think TD actually shows you your current compounded balance, so you will just see the total minus the last three months.

I been thinking on getting an I-Bond and waiting the year, cash it in and pay the last 3 months interest back. Still not a bad investment. Question I have is will I be paying taxes on the full 12 months interest or just pay taxes on the first 9 months interest. Maybe a simpler way will I have to pay taxes on the 3 months penalty? This may be a dumb question as I have never bought a bond, but I did get my account set up and bought a $25.00 just to see if it worked. Now I am thinking about getting serious.

You’d only pay tax on the interest you receive. The penalty won’t be reported.

Pingback: Can you have two names on premium bonds? - Communication And Discuss

For an LLC account it asks for company status with registration… for what exactly is it asking? It just uses the words company status like it is a common term, I’ve googles everything I can think of to try to find out what it is asking. I’m hoping some here knows.

Not sure, but TreasuryDirect limits entity accounts to these types, so it may want to know what type you are registering:

Corporation

Deceased Estate

Limited Liability Company (LLC)

Living Estate (court-appointed legal guardian of the estate of another living person)

Partnership

Professional Limited Liability Company (PLLC)

Sole proprietorship

Trust

Pingback: Looking to put cash to work? Consider short-term Treasury bills | Treasury Inflation-Protected Securities

In Treasury Direct is it possible to designate a Vanguard or other account to receive interest payments?

This is how it works, at least in most cases. You have a bank or brokerage account linked to TreasuryDirect, and then your original investment is drawn from that source, and interest payments and maturing issues are paid into the connected account.

I have had mature bonds just sit in account and had to manually xfer.

Don, this could happen if you didn’t specify how you wanted the redemption to be handled. In the current system, you can specify the outgoing account when you buy the Treasury. Also, you can view how this is handled with your existing holdings, and edit the settings if you need to. After maturity, if the money isn’t sent to your linked account, it goes into TD’s “Zero-Percent Certificate of Indebtedness,” a cash account that pays no interest.

I just signed up for a TD account. I didn’t enter enough digits for my bank account number (there are several at the beginning, mostly 0’s, that I left off). Got a response from TD saying they couldn’t verify my bank account info. Ok, that’s understandable. But when I went in to edit my bank info, it says I have to get a SIGNATURE GUARANTEE on their PRINTED form and MAIL IT?? Are they serious?? Could I just open another account, or is it only one account per SSN? That’s what I came to this site to find out.

I had the same problem. Made a small error with the bank account number. Once they told me, I thought it would be easy to fix. No! I ended up having them closing my account entirely, which took two to three weeks in itself. I decided not to try again. If a website is this much trouble to use at the outset, it’s just going to be more trouble down the line.

Call them on the phone to fix it! Worked for spouse. It almost impossble to close the new account! Signature Guarantee good luck!

This is one issue where you really need to call TreasuryDirect and work it out with them. 844-284-2676

Thank you, Scot, Don, and Tipswatch. After 2 hours and 53 minutes on hold, I did get to speak to a person with a pulse. They are only able to add up to three digits to an account number, and only when it is obviously a case of omission. Because I omitted more than three zeros, I have to fill out the paper form and mail it in. He said a BANK notary is ok, or a paying agent or bond stamp, since Medallion signatures are so difficult to get. It will take up to thirteen weeks to process. He did mention that someone else could buy a gift bond for me with my SSN as the recipient, but I won’t go that route unless I they take too long and I run out of time. Anyone reading this, here are the lessons: 1) you can NOT edit your bank info online once you enter it, even though it appears that you can, and 2) in order to “get in line” to speak to a person, call as soon after 8 a.m. ET as you can – even if you have to get up at 5 a.m. PST, as I did. Any later than that, they will tell you the queue is already full and to try again the next day.

I did the same thing and could not believe in this day and age, that actual paperwork had to be completed and mailed in. I went to the bank to get a Medallion signature. Note – a notarized document is not acceptable. While it says that all banks and credit unions do have someone who can do the Medallion signature, the 3 I tried only have one person, the bank manager, who can do that. After stopping at the 3 banks, all managers were either unavailable or not in the office, I made an appointment with our bank manager and it only took 2 minutes to get the signature. But yes, a hassle.

If I check the box to register my computer in my Treasury Direct account, I am supposed to be able to skip the OTP process going forward. However, no matter how many time I check the box, I continue to have to fill in the OTP every time I log into my account. Why is this?

Do you have cookies blocked? That could be the reason. Still, the “remember computer” feature only works for a limited time, like a month.

Get max bonds for your tax refund. You have to ball park your refund in Dec. You can remove money from a tax-deferred account but have the custodian withhold it all for taxes. This way you can max out your bond purchase. This works for estimated taxes if you are short also.

Pingback: Ready to convert paper I Bonds into electronic form? Here’s a step-by-step guide. | Treasury Inflation-Protected Securities

How do we contact the Treasury Dept? They say that we already have an account, and we don’t.

Thanks

You can call TreasuryDirect at 844-284-2676 (you may experience a long wait time because of the popularity of I Bonds)

Question – It is a question about someone who is not a citizen and is living in USA on work VISA. What happens to an electronic ibond if after purchasing it, the holder decides to leave USA and go back to his country? We know that for buying ibond we need to be resident of USA.

Does cashing out an electronic ibond also require you to be a USA resident OR one can cash it out online even being outside the country?

I think the only issue would be that you would need a U.S. located bank account to receive the payment.

Yes the US bank account would still be there to receive the payment. I hope then it should be ok right?

Yes, should work.

Can a couple be able to create two joint accounts to buy $20,000 I-Bond a year after providing both SSN?

Yes, a couple must create two separate accounts at TreasuryDirect, and then each can purchase $10,000 in I Bonds each calendar year.

Is it ok to use the same bank account for the two treasury accounts of both husband and wife? The bank account belong to the husband and the wife is not a joint holder on that bank account. Can it still be used for treasury account of wife?

Never seen this question before; the fact that both spouses aren’t connected to the account could be an issue. Don’t know.

Can we open Individual “WITH” accounts now and later open a Trust account for everything going forward? I’d like to set up some kind of Trust, but just don’t know how or where to get started. In the meantime, I want to open and invest in I-bonds since their rates are screaming right now.

Yes, you can do this.

You will need two Trusts to buy the full couple amount. Im gonna try one trust change the order on the registration and use each ss number.

Pingback: Ready to invest in I Bonds for the first time? My advice: Act quickly | Treasury Inflation-Protected Securities

Pingback: Treasurydirect Login | Find Official Site

We have a Trust so created an Entity Account with Treasury/Direct. Wife is Account Manager, and as we understand it, she is the only one who can do anything with the account even though we are both the Trustees of the Trust. What if Wife passes away suddenly? How does the other (Trustee) or (Trust) access the Account?

Currently Bonds are in name of “Husband or Wife” names. Should we send them to Treasury/Direct to re-issue to our Trust? Is it safe to mail a great number of paper EE and I Bonds to Treasury/Direct?

Pingback: open treasurydirect account all - trustrose.com

Pingback: abrir una cuenta de tesorería directa en línea

Can I add a beneficiary after I made my purchase?

TreasuryDirect uses a WITH registration for every purchase. For example, Person 1 WITH Person 2, and then Person 2 is the beneficiary. You can change this registration after the purchase by viewing the details of each individual I Bond or TIPS. There is an “Edit Registration” button at the bottom of that page for each I Bond or TIPS. You can also set the preferred registration for all purchases by clicking on ManageDirect > Registration List.

“With” can control (buy/sell) the account while the other is alive like a joint POD. The beneficiary only owns the account with a death certificate. Course with today’s electronic selling and xfer, seems to make little difference. If both the “with”s die, its an estate problem.

Thank you for the excellent website. Two questions please.

1. Can both people in a married couple get the extra 5,000 in cash i bonds? If we file jointly can we both buy 5,000 if we have 10K in refunds?

2. If we submit an extra tax payment now for 2021 in order to get a refund, will that work?

Thank you!!

No. 1: No the Treasury allows $5,000 per tax return, so if you are filing jointly, you are limited to $5,000.

No. 2: Interesting question, because I believe the deadline for 2021 estimated taxes was Jan. 18. I don’t know how the IRS will view payments after that date.

The Treasury Direct website allows for creating a “Person 1” With “Person 2” as well as a “Person 1” POD “Person 2.” If I do the WITH option with my wife as “Person 2” can she do the same in her account with me as “Person 2” or do I need to use the POD option?

Yes, you can each have the other spouse as WITH in each account.

I’ve just run into a snag while filling out the Individual Account Application at the TD website. When I get to the “Bank Information” section, there is not enough space in the “Names on the Account” box to type both my name and my wife’s name as they appear on our joint bank account. The box only allows for a limited number of characters, so when I try to type my name and my wife’s name in full, I only get as far as JOHN WILSON / ELIZABETH WIL. (Just as an example.) I can’t find any instruction regarding this on the website. Would it be okay to type JOHN & ELIZABETH FERGUSON? I can’t imagine that many other people haven’t encountered this same problem. This is pretty frustrating; our names are simple and not very long.

I have good luck with their customer service people both on the phone and with e-mail. They may have some ideas.

What is maximum length of the name of a revocable trust that can be used as the entity? Does that number include hyphens, spaces, periods and commas?

Sorry, I don’t know the answer. Possibly others do? Can you abbreviate the name if necessary?

Spouse had that issue, she called and they really only care about the account and routing numbers. So just put in as much as you can.

Hi Tipswatch,Don,

Looks like based on Don’s message, Treasury care only about account and routing numbers, so I guess it should be ok to use husband’s account in wife’s treasury account, even if she is not a joint holder in that account.

Thanks to all for the answers!

Hi Tipswatch,

My last comment was actually a question. Sorry I missed a question mark. Should it be ok then, to use one bank account for both husband and wife’s treasury accounts, even if the wife is not a joint holder in that bank account?

Your site does a great job of getting started and on-going help, yeah but (there is always a yeah but). Need help with regards to estate planning.. Do you recommend completing Form 5188?

I have never used that form. My wife recently converted some her mother’s Savings Bonds from a trust to her mother’s individual account but I don’t think she used the power-of-attorney form.

I accidentally mis-entered my bank account info. It’s going to be a pain to get it corrected, so make sure you enter your bank info correctly!

Pingback: U.S. Series I Savings Bonds Simplified featuring David Enna - Milwaukee Financial & Retirement Advisors | Keil Financial

A real can of worms. Anyone register a Living Trust revokable? Seem like the registaration name needs to contain something other then xxx family Trust!

I closed my treasury direct account because it was too clumsy and I heard on various forums that customer service can be pretty bad if anything goes wrong or someone needs help with the account after the account holder is incapacitated or dies.

I have had good luck getting to talk to someone about I-bonds at Treasury Direct. You need to phone and ask for someone who has been working there a long time. I got to talk to a nice really old lady, who knew all the ins and outs.

Couple people here have noted the good phone customer service. However, aside from not seeming to have an option for “other” questions (like navigating their confusing website or clarifying something), their phone hold message said it would be an hour, and it continued to say one hour even after half an hour of waiting, before I gave up. Calling back again I selected the option for people who had gotten messages asking them to call TD back, and that hold message first said 15 minutes and after awhile said 30 min. before I bailed.

I suspect that the strong demand for I Bonds among new TreasuryDirect customers has overwhelmed the help system.

How did you close your TreasuryDirect account? I have been trying but can’t figure out how

Me too. I sent them an Email have not heard back yet.

On the other end of opening an account an account is closing it. The Treasury Direct site has a page on handling savings bonds after somebody dies so buying I or EE bonds seems OK.

Motivated by a potential need for a Medicaid spenddown for a nursing home spouse I have been trying but not succeeding in opening a brokerage account to transfer some TIPS or 30 year bonds into so I can sell them if needed. My bank and then my insurance company did not want to help here so I am trying a 3rd financial institution. If inflation is coming and TIPS become attractive again this is worth keeping in mind. The Treasury Direct Web site talks about the secondary market but does not say much more. Keeping TIPS until they mature is a good idea unless life circumstances get in the way:) If people already have a brokerage account it seems like they are OK.

Treasury Direct is a competitor to brokerages, so it will be difficult to get any help from a brokerage. But I imagine if you keep calling brokerages, and say you are willing to pay a fee, some brokerage will help you. You could try phoning Treasury Direct and ask for someone who might be able to help you with this matter.

I successfully opened an account for myself using Safari on my Mac, with passwords stored in Keychain access. All good. However, when I went to create a second account for my wife, Keychain became confused and things went downhill from there.

Also, I’m not entirely sure but it seems there’s a 20 character limit on passwords that TD doesn’t warn you about.

From my experience, you can have a password manager save your account number, but it can’t save the password, since you have to enter it in using the virtual keyboard. I always tell my browser to “not remember” the password each time after I enter it in that keyboard — because even if it could remember it, it wouldn’t matter.

Whether or not the password can be saved and entered automatically may depend on the browser; Safari on the Mac does supply a password when attempting to log in and it had been remembering and supplying my password OK for a while. It’s also happy to supply the account number, so logging in is – usually – a breeze.

Where I ran in to trouble on the Mac was with the account number. The Mac doesn’t recognize the Account Number as a “UserID” and only saves one account number for the TD site. After I created a second account, I inadvertently let the Mac update the one password for the site to my wife’s password but that’s invalid for my account number.

Another little gotcha – and I hate this everywhere I encounter it – is in the security questions. TD lists out about 8 possible ones and you pick 3 but, when doing password recovery it offers you all 8 questions again. Which 3 did I pick?

This was the ONE time I let the Mac remember my password for me and never wrote it down. I usually also write down question hints but, again, this is the ONE time I didn’t do that. Lesson learned.

It would be helpful if MacOS stored the last few passwords in Keychain but it doesn’t. That would have gotten me out of the jam immediately.

As it was, calling in for help got a very fast response and a quick path to reset.

The two most annoying aspects of I-bonds are:

1. the maximum purchase in one year is $10,000 ($5,000 more if you buy them with a tax refund). It used to be $30,000 a year per social security number.

2. You cannot have a living trust as a beneficiary. A living trust can own the bond, but cannot be a beneficiary. This is particularly annoying for me. I had to convert all my I-bonds in my name to my living trust, a tedious task. All my bank accounts do allow a living trust to be a POD. As you say, I-bonds are something of a relic, which is good and bad, but in this case not so good.

Yes, the purchase limit really is annoying, it should be higher. I hear from now-retired investors all the time who say: “This won’t make a meaningful difference.” And that is true. It takes many years of I Bond purchases — $20,000 a year for couples — to build a sizable asset allocation. And is why many people use tax refunds and trusts to bolster their purchases, since trusts have a separate purchase cap.

When you say trusts have a separate purchase cap, I assume you mean irrevocable trusts. My revocable living trust uses my social security number (not an EIN or TIN), so I believe I am stuck with the $10,000 annual cap.

I don’t know much about trusts, but if that trust has your same Social Security number, then I’d guess it would fall under your cap, as you note.

Question: when the primary owner of a savings bond dies, can the co-owner change the e-mail address on the account? Opinion: people should be able to open TreasuryDirect accounts with just their Social Security numbers and/or a direct link through their bank accounts.

If you are a co-owner and you can log into the account, you can change the account’s email address. I did this awhile back and it was a simple process. You can find that information on the “Account Info” page.

For the 2018 tax year I made a data entry error the IRS caught. They asked for information so I sent copies of everything I had including 1099INT forms. They replied asking for the 1099INT from Treasury Direct which I had already sent to them. I called Treasury Direct and they told me they only do 1099INTs online so I sent the IRS another 1099INT and asked the IRS to call customer service at Treasury Direct with the hope that would help settle things. The IRS person who did the review it seems could not tell what Treasury Direct calls a 1099INT really is one.

Wow. It is true that the form that TreasuryDirect creates looks very little like the usual 1099INT, but it clearly marked “Form 1099-INT Interest Income” so the IRS should have recognized that. I checked to see if can still access my 2018 tax forms, and I can.

After 1099INT, the form continues on with “Form 1099-B Proceeds from Broker and Barter Exchange Transactions” and then with “Form 1099-OID Original Issue Discount” for any TIPS interest accruals. You would think that TreasuryDirect communicates this information directly to the IRS.

Form 8888 lets me use my tax refund to get I-bonds, but currently they have to be paper bonds. Is there a way to put those paper bonds into TreasuryDirect? or track them electronically somewhere?

Yes, TreasuryDirect has a program called SmartExchange that allows you to trade paper I Bonds for the electronic version at TreasuryDirect. Here’s is an excellent guide on how to do it: https://www.treasurydirect.gov/indiv/research/indepth/smartexchangeinfo.htm

This year, I received my paper bonds (the only choice given). Then, I logged into TD, and created what is called a “manifest”. Think of it as a request that lists all the paper bonds that you want to link to your account. You print out the manifest, and tuck all the bonds in the same envelope, and send it to TD. I use USPS PRIORITY MAIL with tracking. About 10 days after receipt, the manifest will be processed, and the bonds will show up online. It can take a little longer if you do it right at the peak of tax season.

Here’s the link with more detail about how the manifest list is formed:

https://www.treasurydirect.gov/indiv/help/TDHelp/howdoi.htm#convertpapersb

This year the IRS did not use my refund to purchase my I Bonds. Form 8888 instructed them to do so. Is there a way to correct their error?

This would probably take a direct communication with the IRS, especially if you have already received a refund payment in a check or automatic deposit.

The only time I have experienced security issues (meaning, being run through the wringer on medallion guarantees) is for my LLCs. For one LLC, it was on adding a second bank account. For the other LLC it was upon adding the first linked bank account. No issues with the irrevocable trust. So, yeah – I have five accounts: husband, me the wife, two LLCs, and one irrevocable (not a living) trust. The trust has its own EIN and linked bank account also under the EIN. As for the individual accounts, never any trouble.

I have found that medallion signature guarantees are hard to get suddenly, even at a bank where I have done business for 30 years. I end up having to go to a credit union where I have a small account, and they will do it quickly. For your main accounts, did you need a medallion guarantee? I don’t think I needed one when I changed linked banks recently.

They are beastly difficult to get. My Bank of America bank stopped doing them. (And, frankly, that is the only reason I had had a linked Merrill Edge account at all with Bank of America). So, I went to BB&T and opened an account there, because they did them. And, now, BB&T has been bought by SunTrust, and is now Truist. So, I have no idea if they still do it.

I only had to do this for my LLCs and never the main individual accounts. I have in my estate instructions to never close out any linked bank account, and never close my phone number (for two factor authentication) until all the money is depleted!

My wife and I opened out TD accounts in January. Mine went through no problem but my wife’s account was out on hold until she sent them a signature Guarantee form signed by our credit union.

Made an appointment at the credit union and they signed the form and provided their bank stamp.

Not convenient but not real inconvenient either. Just weird why mine went through and the wife’s did not.

Hi Bill,

Did you provide your name in the “Name(s) on the Account” line of bank account section of your wife’s treasury direct account?

I wanted to change my main linked account, does not let you do it online, but have to send in a form! Have not gotten back to it. Also have to covert my refund bonds