The Treasury will offer $9 billion in a new 30-year TIPS at auction Thursday. Here’s what to expect.

By David Enna, Tipswatch.com

It’s been two years since we’ve seen any TIPS auction, of any term, generate a real yield to maturity higher than zero. But that could change Thursday, when the Treasury auctions $9 billion in a new 30-year Treasury Inflation-Protected Security, CUSIP 912810TE8.

The coupon rate and real yield to maturity will be set by the auction, which closes at 1 p.m. EST Thursday. But we can get a pretty good idea where this auction is heading: The coupon rate will almost certainly be set at 0.125%, the lowest the Treasury will go for any TIPS. And the real yield to maturity has a decent chance of rising above zero, making this the first TIPS auction since February 2020 to get a positive real yield.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

The U.S. Treasury issues an estimate of the real yield of a full-term 30-year TIPS each day after the market closes. On Friday, this estimate was 0.09%, up 45 basis points since the beginning of the year. A lot could change over the next week (for example, in the Ukraine), but for now, it looks like this auction has a good chance of generating a positive real yield, meaning a yield that will exceed official U.S. inflation over the next 30 years.

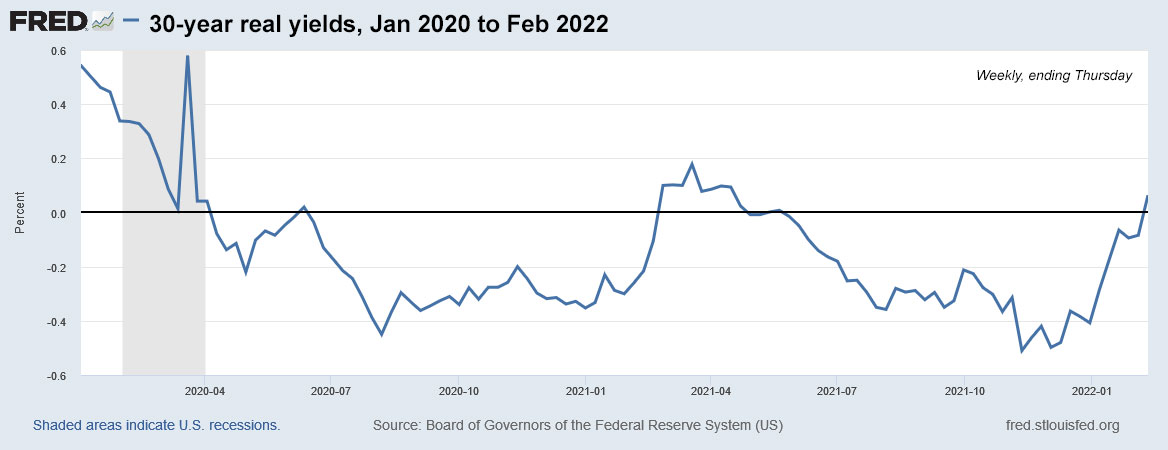

Here is the trend in the 30-year real yield over the last two years, a period that began before the pandemic-caused market panic of March 2020 and continued through two years of aggressive economic stimulus by both Congress and the Federal Reserve:

In recent months, as the Federal Reserve has indicated it will end its bond-buying quantitative easing in March, 30-year real yields have been rising steadily, but still remain below pre-pandemic levels. My opinion is that a “normalized” 30-year real yield would be in the range of 1.0% to 1.5%, and even that is low by historical standards. So these long-term real yields have room to rise, if the economy remains strong and the Federal Reserve begins reducing its massive balance sheet of Treasurys.

However, if the U.S. economy shows any sign of weakness, I’d expect long-term real yields to be depressed by a flattening yield curve. But they should still be positive, offering a return above inflation.

Even if it gets a yield positive to inflation, CUSIP 912810TE8 could still end up auctioning with a slight premium price, because the real yield will still be below the coupon rate of 0.125%. Most likely, that premium will be about 1% above par, if the real yield holds at 0.09%. However, this TIPS will carry an inflation index of 1.00142 on the settlement date of Feb. 28. This means investors could end up paying about $101.14 for about $100.14 of value, after accrued inflation is added in. That’s a rough estimate!

Inflation breakeven rate

With a 30-year Treasury bond trading at 2.24% at the market close Friday, a new 30-year TIPS would have an inflation breakeven rate of 2.15%, which seems reasonable. That means this TIPS would outperform a nominal 30-year Treasury if inflation averages more than 2.15% over the next 30 years.

An inflation breakeven rate of 2.15% is in line with 30-year TIPS auctions back in 2017 and 2018, when U.S. inflation was running at about 2.0%. Now that number is a much-more threatening 7.5%. But the financial markets don’t seem worried, and don’t this trend continuing over 30 years. In fact, markets are predicting inflation at a very moderate rate. We’ll see.

Here is the trend in the 30-year inflation breakeven rate over the last 2 years, showing that long-term inflation expectations have stabilized and even declined slightly over the last year:

Thoughts on this auction

I’ve made it clear for years that I am not a fan of 30-year TIPS with real yields this low. This is a highly volatile investment, and a move of 50+ basis points higher, as we have seen in just the last three months, can reduce the market value of a 30-year TIPS by 15%. For example, a 30-year TIPS reopening auction last August had a premium price of about 12.8% above par value, or $112.84 for $100 of value. Today that same TIPS has a market value of $101.50, meaning it has lost more than 10% of its value in just six months.

Of course, volatility can work both ways, and if you are interested in trading TIPS as a speculative investment, a 30-year TIPS can be attractive. Otherwise, the very long term and high volatility make it unattractive for me. Just my opinion.

30-year TIPS versus a 30-year I Bond

So, if this new 30-year TIPS gets a real yield to maturity slightly higher than zero, does it become more attractive than a U.S. Series I Bond, with a fixed rate of 0.0%? I’d say no. I Bonds have several key advantages over a TIPS:

- The holding term of an I Bond is flexible, anywhere from 1 year (with a three-month interest penalty), to 5-plus years with no penalty, all the way to 30 years when they reach final maturity.

- An I Bond will never go down in value during a time of deflation, while a TIPS will lose accrued principal during deflationary times.

- Interest earned on an I Bond can be deferred until it is sold or matures. For TIPS, both the coupon payment and inflation accruals are taxable in the current year. This “phantom income” makes a 30-year TIPS very unattractive for holding in a taxable account.

- I Bonds have an advantage in the way their interest is compounded, since it all gets compounded. With a TIPS, the coupon rate is paid out as current income and is therefore not compounded (but could be reinvested elsewhere).

My feeling is that I Bonds — at this point — remain more attractive than any TIPS of any maturity. My view would change if we see real yields on 5- and 10-year TIPS climb well above zero. But at this point, I Bonds up to the purchase limit of $10,000 per person per year should be your first money invested in inflation protection.

Auction details

Thursday’s auction will close to non-competitive bids — like those made at TreasuryDirect — at noon EST and then finalize at 1 p.m. EST. If you are purchasing this TIPS in a brokerage account, be aware than auction purchases might be closed by 10 a.m. the day of the auction, or even earlier.

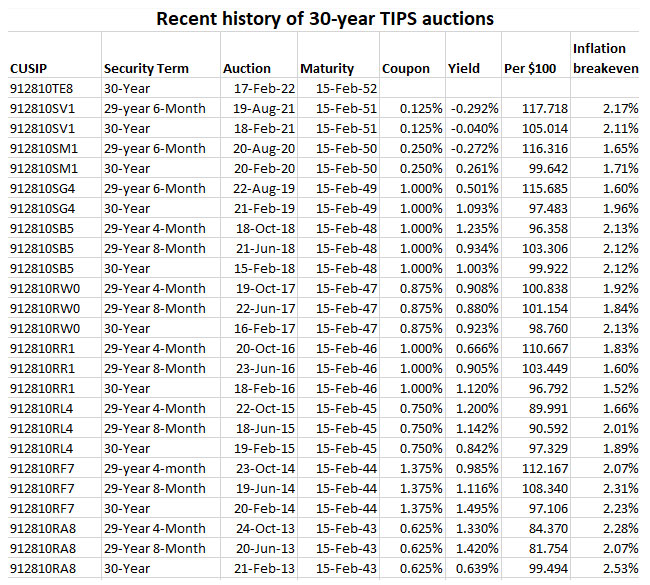

I will be reporting the auction results soon after the close. Here’s a listing of recent 29- to 30-year TIPS auctions, showing that the string of three consecutive negative yields is actually an aberration for this term, even during earlier times of Federal Reserve quantitative easing:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

UPDATE: At Wednesday’s market close, the Treasury was estimating the real yield of a full-term 30-year TIPS at 0.17%. If that holds through the auction close, this TIPS would have a very slightly discounted unadjusted price. Haven’t seen that in two years.

Something I always try to keep in mind. The Treasury offers TIPS to lower its cost of borrowing. Nominal securities have an implicit risk premium to hedge against future inflation. At least in normal environments.