13- and 26-week Treasury bills are an ideal way to maximize yield on your short-term savings. Here’s how to get started …

By David Enna, Tipswatch.com

When you get to be a certain age, cash becomes a lovely thing. Anyone who is retired and lacking steady income from work knows what I am talking about: It’s great to have a stockpile of cash to use for daily expenses and splurges like travel, but also for sudden disasters like the day two weeks ago when my 12-year-old KitchenAid dishwasher went dead.

I define cash as a safe investment — savings account, bank CD, federal money market account, U.S. Treasury bill — with a term of up to one year. But the problem over the last few years has been that safety also meant pathetically low returns, with yields typically topping out at 0.05% on money market accounts and maybe 0.2% in an online savings account.

For much of that time, inflation was very low, which held down the pain of very low yields. Now U.S. inflation is running at an annual rate of 8.6%, and looks likely to remain high for many months into the future. So there’s the dilemma: Where can we get better returns on our cash stockpile?

Let’s take a look at some possibilities, all very safe, in order of potential yield:

- 1-year Treasury bills, now yielding 2.79%

- 26-week Treasury bills, now yielding 2.62%

- 1 year bank CDs, typically yielding close to 2%

- 13-week Treasury bills, now yielding 1.73%

- 4-week Treasury bills, now yielding 1.27%

- Vanguard Treasury Money Market Fund, yielding 1.11%

- Online bank savings accounts, typically yielding 1% to 1.2%

- 6-month bank CDs, typically yielding 0.75% to 1%

- Fidelity Treasury Money Market Fund, yielding 0.98%

- 3-month bank CDs, typically yielding about 0.35%

I highlighted two investments in this list — the 13-week and 26-week Treasury bills — because I think they offer the best combination of safety, current yield, length of term and potential to adjust to higher yields as the Fed continues raising short-term interest rates.

For well over year, I’ve been holding cash in a T-Mobile Money banking account, which pays 4% on the first $3,000 invested (under certain circumstances) and 1% on the remainder. I wrote about this account back in July 2021 and I have been happy with it, because that 1% was at least 2 times what I could earn elsewhere. But now — sorry T-Mobile — 1% is no longer an attractive rate.

I like short-term Treasurys because these issues will react very quickly to any future rate increases by the Fed. You can easily schedule and stagger purchases on TreasuryDirect, and then have the investments roll over every 13 or 26 weeks, riding interest rates higher. The 13-week and 26-week Treasurys are auctioned every week, on Monday. (But it’s Tuesday this week because of the July 4th holiday.) This makes it very easy to stagger purchases to allow you to have access to your money on short notice.

For example, let’s say you have $60,000 in cash you want to put to work.

13-week Treasurys. You could make three purchases of $20,000 each, four weeks apart. Then you can roll these purchases over on TreasuryDirect, meaning you will always have access to $20,000 within about 4 weeks. Through the process, you will be riding interest rates higher if the Fed continues on its current course. Staggering 13-week Treasury bills is a good strategy for someone who might need the cash back in a short time.

26-week Treasurys. You could make three purchases of $20,000 each, eight weeks apart. Again you could roll these purchases over, riding interest rates higher, and always have access to $20,000 within eight weeks. Staggering 26-week Treasurys is a good strategy for someone who feels comfortable with a little longer delay in re-accessing the cash.

A combination. Put $30,000 in staggered 13-week Treasury bills, and $30,000 in staggered 26-week Treasury bills. You’d ride interest rates higher, get a slight yield boost for the 26-week term, and still have access to $10,000 within four weeks.

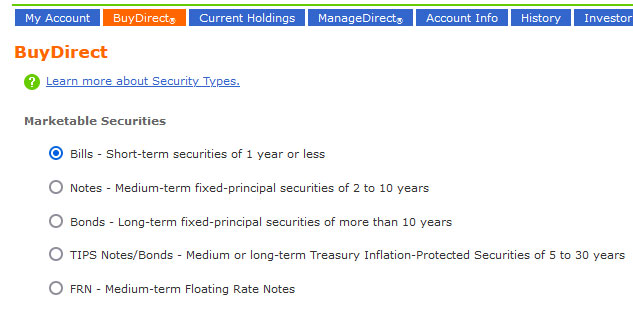

Scheduling these purchases on TreasuryDirect is simple, and I am assuming all my readers now have TreasuryDirect accounts because of the current I Bond mania. (If not, here’s my guide to opening an account.) Simply log into TreasuryDirect, and then click on BuyDirect in the top line of links. Here is what you will see:

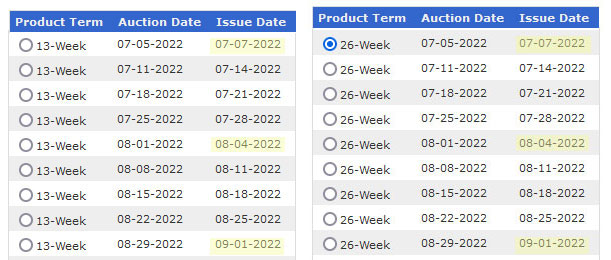

Click on Bills and then click Submit. That will take you to the full list of near-future auctions of Treasury bills, all with terms of 1 year or less. For the 13-week and 26-week Treasurys, you will see lists like these:

In this example, I have highlighted how you could stagger purchases of the Treasurys, but when you go to schedule a purchase, you have to enter each one separately. You can schedule purchases out two months on TreasuryDirect, and note that these issues auction each Monday and settle each Thursday.

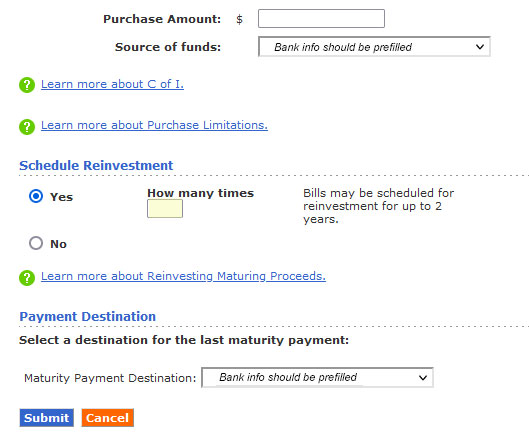

At the bottom of this page is where you enter the amount of each individual purchase, designate the source of the funds and note that you want to schedule reinvestments, and how many. Here is what that looks like:

Reinvestments can only be made for two years out, so that will limit you to 7 reinvestments of the 13-week bills, and 3 reinvestments of 26-week bills. To extend those reinvestments, you’d need to log into TreasuryDirect in the future and set them up. Also, when you need to retrieve the cash, you can log into TreasuryDirect at any time and cancel one or all your reinvestments. After maturity, the cash will return to your linked bank or brokerage account.

This strategy of rolling over short-term Treasurys will be most beneficial while the Federal Reserve is continuing to raise short-term interest rates. When the Fed stalls on rate increases or begins cutting rates, then you may want to look at investing elsewhere, or go with a longer-term Treasury or bank CD.

TreasuryDirect says you can schedule a reinvestment either when you buy your original security or up to four business days before the original security matures. Once you schedule a reinvestment, you can edit or cancel it within the same time frame.

How Treasury bills work

Treasury bills (often called T-bills) are a bit different than your standard bank account or CD. They are zero-coupon bonds, meaning an investor buys them at a discount to par value. Instead of paying a coupon interest rate, T-bills are eventually redeemed at par value to create a positive yield to maturity.

Here is what the auction result looks like, using the auction result for last week’s 13-week Treasury bill as an example:

In this auction, a person making a non-competitive bid (that is all of us little guys) got the high rate of 1.75% (annualized) and an investment rate of 1.782%. The investment rate extrapolates a higher annualized return if the proceeds are reinvested. The Treasury calls this the “equivalent coupon-issue yield.” An investor buying $10,000 of this T-bill would have paid about $9,955.76 and will get $10,000 at the Sept. 29 maturity.

These short-term Treasurys react very quickly to Fed rate increases. Two months ago, on May 9, a 13-week Treasury got an investment rate of 0.915%. Four months ago, on March 7, the auction got a rate of 0.386%.

When the T-bill reaches maturity and is not reinvested, TreasuryDirect will deposit the principal into your designated bank account. The deposit is made on the day the security matures.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: The one key rule for using TreasuryDirect … | Treasury Inflation-Protected Securities

Pingback: Investing for safety: The era of 5% yields is ending | Treasury Inflation-Protected Securities

Heh. Already it’s been pretty much two years since this article was published. What a difference a couple of years make. Interest rates on those short term T-bills are definitely higher than they were since this article. And it doesn’t look as if the government’s in any major rush to lower them any time soon.

Anyways I prefer lump sum on short tem t-bills as opposed to laddering. Especially now in today’s economy and my own personal situation.

The idea of staggering T-bill investments is to give you access to part of the money in just a few weeks, instead of needing to wait 13 weeks or 26 weeks, but you still get the advantage of potentially higher rates for the longer terms. (This hasn’t been true through much of this cycle.)

Pingback: Let’s weigh in on the I Bonds vs. T-bills debate | Treasury Inflation-Protected Securities

How does one use a sole proprietorship to purchase an additional $10,000 in iBonds each year?

From the Harry Sit website: https://thefinancebuff.com/buy-i-bonds-business-sole-proprietor-llc.html

Pingback: Short-term Treasurys: Is it time to go out a little longer? | Treasury Inflation-Protected Securities

Hi David,

I read this article after you mentioned it in the comments of a recent article you wrote. I just invested in some 4-week T-Bills, 912796Z77. The auction finished with a high rate of 4.510% and an investment rate of 4.589%. I did the automatic reinvestment. If I read it correctly, the 4.589% will therefore be the rate I receive, correct? Also, by doing the automatic reinvestment, I won’t have to pay taxes until it stops reinvesting, correct? Lastly, if I needed to withdraw the money before the number of times I set it up for automatic reinvestment, would I be able to stop it or is the money tied up similar to I-Bonds and I can’t touch it?

The investment rate is meant to duplicate the annualized yield you would see on a typical CD. It is the best number, I think. When you buy a T-bill, you pay a discounted price and then get the full amount at maturity. If you roll over the investment, you keep rolling over the original amount and the Treasury pays out your earnings each time. Every time you get interest, it is taxable. It doesn’t matter if you are rolling over the investment, taxes are due. … Yes, you can stop the reinvestments at any time on TreasuryDirect, if that is where you did this.

Pingback: Starving for Yield? Check Out Money-Market Funds - Alt Investopedia

Hi what are the pros and cons of 10 year treasury notes.

At this point there are no huge negatives. The current yield is good, about 4.07%. If yields continue rising, your investment value will go down, but if you plan to hold to maturity, no big deal.

I do not understand the relationship between yield and how it affects the value of investment in US treasury 10 year notes/bonds. I you buy a 10 year treasury note and hold it to maturity does the yields matter? thank you

Yield definitely matters on the day you purchased the T-note, that will be your future return. After that, the market yield will rise and fall, but that really on matters if you plan to sell the Treasury early.

Is there a site like this for people interested in 10yr treasuries?

The 10-year Treasury note gets a lot of coverage in mass media, but I don’t know of a site specializing in that one investment.

My wife and I are now 75. We made it thru the I Bond @ 10k each (wasn’t all that easy) and it is over 9 %. Sounded great… but when can we take it all back out if the rate drops ?

You can’t redeem the I Bond until one year after the month you made the purchase. So it will depend on when you made the purchase. The next variable rate is likely to be about 6.4%, so you’ll do fine for those six months. After the year is up, you should look at the composite rate you are earning. If it is high, you should wait another 3 months to redeem because of the three-month interest penalty on withdrawals before five years.

You are locked into I-Bonds for the first 12 months. This means you have no choice but to accept whatever the new rate may be for months # 7 through #12. I You can withdraw after 12 months but will lose the interest for the last 3 months of ownership unless you keep the bonds for at least 5 years. If the rate drops after the first 12 months and you are not in a hurry to cash out, consider holding for another 3 months, for a total of 15 months. That way, your loss of interest rate will be lower (for months #13 – #15) than if you cash out after 12 months, when you will lose higher rate interest, for months #10 – 12.

Thanks for the informative post. I live in a state where there is no city or state taxes. In reviewing some of the market rates for CDs, I find that there are attractive options with 6 month rate at 3.9% yield through Fidelity. I believe it is one of the MUFG ones. With enough consideration, it looks to be a better option than short term treasury bill since there are no tax advantages for me in either case (pay Fed tax on either anyway).

Pingback: Short-term Treasurys: Even more attractive now. | Treasury Inflation-Protected Securities

Can you provide a comparison of the timing of federal income taxes on interest earned on Treasury bills and on Treasury notes? For example, if I buy a 26 month T-bill today, will I owe any tax for 2022 or will it be deferred to 2023? Similarly, if I purchase a 2 year Treasury note today, what tax, if any, will be due for 2022 for 2023 and for 2024?

Thank you.

For T-bills, the taxes are due in the year the issue matures, according to TreasuryDirect:

“If a bill in TreasuryDirect matures at the end of a year and we don’t issue payment until the first days of the following year, the interest for that bill will be shown on the 1099-INT for the year in which the bill matured, not for the year in which the interest was paid.”

https://www.treasurydirect.gov/indiv/research/indepth/tbills/res_tbill_tax.htm

For Treasury notes, it appears taxes are due on interest paid in any year, as you would expect.

https://www.treasurydirect.gov/indiv/research/indepth/tnotes/res_tnote_tax.htm

You can view any current tax records in TreasuryDirect by clicking on ManageDirect, then find the “Manage My Taxes” link at on the bottom left and click on 2022. This page will include coupon payments for TIPS, but not the inflation accruals, which are reported separately on a 1099-OID and you can’t see that until the end of the year.

When purchasing 26 week notes, can I co-register similar when purchasing I bonds?

David, thank you for the wealth of information and helpful, instructive articles. What a fantastic website!

Question: Where is the easiest/quickest place to find the current (most recent) yield of the newly issued (not secondary market) 13-week and 26-week T-bills? Thanks!

The best source for this is the Treasury’s Yields Curve page: (This shows the Treasury’s estimate each day for each term. It’s a good predictor of the next auction yield, but not perfect.) https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value_month=202207

I spent a lot of time but just could not figure out that table. (Do you use the Par Yield or Bill rates table? Why is there a figure for every day when they are only issued weekly? Why are there 2-Mo amounts? Bank Discount or Coupon Equivalent? I am just not smart enough to figure out those tables.) For anyone else like me, I found the easy answer. Auction results are published here in a table that’s really easy to understand:

https://www.treasurydirect.gov/instit/annceresult/annceresult.htm

Thank you so much for this informative site, David!!

Can you please help me understand the difference between the link above — Daily Treasury Yield Curve — and the equivalent for Daily Treasury Bill Rates? I couldn’t match Par Yield rates for a 1 month Treasury on the former with either the Bank Discount or Coupon Equivalent for the 4 week T bill on the latter… nor any of the above with the 2.029% Expected Yield from Fidelity’s auction purchase page.

https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_bill_rates&field_tdr_date_value_month=202207

I see now what you are asking. If you want to see actual auction results, not current yields, you can go to this page: https://www.treasurydirect.gov/instit/annceresult/press/press_secannpr.htm …. The clickable areas at the bottom will take you to the official auction press releases for every term.

Perfect! Thank you, once again!

This article is the one of the BEST I read regarding T-Bills. It is beautifully drafted and full of gold nuggets. I look forward to reading more of your articles in connection to US Treasuries. -With gratitude + utmost respect

Great article! Do you think it’s worth waiting till July 27th to start a 13 or 26 week ladder now that the latest inflation numbers cement a 75-100 bps Fed hike? Or will it already be priced in?

No harm in waiting, but I think the market is already pricing in much of that Fed rate increase.

David, I really enjoy your articles. I have a question. According to the Treasury Direct Data Results page: https://www.treasurydirect.gov/instit/annceresult/annceresult.htm, the 1-year Treasury bill issued on 6/16/22 was for 3.134%. If the one coming up next week is around the same, or possibly slightly higher, wouldn’t it be a good option? Considering that the the latest 26-week bill was for 2.5%, even if it goes up by 0.5% to 3.0% in the next 6 months, the 1-year bill will still have a higher APR overall since it would have already yielded 3.0% for the first 6 months vs the 2.5% of the 26-week one. Am I missing something?

That 52-week auction is coming up Tuesday. The Treasury as of Friday was estimating the yield at 2.96%, which I consider pretty attractive. Rates could definitely go higher, it’s impossible to know. If you are comfortable with the 1 year term, getting 3% seems attractive. Most 1-year bank CDs are topping out at about 2 to 2.2% right now.

Thank you for the quick reply. How do I find out what the Treasury’s estimated yields are for upcoming auctions? Is this information posted somewhere?

After the market close each weekday, the Treasury posts estimates on its Yield Curves page. https://home.treasury.gov/policy-issues/financing-the-government/interest-rate-statistics

You can use this to see daily estimates for full-term Treasury issues. The nominal Treasurys are listed under Daily Treasury PAR Yield Curve Rates, and the TIPS are listed under Daily Treasury PAR Real Yield Curve Rates. The coupon equivalents for the Treasury bills are listed under Daily Treasury Bill Rates.

Hi David, I am trying to figure something out and I hope you can help. The 52-week T-Bill issue from 7/14/2022 lists High Rate of 2.960% and Investment Rate of 3.070%. It also lists Price per $100 of $97.007111. Wouldn’t that make the actual rate of return 2.992889% ($100 – $97.007111)? What do these 3 numbers represent?

The high rate is the highest rate the Treasury had to offer to move all the inventory. Non-competitive bidders (like us) get the high rate. The investment rate is an attempt to show an annual yield similar to a bank CD; in other words, if this was a bank CD it would yield 3.07%. I have no idea exactly how that price is computed, however.

On my purchase of the 52-week Treasury Bill priced on 7/12/22 my yield will be 3.085%

That’s a very good one-year yield, with best-in-nation 1-year bank CDs barely touching 2.0%. I bought a tier of my phased 13-week Treasury bills this week, investment yield of 2.151%. I’m buying every three to four weeks at first, and then going to roll those over.

Hi David,

Have you use any of the FRN – Medium-term Floating Rate Notes from the Treasury. I been lightly investing in them this year with rates increasing. These are 2 year notes that pay quarter yields. The yields are tied to the weekly auction of the 13 week bills. So the rate floats (up/down) with each auction. They have been increasing nicely as the fed increases rates. Any experience with these?

I have written about FRNs in the past, and you are right, the current rising rate environment is the time to invest in them. From Nov 2013: https://tipswatch.com/2013/11/06/the-new-treasury-floating-rate-notes-why-they-look-like-a-bad-deal/ And in June 2019: https://tipswatch.com/2019/06/03/frns-their-time-in-the-spotlight-is-about-to-end/

My problem with FRNs: 1) It is a two-year investment based on 13-week yields, and 2) the spread is currently *negative* (about -0.003%), so there is no advantage to owning an FRN over simply owning 13-week Treasurys and rolling them over. Seems like they should trade with a yield positive to the 13-week.

Hi David,

Good insight, Maybe I totally wrong and in my thinking on negative spread.

Would the FRN(Floating Rate Notes) be a little different than owning the 13 week bill rate and maybe account for this negative spread because of the speed rate change. Upwardly hopefully

I am say this because the rate sensitivity of the FRN, as rates increase, would adjust more quickly with each 13 week auction and maybe offset the spread different of owning the same dollar value of a few 13 week bills?

Maybe I totally wrong but I could see the case where the spread would come into focus if we would have a full 13 week bill ladder that continuously buys each weekly auction.

Thanks again for the FRN link and love the site and thank you for your wisdom.

Steve

Yes, good point, Steven. Last week’s 13-week got a high rate of 1.850%. The week before it was 1.64%. And the week before that it was 1.230%. So you do benefit for fast-rising short-term rates with the FRN.

i bought some FRN at the auction end April. that yield has floated higher by almost 100 bps since then, but still trails the 2 year treasury auctioned end April by 80 bps. seems to me that the FRN can be a winner when the combo of rising rates and yield curve flattening/inversion occurs during the majority of its duration.

Vanguard Federal Money Market Fund (VMFXX) is now at 1.42% SEC yield and is likely to increase. Would that be a more profitable and more flexible place to put funds these days, as opposed to a 13- or 26-week Treasury?

It is a very good fund, with an expense ratio of 0.11%. It has a higher yield than the Vanguard Treasury Money Market, VUSXX at 1.14% right now, because it turns over its holdings quicker, and so it adapts faster to rising (and falling) rates. VMFXX is considered a slightly riskier fund, because it invests in federal agencies along with Treasurys. I’d expect the returns to track a bit above the 4-week Treasury, now at 1.36%.

If you are looking for an easy way to store cash, this fund is probably it. It is Vanguard’s default cash account. Vanguard makes access a little more complicated than Fidelity’s Cash Management Account, where you can use the Fidelity Treasury Money Market Fund with a current yield of 1.02%. It has a higher expense ratio, which covers Fidelity’s CMA account costs.

Thank you for this clearly written “how to” which I plan to share with others looking to park money for under a year.

Am I wrong in thinking that the Ally 20-month CD (with 60 days EWP) is a better deal for a six-month investment? I’d like to put $20K somewhere with a decent return before I spend it on purchasing I-Bonds in January (10K for my individual account and 10K for sole proprietorship account). If we take into account the early withdrawal amount after 6 months, the Ally 20-month CD is 1.59%. https://www.ally.com/go/bank/20m-select-cd/ and https://www.depositaccounts.com/tools/ewp-calculator.aspx?ids=393198,358683,5207,5205&penalties=2 Ken Tumin’s article has a nice breakdown of the advantages of the 20-month CD: https://www.depositaccounts.com/banks/ally-bank/offers/ We aren’t getting 1.59% on a 3- or 6-month Treasury bill when you take into account annualization. Of course, Ally savings account could increase to 1.59% during those six months, but I’d like to start earning a decent interest rate asap.

I’m a fan of Ally and it is a positive with this account that interest is compounded daily. From I can see on their site the early withdrawal penalty for that CD would be 60 days of interest, which is reasonable. The 20-month CD has a annualized return of 2.35%, but the 6-month Treasury that auctioned yesterday has an annualized return of 2.57%, for a shorter term. If you bought $10,000 of it, you paid $9,873.60 and in six months will receive $10,000. That’s a return of $126.40 in six months and you can annualize that to about 2.5%+. However … if you think interest rates are likely to decline in the next 20 months, then the Ally CD would be the preferred investment, since it will pay 2.35% for a longer term. If you think rates will be heading up, I’d prefer the 6-month Treasury. Both are very good, safe investments.

Thank you so much for responding! The Ally 20-month CD (2.35%) has a return of 1.59% if I withdraw the amount at six months. So if I pay $10,000 and withdraw in six months, then the profit is $159 at the end of six months. If I understand you correctly, if I had paid $10,000 for the 6-month Treasury bill at auction yesterday with annualized return of 2.57%, then the profit would be $126.40. So am I incorrect that going with Ally would be more profitable?

OK, let’s think through your 1.59%, after the two-month interest penalty. The CD pays 2.35% annually, so a six month interest rate would be approximately 1.18%. Then, when you subtract the 2 months penalty, you are down to about 0.78% after six months. I think you are looking at a full year of penalized interest to get to 1.59%, but you are only going to get four months of interest if you break the CD after six months. You’d earn about $78 on a $10,000 investment, versus $126 for the 6-month Treasury.

Thank you again for responding. Have I misinterpreted Ken Tumin’s withdrawal penalty calculator for the 20-month CD? https://www.depositaccounts.com/tools/ewp-calculator.aspx?ids=393198,358683,5207,5205&penalties=2 This chart seems to indicate that at six months, taking into account the two months’ penalty, the interest rate would be 1.58%.

After a bit of confusion, I figured out that Ken Tumin’s chart is showing the “effective ANNUAL percentage yield” if you break the CD early. So, if you break the CD at 6 months, after a 2 month interest penalty, you will get an ANNUAL percentage return of 1.58%. But that applied to six months, not a year. On a $10,000 investment you would get about $79, much lower than the 6-month Treasury’s yield of $126.40 on the same investment amount.

Wow. I would never have been able to figure that out. Thank you so much for taking the time to respond and explain! You just saved me from making a big mistake! (I love your website and link it to the Bogleheads forum quite often.)

If you know you are going to buy I Bonds you might as well keep it in TD for convenience as the six month rates are higher than Ally, although breaking it is a pain (paper form with signature guarantee to a broker).

I’m interested to know your rational for choosing the longer duration T-bills (13 and 26 week) vs the shorter duration (4 week) considering the likelihood of more rate increases this year. It seems we might only be a month away from the 4 week bills paying more than the 13 week are now. I’ve been buying the 4 week bills (using TD) for a few months now thinking that was the better choice in the present environment.

It could be considered a tossup. The 4-week lags a bit under the federal funds rate, which the Fed controls. The federal funds rate is now in the range of 1.5% to 1.75%, and the 4-week Treasury closed today at 1.33%. The 13-week closed at 1.90% and the 26-week at 2.59%. So the 13-week is already pricing in a rate increase of about 57 basis points, over the 4 week. Most likely the Fed will go 75 basis points in late July. I think market expectations fairly accurately price the 4-week and 13-week. The 26-week faces more uncertainty, though, and seems pretty attractive to me.

The benefit of buying through Schwab or Fidelity is the ability to sell before maturity at market price easily. TD will require you to transfer the bills to a brokerage and fill out a form which will need the dreaded signature guarantee.

Ultimately SoFi is paying 1.50% with check writing privileges and that is good enough for my spare cash.

Thanks for the tip, Henry. I assume Vanguard also offers this, and the resell loss before maturity would be minimal if in a reasonably stable market.

Henry, thank you for the reminder. The ability to sell before reaching maturity is great. Also it is very convenient for get a bit more from cash positions in IRA accounts.

UPDATE: Today’s T-bill auction investment rates: 13-week, 1.885%; 26-week, 2.567%. These auctions closed at 11:30 a.m. July 5.

Thank you for the “tip” got my order in early this morning on TreasuryDirect.

Hi- Great article, very concise & clear. Question — In your example of buying three $20K, 13wk bills, can you do that in a sinlge logged-in session by clicking multiple dates as shown on the (Product Term, Auction Date) table below? Or do I need to login to TresuryDirect multiple times and buy one at a time? Thanks.

You can do it in a single session, but you need to make each purchase separately and set up that reinvestment number, and then go on to the next purchase, etc. Not a big deal.

This is a bit off topic, however, I would be interested in your thoughts about lump sum vs. DCA for buying TIPS in the current environment. I’m tentatively planning to make my very first purchase of TIPS at the July 21 auction and using DCA over the next 6-12 months. I want to end up with a mix of 5s and 10s.

I am a fan of the “dribble in” approach, since there is an auction every month and a 10-year auction or reopening comes every other month. This 10-year auction July 21 is starting to look a little weak, since real yields are slipping. But things can change. But I will probably also be buying some amount.

DCU (digital credit union) gives 5% on teh first $1000 put in their online savings. Anyone can join by spending $10 to join a Boston based group during the signup process.

For a different approach, I purchase our Treasuries at Vanguard and use a Google Sheets worksheet to remind me when a Treasury is due to mature. Here’s a copy of the formula taken from cell F11 where column F is titled, “Time to Maturity”.

=DATEDIF(TODAY(),E11,”ym”)&” months,”&DATEDIF(TODAY(),E11,”md”)&” days”

The “Maturity Date” (date formatted column E) with the date of maturity is on the left.

So today, my one year Treasury bill purchased 10/7/2021 reads “3 months,2 days” in column F. (Okay, it gets silly when it reads “1 months, 1 days”, but I’m fine with that; it’s just me reading it.)

The formula for Treasury notes is:

=DATEDIF(TODAY(),E11,”y”)&” years,”&DATEDIF(TODAY(),E11,”ym”)&” months,”&DATEDIF(TODAY(),E11,”md”)&” days”

Thanks for sharing, but I suspect most of us won’t be able to translate the way this copied into text.

Copy the formulas from the text given here to the clipboard and then paste it into the worksheet cells. If needed, find someone that has experience with Sheets that can help.

Any advantage or disadvantage using TD over Vanguard or Fidelity? Trad and Roth allowed just on the former? Thanks David.

Probably no advantage, and some would claim TreasuryDirect has disadvantages (see … cryptic tax forms). But I am fine with using TreasuryDirect for purchases in after-tax accounts and of course … for I Bonds.

Schwab is the place. They do have CDs also that yield more, short term 90 days. TD is a dinasour, wish I could xfer my TD to Schwab! TD got me cuz of IBonds!

I am a money manager. Your site is great. We have been rolling Treasury bills for some of our clients for many months now. Exactly in the manner described here except we invest via our clients custodial accounts at Charles Schwab. Another reason we like the strategy is that T Bills are extremely liquid so should cirumstances change for our market views, asset allocaiton recommendations, or individual client needs, we can easily sell and reinvest elsewhere while in the meantime earning well above money market yields.

Good to hear, and thanks for reading!

Note that when you use auto-rollover at Schwab, your funds sit *UNinvested* for a week between each rollover (repurchase). (That is not the case at Fidelity where the *same day* that a T-bill matures, the next T-bill is purchased.)

Discussion:

https://www.bogleheads.org/forum/viewtopic.php?p=6859184#p6859184

How does the auto roll work at Fidelity? As smoothly as Treasury Direct?

I have been buying T-Bills via Fidelity Brokerage for several months. I find their site very easy. And when you put in an order, there’s a checkbox asking YES/NO to auto roll. So it’s the investor’s choice.

Thank you, David. I didn’t know the answer, so I am really glad you provided it!