Despite a real yield deeply negative to inflation, CUSIP 912828TE0 out-performed a nominal 10-year Treasury.

By David Enna, Tipswatch.com

Back on July 19, 2012, the U.S. Treasury auctioned a new 10-year TIPS, CUSIP 912828TE0, with a rather dire result: The real yield to maturity was -0.637%, which at the time was a record low for any TIPS auction of this term. The coupon rate was set at 0.125%, and buyers paid a hefty premium of about $107.84 for $100 of par value.

In July 2012 U.S. inflation was running at 1.4% and investors weren’t very interested in inflation protection, as noted in this Wall Street Journal report after the auction:

The $15 billion auction of 10-year Treasury Inflation Protected Securities, or TIPS, garnered mediocre interest given the negative-0.637% yield that was offered in a time of little inflationary threat. That’s the lowest yield the government has had to deliver in its sales of 10-year TIPS. It drew a bid-to-cover ratio of 2.62, the lowest measure of overall demand since September.

So, this was a hopeless investment, right? Not exactly. When you compare this TIPS to a nominal 10-year Treasury note available in July 2012, it turns out that — against the odds — CUSIP 912828TE0 ended up out-performing the nominal Treasury.

CUSIP 912828TE0 will mature on July 15, 2022, with an inflation index of 1.26346, meaning that a $10,000 investment at the original auction (which would have cost about $10,784 because of the premium price) will be returning $12,635 to the investor, along with that 0.125% annual coupon rate on the growing principal balance.

That’s a return of about $2,000 over 10 years on a $10,000 investment., or an annual percentage return of about 1.85%. Not stellar. But at the time, a 10-year nominal Treasury was yielding only 1.54% and would have returned only about $11,658 after 10 years, even if you figure in compounding.

So CUSIP 912828TE0 ended up being a “winning” investment, despite its deeply negative real yield to maturity. It auctioned with an inflation breakeven rate of 2.18%, and 10 years later, inflation has averaged 2.4% a year.

The big picture

Up until a year ago, TIPS had been under-performing nominal Treasurys for most of the last decade because inflation was running much lower than expectations. Obviously, with U.S. inflation currently running at 8.6%, we have turned the corner on that. Will that trend continue? It seems very likely, for awhile at least.

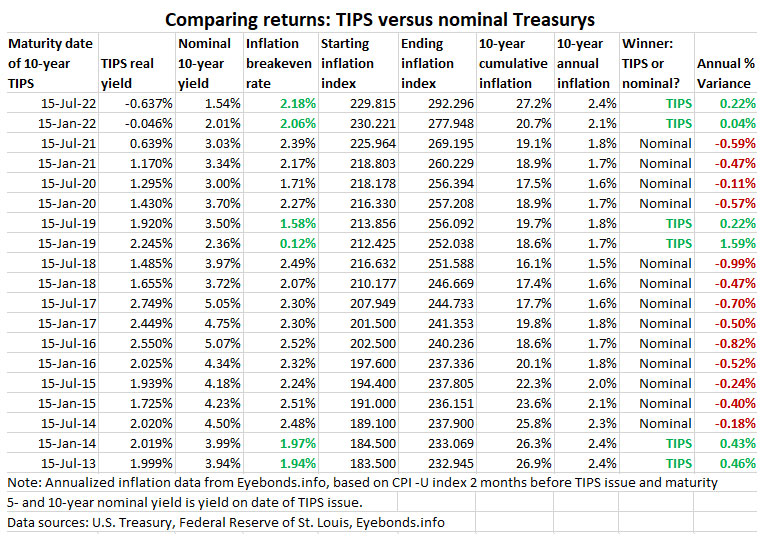

Here is how 10-year TIPS have performed versus 10-year Treasury notes for all maturities since July 2013:

Notes and qualifications

This chart is an estimate of performance, because it uses a full month of inflation in the beginning and ending months, when actually TIPS accruals are based on a half month for the first and last months, with the origination and maturity occurring on the 15th of the month.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David, Your site has been extremely helpful to me in understanding the various Treasury offerings. Thanks for all your hard work.

Thanks for reading, Ed.

David, thank you for your many informative posts and for sharing your knowledge and observations. I have benefited from your work in making better financial decisions. Cheers to you. – Jeff

One of the reasons that my wife absolutely hates TIPS is because is because over the last 10 years 5 year CD’s have outperformed them by 1% a year. She has a similar disdain for iBonds.

I’ve been a fan of both of them as a hedge against inflation. iBonds protected some of our taxable funds. TIPS protected some of our retirement funds.

This last year those 3% CD’s are looking pretty sad. Losing 5% to inflation in a single year has eaten-up half of the 10% gain that CD’s gave us over the last decade.

What happened last year was a classic example of the purpose of TIPS. To protect cash from unexpected inflation. Until last year, that was sort of a nebulous term, wasn’t it?

This year I’m going to take advantage of those TIPS positive yields and move maturing retirement CD’s into 5 and 10 year TIPS. And, maybe do the same with taxable CD’s.

Just in case we get another bought of “transistory inflation” over the course of the next 10 years.

Jimbo, you’ve been a long-time reader so I know you understand why inflation protection is needed, even through that long time inflation was very low. The Fed and Congress got way too confident that low inflation was permanent, even as money poured into the economy.

Hi David,

Thank you for the chart with the Tips Vs Nominal treasuries comparison.

Nominal came out on top 13 or the 19. so 68~% as you pointed out.

Any way to see how I-bonds purchased in the same months would have compared in this mix against these two?

Thank You again for all the good information,

Steven

I don’t track I Bonds vs nominals or TIPS because it would be a LOT of work to collect all that information. I can tell you though that a $10,000 I Bond purchased in July 2012, with a fixed rate of 0.0% at the time, is now worth $12,192, so it has done a bit better than both the TIPS and the nominal Treasury.