Annual inflation is now running at the hottest pace since 1981.

By David Enna, Tipswatch.com

Have we hit peak inflation yet? The answer is: we don’t know, because the June inflation report showed inflation surging ever higher, greatly exceeding already lofty expectations.

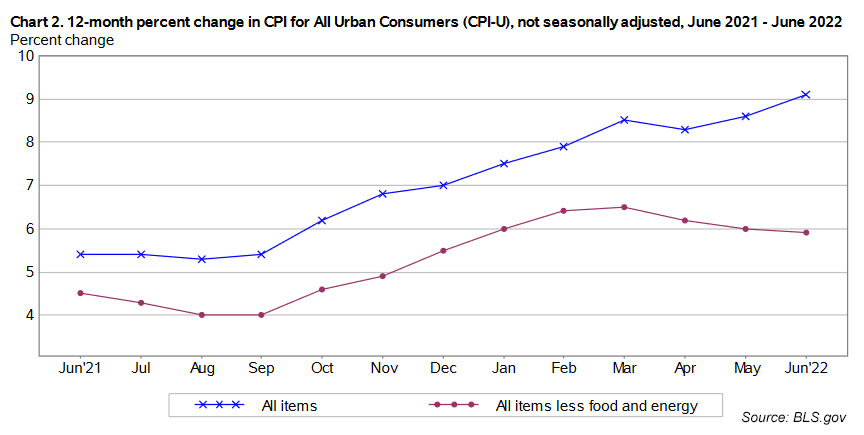

The Consumer Price Index for All Urban Consumers increased 1.3% in June on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 9.1%, the largest 12-month increase since November 1981. These results were much higher than economist expectations, which called for 1.1% for the month and 8.8% year over year.

Core inflation, which eliminates food and energy, also exceeded expectations, rising a disturbing 0.7% for the month (versus a consensus of 0.5%) and 5.9% year over year (versus an expected 5.8%). This surge in core inflation indicates the broad-based nature of U.S. inflation, which looks likely to continue running hot even if gas prices start falling.

The BLS noted that June price increases struck “almost all major component indexes.” Some highlights:

- Food at home costs increased 1.0% for the month, after rising 1.4% in May, and are now up 12.2% year over year. The dairy index rose 1.7% in the month, following a 2.9% increase in May. The sole food group to show a decline was meats and poultry, falling 0.4% in the month.

- Gasoline prices surged 11.2% in June, and were up 59.9% over the last year. This trend seems to have reversed in July, with gas prices falling a bit throughout the month, so far.

- The overall energy index rose 41.6% over the last year, the largest 12-month increase since the period ending April 1980.

- Shelter costs increased 0.6% in June and are up 5.6% for the year.

- The rent index rose 0.8% over the month, the largest monthly increase since April 1986.

- Prices for used cars and trucks continued climbing, up 1.6% for the month.

- Apparel prices surged 0.8% for the month and are up 5.2% for year.

- The medical care index rose 0.7% in June, and is up 4.8% for the year.

- Airline fares fell 1.8% in June after increasing strongly over recent months.

My overall impression is that, yes, U.S. inflation may have peaked in June because we could see gasoline prices begin to fall the rest of the summer. But clearly, even if the annual inflation rate begins to inch down from 9.1%, prices will continue to rise across the economy. Don’t be fooled by any claim in coming months that “inflation is under control.”

Here is the 12-month trend for both all-items and core inflation, showing that core inflation has started to stabilize at close to 6%, an unacceptably high rate:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for all TIPS and set future interest rates for I Bonds. For June, the BLS set the inflation index at 296.311, an increase of 1.37% over the May number.

For TIPS. The June inflation index means that principal balances for all TIPS will increase 1.37% in August, after rising 1.1% in July. For the year ending in August, inflation accruals will have totaled 9.1%. Here are the new August Inflation Indexes for all TIPS.

For I Bonds. The June inflation report is the third in a six-month string — March to September — that will determine the I Bond’s new variable rate, which will be reset November 1. After three months, inflation has increased 3.06%, which would translate to a variable rate of 6.12%. But three months remain, and a lot can happen in three months, especially summer months when inflation is very hard to predict. The I Bond’s current variable rate is 9.62%.

Here are the numbers so far:

What this means for the Social Security COLA

The June inflation report sets a baseline figure for next year’s cost-of-living adjustment for Social Security, but the Social Security Administration uses a different index, Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). For June, CPI-W was set at 292.542, a year-over-year increase of 9.8%.

Does that mean Social Security benefits will increase 9.8% in January? No. the SSA uses the average of CPI-W over the months of July, August and September to determine the next year’s increase. Last year’s three-month average was 268.421, so at this point the increase would be 9.0%. That’s not a projection, because inflation should continue rising through the summer. But it is a starting point. I will be tracking these numbers on my Social Security COLA page.

What this means for future interest rates

I suspect that the Federal Reserve was prepared for this rather disturbing June inflation report, and will move forward with plans to increase short-term interest rates 75 basis points at it July 26-27 meeting, and then possibly again in September.

As we have seen in recent weeks, the Fed can move short-term rates higher, but has no real control over longer-term rates, which have been declining on recession fears. The nominal yield curve has flattened, with the 1-year Treasury trading at 3.18%, the 2-year at 3.18%, the 5-year at 3.11% and the 10-year at 3.02%.

Real yields on TIPS have been holding up nicely, with the 5-year now at 0.53% and the 10-year at 0.65%. I am thinking next week’s auction of a new 10-year TIPS will be a decent buying opportunity.

I wouldn’t be surprised if inflation moderates in the next few months, but continues at a historically high range. The economy is likely to weaken, and the Fed will be under pressure to “declare victory” and stop the rate hikes.

My conclusion: Take advantage of attractive short-term rates (about 2.2% on a 13-week Treasury) and continue to lock in attractive real yields on TIPS. Yes, rates are likely to go higher, but there is always the threat of the Fed backing off and intervening in a weakening economy. We’ve seen it before.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: This week’s 10-year TIPS auction has ‘potential’ | Treasury Inflation-Protected Securities

Pingback: Social Security COLA looks likely to rise about 10% for 2023 | Treasury Inflation-Protected Securities

You have discussed CDs. What are your thoughts on MYGAs, which pay more… and have you purchased? Thanks.

I’ve never invested in a Multi-Year Guaranteed Annuity, but if the fees were extremely low and the interest rate was attractive, I could be interested. Annuities are complex investments and I am not an expert in annuities.

It is like a CD but purchased from a life insurance company and insured by a state guaranty, usually up to 250k. You can get a 4.5 fixed rate from an A rated company right now. Term is 2-10 years. There is no additional fee as it is built into the rate. Also tax deferred.

Do you mind sharing where you see a 4.5% from A rated for 2-5 years….I see it for B++ but not A

Blueprintincome.com shows A rated Americo at 4.5 for 7 years and 4.2 for 5 years. This may vary depending on the state you are in.

Ah thank you for sharing. I need to dig further to see if I am missing something (fees …which I know you pointed out are baked into rate.) but I have been paying extra on a 2.65 mortgage seems like a no brained to switch to this. I really do appreciate you sharing (I had not heard of these before your post) and please let me or us know your plan. My only hesitation is it seems too good to be true.

You might also checkout Income Riders on Fixed Income Annuities. These are designed to take income payments and the payouts like mine are about 7% plus inflation! Depends on goals. These are the do not run out of money schemes you might of heard about. Ken Fisher hates em, cuz he does not get a management fee!

Well, actually there is no guarantee of annuities issued by state governments. In the event of a bankruptcy of an insurance company the annuity is backed by guaranty associations. These are private non-profit companies that are funded by assessments against all of the insurance companies that sell policies in that state. If that non-profit guaranty association were to fail there is no law that requres the state government to step-in and make policyholders whole. Any comparision to the FDIC or NCUA is just totally bogus. In fact, in California only 80% of an the value of an annuity is covered up to a maximum of 250K . That means you’d lose 20% of the value of your annuity in a worse case scenario. Or in this case 50K. That sort of put me off purchasing an annuity in the Californial

To be fair if you have any money invested thru a brokerage account the insurance thru SIPC is structured similarly to that of the annuity guaranty associations. The difference here is that it is regulated by federal, not state law. SIPC insurance covers investors for up to $500,000 in securities and up to $250,000 in uninvested cash. Another big difference is that the SPIC has a 2.5 billion dollar line of credit with the US Treasury. So, it is partially back-stopped by the US government. Of course, if one of the large brokerage firms ever collapsed, that wouldn’t even be enough to cover the loss. Would that fall under too big to fail? Or, is the SPIC a bigger joke than the annuity state guaranty fund?

PS

When comparing annuity rates against CD’s, remember that the annuity payout is also giving you part of your principal back. So, it’s an apples to oranges comparision.

https://www.annuity.org/annuities/regulations/state-guaranty-associations/ No one every lost money due to failure! AIG was too big to fail. Insurance runs the world!

This is a bit off-topic, but since it relates to Treasury offerings, I’m hoping you can offer some comments. In one of the Treasury’s regular announcements about upcoming auctions, I received this today at about 9:45 a.m.: 1-Year 10-Month -0.075% Treasury FRN Auction Announced. I’ve never considered purchasing one of these floating-rate notes before, but as I understand corporate floating-rates they are basically linked to prevailing rates, so when rates rise, these rise (assuming the borrower doesn’t default). This auction takes place today, so this question is really for future reference, but can you explain how a Treasury FRN would work? Or can you point me to a resource? Thanks.

An FRN is a unique Treasury, generally with a 2-year term and a yield that has a slight spread above (or below) the 13-week Treasury, which has a new auction every week. Last month’s auction spread was -0.075%, so the FRN will actually slightly trail the 13-week yield, but it is a 2-year commitment. I was baffled by that, but several readers have noted that the FRN readjusts its yield every week, so you quickly follow along with rising yields. That probably explains the slightly negative spread.

I look at CD rates from 1 month to 10 years on

Fidelity Investments about twice a week. I’ve yet to see ANY CD offered

that isn’t callable

Over 5 years and those that do top out at 3.35 or 3.5% or so….

That supply will dry up once the Fed even hints at a moderation.

6-8 months ago on Fidelity’s site you could look up maybe 1% for 3-5 years.

Not that anyone thinks that is a good idea. I don’t see any non callable CD offerings over 3.5% with a duration longer than 5 years.

That speaks loud enough about where they think long term rates are going.

Kudos to all those who max out the I-Bonds year after year. It adds up.

Im playing this with a 90 day 3 tier ladder brokered CDs These will jump when the Fed raises .75 end of month. Believe the Fed they are going to 5% they said so!

I am doing the same thing but I don’t believe I ever heard the Fed said they were heading to 5%.

I’ll also add that if the 5-year nominal Treasury rises above 3.5% right before the July 26 auction, I might be a buyer.

Just checked the brokered CDs at Vanguard. There are none on the quick search page are over 5 years in length. Rates for the 5 year are 3.35-3.40. None are callable.

Agencies are running 1 year at 3.38 up to 30 year at 4.20. The highest 10 year agencies are listed at 4.90. Most that I looked at from 1 year to 10 year are callable.

I was perhaps naively hoping for a TIPS yield spike after another upside CPI surprise today. But, alas, 5 year TIPS are at 0.47% and 10 year at 0.58% – so the market basically shrugged it off. Why do you think no reaction this time?

So did I. Yesterday, it was at 0.50%. So, I was expecting an upside move today.

Since the yield was actually better today than at the last 5 year TIPS auction, I bought 10K on the secondary market at 0.475%. The amusing thing is even though the unadjusted price was 52 cents lower than the auction, after the inflation factor was included I only picked it up for 4 cents less than the auction. Basically a wash.

I was thinking that inflation also impacts the decision of when to start collecting Social Security. The usual assumption was to wait for as close to age 70 as possible. Since the value of the age factor was considered to be worth more over an extended period than the deferred payments. But since initial benefits are tied to historic earnings, the decision has to be considered whether to get in to start getting those COLAs. I wonder if there is a chart that would illustrate the advantages and tradeoffs of waiting a year and forfeiting the COLA and those years of collecting versus the added benefit of waiting. If the COLA is equal to say three years of waiting, then maybe taking SS earlier would make sense.

I am not sure of the exact rules, but I believe your base Social Security level is set when you reach age 60, and you get the COLA increases even if you delay taking Social Security until age 67 or 70. So delaying has no effect on the COLAs — you will still benefit from them.

I took my SS early to reduce the amount of money I would of had at risk in the stock market equal to the SS income. Take the extra money and put it in a safe investment like Ibonds if you do not need the money!

Social Security is based on the highest 35 years of wages but those wages are inflation adjusted. https://www.ssa.gov/oact/cola/Benefits.html

I read a story on Marketwatch, that cited President Biden claimed gas prices have fallen since June, that is true, and more interestingly, the CPI uses average prices throughout the month, not the end of month price.

Wondering if that is true? Because AAA and other sources post daily gas prices, nationally. So it is easy (for these companies at least) to get month-end prices.

As to lower gas prices, they have gone down since the peak, but are still up almost exactly 50% from a year ago, the same as my recollection in May.

https://gasprices.aaa.com/

Gas prices in my area (North Carolina) appear to have fallen about 20 cents a gallon this month, a drop of more than 5%. So that should be help keep a lid on July’s monthly inflation. The Cleveland Fed is “nowcasting” an inflation rate of 0.39% for July, but has core at 0.48%, an indication of falling gas prices. https://www.clevelandfed.org/en/our-research/indicators-and-data/inflation-nowcasting.aspx

Re the Treasury’s short-term rates, today’s auction for a 119-day (about 4 months) bill was 2.60%. Last week’s yield for the same term was 2.23%. These things are hard to pass up! I’ve bought several over the past few weeks as rates have steadily been jacked up.

Do you think the fixed rate portion of the I Bond interest rate will increase from the current 0% when adjusted in November? Or maybe a better question is: what methodology does Treasury use to determine the fixed rate?

The Treasury has no defined formula for setting the fixed rate and doesn’t give any guidance. My observation is that the fixed rate will tend to lag 50 to 60 basis points below the 10-year TIPS real yield. Right now the 10-year real yield is 0.64%, so the Treasury could raise the fixed rate a bit in November. However, because the demand for I Bonds will still be so strong, it may not make the move.

Thank you.

Dumb question: Does this mean the absolute minimum for the next I-bond variable rate is 6.12% (annualized)? For instance, can the next inflation index be lower than the current one (highly unlikely I know)? If so, would that being the variable rate down from 6.12% (annualized). Apologies if this has been answered before.

No, the 6.12% indicated rate could change a lot before the final September inflation report. Yes, it could go lower. If we have some months of deflation from July to September, the six-month inflation rate could be lower than 3.06% and the variable rate would then be lower.

Thanks so much! I know that the value of I-bonds can’t go down, but wasn’t sure if the intermediate numbers could go down before they were “officially” published every six months. Of course, I don’t think any of us are expecting that to happen.

“but has no real control over longer-term rates”

Well, I beg to differ. The FED could get serious with regards to reversing QE.

So far, they’ve done diddly with regards to that.

This inflation report just shows that the FED has hardly any control over inflation.

Continued COVID lockdowns in China and the war in Ukraine being the primary causes.

On the margins, the FED can attempt to control the affects of labor shortages.

But as the latest employment report shows, it’ll take a recession to do that.

In the meantime, the conditions are a perfect opportunity to load-up on TIPS.

As you said, how long that window will last remains open to question.

However, inflation over 9% kind of ties the hands of the FED for the near future.

Hopefully, we won’t see an erosion of the TIPS yields right before the next 10 year auction.

Since that’s only a week away, that probably won’t happen this time around.

The FED can jawbone all it wants but it can’t dance around 9% inflation.

With this kind of inflation, I may even fill-in gaps in my TIPS ladder from the secondary market.

Usually I’m loathe to do this, but 3 and 4 year terms probably won’t be affected by deflation.

At least not as much as how CD’s will be adversly affected by inflation over the next few years.

But then, I’ve been wrong before.

Who saw 9% inflation coming during COVID.

Like nobody.

Yes, the Fed definitely had strong influence on long-term rates when it wanted rates lower, by buying billions of Treasurys every month. Now it is simply letting maturing Treasurys roll off the books and not reinvesting. But this is actually much more aggressive than the very weak response from the Fed in 2015 to 2018, when it barely lowered its balance sheet. Of course, inflation wasn’t a big problem from 2015 to 2018. I think the Fed knows a recession is all but certain, but it could never say that.

When the yields go down on Ibonds, will be time to switch to CDs, the yields will be way up!

I disagree, because of the $10,000 purchase limit on I Bonds. It takes many years to build up a sizable allocation in I Bonds. My recommended strategy is to 1) buy them every year up to the limit, if you can, and 2) hold them until you really need the money, or 3) hold the 0.0% fixed rate I Bonds until you can roll them over to a higher fixed rate.

I Bonds will be paying a very attractive rate of interest over the next 12 months, but that won’t last forever. People who bought I Bonds in the past, over many years, are very happy to see this inflation hedge doing exactly what is needed in July 2022.

But I do think I Bonds have attracted a lot of short-term investors looking to collect 7.12% interest, then 9.62% interest and then … whatever the next rate will be (likely higher than CDs). That was their strategy and its a fine strategy if you need I Bonds for a short-term investment.

its only worth keeping them over the long haul if they got some fixed rate. Those with some fixed rate that held for 20 yrs the rate of return is about 4% annually, just a little more the my fixed rate! So really not an investment, just a place to park cash. I be dumping my no fixed rate ibonds and put em into higher yield CDs when the cross happens. There will be a time where interest rates work jacking up CD rates and Ibond inflation rates will fall. Ill keep the old ibonds with a fixed rate, do not want to pay big income tax bill!

Of course, everything depends on the financial goal that you want to accomplish. If maximizing yield is the goal, then iBonds and TIPS aren’t a very good investment. If protecting the assets you’ve accumulated is the goal, then iBonds and TIPS really can’t be beat (especially for protecting the value of retirement assets).

Up until this year, in 50 years of owning CD’s and nominal Treasuries, I had never lost a cent to inflation. Even during the inflation of the 1970′ and early 1980’s I was able to beat inflation handily. Heck, I could marginally beat inflation with just a 3 month nominal Treasury. In fact, the 3 month Treasury was a proxy for inflation before TIPS came along.

So, good luck with beating inflation with CD’s. The best 5 year CD’s currently being offered are in the pathetic 3% range. That’s a 6% loss to current inflation. Even if CD rates reach 4% and 5% in the near future, they’re still going to be losers until inflation reaches 4% to 5%.

Of course, all of this is the result of ZIRP and QE. Those policies have been eroding the intrinsic value of CD’s and nominal bonds for years now. Even TIPS suffered thru several bouts of negative yields as auction. I can remember when financial experts would joke about the fact that anyone mentioning that possibility was basically a Chicken Little.

No one is advocating this is your total portfolio! I try to maximize the return within the scope of each allocation, not try to have everything do everything! Market returns, not your cash, in the proper amount through off excess gains to offset some minor inflation loses in your cash portfolio. I have 40% in the market and 60% cash/cash like. My 40% yields 10% and the 60% cash(Ibonds,MM,Cds) yield about 2.49%. Also some of this cash goes in and out of the market for a quick double, like Covid and when the current market crashes! Whos portfolio is the closest to keeping up with inflation this year, the one with the cash. Just hoping the market positions come back to even is not much of a plan! Think its gonns be another lost decade! A big chunk of cash lowers your beta (drawdown). My portfolio is only down 7% right now. Cash is king! How is being down in the market maybe 30% help you with inflation today? Good luck with that plan!

I’ve always used them as a source of dry powder and second tier emergency fund. So in the event I need to buy a new home, or a natural disaster happens, I have a source of cash readily available. The hope is, of course, I don’t need it, although if home prices actually drop I may take advantage and use it as a down payment.

Thank you.