The outer shell is new, information is easier to find, more clearly presented. And then … same old, same old.

By David Enna, Tipswatch.com

If you’ve visited everyone’s favorite financial website — TreasuryDirect.gov — in the past few days, you might have noticed an important message on the homepage: A redesign is coming! And today … it launched.

The TreasuryDirect site is almost universally ridiculed, especially by new investors who have been piling in recently to load up on U.S. Series I Savings Bonds. I’ve been using this site for about 20 years and I’m comfortable with its quirks. But I still tell people, “It will remind you of MySpace.”

To be honest, the site never bothered me much. I used it. Most of the time it worked. I knew where to go and do what I had to do. But that came from 20 years of using it.

The biggest complaints I hear from readers concern difficulties in account creation and logging in, and unfortunately, the new design does nothing to solve those issues (at this point). Is more coming? I can’t say because TreasuryDirect has not formally announced the redesign. Its news section has no items posted in October and no mention of the redesign.

“Improving the front-end informational pages on TreasuryDirect.gov enhances the user experience by helping customers more easily find the information they’re looking for and improving the website’s information quality, appearance and usability,” a Treasury spokesperson told CNBC.

CNBC also noted the Treasury said it has “more than doubled call center resources and made other technical enhancements” in response to investors struggling to get answers on the site.

Let’s take a walk through the new look … and the old look hidden inside:

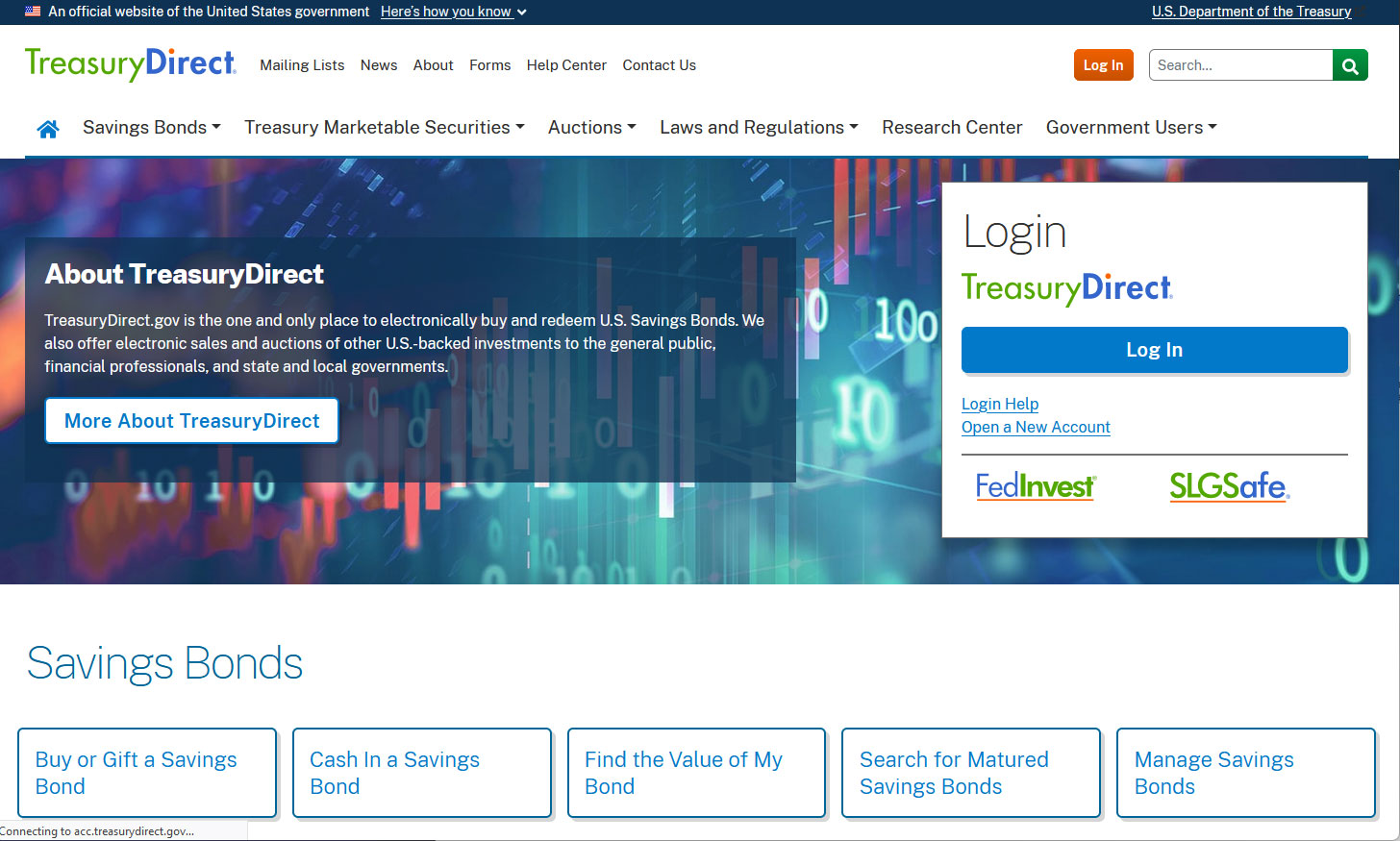

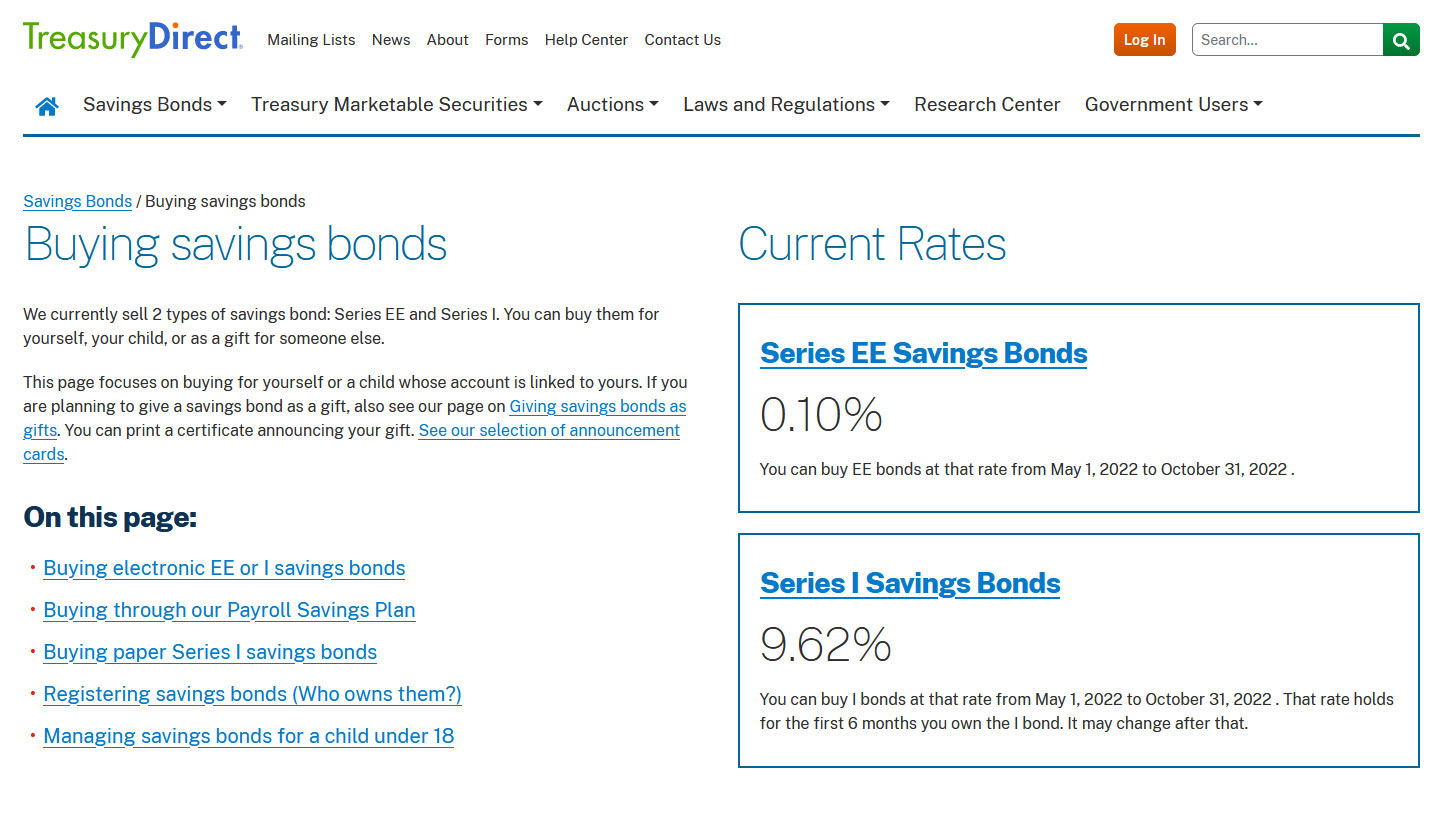

The new homepage

I worked on a newspaper website for more than 20 years, and my impression of this design is that it is unfocused and needlessly busy. But on the positive side, the type is larger and I like the font. I love the very prominent presence of Savings Bonds links “above the fold.” This shows a strong commitment to the Savings Bond program.

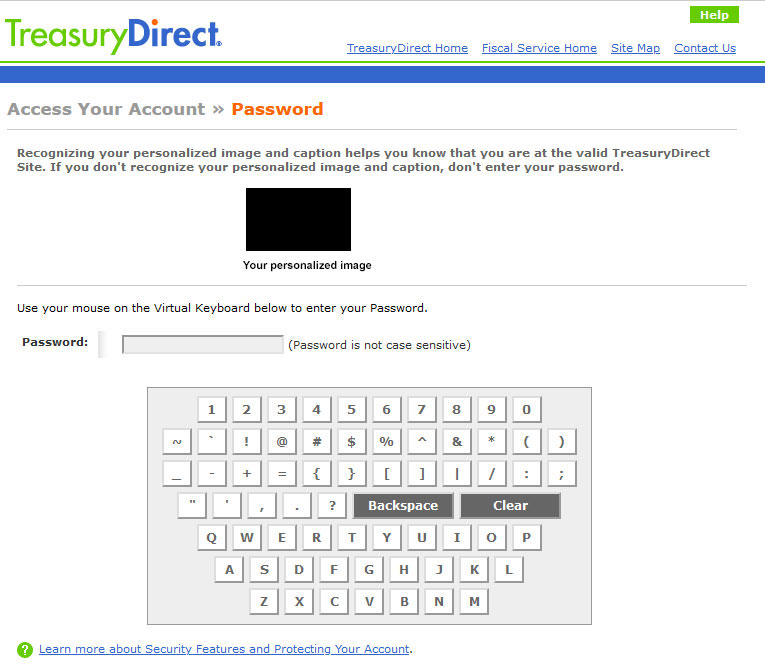

The login page

Hey, that looks familiar! Yes, you jump back in time to the old site design’s login page, which is probably a good thing. It works exactly the same way, meaning you won’t have to reestablish credentials to log in to your account. After you enter your account number, you get this:

It’s the virtual keyboard, and TreasuryDirect is the only site I have ever seen that uses one. This login method triggers hilarity around the financial internet, but I am saying: I LIKE IT. TreasuryDirect is taking this step to keep your password safe from keystroke tracking spyware, also called “keyloggers.” I want TD to take every step possible to protect my account.

Account summary page

Again, this is a holdover from the old site. And there at the top is the “important message”: Do not use your browser’s back button on TreasuryDirect. If you do, you will be bumped out and have to log in again. Instead, use the “return” button at the bottom left of each page. Not sure why this is necessary, but it is what it is.

The back button issue only applies when you are logged into TreasuryDirect and looking at your account information. The back button works fine everywhere else on the site.

The BuyDirect page

Again, this is exactly as it was on the old site. No changes.

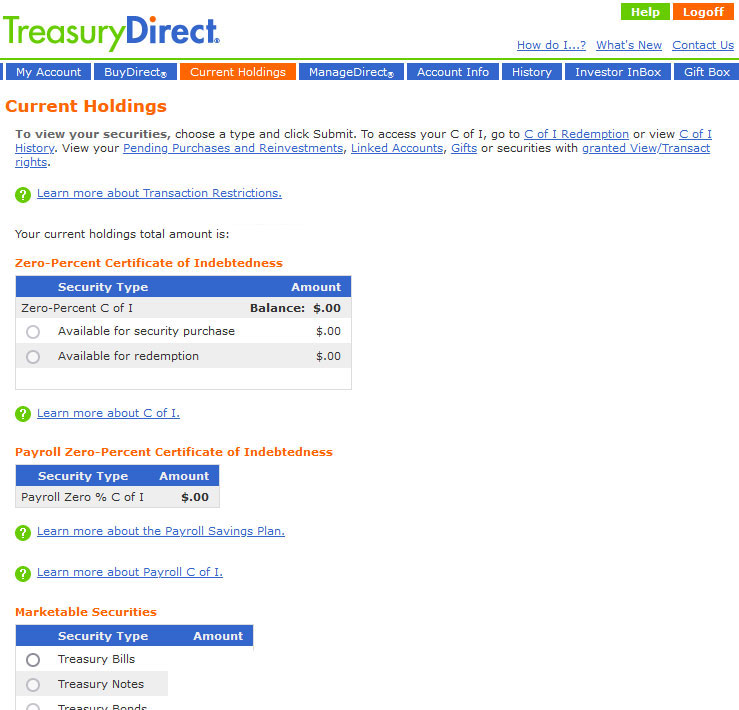

Current Holdings page

Nothing new here. Same as always.

So what’s new?

The folks at TreasuryDirect have been working hard to improve the site as an “informational” resource, creating new, more scannable guides to buying Savings Bonds, for example. Some screenshots:

—————————————–

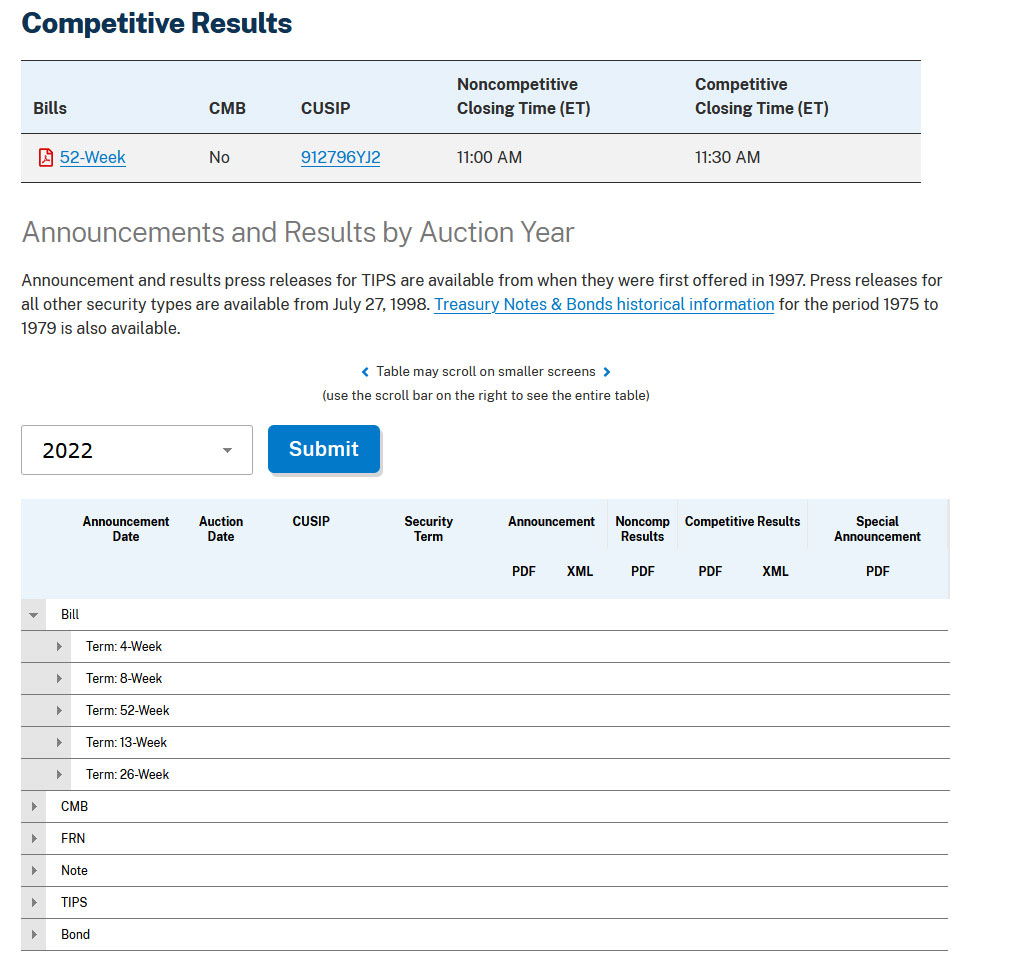

Auction results

I use TreasuryDirect several times a week to check on auction results for TIPS and T-bills. The same functionality is on the new site, but the look is updated. This morning, when I tried to see the 1-year T-bill auction result, I got nothing. The page never finished loading the results portion, which also happened often on the old site. Later, it worked. I would really like this to work, every time. This is the opening page.

Click on Today’s Auction Results, and you get this, when it is working:

Inside the auction results section there is a nice guide to TIPS/CPI Data, which was probably on the old site — I must have used it — but I couldn’t have found it easily. (TreasuryDirect emails me the new TIPS inflation indexes a few minutes after the release of each monthly inflation report, so that was my reliable source.)

A revamped mobile site

I have to admit that I have never — not once — tried to view TreasuryDirect on my iPhone. I guess I figured it would be hopeless. But now the site’s opening and informational pages have been revamped to be more mobile-friendly. I guess. I still won’t be using the mobile site. Here’s the opening page:

It’s probably worth a look for any of you who use TreasuryDirect on you phones.

What do you think?

Take a look around the new TreasuryDirect.gov and post your impressions in the comments section. If you find anything really new, interesting or helpful, let us know!

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you for alerting us about the update. Curious, have they made it any easier to add new bank account information? Last time I checked, they wanted you to make the request, only via mail. I don’t have enough confidence in the security of sending documents via the USPS, to do that. Don’t understand why we can’t provide the information online.

I have read that this is a priority for the Treasury, to ease updates to account information. But obviously, security is a huge factor in their decisions, so we will have to be patient.

The old site always worked for me and I could login at least. The new site worked right after launch, but not will not allow me to login and has been this way for several days now. Many others have the exact same experience and cannot login. You actually do “login” and then it asks you to verify your information on file. Whether you click Cancel or Verify at this point (only options), it then sends you to a “TreasuryDirect is unavailable” and “We apologize, please try again later” error page.

For me, the new application is broken. I can login, but then I get to a verify page for my email address. I click verify, then it tells me my account is unavailable. Calls to customer service were not helpful. By the way, I called customer service at exactly the time they opened and still had to wait 40 minutes. Its like they need 30 minutes to get their coffee or something.

I know that things are still changing within the site, could this be a temporary problem? Or are you getting stuck at the two-factor authentication page? Is it possible you previously used a different email address?

Thanks. It is the same e-mail as I have been using for years. There is a page that pops up occasionally that asks you to verify address, phone number, and email. It is after the two factor and password. You click verify and your get a message that your account is unavailable. You click on any links on that page and it takes you to a broken link page. So it must be a legacy page that isn’t fixed yet and my bad luck for hitting it now. The verify page only comes up once in a blue moon. Unfortunately customer service was no help with the issue.

And the problem has been going on for several days. I am used to TD being down for a few hours, but several days seems too long. Tried other browsers / computers with no luck.

This is not just a problem he is having. I am having this problem too and so are many other users that never had a problem with the old site. You “successfully” login but then it asks you to verify your personal info. You can only click “Verify” or “Cancel”. No matter what you click, it sends you to that “TreasuryDirect is Unavailable” error page and you cannot login. I’ve seen dozens of other people on message boards and comment sections who never had trouble with the old web site describing the exact same problem with the new site and it just started recently in October, but many of us did not have that problem when the new site initially went online.

The technical person said it was a problem with last Sunday’s rollout. I am a programmer so we talked a bit of shop. Insist on getting transferred to a technical person. The first level customer service are not very knowledgeable.

Sorry. Absolutely no improvement in the look, feel, or operation of the account website. Like being in the 90s only worse. But who can refuse a safe investment that pays 9%+….

While 9.6% is currently impossible to beat for any U.S. fixed income security, let’s realize that even that rate does no more than provide some, but not total, protection of principal, and no return ON the principal, because of the current zero fixed rate component of the composite I Bond rate. “Some,” because that 9.6% “return” is, in most cases, subject to federal income tax, though most people will defer the taxes until they redeem the bonds. In effect, we are taxed on principal protection rather on any return “on” our savings, so effectively we do not have complete inflation protection.

All true. Of course, all other safe investments will return less than inflation after taxes, at this point. It’s possible that locking in a very good nominal, longer-term Treasury could have a return greater than inflation after taxes, if inflation slips to very low levels. I Bonds will track inflation. TIPS will beat inflation by about 1.5% over their term. TIPS might be a good option if this is your concern.

My problem with TD was resolved. I had to nag them for a couple of days. They introduced a change last Sunday, Oct 9, that broke some code. This is the first major problem I have had in about 20 years of using the app. I am not to crazy about the first level of customer service. I had a 40 minute wait each time I called. And at the moment they ignore all emails even if you add your case number. When you can get them to transfer to technical support, the service is much better.

Hi Jack, I have the same issue. How did you get it resolved?

I had to call them twice. Both times I had to wait 40 minutes in queue even though I called at exactly 8am ET. And they shut off the queue around noon from all the calls. The technical people know all about the problem, but customer service seems to have not gotten the word. I would wait until Monday to see if they rolled out a new fix.

Thank you Jack. I waited until Monday (today), and I was able to get through.

I wish I could get through. I’ve been on hold for 3 hours and 11 minutes so far. I’m afraid to hang up because then I’ll need to wait on hold another time.

Were you able to fix this or did they have to do something on their end? I and many others are having the exact same problem you describe.

Treasury Direct had to do something for my account to get past the Verify Information page. It was a pretty fast fix, so it may have only been for my account. After I talked to the actual technical support, she seemed to know exactly what was wrong. Someone called me back in a couple hours and I was able to click on Verify and get to my regular account.

Pingback: A nostalgic look back at TreasuryDirect’s ‘decoder ring’ login system | Treasury Inflation-Protected Securities

I remember a time when logging into the Treasury Direct web site required the use of an Access Card, which had a grid of random letters and numbers printed on it. In a sense, it was a form of MFA (multi-factor authentication). But I could never get over how much that card reminded me of a secret decoder.

Is a medallion & signature still required in a random basis for I-Bonds purchased by trusts?

No not required; I did the trust purchase earlier this year. HOWEVER, in both cases the accounts were not easily opened; instead I needed to fill out the dreaded form 5444, Treasury Direct Account Authorization, which must be signed/approved by a bank officer (not a notary). Then you MAIL it to Treasury, and they take 5+ weeks to approve and release your account to add $.

The new TD web site is okay, nothing to get very excited about. I needed some questions answered about some savings bonds issuing problems and got this message:

“Due to heavy volume, we are temporarily limiting communication by e-mail. For us to respond to your e-mail, it must concern a pending case and it must state your case number in the subject line of your e-mail.”

This sucks. This of course makes it more difficult for citizens to use TD if you need to speak to a human. I used to be able to phone up and get an agent to answer pretty quickly. I’ll try to phone again tomorrow. All I get is a busy signal today.

While one would hope the Treasury will see fit to at least begin to resume offering a fixed rate component that is in line with, say, 30 year Treasury Bond rates, the question of course is: at what cost to the Treasury (i.e. the government)? It also raises wider questions, such as, what are Treasury’s plans about the future role these bonds should play in Treasury financing operations, given the highly volatile and uncertain dollar cost of interest payments based on inflation, as well as the unknown variables of what the future volumes and timings of new I-Bond purchases and redemptions of existing holdings will be? Suppose a new fixed date of 1.5% becomes effective on November 1. Given that so many people have already purchased their maximums this year, how many people are even eligible to make new purchases before next year? What will happen if inflation drops sharply between now and April next year, reducing the inflation component of the rate effective May 1 next year, and if inflation continues to drop after that, how many bond holders who purchased at least 12 months ago will prefer to redeem their bonds and switch into the new issues that provide a return on top of inflation, or exit their bonds altogether?

It is highly unlikely that Treasury would raise the fixed rate higher than 0.5% on November 1. For people who have already purchased a full allocation in 2002 (almost all of us) the new fixed rate, combined with the new variable rate, will be available for purchase on Jan. 1.

Since I Bond purchases have increased 100-fold in the last two years, I am sure a large number of the new buyers are in this for the short term. They will be moving on when inflation eases off or competitive interest rates rise. For example, TIPS yields are now quite a bit higher than the current I Bond yield.

My uncle asked me a simple sounding question recently but I realized I didn’t know the answer….Suppose I want to bid in the next TIPS auction and want to buy a total of $50k, all thru TreasuryDirect. Is it possible to split this up into various smaller amounts (like $20+$20+$10k, or $10k*5, etc), or are we only allowed to bid one amount per auction per TD account? And does the same apply to all other securities auctioned in TD? Thanks!

I’ve never seen this question before. Why split the purchase into separate amounts? Are you planning to trade these in the future? If you are planning to trade, I advise making the auction purchase in a brokerage account. Or, do you want to make separate registrations for each with different beneficiaries? That would be a logical reason to do this.

If you want to try the separate purchases, make one for $20K and see if you can add another. I expect that you will be allowed to add on to the first purchase and change the registration if that is what you want.

I usually break-up my auction purchases so that I can cancel part of it easily if the yields at the auction fall below what I want.

For example, back at the June 5 year re-opening I broke-up a 50K purchase into 5 10K orders.

As the yields sank on the morning of the auction, I started cancelling some of the orders. I ended-up only purchasing 20K that day.

It would have been difficult to cancel the 50K order and then try to enter a new one before the auction cut-off.

However, I do this thru brokerage, not thru Treasury Direct. The only thing I have there is iBonds.

Excellent info, thanks

David and Jimbo, what is the best way to monitor this live and what is the cutoff for changes? Thanks.

Sorry, I don’t know what the cutoff time is. If you want to watch trends in real yields, look at the Bloomberg Real Yields page for real time estimates. That won’t be totally accurate for a new issue (and the auction results may differ anyway) but you can see the trend if you look a few times on the morning of the auction: https://www.bloomberg.com/markets/rates-bonds/government-bonds/us

It’s a mix of the reasons you mention. My uncle was interested in 7 year notes but, besides naming different beneficiaries, wanted to know if he could sell only some of them early in case he needs the money before maturity. He doesn’t have a brokerage acct so was hoping to do it all thru TD. Anyway I might just help him try it and see if it works, starting with a small amount.

You cannot sell Treasuries at TD. If you want to get out before maturity you have to use a broker. It’s best to use a broker for Treasury purchases anyway. Most do not charge a commission.

Remember you can only buy and sell savings bonds through TD.

“To sell a Treasury marketable security, you must work through a bank, broker, or dealer.” -TD website

oh by the way, if you are as annoyed by the Virtual Keyboard as I am – hit F12 on the password field and remove the the read-only attribute…

Security through obscurity is never good. They should have implemented MFA…

This sounds exciting, but I’m not an HTML programmer. Would you mind sharing >exactly< what steps to follow after using F12 to open the HTML editor? I don't see a line that says "don't let this fool type or paste into this box." Thanks!

In Chrome, right click on password field – select “Inspect”.

On the right side in inspect window you will see : readonly=”readonly”

Remove it by clicking in that field and deleting the words. The world is your oyster now.

Okay but I’m using Firefox — but with your clues I was able to figure it out and it worked; I used copy/paste to stick in the password and I was in my account! Joy!! But I was was so excited that I decided to go through the steps again and post them in this very reply. But I can’t find the same code string from which I was able to delete “readonly” or something like that. I’ve been fiddling around trying to relocate it for 15 minutes, and I’m giving up. I’ve been using the hunt-and-peck system for 5 years and I guess I can continue to do so.

once you edit the code, just hit reload in your browser to discard your edits. or shift-f5 for full reload

Virtual Keyboard – what a idea! Making me type 15 mix special character from LastPass window that I had to unhide.

Protecting me! From what? Someone selling my bond and sending money to my account? Buying more bonds for me?

Or may be its protection from someone trying to change my banking account information to steal my money? Well, they would be fools because to change your bank you need to: mail a Bank Change Request Form FS 5512 E . That needs to be signed by an office of the bank with a bank seal…

Fooled me as well when I used an account I planned to close to fund my purchase and now I cant buy more until I mail the damn form…

Totally agree. The virtual keyboard means you cannot use a password manager on this site – which all experts recommend to use complex passwords and keep you safer. Typing in a complex password using that thing is a pain – I wonder how many use a “simple” password just for TreasuryDirect as a result.

This may be absurdly obvious (“Hey, Bob, this guy says he cracks open the egg and pours the insides into a pan instead of eating the whole thing! I’m gonna try that!”) but I use a password manager with Treasury Direct by copying the password into MS Word and shrinking the Word and browser windows to half-screen, so I can see the complex password as I painfully hunt-and-peck it in.

Not “all experts” recommend password managers.

Over the years, a number of those outfits have been hacked.

This retired IT guy has a mnemonic method stored in his head.

Thats for both user id’s and passwords.

Heck you’re better off having it on a piece of paper.

That’s two level security.

First, someone has to break into your house.

Second, that same someone has to find where it’s hidden.

That’s a lot better than entrusting your passwords to a third party.

That doesn’t mean that you can’t get hacked.

It just makes it more unlikely.

https://dpl-surveillance-equipment.com/cyber-security/which-password-managers-have-been-hacked/

there are about a 1000 entries in my LP, one day I will go all mnemonic on them. In the meantime I will write them down on piece of paper and have that bag with me anywhere I travel. I will also make a copy for my family so they have a thousand more pieces of paper to go through in case of my demise.

May be one more stack to put in a safe-deposit box in case of fire?

While I stock up on paper to make it happen, I am going to continue using LP with MFA combination of Google Auth and Ubikey.

Well, Lastpass certainly has a checkered history with regards to security breaches.

When Wikipedia lists 7 known hacks in the last decade, that’s not too encouraging.

The last one was detected as recently as August of this year. Their development server was hacked.

The thing that really bothers me about password managers is that most financial institutions encourage their use.

However, those same financial institutions have disclaimers about sharing user id’s and passwords with third-party sites.

At far as financial institutions go, Regulation E is the firewall for protecting your accounts.

Whether the bank disclaimers actually allows them to avoid their liability under Regulation E is open to debate.

That’s pretty much the case for all of this third-party financial software. There is no governing case law.

All of the financial institutions want you to use third-party software to make life easier for them (like esignatures).

But then, buried in the fine print somewhere, are attempts to avoid any liability if one of their third-parties causes you to get hacked.

The bottom line is that you audit your financial accounts upon each statement date, you can limit or avoid any liability.

That’s why I’m getting cold feet about purchasing iBonds from Treasury Direct (again). You have no legal protections there.

Wikipedia.

https://en.wikipedia.org/wiki/LastPass#2011_security_incident

Lastpass.

https://blog.lastpass.com/2022/08/notice-of-recent-security-incident/

I’m a LastPass user, too, but I don’t have my TD account password in there, probably because of the virtual keyboard. But LastPass is great because it does remember our two account numbers, so I don’t have to go looking those up each time.

Back when I created my TD account you could do all sorts of things online. Actually, I thought that they allowed too many things.

When I created the TD account I made sure that I had a secondary bank account just in case there was a problem with the primary one.

At that time, you could just toggle between the two bank accounts without any paperwork involved (don’t know if that’s still allowed).

Requiring the change or addition of banks accounts via the route you described is actually a great security feature.

There’s nothing like a paper form that has to be signed and one’s identity verified in the presence of a bank official to deter fraud.

This is especially true considering that it doesn’t appear the the TD ETF transactions are covered under Regulation E.

I have to admit that this does give me pause for using TD for purchasing iBonds (especially with TIPS yields positive).

If your TD account is hacked TD’s Terms and Conditions doesn’t provide any legal recourse whatsoever.

Click to access CFR-2013-title31-vol2-part363.pdf

§ 363.17 Who is liable if someone else

accesses my TreasuryDirect ® ac-

count using my password?

You are solely responsible for the

confidentiality and use of your account

number, password, and any other

form(s) of authentication we may re-

quire. We will treat any transactions

conducted using your password as hav-

ing been authorized by you. We are not

liable for any loss, liability, cost, or ex-

pense that you may incur as a result of

transactions made using your pass-

word.

[72 FR 30978, June 5, 2007]

I like the old way just fine. Tell the millennial to grow up and consider the security a favor. Never had a problem.

I have used TreasuryDirect for 20 years, my wife also. We have purchased I and EE Savings Bonds, Treasury notes, bills, bonds and converted our paper bonds. Purchases, redemptions and reinvestments work extremely well and you can easily set up repetitive purchases for up to 5 years. Really what’s not to like. I like the new website, information is more easily obtained. You can even subscribe to an email service to announce future Treasury Auctions and Auction results (send out shortly after auction completion). You have multiple funding and redemption options. Honestly, this site is fantastic and the Treasury Department has my gratitude for a site that allows meto buy, hold, redeem, reinvest and withdraw funds without issue for the ladt 20 years at absolutely no cost.

Other than the tax refund route, it’s the only game in town for savings bonds. The downside is that Regulation E doesn’t apply to the Treasury.

Is it better to buy Treasury TIPS or Notes through Treasury Direct or through brokers like TD Ameritrade. TD Ameritrade claims that they do not charge any fees to purchase the Treasury TIPS or Notes at the time of auction.

If TD Ameritrade does not charge any fees at the time of auction, wont it be better to buy through them as they would provide a secondary market in case one has to sell it?

If you want to buy a TIPS in a tax-deferred account (which is recommended) then you have to buy through a broker. Also, if you think you won’t hold until maturity, buy through a broker. If you are buying in a cash account and definitely holding to maturity, TreasuryDirect is a fine option. It won’t show you the current market value, just the redemption value, and if you are holding to maturity that’s fine.

Hi,

TreasuryDirect does not show the “redemption value” it shows

CUSIP #:

Security Type: 9-Year 10-Month TIPS

Par Amount:

Inflation-Adjusted Value: as of 07-15-2022

Price per $100:

Investment/Interest Rate:

Even more important – increased customer support!

The interface was confusing but the most egregious issue was removing money from your account THEN checking to see if you had exceeded your yearly limit for I bonds. HAVE THEY FIXED THIS??? It took 6 months to issue a refund not the quoted 8 weeks.

Very clunky! Accidently closed an open tab and had to sign back in. Found a File Not Found in about five more clicks! I hope it is a work in progress! And I hope it doesn’t dissuade people from completing their October purchases to lock in that 9.62% for six months!