By David Enna, Tipswatch.com

I am writing this posting after just arriving in Zadar, Croatia. My time is short, so I will need to be brief this month.

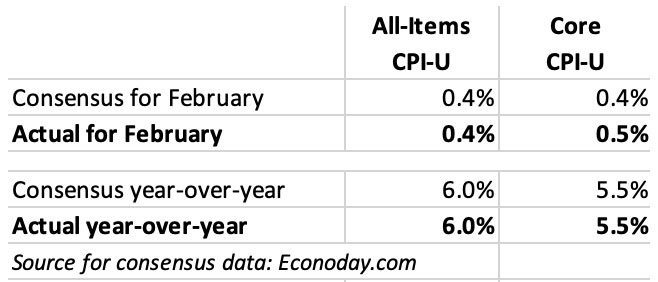

The Consumer Price Index for All Urban Consumers rose 0.4% in February on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 6.0%. Those numbers matched consensus estimates, but core inflation ran slightly higher than expected, at 0.5% for the month, versus the estimate of 0.4%.

The index for shelter was the largest contributor to the monthly all items increase, accounting for over 70% of the increase, the BLS said, with the indexes for food, recreation, and household furnishings and operations also contributing.

This report ended up close to expectations. The shelter index continues to run hot (up 8% for the month and 8.1% for the year), but this is a lagging indicator and should begin sliding lower in future months. The annual increase in the all-items index of 6.0% was the lowest 12-month increase since the period ending September 2021. The core increase of 5.5% was the smallest since December 2021.

Gasoline prices were up 1% for the month, but have fallen 2.0% over the last 12 months. Food prices were up 0.4% for the month and 9.5% for the year.

Here is a one-year look at trends for all-items and core inflation, showing the gradual decline in core inflation versus a steeper decline for all-items:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds.

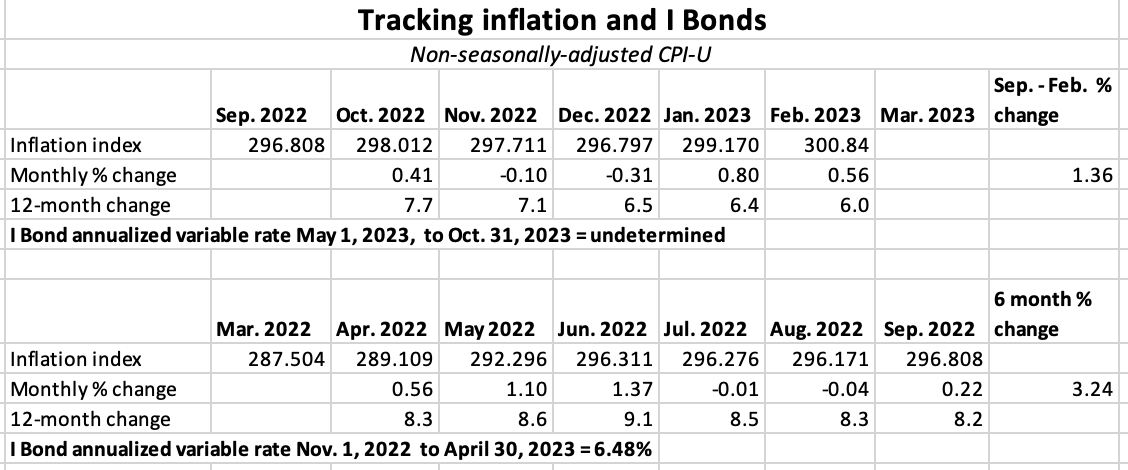

For February, the BLS set the inflation index at 300.840, an increase of 0.56% over the January number and 6.0% year-over-year.

For TIPS. The February inflation report means that principal balances for TIPS will increase 0.56% in April, after rising 0.80% in March. Here are the new April Inflation Indexes for all TIPS.

For I Bonds. February is the fifth month of a six-month string that will determine the I Bond’s new inflation-adjusted variable rate. Through the five months, inflation has run at 1.36%, which would translate to a variable rate of 2.72%. One month remains, so it looks like the new variable rate should fall into a range of about 3.2% to 3.5%, down substantially from the current 6.48%. The I Bond’s fixed rate will also be reset May 1, but the outlook for that reset is highly uncertain, given the volatility of real yields over the last week.

Here are the relevant numbers:

Sorry, but this is all I have time for on this busy travel day. I hope to post more later this week.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I think I will buy at the end of April and withdraw some 0% I Bonds which are seasoned to pay down the HELOC. While I am willing to pay 7% on a loan if I have equivalent funds earning 6% or more, I am less willing to do that if the equivalent funds are earning 4% and the spread is 3% or more.

Thanks and safe travels. If at all possible, see Plitvice National Park. It is truly awesome.

The variable rate on iBonds seems like it will be just high enough to make selling my 0% fixed to buy either TIPS or iBonds with a positive fixed component a more difficult decision. I wonder how long one would have to hold to break even? My quick math says just over 2 months if buying the current 0.4% fixed iBond…

I hiked in Plitvice Lakes National Park today, just 2 weeks after the big snow melt. It was sensational. In your calculations, make sure to figure income taxes owed. That would lower your return.

Correction – I see I am still collecting the 6+% so my window for considering selling isn’t until September.

Thank you for taking the time to post this update.

So, if you purchase an I Bond before May 1, you get 6.89% annualized for the first six months and possibly 3.5% annualized for the second six months. Averaged together, you could be looking at a 5.2% annualized return for the first 12 months (while always getting the 0.4% fixed rate above inflation in future years).

With treasuries dipping recently due to the SVB collapse and lower expectations for future interest take hikes, I Bonds could still be the better short-term investment.

By my calculation, if next month’s CPI comes in at 5%, that’ll be m-o-m of 0.35% resulting in a new variable rate of 3.42%. (Current Cleveland fed inflation tracker is estimating 5.22% for next month so it’s a little conservative).

With 0.4% fixed rate before May 1st, that’ll result in 6.89% for 6-months and 3.82% for 6-months, averaging 5.35% over 12 months. That’s better than current 1-yr treasury. I’m likely to pull the trigger this month (or latest after April 12th CPI once we know next 6 month variable rate for certain). The 6.89% is too good to pass up even with a possibility of a higher fixed rate starting May 1st. The breakeven would likely be several years, but I haven’t computed that yet.

short concise posts are great! Thanks.

Thanks so much for taking the time to add this quick update while traveling! Short and concise and answered my top of mind “impact on ibond projections” questions 🙂 Appreciate your insights, as always.