By David Enna, Tipswatch.com

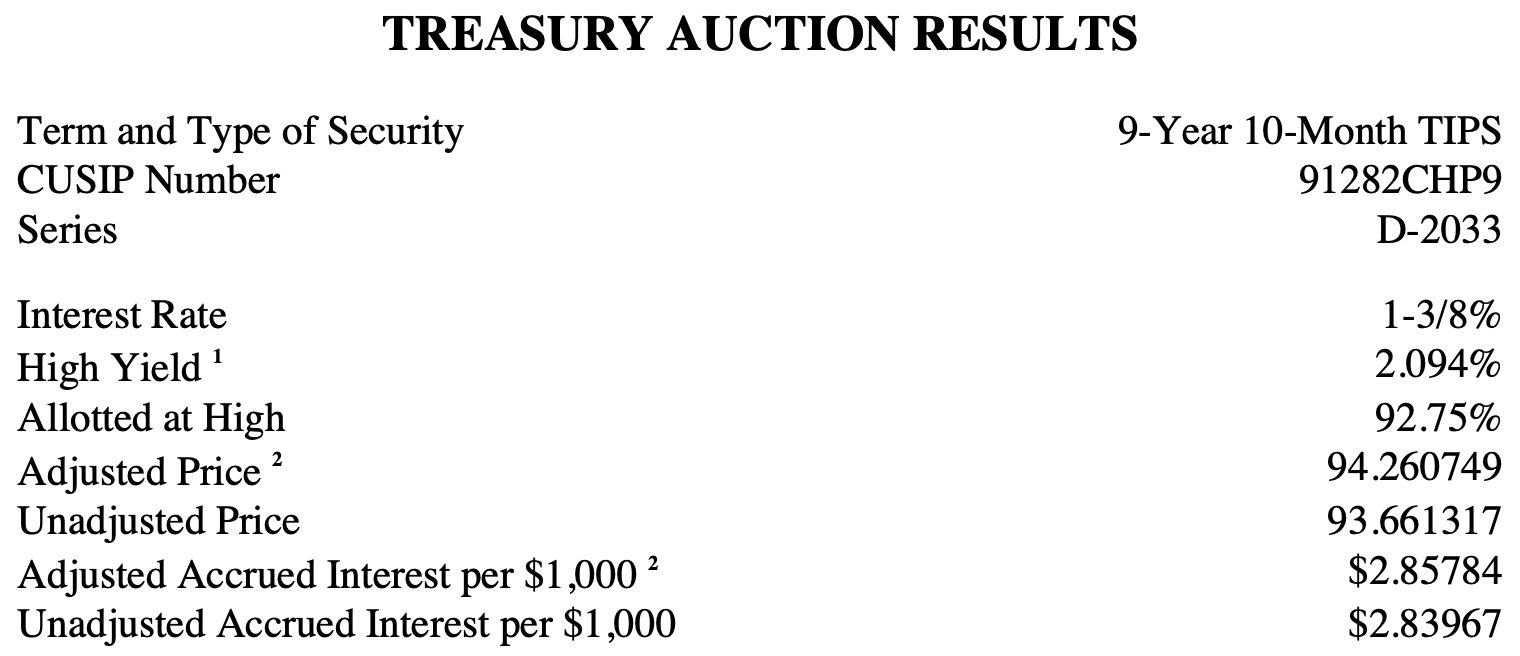

Today’s reopening auction of CUSIP 91282CHP9 — creating a 9-year, 10-month Treasury Inflation-Protected Security — generated a real yield to maturity of 2.094%, the highest for any auction of this term since January 2009.

Investors at this auction should be pleased with the result. This TIPS trades on the secondary market, and for most of the morning it was trading with a real yield of 2.07% to 2.09%, so the auction came in right on target. The real yield to maturity of 2.094% was about 60 basis points higher than the yield investors got at the originating auction, just 2 months ago.

The bid-to-cover ratio was 2.44, which indicates fair, but not spectacular, demand from investors.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

In essence, this TIPS will outperform U.S. inflation by 2.094% over the next 9 years, 10 months.

Pricing

The originating auction for CUSIP 91282CHP9 set its coupon rate at 1.375%. That means investors at today’s auction got the TIPS at a substantial discount because the auctioned real yield was so much higher.

Here is a rundown of costs for a $10,000 investment:

- Coupon rate: 1.375%

- Auction’s high yield: 2.094%

- Inflation index on Sept 29 settlement date: 1.00640

- Par value: $10,000

- Principal on settlement date: $10,064

- Cost of investment: $9,426.07 (based on unadjusted price of 0.93661317)

- Plus accrued interest: $28.58

- Total cost: $9,454.65

In summary, an investor paid $9,426.07 for $10,064 in principal and will now receive accruals matching U.S. inflation plus a coupon rate of 1.375% for the next 9-years, 10 months. The accrued interest will be repaid at the first coupon payment.

Inflation breakeven rate

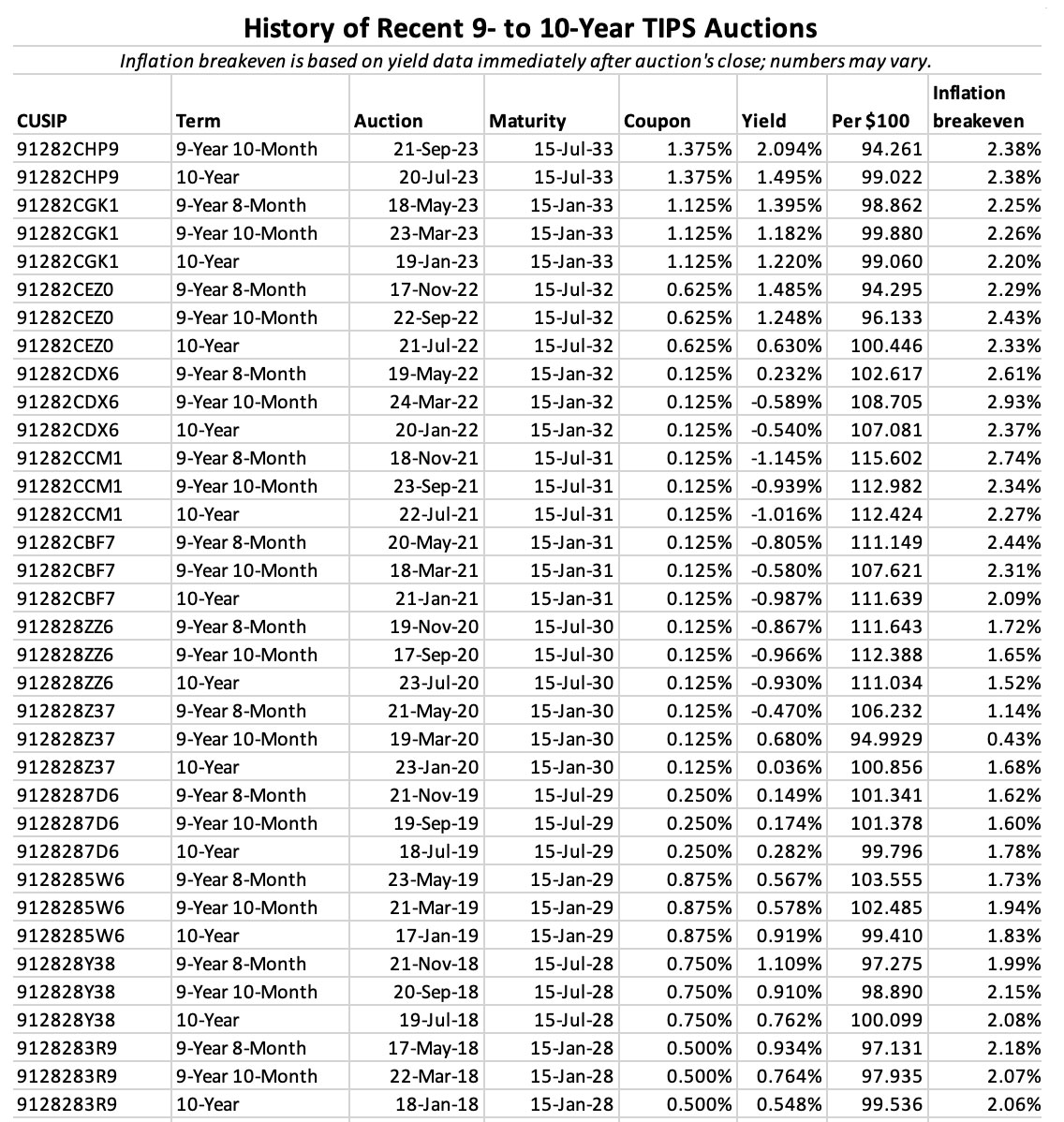

At the auction’s close, a nominal 10-year Treasury note was trading at 4.47%, setting up an inflation breakeven rate of 2.38%, exactly the same as the originating auction’s breakeven rate. Seems reasonable. Here is the trend in the 10-year inflation breakeven rate over the last 5+ years:

Final thoughts

I am traveling in northern Greece at the moment and I haven’t been able to watch financial markets carefully. This looks like a good result for investors. Getting a real yield to maturity of 2.0%+ for 10 years is highly desirable. Will real yields continue climbing higher? That definitely could happen, but today’s result looks like a solid investment.

Here is a history of auctions of this term over the last 5+ years. Today’s result was by far the most attractive in more than a decade of auctions of this term:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Amid volatility, this week’s 10-year TIPS auction still looks attractive | Treasury Inflation-Protected Securities

Agree

David, I followed the chart for when to redeem IBonds. I redeemed two $10,000 bonds October 2 that were purchased in January – one in 2021 and the other in 2022. The amounts paid were $11,500 and $11,208. Are those payouts correct?…seems off, looking at the difference.

Those are correct. You can check the value of I series bonds at https://eyebonds.info/ibonds/index.html. Remember that you forfeited the last 3 months interest, so you received the value shown for July 1 2023

Thanks Jim.

Real rates upwards of 2.3% on all maturities. The market starting to price in government dysfunction.

It appears so. The bond traders are now taking over, versus Fed dominance over the last 12 years.

I’m hoping you can elaborate on this (in a short comment or post-vacation posting).

Do the yield increases imply that traders are pricing in higher risk of default due to governing issues? Or does it seem like something else is driving the traders?

BTW – I love the site and all that you do here for us, David. I’ve learned so much reading your postings and the discussion here over the last year or two. I stuck my toe in the water and bought a small amount of 2028/2029 TIPS yielding around 2.4% a few days ago so that could get a little hands-on experience. I will hold until maturity. The yield is higher today, but I don’t think I can complain about 2.4%.

I don’t think default is an issue. A stronger-than-expected economy combined with a big ramp-up of Treasury issues are probably the main reasons. Big Treasury investors are demanding higher mid- and long-term yields, especially with the Fed pushing short-term rates so high.

I agree with David. As we have previously talked about i) year after year increasing deficit adding to the debt plus ii) servicing the debt at high interest rates plus iii) the fed continuing to do Quantitative Tightening plus, most importantly, core inflation at twice the Fed target are some of the big factors contributing to the higher and for longer rates. Today’s good news on JOLTS does not help on the interest rates front.

However, I do believe that the Fed is slowly making good progress..we better keep locking in current decent income opportunities now before it’s too late…….but then what do I know….not much….:))

Hi David,

I had a question about the new Ishares defined maturity ETF’s. (IBIF) Is one for example. Does this have the similar benefits to individual tips where you get your principal back in deflation? If so this helps fix some of the issues with VTIP and SCHP. It also gives monthly payments as dividends which is nice. Just not sure if the ETF has that deflation risk guaranteed though. Probably not, but maybe still likely? What do you think?

I’m traveling in North Macedonia this week and haven’t been able look at these ETFs. I like the idea, though.

With ETF’s, it is like crowd-sharing everything from one bucket. You buy ETF, ETF in turn buys TIPS and puts it in ONE BIG bucket alongwith other buyers’ purchases and redemptions. What you get in the end, only in the end you can know.

For example, there is a mutual fund money market fund in a 401k. STABLE VALUE fund. But average duration of securities it HOLDS is 6-7 years. So when a bank money market funds were all yielding 4-5.5% in the past year, thsi STABLE VALUE fund was yielding 1 to 1.5%. Thats what you get by crowd-sharing and letting them take duration bonds on your behalf – that is, you don’t know what you will get in times of inflation or deflation.

On the contrary, simplest thing is to BUY IN TREASURY AUCTIONS so you dont have to deal with tax consequences like OID and DEEP MARKET DISCOUNT that is prevalent now where you buy a 100$ face value bond for $50 and upwards dollars to compensate for interest rate movement form 1% to 5% as in past year or two. Now you get interest payment on coupon (coupon rate) that is taxed federally as treasury interest and free form state and local taxes. You get inflation adjustments that accrue but you pay tax in the same tax year as interest income. But there is the other consideration in DEEP DISCOUNT bonds, OID or not is all the same. You paid 55$ for a 100$ face value bond. Let’s say it has remaining 20 year duration left as original issue is 30 year bond or TIPS. This difference of 45$ should be divided by remainder of duration of 20 years and you have OPTION TO ELECT that this divided annual amount paid as TAXES ON INTEREST INCOME in same tax year or you have the OTHER OPTION to defer payment of taxes on this $45 at the very end when coupon is redeemed, which is 20 years – that is, if you don’t sell in that time. If you sell let’s say in 10 years, then you have to compute 45$ (20 year amount) divided by 2 (10 year amount) and treat that as INTEREST INCOME and subject to ordinary income taxes (maybe this too will qualify as state and local tax free as it is treasury interest, this i have to check). Any amount over this $22.50 on sale after holding for 10 years or $45 at the end of 20 years is considered CAPITAL GAINS. In other words, at end of 10 years, lets say interest rates moved favorably for you and you sold it for 85$, then you pay ORDINARY INCOME TAX on INTEREST PAYMENT for $22.50 for 10 years due to purchase at a deep discount which adjusts your BASIS for capital gains taxation to $55+22.50 = 77.50$ and now you calculate capital gains tax, long term as it is 10 year holding period for remainder which is $85-$77.50. Long term capital gains even if from treasury security is subject to state and local taxes in addition to federal (only interest income is not subject to state and local taxes). And on top of all this, if one dies in t he time, the heir must figure all this out as STEP-UP-IN-BASIS would apply to capital gains portion I guess! TRUST BUT VERIFY as I am trying to learn and figure this out as well.

It is all complex – so why would anyone want to subject themselves to such complexity of buying DEEP DISCOUNT BONDS in secondary market as opposed to BUYING AT AUCTIONS at PAR or atleast close to avoid OID which is taxed as ORDINARY INCOME i believe? – to minimize CURRENT INCOME TAXES and defer to a future date for TAX PLANNING purpose I guess!!

Of course, one key reason to buy on the secondary market is to buy all those years that won’t be auctioned this year. If you want to build a TIPS ladder quickly, you need the secondary market.

When in MACEDONIA, BE in MACEDONIA is TRUE FINANCIAL FREEDOM – “Setting the mind free of all preoccupations so one can enjoy BEING HERE NOW, in the PRESENT moment”!

For that, one must keep life including financial life so simple and straightforward and mechanical as in BUY and HOLD strategy popularized by this USEFUL BLOG (thanks, i enjoy reading).

Laddering is fine to do for BUY and HOLD investors.

Everybody else, body will be in MACEDONIA, mind will be preoccupied in markets if we keep mind BUSY THINKING of price movements, UP or DOWN, all the same for the BUSY MIND 🙂 This is BONDage and not freedom 🙂

Looks like PCE was revised going back 2 years. That probably means CPI data points were also likely higher, but weren’t revised. So treasury likely underpaid interests on TIPS, I-bonds as well as shortchanged on COLA increases for social security.

And you are surprised that the Government shortchanged everyone? This is why, investors are now demanding more from the government. Their lies have now come home to roost.

I wanted to share this. It looks like a buyer does not get a “ladder” with each fund. The buyer would have to buy multiple funds for the terms that they wanted. There is a list of funds in the press release.

“iBonds ETFs hold diverse bonds with matching maturity dates. Each ETF provides regular interest payments and distributes a final payout in its stated maturity year. Designed to mature like a bond, trade like a stock, and diversify like a fund, iBonds ETFs make bond laddering simpler with only a few ETFs rather than researching and purchasing numerous individual bonds.”

https://www.benzinga.com/pressreleases/23/09/b34791264/blackrock-expands-ishares-ibonds-etf-franchise-with-tips-etf-suite

These are target-date ETFs, so each only covers one year. Interesting idea, and the expense ratio is only 0.1%. Maybe this a good option for someone looking to buy and sell.

The weakness in this approach is that the bonds are acquired at different times and at different prices as the fund grows.

It’s hard to see who these funds are designed for, but I am guessing asset-under-management advisers.

Yields across the maturity spectrum have been going up for a while now, even before the Fed meeting.

There’s still a tremendous amount of supply coming from the Treasury, and the Federal Reserve is planning to decrease their balance sheet for years, at a rate of over $1 trillion a year

Additionally, China has been cutting back significantly on their Treasury holdings

We might have just reversed a 40 year bull market in bonds. I’m certainly surprised to find yields making new highs at this point. SOMEBODY has to keep buying these bonds, and the yield necessary to clear the market might keep increasing for longer than I expected.

I pretty much loaded up my boat with Treasuries and 5 year CDs paying 5% at the high in yields 6 months ago (at the SVB dislocation) – which looked like a genius move until recently.

I also have a good piece of change in 3 year Tnotes I bought a year ago when 4% looked like a bargain. The fact I was getting better returns than elsewhere for the past year softens the blow of missing the top by (at least) this much.

I think, we need to get a handle on what the government wants to do (Dems and Repubs share blame here) in terms of their profligate spending. While you may not have gotten the best yields, you at-least are nearer to the higher end of the yield spectrum. Most of the Banks who are FORCED to buy treasuries to pass their liquidity tests (genius move on the part of the honchos in treasury and the Fed – creating an artificial demand for their issuance), and are sitting on losses with average yields less than 2% (some even at 1%). Worry is, we will probably get another debacle before we get anywhere.

The amazing part of all of this is that an individual only comes out ahead if the bond purchased pays more than future inflation. In this way an I-bond with a fixed rate is good or a nominal that pays more than the average rate of inflation over the term of the treasury. Further, the interest from the nominal needs to be reinvested perpetually in order to come out ahead (inflation adjusted value) and those reinvestments need to be at a rate that is more than the average rate of inflation over the term(s).

It is not easy to come out ahead and some luck is required, but don’t put off getting every cent that you can because anything is better than nothing.

David,

I see the coupon is only 1.38%, so of course the purchase price was around 94

Question: If I sell a TIPS before maturity at a profit (for example, let’s say this TIPS went to par next week as an absurd but illustrative example), is that gain considered a capital gain or interest?

I don’t have experience selling TIPS early, so I am not sure. Financial writer Terry Savage tried to explain here: https://www.terrysavage.com/ask-terry/bond-capital-gains-and-losses/

these 2% plus inflation yields look like a generational opportunity to me.

The coupon, however, remains fixed at 1.38%.

If coupon rates on “Regular” Treasuries keep increasing, that will detract from the value of these securities (just as it will for all existing “regular” Treasury securities)

So it’s possible the outcomes (compared to other alternatives, such as staying in shorter term fixed income) might not be quite as attractive as it appears on the surface.

Like you I bought at the original auction two months ago. Have you ever run a calculation to determine if it would be net positive to sell a TIP at a loss and rebuy on the secondary market to lock in a higher real rate? That 50-60 bps improvement in two months is rather stunning!

John, see the comments on the 9/13 post. David doesn’t sell tips.

I haven’t done a deep analysis, but a quick reaction is if you are selling a TIPS and then immediately buying it back, you wouldn’t get any benefit. (This would have to be in a tax-deferred account.) The TIPS is trading at market value. The price you get and the price you pay should be essentially the same. In other words, the TIPS you are selling is trading at the current market real yield.

In a taxable account, to avoid wash sale rules, I suspect you could sell a 10 year TIPS and buy a different maturity.

But this goes back to my earlier question: Are gains on the sale of a TIPS considered interest or capital gains?

I would think that what you get paid in interest and inflation adjustment on the security is considered interest and accrued interest to include inflation factor calculations would apply at the time of sale………. and what you get in sale price in gain/loss due to interest rate fluctuations would go in the capital gains/loss bucket.

Is this any indication of what investors think of inflation and interest rates over the next 10 yrs?

At the least, the auction results tell you that investors expect nominal interest rates to maintain at least at current levels. Plus, inflation sentiment is 2.38%.

I’m just dipping my toes into TIPS, but I don’t understand why at this yield one wouldn’t just buy on the secondary market which is yielding around 2.2%? Is it just because you can buy smaller quantities direct?

Right now, the secondary market is the way to go, with attractive real yields across all maturities. Huge-money investors need the auctions, and so do small-lot investors. Anyone using TreasuryDirect can only buy at auction.

Worth mentioning:

If you BUY at Treasury Direct, you’re unable to sell before maturity as long as the security remains at Treasury Direct

You can however have Treasury Direct transfer the security to a brokerage account, where you will have access to the secondary market

People should also be aware that they can participate in auctions at the major brokerages (like Schwab, Fidelity and Vanguard) on the same terms as at Treasury Direct (i.e. without commissions, and as non-competitive bids)

This simplifies things if you think there’s a good chance you’ll want to sell before maturity

David,

Thank you very much for telling about this. You’re the best!!!!!

Have a great (and safe) time in Greece.

Brent Fine

Efcharistó, David. Thanks to you and the others on this listserv, I have learned so much, and my first auction was a success. Wouldn’t have had the guts to do it without your mentoring.

It looks like a gem or at least a nice shiny thing. Congrats