By David Enna, Tipswatch.com

I am sitting in Vienna International Airport this morning, beginning the trip home after a three-week adventure across northern Greece, Albania, and North Macedonia. I had a great trip, and barely had time to gaze warily at roiling stock and bond markets back home.

So today I will start catching up. My impression is that we’ve encountered a month-long Black Swan event, with mid- and longer-term real and nominal yields surging higher and the stock market slumping in response. What exactly happened? Don’t look to me for the answer: I haven’t been following financial news.

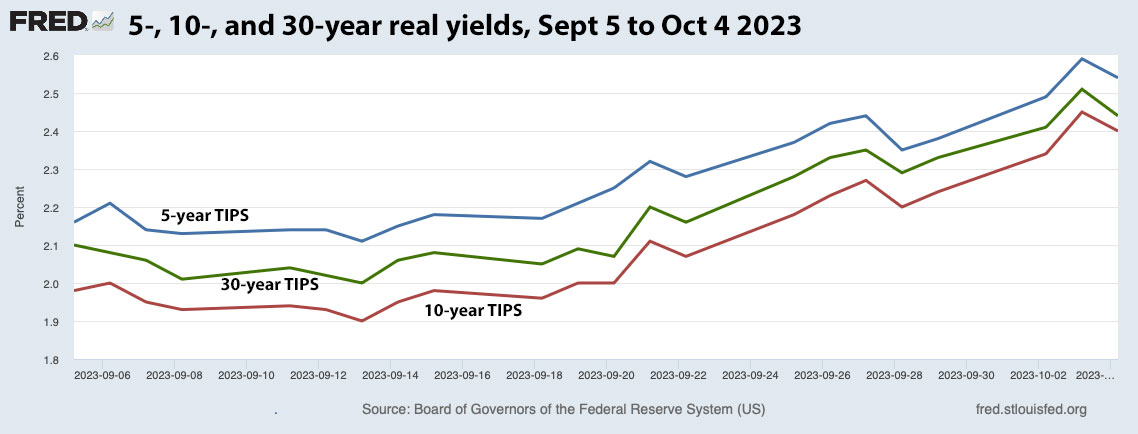

Here is a chart showing real yields over the first four trading days of September versus the first four days of October:

What’s unusual is that real yields had already been climbing since mid-May, reaching levels we haven’t seen in at least a dozen years. So this surge of nearly 50 basis points across the board — in a month — is surprising and seems to be a sign of distress in the bond market. It looks like financial markets are finally realizing that massive deficits do matter.

Here is a chart of 5-, 10- and 30-year real yields over the last month. A lot of the surge higher came after Sept 15, the day I left on this trip. (So am I responsible? Sorry!) At the same time, though, the Federal Reserve decided to hold short-term rates steady and Congress avoided a harmful shutdown. So the news wasn’t so bad, by all appearances.

But now we are heading toward another shutdown crisis with the House of Representatives stuck in a leadership brawl, and it looks like the stock market is heading for another down day, after falling about 5% over the last month.

Exciting times. I have a question: Have you been taking advantage of this surge in yields to build out your TIPS ladder or other bond investments? I will have some investment decisions to make this week, I think.

But first … On Sunday I hope to post a projection of the I Bond’s fixed-rate reset, which is coming November 1. That fixed rate will be rising, but by how much? As you know, my projection is actually a guess, but an informed guess.

It will be good to be back.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi David,

Will you be posting your thoughts on the pricing of the 5 year TIPS auction coming up on 10/19?

Thanks much!

Lon

I will be posting a preview article on Sunday morning.

Hi, David.

Here is a concept I can’t get through my thick skull. Can you help me here?

I have built a TIPS ladder through 2033 with at least 2x the most I anticipate needing to spend maturing in every given year from 2024-2033.

My plan is to use at least half of that maturing each year between 2024-2029 to invest in TIPS maturing 2034-2039 . In 2039 I will be 87 y.o. My thinking is I want to maximize the possibility of being alive when my TIPS mature, so I have not invested in TIPS maturities in the 2040s (yet). I have excess “gambling money” in the stock market that I can tap into if necessary- whatever happens I should have enough there to cover later years if I live longer.

Some people near my age have divided their investments between 2032/2033s and 2040s (I believe you may have taken that route).

Their logic, if I understand it, is that (for example) if money is withdrawn from the 2040 TIPS prematurely in 2036 , the YTM would approximate the average at time of purchase of the YTMs of the 2032s and the 2040s quoted when purchased.

I either misunderstand or I am missing something here.

Let’s say, hypothetically, the YTM at purchase on 2032s and 2040s are both exactly 2.5%. That would mean that if you held TIPS to maturity in 2032 and 2040, at both times you know you would get a YTM in real terms of 2.5% annually over your investment.

But if withdrawn prematurely, you will get whatever the market will bear at that point. If the potential yield on new 2040 TIPS purchased between now and 2036 climbs higher than 2.5%, the value of your TIPS will fall if withdrawn prematurely- you have no idea how much they will sell for, unless you hold to maturity in 2040. Yet your interest payments in the interim are only based on the coupon rate.

So, in this example, how would buying 2040 TIPS guarantee an approximate 2.5% real return on investment if you sell in 2036, and NOT be dependent on market fluctuations? That seems wrong to me.

Thanks in advance. BTW I really enjoy your blog.

It’s a tough question. I hate the idea of selling TIPS early and in fact I have never done that. So I have been leaning more toward boosting the supply in 2033. In addition, I have been putting nominal Treasurys in place to mature in 2024 to 2026, which will allow me to buy a 10-year TIPS in each of those years. After 2026, RMDs begin for me and that will complicate things. I’d personally feel comfortable with nominals backing up my TIPS in some of the later years, too, but the yields aren’t as great. Spending money in those gap years isn’t really an issue, because I could draw down from I Bonds if I needed to.

Financial adviser Allen Roth has noted that as a TIPS gets near maturity, the risk of an early sale gets lower because the price will align toward 100.

I have been rolling maturing T-bills into TIPS in my IRA. I’m debating what to do in the 401k where only mutual funds and ETFs are allowed; individual stocks and bonds are not allowed. Some of the 401k is in an intermediate term Treasury ETF and a short term TIPS ETF, but the rest is in stock funds (need to rebalance) and quite a bit in a money market fund while I figure out options. I’m not a fan of bond funds and have been burned in the past. Unfortunately to maintain my asset allocation, I’m going to have to bite the bullet in some way. I likely won’t need to tap in the 401k for 10 years (RMDs start in 15). Any thoughts? Should I got with a longer term TIPS ETF?

Yes, this is a tough one. In my former 401k, I had a core holding of Vanguard Total Bond Index and I still own some of that fund in the IRA where the 401k ended up. Do you have a stable value fund? That could be an option for an ultra-conservative investor. Right now, good money market funds are paying 5% or even 5%+, so in the near term those are good options. But long-term, probably not. (I am not a financial advisor, so I am just giving my personal opinion.) If I still had a 401k for fixed income I’d probably use total bond + short-term bond + a REIT fund if that is available.

Thanks so much for your response! I had bonds on the brain and forgot to mention that I also have a 5% REIT allocation in the 401k. I’ll look into stable value funds and consider the other suggestions. With money market funds paying 5%+ there’s no sense of urgency, but I do need to figure out a strategy.

I own 9128286N5 a TIP that matures on April 15, 2024. I was thinking of selling it and buying some 10-year treasury.

But I’m not sure how pricing works. Today, this TIP is trading at $98

With six months to maturity and assuming a 3% inflation rate, my calculation is

that I will receive 2% from price increase + 1.5% from inflation for a total of 3.5% from today to April 15, 2024

Is my calculation correct?

I would appreciate a feedback.

Thank you

Allen

OK, looking at 9128286N5, it currently has an inflation index of 1.213 an a coupon rate of 0.50%, which is below the current market. So let’s say you own $10,000 par of this TIPS. The current inflation-adjusted principal is $12,130, and the current market price is around 98. So if you sell under those terms, you should receive $12,130 x 0.98 = $11,887, plus a small amount of accrued interest. If you don’t sell you will have $12,130 rising with inflation until February 2024, plus 0.250% coupon payments in October 2023 and April 2024.

October 2, my wife and I redeemed our January 2022 issued 0% FRC I-bonds. The proceeds are now in 8-week T-bills with one reinvestment. They mature January 30, 2024 in time to purchase January 2024 issue I-bonds. We’re small buyers of TIPS but expect to purchase this month at auction 5-year TIPS in Roth and taxable accounts.

I redeemed some 0.0% I Bonds earlier this year, with the intention of doing gift-box purchases (spouses) at the 0.9% fixed rate. But then I canceled that idea because I think the fixed rate will rise Nov 1. So I might do gift-box purchases in November and then another $10,000 set before the end of April 2024.

So I guess it is a no-brainer good decision to redeem all 0.00% fixed rate I bonds by Jan 2024 and then max out your purchase of new I Bonds with fixed rate hopefully greater than 1.00%? Put difference in T-bill, T-notes, or TIPS.

If the fixed rate remains high, it makes sense to roll over 0.0% I Bond to capture the higher rate. Especially I Bonds held 5 years or longer. Taxes will be due.

I will put the proceeds from my sale this month of my Nov-21 and Jan-22 (0% fixed-rate) I-bonds into 26-week T-bills (5.5% yield), and then sell my Oct-21 and Apr-22 (0% fixed rate) I-bonds next April and put the proceeds into new I-Bonds, which should have a fixed rate somewhere north of the current 0.9% fixed rate.

I-Bonds had a great run in 2021 and 2022 but they are no longer the best deal in town.

If the fixed rate is decent, I think I Bonds remain attractive because of the potential of 30 years of tax-deferred inflation-plus earnings, along with a flexible maturity date. The new six-month composite rate could be around 5.2% to 5.4% at the November reset, still attractive.

I have been building a TIPS ladder inside my IRA over the past month or so. It now covers about two-thirds of my RMD up to age 90. The weighted average yield to maturity is 2.4%. I’m considering cashing in the remainder of my bond fund to expand the ladder to cover all of my RMD.

I struggled a bit with a plan to fill the gap years of 2034 to 2039

There seems to be a number of strategies:

1. Buy 6 additional years worth of TIPS maturing in 2033, and reinvest those funds into the gap years when they mature

2. Buy 6 additional years worth of TIPS maturing in 2040, and sell a portion of those in each of the gap years

3. Buy a 10 year TIPS in each of the years 2024 to 2029

4. Build a 6 year ladder with rungs 2024 to 2029 with the intent of buying a 10 year TIPS when each of those rungs matures

5. Some combination of (1) through (4)

6. Something else that I’m not thinking of

Each of those has a different set of risks, and they have differing execution complexities (although none is really complex), and may be dependent on where the funds for the ladder are sitting right now.

I’ll admit to being baffled my the “TIPS gap.” Financial author Allan Roth, who put a spark under this TIPS ladder idea, has suggested buying sizable extra amounts in 2033 and 2040. Or you could sell off I Bonds in those years to provide funds. Or buy nominal Treasurys maturing in those years to ensure a stable flow of cash.

I have been setting up my ladder — now all in a traditional IRA — with some nominal Treasurys maturing in January 2024 through 2026 so I can fill those spots in 2034 to 2036. After 2026, RMDs kick in, for me. Another complex issue.

As an aside, I wasted way too much time trying to figure out how to track TIPS in Quicken. After a few futile attempts, I gave up and created a Google sheet to track purchases, dividend dates and current inflation index. Once I set this up, it’s fairly easy to update as I buy more TIPS

I was baffled at first at the way Quicken + Vanguard report my TIPS holdings in an IRA brokerage account. Every so often, the inflation accruals are added as additional shares, which does make sense, but the total values in Quicken and Vanguard never quite match. However, just like you, I want to track accrued principal and not market value, since I am holding to maturity. So my true tracking is done in Excel.

The TIPS ladder my wife and I have is pretty small value because that’s all we feel we need for that segment of our portfolio. But I was happy add a bit just yesterday to help close a gap in 2030 rather than waiting and taking a chance on a later new offering or later secondary rates. There were three TIPS issues offered in the 2029-2030 timeframe. It was interesting trying to figure out just why the pricing on each was as it was. In the end I decided the differences were pretty minor. I chose the one in the middle of the range, which also had the (slightly) highest YTM.

Generally, but not always, the TIPS with a higher inflation accrual will demand a slightly higher real yield, because of the possible risk of deflation.

Right, I rather expect that. In this case, the one with the higher inflation accrual also had a higher coupon rate than the other two. I think that may have made the difference to make it more attractive at a slightly lower real yield than the other two. The spread in CPI over the 12 month span that encompassed the dated dates of those three TIPS was only about 0.6% and the spread in real yields when I purchased the other day – for the quantity I purchased – was 0.07%. As I said, very little difference at all. My puzzling about the pricing was mostly just academic.

The next pricing of I bonds need to have a fixed component of 2% for me to even start to consider investing in I bonds. It doesn’t even make sense to look at I bonds at less than 2% when a 20 year TIPS on the secondary market is paying 2.61% right now.

Sure, there are some tax and deflation advantages to the I bonds. For me, that’s not worth the trade of 30+% real return when compared to TIPS.

I don’t think we’ll see a fixed return on I Bonds that would lure me away from current TIPS. I’m excited to read your analysis this coming Sunday!

I pretty much agree, and I don’t think the I Bond’s fixed rate will rise to 2.0% in November. But I will still be a buyer because of the simplicity of the investment, tax deferral and flexible maturity date.

Pretty much all our Treasury bills and notes will be maturing in the first half of 2024 (just bought some 13-week bills). No decision yet re. next steps. Can‘t go too long as we expect a major expense within about two years. Am considering two year notes or CDs. In Roth accounts still holding short and intermediate term Treasury bond ETFs, nice monthly interest payments (which we reinvest) but prices have of course fallen for the longer duration ETFs, though all of ours are > three years. Bond market seems fragile, like an unexpected stock could cause something to break.

Bond ETFs are losers except in a declining market( they dont have the maturity safeguard of owning the real bond in increasing interest rates.) Im staying 3 month tbill ladder. Many economics think interest rates are going way higher or the next few years.

Could be true … but I think it’s possible that short-term T-bills are topping out as the yields on mid- and longer-term Treasurys are rising, fairly dramatically. There is no way to forecast where this is heading, unfortunately.

My opinion is that the 2-year Treasury note looks really attractive now at 5.08%. But who knows where we are heading.

Naive question!

When you talk about “building out” one’s TIPS ladder.. Do you mean filling in the gaps in maturities? For example if I want my ladder to cover 2030 – 2050, are you assuming that it takes quite a while to acquire maturities for each year? So maybe I first buy 2031, 2032, 2035, 2040, 2045, 2050 and then later buy 2034, 2035, 2041, 2042, and periodically continue to fill in the gaps?

Or does it refer to increasing existing positions? Or maybe both?

What I’m trying to understand is, I’d assume when creating a TIPS ladder one would want to “fill it out” all at once, rather than over time. Is the problem just that not all maturities are always available on the secondary market?

I recently talked with financial adviser/author Allan Roth and he said he has been building TIPS ladders for his clients in one or two days, using tipsladder.com to set a strategy and then calling Vanguard’s bond desk to help his clients execute the trades. So no, you don’t have to wait. You could do it quickly, like in a day or two, or stretch it out over time. Most, but not all, maturities are available to purchase in smallish lots on the secondary market.

What about the collapse in the bond market. What was that all about?

it COLLAPSED only for those who HOLD something “longer in duration than 6 months at most” in their hands.

everybody else, life goes on, as usual.

4 week Tbills.

3 month is good enough for me.

I am still rolling over staggered 13-week and 26-week T-bills, a strategy I started in spring 2022.

I want simple, 3 month 3 tier. Actually got a 4th tier money market.