Note: Since I posted this article on Oct. 8, real yields have declined about 20 basis points. That could shift the fixed-rate reset lower than I predicted, if this trend continues.

By David Enna, Tipswatch.com

It’s clear to me that Treasury will increase the fixed rate on the U.S. Series I Bond at the November 1 reset. This is an easy call. But how high can it go?

I do these projections every April and October, but there is one piece of information you need to know: The U.S. Treasury has no announced formula for setting the I Bond’s fixed rate. TreasuryDirect provides this cryptic information:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

Translation: The Treasury looks at current real yields (such as market yields on Treasury Inflation-Protected Securities) and adjusts those yields to reflect the advantages of I Bonds: primarily tax-deferred interest and a flexible maturity.

In my projections I use the real yield of 10-year TIPS as a comparison. Not perfect, I admit. But in the 12 years I have been doing these projections, I have never seen a more compelling case for raising the I Bond’s fixed rate, which is currently 0.9%, a whopping 157 basis points lower than the 10-year TIPS real yield, now 2.47%. That spread is more typically around 50 to 60 basis points.

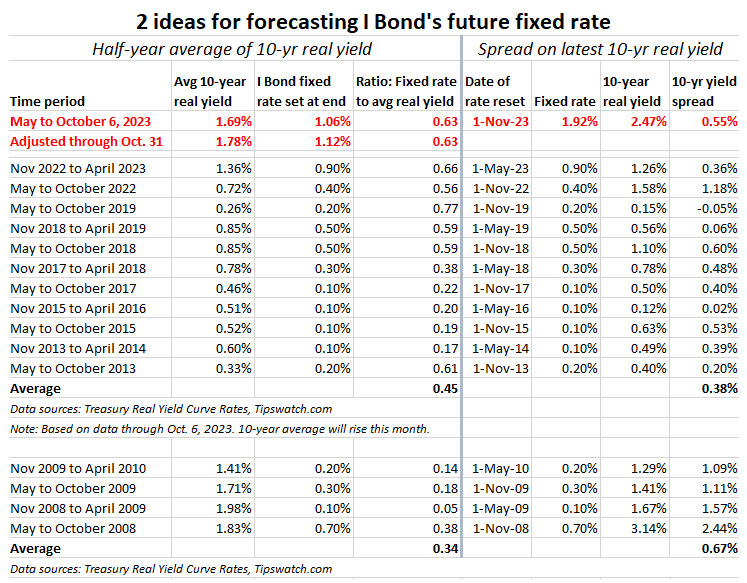

In refining these projections — based on good feedback from readers — I have more recently been looking at the average 10-year real yield over the November-to-April and May-to-October periods leading up to the fixed-rate reset. I think this gives a better prediction, because it smooths out any sudden rises or falls in real yields.

So here are my current projections, based on real yield data through October 6. Keep in mind that the half-year average is highly likely to rise in the next three weeks. But here is what we are looking at right now:

Half-year average: On the left is the projection using the half-year average 10-year real yield, which through Oct. 6 is currently 1.69%. I added a line showing an adjustment for the rest of October, with real yields remaining at 2.4%. That increases the average real yield to 1.78%.

In the last five rate resets, the average ratio of fixed-rate to real yield has been 0.63. If you apply that to the 1.78% half-year average, you end up with a projection of 1.12% for the November 1 rate reset.

Latest 10-year real yield spread: Here is where things get interesting. The current real yield for a 10-year TIPS is 2.47%, much higher than the half-year average of 1.78%. This is because yields have surged nearly 50 basis points higher in the last month.

In recent years, the typical spread between the fixed rate and the 10-year real yield has been in the range of 50 to 60 basis points. I used 55 basis points in this example. The result is a projection of 1.92% for the November 1 rate reset.

Adding this up

If you look at the May 1 reset, it appears the Treasury leaned toward a higher-than-expected fixed rate of 0.9% because the half-year average of 1.36% was higher than the then-current 10-year real yield of 1.26%.

But this month, the reverse is true, dramatically. The adjusted six-month average of 1.78% is going to fall well below the current real yield of 2.47%. Will the Treasury take that into consideration? I think so, because real yields are likely to remain elevated for some time. Without a competitive fixed rate, the I Bond will fall completely out of favor.

Looking way back

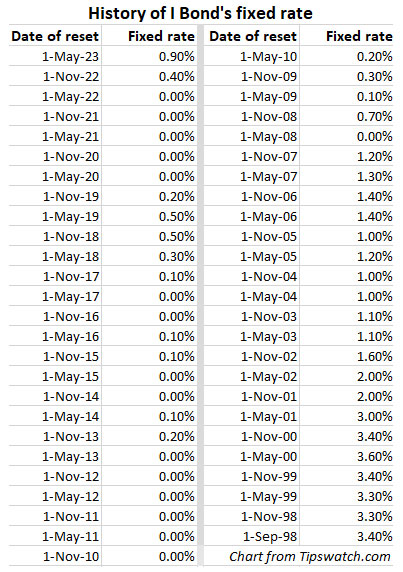

You have to go back to November 2007 to find an I Bond fixed rate reset that was 1.00% or higher. Usually, I exclude these earlier I Bonds years from my projections because the bond market changed dramatically after the financial crisis of 2008.

But let’s take a look at the yield spreads in those early years, going back to 2003, the last year with full data available:

The I Bond’s fixed rate was 1.00% or higher for each reset from May 2003 to November 2007, averaging 1.17%. In those years, the 10-year real yield averaged 2.05% (lower than today’s 2.47%) and the average fixed-rate versus 10-year yield spread was 88 basis points.

So, if you subtract 88 basis points from current 10-year real yield of 2.47%, you get 1.59%. This reinforces the case for a sizable increase in the fixed rate on November 1.

A projection + a caution

It’s early. October could be a volatile month. But my current thinking is that the I Bond’s new fixed rate should fall in the range of 1.40% to 1.70%, if the 10-year real yield continues at the current level of about 2.4%.

I am thinking that 1.40% is possible, but anything lower would be a huge disappointment for I Bond investors, putting the fixed rate (which is equivalent to a TIPS real yield) more than 100 basis points lower than the yield on 5- and 10-year TIPS, which are equivalent investments.

In my opinion, a 100-basis point spread is too high. The number should be closer to 60 to 70 basis points. Otherwise, forget I Bonds and buy TIPS. A spread of 70 basis points gets you to 1.77%. Acceptable.

But a caution: In November 2022, the Treasury set the fixed rate at 0.40% at a time when the 10-year real yield had climbed to 1.58%, a gap of 118 basis points. That occurred after a recent rise in real yields, just like we saw in September 2023. So it’s possible we could see a disappointing reset, something like 1.2%. I hope not.

And remember one of my North Star beliefs, repeated often: The Treasury sometimes does strange things.

Coming up

The I Bond’s new variable rate will be revealed on Thursday with the release of the October inflation report. A few days later, I hope to post some ideas on I Bond buying strategies for the rest of 2023 and into 2024.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: I Bond’s fixed rate: An updated projection | Treasury Inflation-Protected Securities

Pingback: Are I Bonds a good investment? Shake-up in rates changes the answer (a little)

Pingback: Are I Bonds a good investment? Shake-up in rates changes the answer (a little) | News Scrap

My main trade-off is Money Market vs. I-bonds.

Thus, if the CPI(2023) + Fixed-Rate(I-bond) > Money Market rate, then I buy I-bonds. Otherwise, I stay in Money Markets.

Assuming a 60-80 point spread between TIPS and I Bonds and current historically high rates, this makes purchasing TIP STRIPS (0.125% coupon TIPS) on the secondary market an even better proposition. Sure, you have to pay tax along the way, rather than in one lump sum at redemption, and there is real interest rate risk. However, aside from the few years after introduction as the market was wondering how the heck to price this thing and one month in 2008 during the global financial crisis, real yield has always been below 2.8% on the 10 year. I will still continue to refinance I Bonds in 2024, but for the remaining safe funds that I have an idea the latest I would cash out, I will purchase the 0.125% coupon TIPS.

I can’t see the fixed rate being set at more than 1.2% on Nov 1.

1.2% is a possibility, yes.

A fixed rate of 1.2% would be utterly unacceptable to me. That would imply a 4% break-even inflation rate!

The problem now is that since I posted this analysis on Sunday, the 10-year real yield has fallen about 18 basis points. (There was a similar fall right before the May 1 reset. If that trend continues, 1.2% gets more likely.

Then no deal.

I’m staying in MM funds at 5.2%.

Until the Fed drops the hammer on rates and equities take flight. Then what? The Fed talks tough on inflation when the unemployment rate is near a 50-year low. But what happens when the U3-UER has a 4-handle and approaches 4.5%? They won’t say so publicly, but they have a bias in favor of full-employment over price stability and are more than willing to accept core inflation of 2.5%-3.0%. Assets (such as I-bonds) that provide a hedge against inflation are critical.

If the goal of your I-Bond purchase is to maximize your return over the next year, then yep a MM fund is probably better for now. (Assuming a 1.2% fixed rate.) But over a longer period of time, that may not be true. (As a matter of fact, I think it’s unlikely to be true.) What if two years from now, MM funds are only paying 2%?

If MM become less competitive, then you can always put money into I-bonds.

I-bond rates reset every 6 months. So, there is no need to be in a rush.

Since TIPS were introduced in 2003, the I-bond fixed rate has never been higher than 1.6% and was last set as high as 1.2% on Nov 1, 2007. I would temper my expectations if I were you.

But … look back tell me the last time the 10-year real yield was 2.5%. November 2008.

Across TIPS maturities, the real yield has averaged ~1.8% since May 2, 2023. The real yield averaged ~2.0% from 11/4/2008 to 5/1/2009 when the fixed rate on 5/1/2009 was set at 0.10%. The real yield averaged ~2.41% from 5/2/2007 to 11/1/2007 when the fixed rate on 11/1/2007 was set at 1.20%. Just because the real yield spikes briefly doesn’t mean you should use that high print to set your I-bond fixed rate expectations. Put another way, setting aside the recent fixed rate increase from 0.0% to 0.5% to 0.9%, the last time the fixed rate increased as much as 30 bps from one period to the next was 5/1/2006 when the rate increased 40 bps from 1.00% to 1.40%.

dieuwer1234, it’s possible that the I Bond’s new composite rate could be around 5.2%, or higher. But that is only for six months.

Carlos, no one can 100% accurately predict the next fixed rate. In the last reset, the six-month average 10-year real yield was 1.36% and the most recent rate was 1.26%. At the time, I predicted an increase to 0.6% to 0.8%. The Treasury went with 0.9% as a fixed rate. Now, the average real yield will be about 1.70%+ (34+ basis points higher) and the most current rate might be 2.4% (114 basis points higher). Is this really a spike, or a longer-term trend? The fixed rate should rise at least 30 basis points. At least, but conditions could change before Halloween.

I bought I-bonds 5/1/21. When would be the ‘optimal’ time to sell them? I read all the webpages on your site and come up with my conclusion, but I just wanted your expert insight since I’m new to this area of investing. Thank you.

If you bought in May 2021, you earned 3.54% for six months, then 7.12% for six months, then 9.62% for six months and then 6.48% for six months. In May 2023 you transitioned to 3.38%. So May, June, July … you can redeem now if you like with the penalty hitting the 3.38% rate.

Thank you for your insight.

Your translation of the Treasury statement of the factors taken into account in setting the I-Bond fixed rate does not refer to administrative costs. I wonder if there has been an increase in short-term “churning” of I-Bonds, a strategy that is referenced in many comments on this site, resulting in an increase in administrative costs that would justify a lowering of the I-Bond fixed rate in relation to prevailing TIPS rates.

Another way of expressing the same thought is that an increase in short-term redemption of I-Bonds, could lead the Treasury to conclude that the “put” option component of I-Bonds is more valuable than previously thought, again justifying a lowering of the I-Bond fixed rate in relation to prevailing TIPS rates.

Yes, I don’t think Treasury ever saw the 9.62% I Bond freight train coming, which caused a huge surge in demand and even required upgrades to TreasuryDirect, practically an overhaul. So now those buyers who jumped on for the one-year yield are ditching I Bonds. But I think at this point — and into the near future — the administrative costs should be returning to normal

TIPS bonds are still bonds, and the bond market is reeling. It may stabilize temporarily, but I suspect future ongong problems.

I’m not saying not to buy TIPS bonds, but only to do so as part of a diversified portfolio, and expect losses unless you hold to maturity.

And there’s no automatic guarantee of our glorious and immacately honest leaders in D.C. paying their bills forever. If any of you still believe that U.S. Treasuries are the safest asset in the world, well, I don’t know what to say at that point.

If US Treasuries are not backed by the full faith and credit of the US, we will have bigger problems on hand that will decimate other assets with major ripple effects and not just in the US. Along with financial/economic repercussions there will be social as well.

Maybe hard assets will be in order along with stuffed mattresses and a bunker-like mentality.

Trust is a valuable and tenuous commodity.

I agree on the diversified portfolio, but I am not worried about TIPS held to maturity. TIPS funds are getting appealing at these yield levels, but I won’t be a buyer, since I have inflation protection covered with individual TIPS and I Bonds.

What’s safer?

Hmm…1.12% or 1.92% averages to 1.52%, which would be the highest I Bond Fixed Rate in 21 years since November 2002. That would be hard to pass up since it will have increased from 0% to 0.4% to 0.9% to (theoretically) 1.52% + Inflation.

I’ve already cashed out half of my 0% I Bonds and moved that money to T-Bills. I would say 2021 – 2022 were the “years of the I Bond” and 2023 – 2024 are the “years of the T-Bill.”

Question 1: Can a 1.52% Fixed Rate I Bond, which has to be held for a year, overtake a 52-Week T-Bill at 5.5% as a short-term play? It’s a close call but the redemption penalty probably makes it fall short. Stick with the T-Bill.

Question 2: What about a 5-Year Note which last went for 4.625%? Would 1.52% Fixed + Inflation beat the return of a 5-Year Note when the redemption penalty for the I Bond goes away? Although we can’t predict inflation or the future, sitting here today, it seems like a closer call. I’ll bet most T-Bill investors wouldn’t think that’s the case if asked. Maybe go with the I Bond in this timeframe and rest easy about hedging potential inflation spikes.

Question 1: If the fixed rate goes to 1.4% and the variable rate is about 4.0%, then you are looking at a composite rate of about 5.5%, for six months. Can that out-perform a 52-week Treasury at 5.5% in one year? Probably not, because of the three-month redemption penalty.

Question 2: Not simple to answer, since the I Bond’s variable rate changes every six months. Could go higher, could go lower, but you would get 1.4% above inflation over the 5 years. The 5-year Treasury note closed Friday at 4.75%. So if you consider only real yields, with the I Bond you’d get 1.4% (assuming that is the new fixed rate), which creates a 5-year inflation breakeven rate of 3.35% for the nominal to outperform. So the Treasury note is attractive, I think. A 5-year TIPS has a real yield of 2.58%, so the breakeven is only 2.17%, so the TIPS is also attractive.

The point is: Don’t invest in I Bonds (right now) expecting out-performance. Invest for simplicity of an inflation-adjusted savings account with the benefits of tax deferral and a flexible maturity.

So if I have some 0% fixed rate bonds, if I sell them I lose 3 months of 3.38% (.84%) and pick up a new bond with a fixed rate over that I come out ahead. Of course this is a limited opportunity with the purchase limit and also triggers some tax, but it seems like a higher fixed rate will result in people making the conversion. And if you do the repurchase in the same month you sell the older bond, you only lose 2 months of interest (.57%). Is my thinking here correct? If I would buy $10,000 anyway, is it better to keep the older bonds? I suppose David plans to discuss this in the next installment. Thank you for the continuing great articles, looking forward to Thursday.

“ And if you do the repurchase in the same month you sell the older bond, you only lose 2 months of interest (.57%).”

You don’t get paid interest for the month of redemption, even after they’ve reached 5 years. So I think that part is not correct.

If you sell bond 1 in January, you’re not going to get any interest for January from bond 1. But when you buy bond 2 in January, you will get interest for January from bond 2, so it’s a wash. Still lose 3 months if you sold a bond that’s less than 5 years old. Losing 2 months interest is incorrect..

In the long term, this is a no-brainer decision to unload 0.0% I Bonds and then buy high fixed-rate I Bonds. As Paul notes, you don’t earn interest for the month of the sale, so redeem early in the month. Some things to consider: 1) you will probably be receiving more than $10,000 (maybe much more) but you can only reinvest $10,000, so your I Bond holdings will temporarily decline. 2) You will owe federal income taxes on any interest, which reduces your effective payout. 3) You restart the clock on the one-year redemption block and 5-year penalty.

Thanks for another thorough analysis, David. I plan to wait until next April before pulling the trigger on more I Bonds. That will give me time to see how real rates evolve. If there’s any chance of the May 2024 fixed rate going even higher, I might wait until then to purchase. A fixed rate below 1.5% would certainly nudge me to add more TIPS to my portfolio instead.

I might use a similar strategy, since cash is paying 5.5% right now.

That is my plan too Justin. There’s no need to rush with TIPS likely paying much more in real yields than I bonds. I did my usual I-bond purchase in January 2023 and was regretting it at the April reset. I don’t see a compelling reason to jump into I bonds at this time aside from the ability to have tax deferred inflation earnings outside of a brokerage account.

There are so many other attractive investments right now that I don’t see a downside to a wait-and-see approach 5-6 months from now.