By David Enna, Tipswatch.com

The U.S. Treasury’s $15 billion offering of a reopened 10-year TIPS — CUSIP 91282CHP9 — generated a real yield to maturity of 2.180%, a bit higher than traders expected.

This 9-year, 8-month TIPS had been trading on the secondary market all morning with a real yield in the range of 2.13% to 2.15%. The “when-issued” prediction for the auction was 2.145%, well below the result. The bid-to-cover ratio was 2.32, indicating fairly weak demand.

But weak demand adds up to positive news for investors in this TIPS, who got a better yield at a lower price.

Pricing

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

The coupon rate of CUSIP 91282CHP9 was set at 1.375% by the originating auction on July 20, 2023. Because the auctioned real yield was much higher at 2.180%, investors got this TIPS at a substantial discount.

The unadjusted price was 93.043033. Here is how that works out for a $10,000 investment:

- Par value: $10,000

- Inflation index on settlement date: 1.01335

- Adjusted principal: $10,133.50

- Unadjusted price: 0.93043033

- Investment cost (adjusted principal x unadjusted price): $9,428.52

- Plus, accrued interest: $52.25 (will be returned at first coupon payment)

- Total cost: $9,480.77

To summarize, an investor buying $10,000 par actually paid $9,428.52 and will receive $10,133.50 in principal on the settlement date of November 30. After that, the investor will receive inflation accruals and a coupon yield of 1.375% until maturity on July 15, 2033.

We may not see many more reopening auctions with that large a cost below par value, at least for the near future, because new auctions will be much closer to current market yields. Since the spring of 2023, 10-year real yields have increased dramatically, rising more than 100 basis points since April:

Inflation breakeven rate

With the nominal 10-year Treasury note trading with a yield of 4.41% at the auction’s close, this reopened TIPS got a 10-year inflation breakeven rate of 2.23%, a bit below recent trends. Again, this looks like a positive for investors. The breakeven rate indicates that CUSIP 91282CHP9 will outperform a nominal Treasury if inflation is higher than 2.23% over the next 9 years, 8 months.

Here is the trend in the 10-year inflation breakeven rate over the last 12 months:

You could look at that zig-zagging chart and say, “The market has no idea where inflation is heading.” And you’d probably be right.

Reaction to the auction

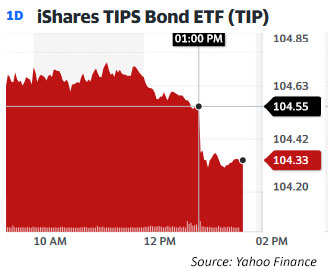

Investors were aided by fairly weak demand and got an attractive result, at least compared to expectations. The TIP ETF, as shown in the chart, dipped in value right after the auction close, another indication demand was weak, resulting in a bump higher in real yields.

But for investors, getting an above-inflation yield of 2.18% is attractive. This was the highest real yield for any 9- to 10-year TIPS auction since January 2009. It came in just a bit higher than the previous reopening auction for this TIPS, on September 21 with a real yield of 2.094%.

From a Barron’s report yesterday posted on MSN:

Tuesday’s sale of 10-year Treasury inflation-protected securities was weak, a sign that traders believe inflation will continue to decelerate. … Buyers likely shunned the 10-year TIPS because data have shown that the pace of inflation continues to slow.

The auction closes out the history of CUSIP 91282CHP9. Next month, on Dec. 21, the Treasury will offer a reopening auction of a 5-year TIPS. Then on Jan. 18, 2024, it will issue a new 10-year TIPS.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I want to set aside funds for RMD five years from now.

1. How do I compare expected yield From TIP compared to a aSTRIP?

2. What do I do with bi-annual interest payments?

I have noted before that I don’t follow STRIPs so I can give an expert opinion on that. With a regular TIPS, the bi-annual coupon payment will be paid out and you’d have to reinvest it.

Thanks – So only thing guaranteed at TIPs maturity is growth attributable to inflation. Biannual checks still leaves you with small amounts that cannot be reinvested efficiently – TIPS or just MM fund?

This is true. The coupon payments will be paid twice a year and then can be spent or reinvested. The inflation accruals continue building until you sell the TIPS or it matures.

All of a sudden, the bond market (and fixed income, in general) seems giddy with a belief the Fed is done raising rates and will begin lowering them soon. This is an about face from the past few months. TIPS yields are coming down quite quickly along with other Treasury debt.

At odds with this are indications the debt the Treasury is peddling is getting lackluster uptake — the US has to refinance a lot of debt, but investors/institutions are not too excited; they are wanting higher rates given the forward looking debt issues (growing deficits, Social Security funding, infrastructure needs etc).

While inflation has cooled, some of the inherent contributors (like lowered gas prices) can easily shoot up once again and a tight labor market could stay tight for quite a while due to demographic changes.

In summary, to me, this current euphoria seems like some whacky short term wishful thinking.

What thoughts do others have?

If I thought I could predict accurately…..But yes, I think you are on the mark.

I don’t think the Fed will raise short-term rates again, and unless we see the economy actually tank, it won’t be lowering those rates for quite awhile. Inflation might be tamed (for now) or maybe not. That’s very hard to predict. But the Fed doesn’t have much control over longer bond yields, especially while it is lowering its balance sheet of Treasurys. Longer-term yields could go higher, for the reasons you note: A huge amount of U.S. debt and lukewarm demand for Treasurys.

a novice question.

using 91282CHP9 reopening as an example what is the base dollar amount for 2023 taxes owed ?

.john.

I have no idea, honestly. If you just bought in November I’d expect very little tax effect.

I hope it’s ok to ask a question on Medicare. I had Medicare A since 2021. I recently applied for Medicare B. I am trying to decide between AARP United Health or Humana for Medicare Supplement. Any words of wisdom. I live in Massachusetts….thanks

Personal/family experience, Wisconsin. Humana stinks. United through AARP? Well AARP is getting a cut somehow. Went directly with United. All the extras Humana touts are a smokescreen.

Hi Len, thanks a lot for letting me know!! For Medicare Supplement plan G, I will be charged $182 a month (after 15% discount) for AARP United Health while Humana has quoted $168 (also after 15% discount). Based on your experience, I am now leaning towards AARP UNH. Any more comments from anyone?

So called Medicare Part C

Medicare Advantage plans? People in our investment club thought this was a way to save money. Until they required surgery! Sometimes you get what you pay for. I would never consider these myself.

No complaints about United in our group, eight went with United.

Got it …thanks!!!

Consider a High Deductible G plan. The difference between regular G and HD G is an additional $2700 deductible (hence “high deductible G”) but the premium is far lower

My 107 year old ex-mother-in-law is paying less than $40/month. If she has a “regular G” her premium would be $300/month (or $3600 a year) more

Even if she blew through the deductible every year, she’s still be better off with the HD G by almost $1000 a year

In my case, being a fairly healthy 74 year old, except for one year when I had surgery, I’ve never had more than $500-600 out of pocket expenses, and save many thousands in the difference in premium between G and HD G

Great point, I have been thinking about this. Recently I was on my wife’s high deductible plan, with contributions to HSA, for many years until she suddenly got laid off. Just to share a coincidence…she joined Vissat on 11/18/2013 and her last day at work was 11/17/2023, exactly 10 years later. The company eliminated many functions and her whole group was let go …anyway…..this group is totally awesome ….. so so giving and helpful…thanks a million….best

Not to brag, but I am as healthy as they come without on any medication, no smoking, no alcohol, no caffeine, minimum carbs or sugar, and daily swim and/or long walks. Never used any deductible while on my wife’s plan. So high deductible makes all the sense for me …thanks again

What we need is an algorithm to enter a person’s current health information and condition and it would return the ideal Part B plan. So for yourself, the answer would be a G plan but for a person with medicated HBP but otherwise healthy, the answer might be different. And for someone with kidney failure, the answer would be something else.

Good points…I have learnt a lot from all the comments here..thanks!!…best

I have original Medicare with AARP UHC for the supplemental, plan G. In North Carolina, they use the unique “community pricing” model, which means everyone supposedly pays the same rate, but the price is discounted by 3% for every year you are under age 77. At 77 the base price remains the same (but can still go up with inflation). This is a good pricing plan for people who expect to have a long life-span. For service, they are fine. No issues.

Thanks much;!;…..I also signed up for Original Medicare based on the exchanges that took place here a while ago. Will check if there is the 3% reduction in MA for the AARP UNH. MA has only 3 options for Medigap not ten. I picked the one closest to G….I am 67, so 3% reduction is good …thanks again!!!

On the high-deductible Plan G, it really is a simple math problem. Take the monthly cost of the regular Plan G, then compare that with the cost of the high-deductible plan G. If the total potential cost with the deductible is less (it might be), consider the high-deductible plan.

HOWEVER … After years of lousy corporate insurance with high deductibles, I decided that I wanted a plan where I wouldn’t think about the immediate cost if I had a health issue. No “should I wait until next year?” So for me the regular plan G met my needs.

Thanks!!!…this afternoon, I checked with United Health for a HD G plan. For Massachusetts, they call it MX1 (no not a car model :)) with $130 per month instead of $182 per month for a regular G. The Medicare B coverage remains the same for both with $240 deductible but they add $1600+ deductible (for the HD G) for hospital stay of upto 90 days If I need to be hospitalized again within 2 weeks no additional deductible otherwise another $1600+…….best solution, can’t stay healthy enough, of course, barring accidents…..thanks again for your take.

I will never go on Medicare Advantage (MA). FYI, it is private healthcare subsidized by the federal government and is NOT Medicare.

MA advantage plans are more restrictive in where you can get your care – they have their own networks (either PPO or HMO). You can get care outside of their network, but will pay more. With Original Medicare, they cover any provider that accepts Medicare. You can go anywhere in the country and get medical service. With MA, some plans have a very narrow network.

MA can deny you coverage for procedures (and many do); while you can dispute it, that takes time and sometimes you don’t have time or the patience (or skill) to fit it out. There have also been MA plans that, mid-year, go belly up and you then have to choose another plan – all those procedures that had already been put against your deductible do not carry over.

Those incessant MA commercials we see this time of year cost a lot of money. The agents selling the MA plans get a very large commission from the federal government (hundreds of dollars) for each person they direct to the plans. I can’t tell you how many calls I have gotten from MA plans trying to get me to change over! That’s a lot of time and money.

So, you can understand why the federal government spends less per person for Original Medicare than for MA. Interestingly, health care insurers make more money from their MA plans than they do from their private and employer-sponsored plans. https://news.cornell.edu/stories/2023/11/report-medicare-advantage-plans-cost-more-provide-less

MA plans have their own deductibles and cost sharing (Medicare is 80/20 and I have seen MA plans that do 70/30). They will tout a maximum out of pocket amount, but they tend to be very high (I have seen $6-7k). With Original Medicare, the reason for a gap/supplemental plan is to provide an out-of-pocket maximum (which is the deductible associated with the gap plan). I have a High Deductible G+ plan that is $60/month and an out-of-pocket max of about $2400. It’s hard to reach that level of expenses – this year I have tested the system with a lot of unexpected and major procedures and likely with not reach it.

With Original Medicare, you also will want/need to get an RX plan (Part D; many MA plans roll-in an RX plan). Oh, the hijinks of those plans! Unlike Original Medicare, these plans are through private insurers. The bean counters do their best to mix apples and oranges but the Medicare.gov website is pretty good at presenting you with your options, given your current prescriptions. HOWEVER, first check a site like GoodRX to see if you can get your drug cheaper than on the Part D plan (and perhaps allowing you to go with a cheaper Part D plan). I don’t understand why GoodRX can give you a drug cheaper than your Part D plan, but very often they do. Question – if you did get it through Part D for a higher price, does the Part D provider keep the difference (and I have had some great savings using GoodRX).

BIG WARNING HERE: In most states, if you are on a MA plan and decide later that you want to move to Original Medicare with a supplemental/gap plan, you will be penalized on the gap plan – very likely higher premiums, less selection and be subject to pre-existing conditions.

https://www.ehealthinsurance.com/medicare/enrollment/can-i-switch-from-medicare-advantage-to-medigap/

So, I am sticking to Original Medicare and hope that enough people do as well so that option does not go away or is whittled down. BTW, about half of Medicare-eligible people have MA plans. Some are good from what I can tell, but there are some very bad apples out there. Personally, I have fought enough with private insurers – I don’t need the hassles with MA. They tout all the things you can get that Original Medicare does not cover (true) but to me that is window dressing. Buyer Beware!

Thanks….I already signed up for the Original Medicare for all the reasons you articulated …. now I am almost there to sign up for Medicare Supplement with Blue Cross Blue Shield of Massachusetts using their high deductible option …thanks for taking the time and effort with your input ….best

My pharmacy automatically compares the Part D cost to GoodRX (and other discount plans) and charges me the lowest price. A nice service. But you are right, knowing that in advance may allow a cheaper D plan to be chosen.

William, I had a very bad experience with CVS using Silverscripts, which is part of the same company. I needed a rather expense “prep” treatment and had a coupon from the drug company to bypass Medicare at 1/3 the cost. CVS refused to use it. Also refused to used GoodRX at 1/2 the cost. And why? Because Caremark/CVS is both the drug supplier and distributor. So not in their interest to provide discounts. I immediately changed pharmacies, and the new one, like yours, looks for discounts.

Anyone done price comparison with Costco Pharmacy?

what percentage of your own porfolio of TIPS is in a MF or ETF? if any.

I bought for the 1st time this offering with 2.5% of my portfolio, much of the remainder is TIPS MF, I bought in an IRA, too much trouble to build a ladder.

My thinking is to lock-in the *real rate instead of the ups&downs of the TIPS MFs , or whatever they will be oer the next 10 years.

Though I dont even think I’ll need the IRA 2.5% in 10 years, Not sure I have a lot of IRA space to buy more , other than selling off more TIPS MF in the IRA.

At this point, I have zero invested in TIPS funds or ETFs. In the past I had holdings in SCHP (smaller investment) and VTIP (larger investment), but as real yields rose in the last 18 months I sold those off to buy individual TIPS in a traditional IRA. I still have a core holding in BND, the total bond fund.

so, you dont mind selling the SCHP for a loss to then buy Individuals? When you say “core” , may I ask your approximate allocations equity/BND/Tips?

About 2 1/2 years ago, I sold nearly all of my SCHP and moved that money to VTIP. This was while real yields were very low, but then came both higher yields and higher inflation, so VTIP did OK. In 2022 all my bond funds had a horrible year. BND had a total return of -13.1%. VTIP was -3%, not so bad because of surging inflation and shorter duration. My wife and I together have 65% in fixed income/cash (including TIPS and I Bonds) and 35% in stocks in low-cost index funds.

David – Do you think the upcoming 5 year treasury looks interesting? The last issue at 10/31 was 4.9%. I’m undecided if I want to lock in for that long, but I might be a buyer for a modest amount.

I don’t follow the nominal Treasurys closely, but I had been interested when the 5-year tipped toward 5%. Right now, though, the nominal 5-year yield is around 4.4%. The next auction is Monday.

First, your observations are spot on. I am preparing for interest from US Treasury Bills going down to around 4% in the second half of 2024. Yes, though the Fed has less influence on the long-term rates, short-term rates, over time, do influence the entire curve. I will love to see normalization of the yield curve and longer term rates going up. I believe that the Fed is done raising rates. The next thing to watch is the timing of cuts…..depends on a lot of incoming data…..of course, the unknown unknowns can quickly change all scenarios/narratives. We should average 4% risk free income in 2024….my wishful thinking…:)

Auction results? ” It’s tough to make predictions, especially about the future.” The late, great, Yogi Berra.

I continue to ladder systematic ally.

Just recall that exactly 2 years ago the auctioned 10-year real yield hit -1.145%, the lowest ever for a TIPS of that term. So systematic investing wasn’t a great idea then. Today … it is.

Thank you for the update. I’m a novice on TIPS and if I stick my toes in the washer, I would probably only do so with a 5-year issue. So I have two questions:

1) Do reopening yields more so reflect current rates or the ones tied to the original issue, or something in between?

2) Do you have a prediction for how the Dec. 21 reopening auction of a 5-year TIPS will do and a recommendation for investing in it vs. current 5 year T-Notes vs. holding a new iBond for 5 years?

The reopening yields do reflect the current market + investors’ willingness to take up, in this case, $15 billion in new supply. It’s too early to say a lot about next month’s 5-year reopening, but I’d guess it will be attractive. I will be posting a preview article on Sunday, Dec. 17.