By David Enna, Tipswatch.com

You can’t watch CNBC for more than 10 minutes without hearing some analyst predict the Federal Reserve will begin cutting interest rates in March 2024 … or May … or certainly by June.

On the other hand, Fed officials have rigorously maintained that interest rates — while possibly not increasing again — will remain at current levels well into next year. This is what Fed Chair Jerome Powell said on December 1:

The FOMC is strongly committed to bringing inflation down to 2 percent over time, and to keeping policy restrictive until we are confident that inflation is on a path to that objective.

It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease. We are prepared to tighten policy further if it becomes appropriate to do so.

Then we got Friday’s jobs report, with employers adding 199,000 jobs last month, considered a sign the U.S. economy is not faltering. The unemployment rate fell to 3.7%, down from October’s 3.9%. Average hourly earnings were up 4% year-over-year, exceeding the current inflation rate of 3.2%.

My conclusion: 1) The Fed doesn’t need to raise short-term interest rates, and 2) The Fed doesn’t need to cut short-term interest rates, at least until data begin showing a slowing U.S. economy.

But the bond and stock markets don’t seem to agree, thanks to a short-term focus. Bond yields have been falling for the last 45 days. The S&P 500 is up 5.25% over the last month. Highly speculative investments like Bitcoin have been surging higher. Here is a “moderate” view from Dryden Pence, chief investment officer at Pence Capital Management, predicting just a “couple” rate cuts next year:

In this video, CNBC’s Mike Santoli attempts to debunk the idea that the surge in higher-risk assets has been caused by predictions of a Fed pivot. “To me, the stock market right now is not at this level because we are assuming we will get 100 to 150 basis points of cuts next year,” he says. “It’s because … we have a little more of a sustainable moment in the expansion.”

Nice theory, but if this were true, you’d see mid- to longer-term bond yields sustaining at high levels. Instead, they have been declining sharply. Expectations of lower interest rates are driving this market.

Next week’s inflation report, coming Tuesday at 8:30 a.m. ET, will probably give another boost to market optimism. The forecast for November all-items inflation is 0.0%, which should inch the annual rate closer to 3.0%. Core inflation, however, is expected to remain steady at 4% year over year.

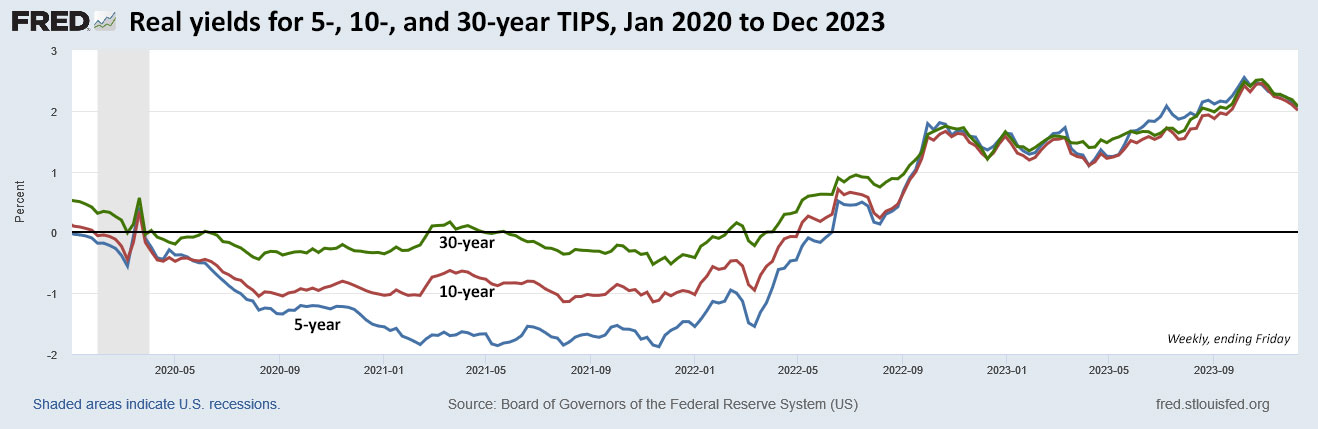

Real yields are declining

We’ve just had a “Goldilocks” period of above-inflation yields nearing 2.5% across all maturities, beginning Sept. 19 and lasting until early October. But that ended last week, with both the 10-year and 20-year real yields dipping below 2.0% for two days, before bouncing back on Friday in the wake of the positive jobs report.

Investors looking to build a solid ladder of TIPS investments, stretching well into their retirement years, had a nice opportunity to fill that ladder, or add to it. I think we will probably see lower yields heading into 2024, but nothing is certain.

Remember, real yields holding around 2% remain attractive. That yield is likely to cover any taxes owed, meaning your investment will at least match, or more likely easily exceed, future inflation, even after taxes. For perspective, here is a chart showing 5-, 10- and 30-year real yields since January 2020, just before the massive pandemic-triggered Federal Reserve easing beginning in March 2020:

This is a strange-looking chart because the yield curve is now close to perfectly flat. For the future, I expect a wider spread, and that will probably mean the shorter-term yields will fall and longer-terms will rise, or at least not fall as far.

This weekend, a Barron’s commentary backs me up:

The better question is where rates will settle in the coming decade. The probable answer: below today’s target range of 5.25%-5.50%, but higher than many economists and policy makers expected a year or two ago, and far higher than the near-zero rates of the past 15 years.

And then there is the fact that budget deficits are going to soar well into the future, forcing ever-higher Treasury borrowing. From Barron’s, a rather scary projection:

What this means for I Bonds

If real yields continue falling, the I Bond’s current fixed rate of 1.3% is going to look more and more attractive. Since Nov. 1, both the the 5-year and 10-year TIPS yields have averaged about 2.2%, which at this point would equate (possibly) to an I Bond fixed rate of about 1.3% to 1.4%. But if real yields continue falling, we very well could see a lower I Bond fixed rate at the May 1 reset. And that could be combined with a lower variable rate if inflation continues sliding lower.

The great thing about I Bonds is that the 1.3% fixed rate is available for purchases through the end of April 2024. Investors who purchase any time before then can lock in the 1.3% fixed rate for the life of the I Bond, plus a composite rate of 5.27% for a full six months.

Several readers have mentioned recently that they are considering over-paying 2023 estimated taxes to get $5,000 in paper I Bonds in lieu of next year’s federal tax refund. Not a bad idea, if you like this strategy.

At this point in time, for an experienced investor, TIPS yielding 2% above inflation remain more attractive than an I Bond with a fixed rate of 1.3%. But the gap is narrowing, and I Bonds have many advantages over TIPS: flexible maturity, better deflation protection and deferred federal taxes.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Many people over did it back in the go-go I bond days of 9.62% where they loaded up on the 9.62% I bonds in the gift box, then realized their mistake when the 9.62% rate is gone and they are stuck with all those 0% fixed rate I Bonds that will take years to get into their account……… Now is the time to buy at least a couple of years of 1.3% I Bonds in the gift box with real rates declining. It appears the 1.3% fixed rate is the peak.

As I shared before, I plan to buy my and my wife’s, $10K each, 2024 I Bonds in January to get the clock started ASAP. Yes, there is some risk, however, I too feel that 1.3% fixed is the peak for this cycle.

Don’t forget that kids can buy ibonds too, and if you have a trust, same applies. However those accounts can’t buy gift box ibonds. In our family (1 kid aged 4) we have four accounts at treasury direct.

Thanks!! … we have just one daughter and she is expecting her first baby girl in February (no SSN for the baby girl yet :))…forever, I have been telling, my daughter, a professor of EE & CS & Neuroscience at UC Berkeley, and her husband (and my neighbors:)) to buy I Bonds. Both are neuroscientists and neuro-engineers, and way way smarter than me; only, for once, if they listened, for a change, more to me…:)). Yes, I should buy for them but, me at 67, it feels a bit early..way way more than you needed to know ,🤓….thanks again!! for the idea though.

I agree.

Two stories everyone seems to believe these days is that stocks are always the best buy over the long run and they are going to get rich owning stocks. Here is a study and a chart that suggest otherwise:

https://www.tandfonline.com/doi/full/10.1080/0015198X.2023.2268556

https://www.advisorperspectives.com/dshort/updates/2023/12/04/regression-to-trend-s-p-composite-129-above-trend-in-november

Very interesting, but … the thing about data analysis is that you can often get it to show whatever you want. The regression curves shown include data from 1871 to the present day. Was the stock market the same then as it is now? Of course not. Also, society, business, trading, demographics, internet, etc etc. If we say, take a sample from 1982 to present day the picture would be a whole lot different. I would guess that the last 40 years is a better indicator of the future that the last 150 years.

And millions putting money into stocks through 401K plans these days in lieu of pensions

Thanks, as always, for the great post. Wasn’t surprised when my 10 year 6.43% FFCB bond was called last week, nice for the few months it lasted! Perhaps I can pick up a decent TIPS with the proceeds…

I generally bypass callable CDs and bonds, but this is not a bad strategy: Take that 6.43% for as long as it lasts, even if it gets called. You did well.

Don’t forget the Gift Box strategy outlined in this blog to boost your purchasing of those 1.3% I-Bonds. If you think 1.3 is a yield that will drop and you are a long term buyer of ibonds annually, you can lock in that 1.3 for several years’ worth. You just limit your ability to sell them until they are slowly gifted into your accounts.

Thank you for the article spotlighting real yields as a key driver of TIPS valuation. Would appreciate your views on the impact on real yields and TIPS pricing if you are correct about no cuts to short term rates but to avoid higher long term rates we end up with yield curve control.

I’ve concluded that there are no analysts on Wall St or CNBC; they are salesmen pumping stocks good news, bad news, no news. We should be grateful that they don’t make money pushing TIPS, or we’d be priced out.

Thanks to this blog I have built a robust TIPS ladder (timed to mature when needed in retirement) in qualified accounts over the past few months – accounting for over 60% of my bond allocation.

If you don’t mind me asking, do you hold your TIPS ladder in TreasuryDirect or in a brokerage account?

I’m assuming it’s a brokerage account because you can’t purchase TIPS in a “qualified” (IRA) account from Treasury Direct.

David, a voice of sanity in a world of Wall Street bull____.

If someone, anyone, would keep tract of their failed predictions, which primarily are made to serve their own ends………….

A great example of this was last month when Cathie Wood of high-risk ARK Investment said, “The Federal Reserve has overdone it, we’re going to see a lot more deflation going forward … If we’re right, and they’ve gone way too far, they’ll have to cut fairly significantly.” Her holdings, by the way, get a big boost when interest rates fall.

I think of Peter Lynch of Fidelity. Never buy bonds. Just rotate; growth stocks, defensive stocks, cyclical stocks, dividend stocks, based on predictions.

Very interesting…..will need to think a lot more on this… especially managing on cash flow and volatility (compared to holding bonds to maturity)….this strategy, for sure, require a lot more active manager of such a portfolio

Lynch was one in a million. Active management is a mirage, only one in five beats an index. And next year it will be a different one fifth. See the books of Jack Bogle ( founder of Vanguard) or professor Burton Malkiel and save a great deal of money.

Thanks!!…I have been following Boggle for a while. I own no active ETFs/mutual funds, pay no fee to anyone to manage my finances, while I look for products with minimal expense ratios. When l said “active”, I meant relative to my current level of active management..

Where do you find the predictions and which ones are the correct ones?

The predictions are generally worthless

That is why many are free.

Reference: A Random Walk Down Wall Street by professor Burton Malkiel. Index and save much grief.

I don’t disagree. Peter Lynch was famous for his quip about buying companies that his young daughter could understand. Unfortunately, I don’t think that strategy is foolproof. I read the Warren Buffet has instructions to move all of his wealth into the S&P 500 after his death. For myself, some of my stock picks have been good (BCC) Others not so good (CVX)(PFE). I have three sector funds though that have performed well. When the money market rates cool off. I might start moving some of my IRA funds into an S&P 500 fund, but I would like to see a different President elected first.

For the economist CPI predictions (which actually do matter because they set market expectations) I use two sources: 1) Econoday.com’s release calendar: https://us.econoday.com/byweek , which updates each Sunday and 2) Barron’s data calendar, which also updates on the weekend before the release: https://www.barrons.com/market-data?mod=BOL_TOPNAV … Are they accurate? Usually, they are close.

David thank you for that insight. Those seem like solid sources for economic forecasts. I have yet to find a good stock forecasting source though. For example, every year at this time (CAT) comes up as a good choice for the new year. Every year (CAT) does nothing. The dividend strategy appears sound but does not look so great when you lose half your principal for no reason.