Composite rate for I Bonds rises to 5.27%. Fixed rate for EE Bonds rises to 2.70%; doubling factor holds at 20 years.

By David Enna, Tipswatch.com

The Treasury announced today it is raising the permanent fixed rate on the U.S. Series I Savings Bond to 1.3%, the highest fixed rate since a reset in May 2007.

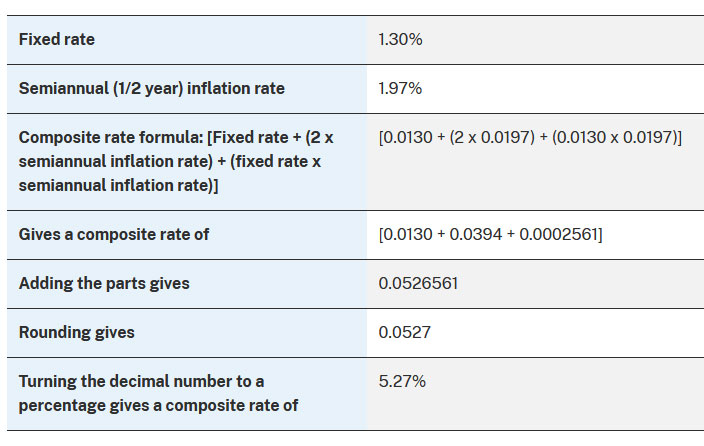

Combined with a six-month inflation-adjusted variable rate of 3.94%, I Bonds sold from November 2023 to April 2024 will get a composite rate of 5.27%, Treasury said.

The I Bond’s fixed rate is important for investors. It is permanent and stays with an I Bond until redemption or maturity in 30 years. This new fixed rate only applies to I Bonds purchased from November 2023 to April 2024.

The variable rate applies to all I Bonds, no matter when they were issued. It changes every six months and the starting date of the change depends on the month you bought the I Bond. This new 3.94% variable rate is based on non-seasonally adjusted inflation from April to September 2023.

Here is how the Treasury calculated the new composite rate:

Note that the new composite rate of 5.27% applies only to I Bonds purchased from November 2023 to April 2024. If you are holding an older I Bond with a fixed rate of 0.0%, your new composite rate will be 3.94% for six months. If you bought an I Bond from May to October 2023, it has a fixed rate of 0.9% and the new composite rate will be 4.86% for six months.

Reaction

I my most recent projection I estimated that the I Bond’s fixed rate would be set in a range of 1.1% to 1.4%, so a fixed rate of 1.3% fits into expectations. It is not spectacular, especially when a comparable investment — the 5-year Treasury Inflation Protected Security — has a real yield of 2.40%, an advantage of 110 basis points.

Not spectacular, but satisfactory and hits a 16-year high. I Bonds are a simple investment to track, earn tax-deferred interest, and can never lose a cent of accumulated value. An I Bond with a fixed rate of 1.3% remains attractive and a worthy investment.

But how worthy? I already bought my $10,000 I Bond allocation this year, back in April when the composite rate was impressive (6.89%) but the fixed rate was what we know see as mediocre (0.4%). That I Bond will soon transition to a composite rate of 4.35%. Oh well. I will still hold that one.

I am not sure a fixed rate of 1.3% is attractive enough to do a “gift-box swap” in 2023, but I will consider it. More likely I will simply wait until mid-April 2024 to decide if the 1.3% fixed rate remains highly attractive. There is no penalty for waiting to buy this 1.3% I Bond. You can purchase any time from November to April and get the same return.

From an article today on Money.com:

What’s notable about the new I bonds rate is not the overall 5.27% yield but the fixed rate. The fixed rate hasn’t exceeded 1% since before the Great Recession ….

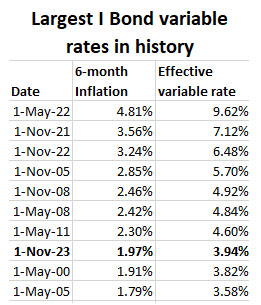

As an example of how critical the fixed rate is, look no further than the folks who bought lots of I bonds when the rate was an eye-popping 9.62% last May. The Treasury Department says it sold billions worth in the first week alone; in the last week the rate was applicable, the website had so many visitors it crashed.

While the inflation-based rate was extremely high, the fixed rate was 0%. Without a fixed rate boosting the yield, those same I bonds purchased in 2022 are now earning only 3.94% (the inflation-portion only) — versus the 5.27% rate for I bonds purchased starting in November.

Then the next question: Is a six-month composite rate of 5.27% attractive enough for short-term investors in I Bonds, looking to redeem in 12 to 18 months? I’d guess most short-term investors (I am not in the category) will pass and look to invest in shorter-term T-bills, with the 1-year currently yielding 5.41% and no penalty for redemption after one year.

Conclusion. For longer-term investors, I’d say this new I Bond with a 1.3% fixed rate is a solid investment, considering the benefits of tax-deferral, deflation protection and exemption from state income taxes. We’ve had a long wait for a super-safe return this attractive.

Rolling over 0.0% fixed rates?

If you are holding I Bonds with 0.0% fixed rate — especially those held for five years or more — you can consider redeeming those older I Bonds for new ones with the 1.3% fixed rate. When you redeem, you will owe federal taxes on the interest earned.

If you are planning to redeem I Bonds held for less than five years, read this first: “The I Bond exit ramp is now open; proceed with caution“.

I think this is a sound strategy, especially if you don’t want to raise another $20,000 to buy I Bonds this year or next in two separate accounts.

EE Bonds

And now for the disappointing news: The Treasury raised the permanent fixed rate of EE Savings Bonds to 2.7%, up only 20 basis points from the past rate of 2.5%. It is retaining the policy that EE Bonds will double in value if held for 20 years, guaranteeing a compounded return of about 3.53%.

I’m baffled. Back in May 2023, when the EE’s fixed rate was set at 2.5%, a 10-year Treasury note was yielding 3.44%. The current yield is 4.88%, 144 basis points higher. Raising the EE’s fixed rate to 2.7% is a weak move, and guaranteeing a return of 3.53% for holding 20 years is also inadequate. You can invest in a 20-year Treasury bond and get a return of 5.21%.

The doubling period should have been shortened to 16 years, at least, which would guarantee a return of about 4.5% if held for 16 years. Even that falls short of attractive. EE Bonds can now be placed on a shelf to collect dust. They aren’t a meaningful investment in November 2023.

What’s your reaction?

Investors are going to be sorting through a lot of issues when considering this new I Bond with a fixed rate of 1.3%. Is it a better investment than a 5- or 10-year TIPS held to maturity? Or is it an acceptable tax-deferred alternative? Is the 1.3% fixed rate attractive enough to trigger gift-box purchases for future distribution? Will you invest in January 2024 or hold off until mid-April when the next variable rate will be set?

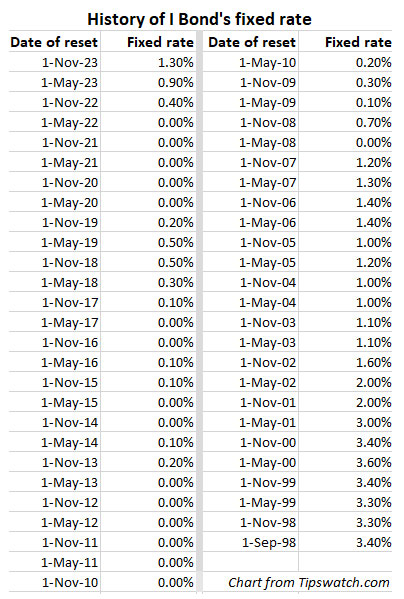

Lots of things to consider. Post your ideas in the comments section below. To close, here is the history of all fixed rates for I Bonds back to their inception in September 1998:

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am “new” to I Bond investment – started with the 9.6% bonds last year. It seems to me that interest rates are normally above the rate of inflation and therefore an I Bond with a zero or low fixed rate would not make a good long-term investment? I have noticed that the fixed rate seems to be set recently to bring the I Bond yield up to current interest rate. So if the spread between interest rates and the inflation rate continues to increase – will the fixed rate increase next May to something higher than 1.3%? Any predictions on the May fixed rate based on what you know now?

As things stand now, the fixed rate is likely to go down in May, but time remains. An I Bond with a 0.0% fixed rate will provide a return matching future inflation, no matter what interest rates do. There were several years in the last decade where T-bills were paying very close to zero and inflation was running higher than that. For example, in January 2022 the 1-year Treasury was paying 0.40%, just a few months before inflation was about to surge to 9.1%. So matching inflation can work out fine, especially when you are earning tax-deferred interest.

Thank you. I think I will wait until April to decide whether to jump on the1.3% or wait for the May rate. I may ask the question again in April.

David,Thanks for your excellent posts. They make the various Treasury instruments and rates comprehensible, enabling me to sensibly and profitably include Treasuries in my investment portfolio. I have a question that maybe you have an answer to. When I go into my Treasury Direct account, for I bonds, it has not updated the interest rates to the Nov 1 rates. My recollection is that in the past, the interest rates were updated on my account as soon as they changed. Is this some glitch by Treasury or might I not be finding the right place in my account to see the new rates on all my I bonds?Thanks for any info on this.John Swan

One thought is this: The I Bond composite rate changes every six months, but the starting month depends on the month when you purchased the I Bond. The schedule looks like this:

Issue month of your bond — New rates take effect

January January 1 / July 1

February February 1 / August 1

March March 1 / September 1

April April 1 / October 1

May May 1 / November 1

June June 1 / December 1

July July 1 / January 1

August August 1 / February 1

September September 1 / March 1

October October 1 / April 1

November November 1 / May 1

December December 1 / June 1

I am sure that’s it. Thank You. Geez, I feel dumb not realizing that after buying I Bonds for over 20 years. Well at least I’ve got enough sense to buy I Bonds:).

Thanks again.

As usual, great commentary again by David and others speculating on rates. When looking at the chart of long-term fixed I-Bond rates that David posted, buying new I-Bonds appears to be a no-brainer, historically speaking. I am one of the folks who is rolling recent zero fixed rate I-Bonds to these newer, automatically higher yielding I-Bonds because in my view, I-Bonds are merely an alternative to high yield savings accounts or CD’s, with the added benefit of tax-deferrals. I treat it as my quasi-emergency fund. But back to rates…I believe rates will indeed stay higher for longer. The economy has proven durable in the face of the fastest rate hike regime in ages, and when you consider the economy is 70% consumer-spending, and 70% of that consumer spending is on services, then higher rates have less impact of consumer behavior than in past cycles. Plus, the two largest spending co-horts, Boomers and Millennials, are inclined to be consumers of services rather than goods, so it appears that higher for longer is sustainable, and maybe can go even higher now considering the U.S. debt financing needs, and the fact that the majority of our debt financing comes from FDI (foreign direct investment), and those tides are starting to turn too. So more supply and less demand in Treasurys could mean higher rates for longer, for sure.

Pingback: Random thoughts on I Bonds in 2023, 2024 | Treasury Inflation-Protected Securities

Regarding EE Bonds vs a 20-year Treasury, the latter coupons at 5.21% per year on $10,000 over 20 years amount to $10,420. Is the $420 over EE Bonds the reason they are inferior or is my math wrong?

The most recent 20 year Treasury bond reopening went for 89.352074 per 100 face value. So on purchase you got $10,000 face value at a discounted price of $8935+. Add to that the annual coupon payments of $437.50 and it adds up to a heck of a lot more than $420.

Okay, on rereading clearly I misunderstood your statement. But I come up with a difference closer to $900 over the 19 year 10 month span for the latest 20 year reissue.

I think that analysis also assumes you don’t reinvest the coupon payments received along the way. If you were to get a return on the coupons, the total gain from the 20-year should be larger.

I am going to “recycle” my I-bonds with the new fixed rate. I haven’t bought any this year so I can still buy $10,000. My question would be, what would you do with anything leftover? I have $11,272 from where I took advantage of the high rates, starting with 7.12%. So that will leave $1,272 after I buy new ones. With T-bills being at 5% or more it would make more “cents” (haha) to buy those or anything greater than 3.94%.

First, David, thank you for sharing your excellent knowledge and observations over the years.

I am really perplexed by all the discussion on this site (this article and prior) about people debating whether to cash out old Ibonds to buy new ones. The annual limit is only $10,000! (you’re going to need a lot more money than that for retirement.) Any cashout simply reduces your total lifetime amount of Ibonds. Do people only intend to hold around $10,000 in Ibonds for their whole life(?) Are they looking at Ibonds as just a $10,000 position in their portfolio and they are actively trading (i.e. buying and selling) just to collect the optimal current year interest return?

I am accumulating Ibonds to hold for the long term. For example, 20 years times $10,000 is only $200,000 and your going to need more than that to pay for a full retirement. Ibonds are only a portion of my portfolio, but a really safe boring portion guaranteed to maintain purchasing power with inflation. If I sell some older, less desirable Ibonds (i.e. lower fixed rate), that means reducing the portion of my guaranteed inflation protected assets. Why would I want to do that? So what am I missing from all these people that keep talking about selling old Ibonds to buy new Ibonds? If you keep doing that, you’ll never have more than $10,000 in Ibonds total, so why bother. I expect to have many times that amount so would think it makes sense to keep buying AND keep holding the old ones.

Help me understand why people are so eager to discuss selling and old Ibond to buy a new one.

FYI – I don’t have any TIPS because I don’t like the tax reporting if held outside of IRAs, but more so, I am still wrestling with the commitment needed to hold them to maturity even held within an IRA.

As David has pointed out, ibonds are not a retirement vehicle per se. They are an alternative to a savings account for rainy days or other short term needs but with the added benefits of inflation protection, liquidity, capital preservation in a deflationary period and deferred tax. And you can buy more than $10k in a year via the gift box strategy.

I always have recommended not redeeming I Bonds “until you need the money” because of the difficulty in building a sizable allocation. However, now that I am retired (with a sizable allocation), I recognize that I Bonds are a potential store of cash for whatever the need. There is no real reason to hold to maturity, in my opinion. In fact, no I Bond has yet matured. I would recommend being cautious in cashing out wholesale from I Bonds. But in some cases, it does make sense to roll over 0.0% I Bonds for issues with a higher fixed rate.

Obviously, a savvy investor could use I Bond money with a real yield of 0.0% to deploy into TIPS with a real yield of 2.4%. But they are different investments, with slightly different purposes. So are T-bills, which will expire very quickly and face reinvestment risk.

Another point is that if you have that $200,000 in I Bonds, whether some are 0% fixed or not, you are well positioned for the next inflation shock, which is not that much out of the question.

benfinret–I don’t think of I-Bonds as my retirement money (and I just retired). That’s what the rest of my portfolio is for. (Which includes a TIPs ladder within an IRA.) Rather, I think of I-Bonds as my “rainy day” fund. I may use the money for some currently undefined expense in five years. Or 10 years. Or maybe never. I think I-Bonds are ideal for this as they’re silently growing on a tax-deferred basis.

In our case, my wife and I figure the right size for our rainy day fund is $60K-$80K. In our case, this means selling $20K of 0% fixed rate I-Bonds to get 1.3% fixed rate I-Bonds.

I maintain a portfolio of LLCs for the purpose of holding I bonds. They are easy to set up and cheap. You can have hundreds of them to buy and sell as many I Bonds as you want, buying and selling without limits.

Unlike everyone here I’m a small investor (not enough disposable money to buy huge amounts of savings bonds/Treasury bonds, etc.). I backed off purchasing EE Bonds for the longest time until 2019 when the fixed rate was still just 0.10%, with the intention of holding them for 20 years to get the 3.53% compounded return and cover any extra expenses in retirement (or leave them for my wife and/or other beneficiaries of my estate). Unlike Dave, I’m ECSTATIC about the new 2.70% rate for EE Bonds — it’s a damn sight better than the paltry interest rate my savings account is earning at my brick and mortar bank, along with the simplicity compared to Treasury bonds. But what I might do is redeem all the 0.10% EE Bonds I purchased (after January 1) and use them boost my monthly $100 purchases of I Bonds/EE Bonds, plus an occasional TIPS in small amounts (based on Dave’s recommendations, of course).

The 2.7% is not in addition to the doubling in 20 years. Therefore if held for 20 years you are still going to get in total only 3.53% compounded return, much less than what you can get in standard Treasury Bonds right now. If you don’t want the duration risk you can buy T bills instead or a Money Market Fund. Ditch your brick and mortar bank’s savings accounts, you should not be earning less than 2.7% right now, more like double that.

But if interest rates collapse in the near to mid future, not that I think that is likely, then the 2.7% and 17 year doubling will appear to be wise decisions. At least versus short term treasuries and CDs.

Sure, but you can also lock in a higher yield by buying a nominal Treasury out that long. And if you want to trade you could capture a capital gain. If things go your way. (By the way, the 2.7% fixed rate is tied to a 20-year doubling.)

If I purchase a nominal Treasury and hold it for a little while, will it gain the six-month’s interest if I transfer it into a brokerage account from TreasuryDirect?

This is a great question. I would think the Treasury would deliver any interest due along with the transfer. But I have never done this.

I found this on TD website:

“In TreasuryDirect, the U.S. Treasury makes interest and principal payments directly to the financial account you choose. In the Commercial Book-Entry System, Treasury’s interest and principal payments may flow through several institutions on their way to you. For example, a payment could go from the Federal Reserve to a large bank to a smaller bank to your broker, dealer, or financial institution before it gets to you.”

Also, the existing EE bonds would have compounded at approximately 4.75% from when you plan to redeem them until 2039. The new ones will be objectively worse.

It does make sense to exit EE Bonds with a fixed rate of 0.1% and 16 years to go to doubling. The three-month interest penalty will be effectively zero. Up to you on where to re-deploy the money. You could consider a 5-year bank CD paying 4.5%? A 5-year Treasury note is yielding about 4.8%. So is the 10-year. The new EE Bonds at 2.7% aren’t that attractive by comparison.

I was planning on redeeming i-bonds purchased in Nov 2018, which I believe (correct me if I’m wrong) can now be redeemed with no loss of interest, to purchase these new ibonds. When I went to TD under the interest rate column for these ibonds it mentions “Not Available” (whereas the one issued Apr19 shows 3.89% for example). Is that a bug?

Yes, it sounds like a bug. Those Nov 2018 I Bonds had a fixed rate of 0.5% so they are transitioning to a composite rate of 4.45%. If you have other I Bonds with a 0.0% fixed rate, consider those for redemption first. …. The April 2019 I Bonds also have a fixed rate of 0.5% and transitioned in October to a composite rate of 3.89% and then in April will go to 4.45%

Yes, I am planning to redeem the Apr 2019 ones in April 2024 (5 years after purchase). Keeping them for these 6 months will yield 9 months of interest effectively (6 months plus avoiding the 3 months penalty) which brings the effective rate above t-bills for the period.

The only other i-bond I have is the Apr 2022 one, for which optimal redemption date is 1st of January.

I plan to redeem all of them and then buy new ones with higher fixed rate or TIPS

Check back November 2 following a site update scheduled between 6:30 and 8:30 am EDT.

As the amount (value) showing seemed correct I redeemed them in order to not waste a day of interest. I hope it was the right move!

I’d like a reaction to the following from some smarter people than me. I have a 10 year TIPS ladder that I will use for income as they mature, starting 2026. I have a large stock portfolio that I intend for beyond that time and will migrate into extending the ladder as time goes by. However, I have additional MM cash that at some point I will need to move to a more sustainable non-stock investment.

I will be buying the new TIPS bond being issued in January, but I’m also thinking that I wait until April and then if it seems rates are on the way down or solidly leveling, to buy 10 years worth of ibonds from my wife and I via the gift box approach and then gradually “unbox” them over the years. If it seems the May rate may be higher I’ll do it after that using the same logic as to timing.

That may be a bit extreme, but I think the logic works if I want to kick the interest down the road for tax purposes. I wonder if anyone else has thought about this approach. Any downside to this?

I have never used the gift-box approach, mainly because I believe it should be used only to lock in a high fixed rate on the I Bond, and not for a high variable rate. So, here we are. I agree on delaying any 2024 I Bond purchase until April. If real yields are around this current level, I’d probably buy the normal allocation in April and *possibly* one set of the gift-box swap. If real yields rise sharply, then I’d wait to beyond April, probably. The one scenario that I’d consider multiple gift-box swaps would be if real yields decline sharply. But personally, I wouldn’t do 10.

We know the benefits of I Bonds so I won’t rehash them here. I’ve been using the Gift Box Strategy in moderation for years. The problem with buying 10 x $10,000 (or 5 x $20,000 with a spouse) of I Bonds in April (or May depending on the latter’s anticipated new Fixed rate) using the Gift Box Strategy is that you are relegating most of that money into limbo (growing in value but inaccessible / illiquid for most of that period). There are several ways that could be an issue:

Possibility 1: If you need that money for an unanticipated expense during those years, you can’t reach it until you deliver it one year at a time.

Possibility 2: If we go into a Recession and interest rates and inflation drop, you’ll be getting 1.3% on your money without being able to move most of it into another investment for years.

Possibility 3: If there’s no Recession and rates continue to rise in the coming years, the 1.3% fixed rate could rise without your ability to lock in those higher rates because your money is in limbo.

Because we don’t know the future, locking in that much money for that many years introduces a risk into the equation even with using a completely non-risky I Bond. That said, if you have other substantial savings beyond this possible I Bond investment that can mitigate these possible concerns, then I don’t see an issue with it, but I’d recommend a more gradual approach to hedge the unknowable.

should I buy 10k of I bonds with the current fixed rate or 10k of 20yr tips in ira a/c ? what is the math here. I will not need to cash them for next 20 yrs. thanks.

This is a personal decision. I consider I Bonds an inflation-protected savings program to be used in the future, at least 5 years out. I’ve been buying 17- to 20-year TIPS in recent months as part of a long-term TIPS ladder to provide future retirement funding. A 20-year TIPS is a risky investment if you don’t plan to hold to maturity. But if you do, it’s fine. You could combine both investments to meet your personal needs.

Tough to make perfect decision. I ended up doing 7,500 in 0.40 fixed rate I bonds before 5/1/23, then 4,500 in 0.90 I bonds in May – Aug (2,000 in Gift Box). Have redeemed 20,242 worth of 0% Bonds with 10,554 greater than 5 years and 9,688 less than 5 years. Think in 2024 I’ll sell remainder of 0% I bonds (16,140), transfer the 2,000 from gift box and buy 8,000 of the 1.3% I bonds. If 5/1/24 fixed rate looks like it will be higher, then could buy those in gift box. Any suggestions on improvement to this plan?

That’s a lot to digest. I do think any gift-box purchases should be delayed into next year, like in April. If real yields plummet early next year, then the gift-box strategy will be wise. If real yields rise, then possibly delay any purchases. My personal choice: I won’t be unloading all my 0.0% I Bonds immediately. I will use those strategically to buy I Bonds at a better rate in the future, if we get the chance.

So why isn’t the fixed rate at least 3.0%, like I got back in 2001 when the CPI was only 2.8%? Just kidding around. I know they changed their formula, or guess, or whatever they use to decide the fixed rate.

BTW, for all those looking to cash out quickly, remember, I-bonds are designed for long-term investment, and when you cash out, you immediately pay federal tax on your interest. This sort of negates one of the big incentives for buying I-bonds (tax-deferred interest).

Interesting point, though. In May 2001 — when the fixed rate was set at 3.0% — the 10-year Treasury bond had a nominal yield of 5.35%, not too far above where it is trading today at 4.88%. A 10-year TIPS was auctioned earlier in 2001 with a real yield of 3.52%. Times have certainly changed.

I will wait until mid-April to decide if to buy these or wait and buy later in the year.

My bigger decision is to keep holding my I Bonds from previous years, even those with 0% fixed rate. I haven’t done the full math (I think you may have in previous posts), but my impression is that when averaging their performance over the last 11 years that I’ve been getting I Bonds, they’ve done at least as well as I’d have done getting CDs at banks. Sure, there are periods where they’ve underperformed, but there are also periods where they’ve outperformed. I expect that trend to continue (right now they are underperforming, but things could well change in a year or three). And all with a very low-maintenance approach of just investing $10,000 each year and forgetting about it.

Plus, I’ve got kids going to college in a handful of years, and I’m hoping to be able to sell the 0% fixed rate I Bonds tax-free to help pay for that. May as well hold out until then before cashing them in.

I would recoup the interest penalty on my 0% I-Bonds in 8-9 months with the 1.3% fixed rate.

Even better, just buy the TIPS

I have a significant amount of TIPS in my IRAs, both traditional and Roth. Just not a fan in taxable accounts.

One thing to consider about 0.0% I Bonds: Do you believe there will come a time in the future when the Federal Reserve again pushes nominal yields close to zero and real yields below zero? If so, those I Bonds will be a valuable holding because they will keep pace with inflation. However … is that era of Fed intervention now over?

In that scenario long term TIPS will do even better, because a) they have a higher yield, b) as real yields drop they will rise in price and the gains will be immediately realizable upfront, and c) the gains will be in the form of capital gains, not income.

Plan to redeem my 0% and 0.4% ibonds of the past 2 years in early 2024, possibly replace in April or May, depending on what trending rates for TIPS and nominal treasuries are.

I am with all of you, going to put my 2024 allocation in T-Bills until mid April rather than by them immediately at the end of January. I won’t be unloading my under five year I Bonds yet though, as I think having that dry powder may be needed if inflation rises in the future.

As far as EE Bonds, the benefits of the bond are not worth a 2.5% haircut, and I am looking into STRIPS to meet the need of supplementing future retirement income. David, it might be useful to do an article comparing STRIPS with EE Bonds if you haven’t already.

STRIPS are my “kryptonite.” I know nothing about them. And I am not so eager to learn. Ask me about floating-rate notes, I know dangerously “little” about them. 🙂

Aren’t STRIPS the same as EE-Bonds in the sense they earn no interest during their lifetime and are sold at discount and are paid full face value at maturity? The difference between the purchase price and the matured face value is the “interest earned” and taxable at maturity, correct?

STRIPS are “zero-coupon” bonds that earn interest via the spread between the purchase price and maturity value.

Like TIPS, there are phantom income tax issues if held in a taxable account. In a taxable account, the IRS requires the holder to report “imputed interest” annually. You pay taxes on interest that was not actually paid.

IMO, best held in a tax-deferred account…just like TIPS.

Thanks. Yes, I missed that tax on phantom interest is due annually.

“ If you bought an I Bond from May to October 2023, it has a fixed rate of 0.9% and the new composite rate will be 4.30% for six months.”

I believe you underestimated the yield.

I updated that awhile ago to 4.86%, but the site is sometimes slow to update if your browser has cached it. I pulled the incorrect number from the TreasuryDirect site, and didn’t realized they hadn’t updated the list to reflect the 1.3% fixed rate.

I own a few of those 0.9 fixed bought on May of this yer. I will only buy the new ones (1.3%) only if I can commit myself to keep them at least 5 years. Otherwise it will be 26 and 52 weeks T-bills.

One thing I found aggravating was that when I saw a mistake in my last post I was not able to edit it. I use to be able to edit my own posts. Is that a bug or a feature?

On this WordPress site I don’t think you could ever edit your own comments.

A little disappointing but in line with expectations. A 1.3% fixed rate is more reasonable than 1.1% or 1.2%, which the Treasury might have been able to justify due to the higher variable rate near 4%.

I was hoping the Treasury would raise the fixed rate by another half percentage point to 1.4%. That would have been a full percentage point above last November’s reset. Instead the new fixed rate is 0.9% higher than it was a year ago, matching the just expired fixed rate of 0.9%. The new fixed rate is also 0.4% higher than last November’s 0.4% fixed rate. Almost makes you wonder if someone at the Treasury chooses the most “symbolic” number when determining the new fixed rate.

Like others, I also plan to wait until late April 2024 to decide how to allocate next year’s I Bond purchases. How real rates trend over the next 5-6 months is anyone’s guess.

One of the benefits of iBonds (as I have learned from David) is the 6-month rate period during which you can make a Buy decision with no impact on the rate. So I think it’s best to wait until we have all available information in April 2024 and then make a decision whether to Buy in April or May. As always I will be following David’s analysis closely.

I continue to be impressed by the accurate analysis you provide when predicting the intentionally vague method by which TD chooses the I Bond’s fixed rate. Thank you for the guidance. It’s helpful to have an idea of what’s going to happen in advance with one’s investment choices.

A 0.4% fixed rate increase from 0.9% to 1.3% is somewhat disappointing and definitely underwhelming in this market, but when you take into account a relatively competitive 6-month composite rate of 5.27%, the tax deferral benefit, the liquidity after one year, the downside protection, the upside inflation tracking, and the historical context, it is indeed a good time to buy an I Bond.

Sure, you can buy a T-Bill for a shorter period at a slightly higher rate, but that won’t be the status quo forever. Rates will eventually drop, and when they do, having 1.3% fixed + inflation in those years will be beneficial. It seems to me the ideal plan hasn’t changed since before the announcement. Park your money in a t-bill earning 5.5% until April, evaluate the inflation rate for the subsequent 6-month period and the likelihood of a higher or lower fixed rate at that time, and then move that money into an I Bond at the end of April or at the May reset.

Excellent analysis, thanks.

Agree with your analysis except for the part that interest rate would drop due to recession or recessionary conditions. With such a huge deficit and therefore the need by treasury to raise money for government spending, this could lead to a stagflation. Rates may not necessarily come down so it is possible that both the fixed and composite rates may rise in May 2024. In short, this could turn out to be not quite competitive/attractive buy.

Yes, pvsfox, that is a possibility. We may still be in a rate up cycle through May 2024, but, as they say, whatever goes up must come down. At some point we will hit a recessionary period, possibly as soon as late 2024, and the Fed may have to reverse course. At that point, you will want to be locked into BOTH the 5.27% rate (with 1.3% fixed) AND the (potentially higher) May 1 rate. And if the May 1 fixed rate is higher than 1.3%, you may want to employ the gifting strategy with a spouse to own both issues.

While David has provided excellent reasoning for the rate, I will speculate. With $2T In deficits into perpetuity, many investors into I-Bonds for the short term 9.62% without understanding it not having read David’s columns, the Treasury has been snookering investors for more than a decade. The very architect of ZIRP now leading treasury, she knows monetizing the debt buys her time. This is deliberate underpricing.

Recently, she commented that high US Treasury Bond rates has to do with the economic growth and not due the debt or deficit….hmm…I a spinned narrative ?

I let out a massive SIGH when I heard these comments from Yellen. I hate political spin, by either side. Rising interest rates could be partially caused by economic growth, sure, but the main causes (by far) are increased debt-raising needs of the U.S. Treasury (because of deficits), Federal Reserve balance sheet reductions, political instability in the U.S. Congress, and the lack of eager foreign investors.

I feel the same and agree with you. Other factors, connected with your list, include perhaps higher neutral rate and expectations for a higher term premium.

I will disagree. I think the 1.3% fixed rate seems fair, if the Treasury does look at 6-month real yields and gives I Bonds a discounted fixed rate, based on the many advantages of I Bonds. If real yields continue in this 2.4% range for the next six months, the next fixed rate will be higher.

No reason to rush. The fixed rate should get higher on next revision. Will have ample notice if that’s not likely.

I agree. I already purchased my 2023 allocation. For next years, I am going to wait until April to see what the fed and interest rates are doing. If there’s a chance the fixed will go higher I will push until the May reset and then do the same in October. I am long term so want the highest fixed possible.

I agree with this, there is no reason to rush if you’ve already made your 2023 purchases. I will wait until mid-April 2024 at least and then evaluate whether to purchase and possibly make additional gift box purchases, or hold off again past the May reset and re-evaluate again in October.

Well done David, first and best source for inflation indexed securities. Think I will wait until January to make a decision.

This takes me back. On April 30th, 2007, when interest rates were near zero, I noticed the I Bond had a fixed rate of 1.2%, which would be changing the following day. I went straight to my credit union and told them I wanted to buy an I Bond. The first teller didn’t know what I was talking about, but I eventually got passed on to someone who found the right form for purchasing an I Bond. I bought a $5000 one, because that was the most I could afford. Now, 16 years later, the fixed rate has finally surpassed that one.

Great story. Thanks for sharing this.

I had almost the same experience. I bought a $5000 I Bond from our local bank in late April 2008, to snag the 1.2% fixed rate. And that was my best fixed rate until now!

Yes! (And I had my date wrong. It was April 2008, but I couldn’t edit it.) It’s fun to have some other I Bond nerds to share these stories with! Ha.

Really interesting news, Dave. Whay would be your take on the durability of the fixed rate throughout 2024? I’m wondering how I should pace my purchases. My opinion is that “higher for longer” means buying before May 1 and Nov 1 should be safe, late in 2024 less sure if we get economic softness and a rate cute.

I think I answered my own question – wait until mid-April and see where we are with fixed rate projections for May 1

You nailed it David. Good job! I was hoping for 1.4 or 1.5. Oh, well.

My hope as well…would have been all in @ 1.5…a tiny bit hesitant at 1.3. Sold all of my 0% I-Bonds last month in anticipation of this.

As I have no I-Bond purchases in 2023 so far, I am tempted to pull the trigger on 11/28 and then wait until April 2024 to see if that is the right time for my 2024 allocation.

Sounds like a good plan. May as well max out your 2023 allocation at the highest available fixed rate for the year before that window closes forever. I bought $5K in April so I’m going to do another $5K in December, earning 5.12% in a sweet MM account until then. 🙂

Good move, seems to me.