By David Enna, Tipswatch.com

We’ve entered a new era. That’s what Bloomberg’s ever-thoughtful Tom Keene repeated over and over in Wednesday’s coverage of the Federal Reserve’s interest rate forecasts. “This is a sea change,” he said. “I have to emphasize how important this is.”

What exactly did the Fed do? It held the federal funds rate at the current level (target range of 5.25% – 5.50%) and signaled strongly that it is likely to cut short-term interest rates three times in 2024, beginning as early as March. This wasn’t unexpected, but the Fed was unusually firm in declaring that we’ve entered a new dovish era of interest rates, after nearly two years of unprecedented increases.

The Fed projections settled on 75-basis-points of rate cuts in 2024, but the stock and bond markets clearly anticipate something larger. Both markets soared Wednesday and into Thursday, with the Dow average hitting an all-time high and bond yields falling dramatically.

Significantly, however, the FOMC also reiterated its intention to continue lowering its massive balance sheet of U.S. Treasurys. It said:

In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

This is an important tidbit of news, because it means that while the Fed will be easing on the short-end of the yield curve, it will continue tightening on the longer end by allowing Treasurys to mature and roll off the balance sheet. That is quantitative tightening, and it should support longer-term yields.

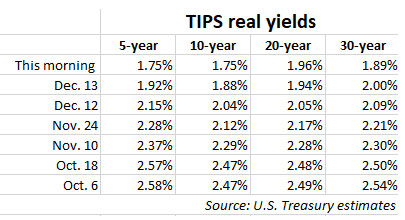

As a result, you should see a widening of the yield curve, with yields on shorter maturities falling, but rising or holding stable for longer maturities (or at least not falling as far). This was immediately evident in the way the Fed action rocked Treasury real yields:

I created this chart at about 9:10 am ET and 15 minutes later the 5-year real yield had fallen to 1.74% and the 10-year to 1.72%. There’s no way to say exactly how far this could go. But it is significant because the Treasury will be auctioning a reopened 5-year TIPS on Dec. 21 and then a new 10-year TIPS on Jan. 18, 2024. Both of those auctions could result in much lower real yields than we have seen in recent months.

The “sea change” nature of the Fed’s pronouncements can’t be underestimated. This morning, the U.S. dollar index is trading at 102.14, down about 2% since the Fed’s announcement at 2 p.m. Wednesday. A fall in the value of the dollar has an inflationary effect, especially on commodities. So it shouldn’t be a surprise that crude oil prices are up 3% this morning.

What this means for TIPS

I don’t think the Fed’s action is dire news, but it will mean lower real yields on near-future TIPS investments. We aren’t heading anywhere near the negative-real-yield fiascos of the recent past. And if the Fed continues lowering its balance sheet, the yield curve should steepen, making longer-term TIPS relatively more attractive.

The Fed must be fairly confident that inflation is indeed tamed, and it also must see some weakening in the U.S. economy. Both of those factors support lower interest rates. But if the Fed is wrong, inflation could surge again. That danger makes TIPS attractive, even if real yields decline.

One thing to celebrate: All the TIPS you currently hold rose in value yesterday as yields plummeted. The net asset value of the TIP ETF surged from $105.30 just after 1 p.m. Wednesday to $107.51 this morning, a gain of 2.1% in less than 24 hours. Of course, we are all buy-and-hold investors, right? Ignore the noise.

What this means for T-bills

Yesterday, the Treasury auctioned a 17-week T-bill that got an investment rate of 5.432%, up from 5.421% the week before. That could end up being the highest yield we will see at that term for quite awhile, but so far T-bill yields have been holding up relatively well.

The 3-month T-bill is yielding 5.36% this morning, down just 10 basis points from two days earlier. That indicates investors don’t see rate cuts happening within the next three months. Seems logical.

The 12-month T-bill is yielding 4.86%, down 27 basis points from two days ago. In this case, investors seem to be pricing in a partial year of rate cuts. Also “somewhat” logical.

And the 2-year Treasury note? It is yielding 4.37% this morning, down 34 basis points this morning. That seems attractive to me. But remember, the yield curve should grow steeper as the short-term yields fall. And also keep in mind that the market was already pricing in future rate cuts, ahead of the Fed announcement.

Final thoughts

Is inflation really tamed? That will be the key question. If you listened to Jerome Powell’s news conference, you didn’t hear that definitive statement and in fact he repeatedly stated that inflation remains a concern. But I think the Fed feels satisfied that it can gradually get to a “neutral” short term interest rate of about 3% without causing inflation to surge.

The Fed has been wrong before. But in this case I think it was time to begin very gradually easing short-term interest rates, while maintaining the commitment to lowering the Fed’s swollen balance sheet.

What are your thoughts? Do the lower real yields sidetrack your investment plans? Are short-term Treasurys and money-market funds starting to look less attractive? Will you make a move to stretch out duration? Post your ideas below.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Questions surround this week’s 5-year TIPS reopening auction | Treasury Inflation-Protected Securities

So what could have happened between October 18 and now that flipped expectations 180 degrees? Who knows? Who can tell?

(my memory is bad – so this is just to illustrate a point)

Bill Ackman, a BIG FISH speculator swimming in an ocean of individual investors to be had, maybe tweeted that he bought exactly at the right time or roughly and maybe tweeted that he sold in time as well, that is, exactly at the right time……..whereas some other speculators maybe Jamie Dimon went public with their interest rate forecasts / speculations that it will top 7% or maybe more………..I am sure Jamie & co made big bucks too no matter which way the bond market went – north or south………..who can tell why they say and do ON AIR what they say and do? (hint: money honey)

The FED is scrambling to find out what happened within such a short time that didnt happen in such long time………….

To date, nobody knows why the stock market keeps on going up and up and away, rising from the depths at 6k to 34 – 35+ k as of today…many are speculating, but who can tell?

In Las Vegas, who can tell why the ODDS are in favor of the house, more often than not? (hint: the house?)

I have low risk tolerance. My attitude is take chips off the poker table and buy Cd’s when your winning.You wont get rich but you will not lose your principle investment amount.I have been buying Cd’s for past 20 years. Not popular amongst the high flying risk takers out there. I had a 52 week tbill ladder ,bought in 2022, having maturities of 5/23,9/23 and 12/23. My goal was to lock into 5 year Cds ,through Schwab , when they matured at 5%. I was lucky, in my opinion , to get 4.45%, 4.65% and 4.45% as the laddered 52 week tbills matured. I think I will not lose principle to inflation in the next 5 years, hopefully, with the fed getting inflation down to 2.5%. I also bought a 5 year tips in April 2022 that I will hold to maturity in case inflation remains at the current level or rises. I can sleep at night for the next 5 years. Longevity is something to think about when buying Cds.I enjoy this sight and have been learning from all of you.Bears make money, Bulls make money and Pigs get slaughtered.

Well said.

Your approach of CD’s, T-bills and low duration TIPS ensure peace of mind – I think you got this formula right – after all, peace of mind and happiness is really what everyone is seeking but trying to find it in the WRONG PLACE, lose it.

Co-mingling money in the same place as BULLS and BEARS (the BIG FISH) who know how to disseminate information to their advantage even though it doesnt take on that OUTER appearance, the small fish scramble and follow them (herd instinct) to the advantage of the BIG fish waiting to have it all.

The BULLS and BEARS (big fish) then TIME their trades to their advantage, the PIG gets slaughtered (small fish gets eaten up) for not knowing what the BIG FISH is saying and doing – two different things mostly.

FED and SEC scramble coming up with newer and newer solutions to same old same old problems (SEC i recall vaguely from news says that they will be intermediary vs. banks in treasury trades due to some liquidity type of problems that makes the 30+trillion or so treasury market go yo yo – thanks to THE HOUSE of BULLS and BEARS and current intermediaries also HOUSE?)

Your CONSERVATIVE INVESTMENT approach is a TESTIMONY that there is SO MUCH PEACE and JOY to be had in CONTENTMENT of mind than in CROWD mentality / HERD instincts in following BIG BULLS and BIG BEARS in GREED / FEAR day-trades which instincts and emotions on the part of the HERD the HOUSE of BULLS and BEARS can easily MONITOR, trigger and/or manipulate at will and DAY-trade away to their advantage!

In a SELFISH WORLD of BIG FISH, TIPSWATCH is a VERY RARE BLOG that caters to the small fish by selflessly disseminating USEFUL INFORMATION for BUY/HOLD investing to ensure the small fish make WELL-INFORMED decisions with their hard-earned money / savings!

This BLOG is SHINING a LIGHT in this corner of the world!

Is the individual investor correct? Is FED correct? Is the market (herd) correct?

TIME is the only giver of CORRECT answer.

Until TIME arrives, someone or other is correct in their speculation and assumptions until TIME proves them wrong.

I am considering a mix. Mid duration very high quality corp bonds and 5-10 tips. I am adjusting to the recent news and still unsure about how quickly to act. My conservative nature will probably move in stages. I haven’t found my crystal ball yet!

Thanks, David, for your timely and insightful analysis. I was quite surprised to see how much yields declined, and wonder if we might get at least a small bounce. At least for the short term, I won’t be participating in any TIPS auctions, although I may buy on the secondary market if the prices are right. Other than that, I will stick to my plan to purchase the current I-bonds before next May, as I agree with others here that this is likely the highest fixed rate we are likely to get in the near future. As for treasuries, I’ll probably stretch them out a bit but I’m unlikely to go for anything with more than 5 years duration.

I think the strategy to actively buy more T Bills when my currently owned T Bills mature, at least for the next 9 to 12 months, seems good to me. In terms of maturity, I feel more comfortable to stay within the 2 years time frame, unless I see surprises on the upside for inflation/rates with longer maturities.

I’m tending to agree with Ann that current I-bonds seem more attractive than TIPS. I was going to wait for higher fixed rates before purchasing but that all changed on Wed. afternoon. There was a headline on Bloomberg that read ‘Investors Baffled After Powell Comments’ and you may consider me as one of the baffled. I’m not sure what if anything happened over the past two weeks to render such an ‘about-face’ in Powell’s policy stance. I’ve come up with three possibilities: 1) Powell sees/knows something that we don’t about looming threats to our economy.

2) This is all about 2024 being an election year and Powell wants to set a predicate for rate-cutting now.

3) Powell perhaps felt that he’d already lost some credibility with markets and any hawkish notes on his part would make it worse. Still, I don’t see how any of these reasons (even the 1st) justify the dramatic loosening of market conditions that Powell had to know would ensue. Like I said, I’m baffled. On some counts, I think the likelihood of more inflation (and ultimately higher rates) just increased.

I guess there is a limit to how much control the Fed can have on a narrative. Facts and data were on the side of market’s projections and that all have a way of wearing down even the all mighty Fed. And, of course, their credibility is so near and dear to them for their future narratives.

If the economy is currently as robust as all the pundits claim it is, with much lower inflation, low unemployment, labor participation increasing, and productivity and growth both going well, all occuring in the face of the highest interest rates in years, then why would the Fed need to cut rates not one, or two, but THREE times next year? Feels like they know things might be slowing more than the market expects. Or is it due to the fact that the Treasury’s financing needs are going to be massive in 2024? Also…two trivia notes: the longer the yield curve stays inverted, the harder the market can fall, and markets also tend to peak right before rate cuts begin. We’re currently still in one of the longest inversions ever. But maybe, “this time is different?”

Fact I found yesterday: The U.S. public debt stands today at $33.8 trillion. One year ago it was $31.3 trillion. That is an increase of 8%. And that means 8% greater need for Treasury funding, along with higher total interest costs. So mid- to longer-term Treasury yields can’t really fall that far, I think.

I agree with your take. Given the fact that the incumbent president is not doing well in the polls, I will not be surprised if there is another or additional fiscal stimulus.. Both of these factors make it a bit harder for me to buy BND, with 6.1 years duration, when I can make risk free, state tax exempt guaranted decent return, with active management, from T Bills. With my wife having recently and suddenly been laid off, negative returns is not an option….only if I could control it…..🤓

And it seems Treasury is relying on short term funding, even though more expensive then longer term bonds. IMHO they know if they extended maturity they would not be able to maintain the low long term rates in the face of increased supply.

You asked “What are your thoughts? Do the lower real yields sidetrack your investment plans?” The Fed’s “sea change” swamped my plan to buy a TIPS ladder. When I first started making the plans and moving some things around it was early October. But I wasn’t ready until a few weeks ago. Meanwhile I watched as the cost of the ladder I planned to buy on the secondary market started going up daily. It’s probably still a decent deal in “real” return terms and I do believe inflation will be an issue over the next 30 years, but I find myself dragging my feet upon the recent Fed news. I’m a conservative investor, so I’ll also be sad to see short-term Treasurys and money-market funds pay less. I will keep reading and learning (and probably missing out, per usual!).

Timing always is difficult, and this is why I was preaching urgency. However, I filled most of my TIPS ladder a month of two before the peak, when yields were higher than they are today, but not at the peak. And I am OK with that. Today’s real yield curve ended up about 1.70% to 1.80% above inflation, still good. If you have other stock and bond investments, you have had a good week.

David and others, I am not a fan of buying bond ETFs or Mutual Funds. However, given the gains others have already experienced with these products in the last few days, do you think it is still a good buy for something like BND (that you shared that you own/owned) with the interest rates expected to fall more at least for the next couple of years. Given how fast the interest rates have come down, I worry that they may bounce back a bit. And with BND duration of about six years, buying now could be a bit risky though long-term it may not matter? I am weighing buying such an ETF, in addition to US Treasury Bills. Pros and cons of such an addition will be very helpful….thanks!!

My wife and I both own BND as a core holding in retirement accounts. We don’t trade in and out, except to re-balance when needed. We didn’t sell when it declined strongly in 2022 (didn’t expect that much pain) and instead balanced into it at times when stocks were high. It is currently yielding about 4.6%. It looks attractive now, I agree, but it’s impossible to see what’s ahead.

Thanks!!!

I will be locking in +6% interest rates with multi-year guaranteed annuities (MYGA) very soon. To be safe, I will stay under my state’s insurance guaranty association coverage limit.

MYGA’s don’t have inflation protection (that I know of) but locking in is an option.

I’m still liking TIPS funds or Ladder for my “bond” AA plus state-tax free.

Unions are making hay lately (and min wages going up in many states) … that will show up soon enough in prices; although, yes Union work is only a few % of GDP.

I ask: If the FED misread initial inflation as “transitory”; could the current reduction in inflation actually be the “transitory” event?

My take, yes, current reduction in inflation could be transitory. Any unexpected events such rise in oil prices, supply chain interruptions due to some escalating war, etc. etc. can reverse the narrative. However, given what we know today, it seems unlikely.

Thanks, David, for your analysis. A few observations about the FOMC and its Summary of Economic Projections (SEP) and its “usefulness” for forward guidance. The median projection is the construction of all the guesses for the ideal stance of monetary policy by yearend 2024. The number could be read as up to three 25 basis point cuts. But the FOMC did leave the door open a crack to “any” tightening of monetary policy IF inflation rears its head in the first half of the year. Suppose it decided it needed to raise by another 24 bps in January, for instance. That might mean 100 bps to cuts in second half of the year to get down to 4.6% median target. And that could come in four 25 bps or one 50bps and then two quarter-point cuts. So, we will need to watch FOMC actions more than any “forward guidance,” which could be just a head fake.

p.s. wordpress wouldn’t let me complete its transaction! Tried signing in with email or google account. Neither worked!)

>

Good points, thanks. Sorry about the WordPress glitch.

If lower TIPS rates persist or drop further, the 1.30% I Bond fixed rate looks even more attractive. I’m considering opening some additional TreasuryDirect trust accounts in order to sell my long term TIPS and replace them with I Bonds before it rate resets (to a likely lower rate) in May 2024.

Hi David, your analysis and summary, as always, is super timely and priceless. I agree with all your takes. Yes, we need to adjust our expectations on the risk-free US Treasuries yields. Before the FOMC meeting and the press conference, I was adjusting in my mind for around 4% in 2024 and 3% in 2025, both nominal. If inflation is slowing as Powell said, I may have to take my expectations even down a bit more. However, for the purposes of income, staying at the short end of the curve for the next 12-18 months makes sense for me. I hope the yield curve steepens enough to make longer duration yields more attractive. We have time and need to monitor and adjust.

Powell’s comments on his sensitivity, rightly so, for real yields made me think about TIPS and I Bonds. Thanks for your up to date table. You have helped me learn as to where to look for what when it comes to monitoring inflation. Love it!!

You did not say anything on I-Bonds fixed rate impact. I reiterate my belief that 1.3% fixed for I-Bonds is the peak, unless inflation flares up again (though this could bring real yields down). Hence, I can not wait to buy them in a little more than two weeks and get the clock started. In case no one has noticed, I need to work on my patience….OOOOOm…:)….best