By David Enna, Tipswatch.com

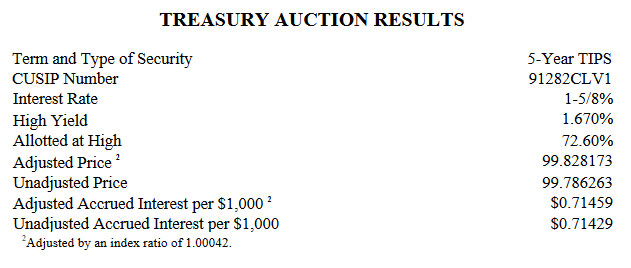

The Treasury’s offering of $24 billion in a new 5-year TIPS, CUSIP 91282CLV1, auctioned today with a real yield to maturity of 1.670%, the lowest for this term since April 2023.

This one is a bit hard to read because of the unusual nature of the October TIPS auction each year, which almost always gets a real yield below the apparent market rate. I talked about this in my preview article on this auction.

The Treasury’s estimate of the real yield of a full-term 5-year TIPS closed Wednesday at 1.82%, but yields have been sliding lower this morning. The most recent TIPS on the secondary market, maturing in April 2029, was trading at about 1.76%. But the new TIPS auctioned each October gets a lower real yield than the April TIPS because it won’t be exposed to weak non-seasonally adjusted inflation in its closing months to maturity.

The key number to look at is the “when issued” prediction for this auction, released just before the close. That number predicted a real yield of 1.641%, so today’s auction result came in higher than expected at 1.670%. The bid-to-cover ratio, a good indication of investor demand, was 2.40, below recent auctions of this term. All of that indicates investor demand wasn’t strong.

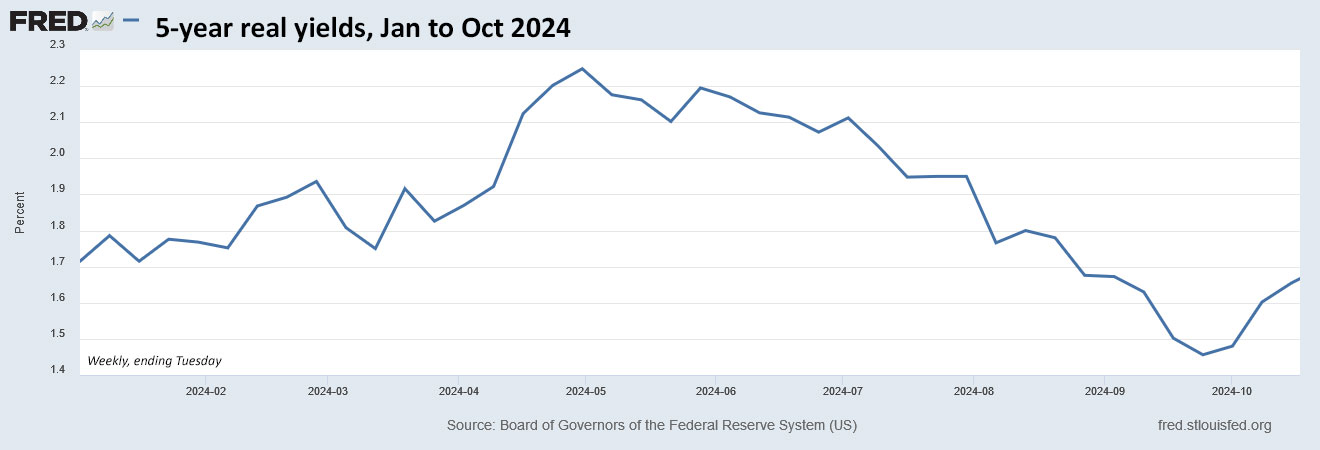

The October auction is always a bit of an outlier. Here is the trend in the 5-year real yield through 2024, showing the sharp decline beginning in May and then reversing in late September:

Pricing

This was a new TIPS, so the Treasury set its coupon rate at 1.625%, one notch below the real yield of 1.670%. It will carry an inflation index of 1.00042 on the settlement date of Oct. 31. All this means investors got it at a slight discount, an unadjusted price of 99.786263. Here is how a purchase of $10,000 par would be priced:

- Par value: $10,000.

- Principal on settlement date: $10,000 x 1.00042 = $10,004.20.

- Cost of investment: $10,004.20 x 0.99786263= $9,982.82.

- + accrued interest of $7.15.

In summary, an investor purchasing $10,000 par paid $9,982.82 and will receive principal of $10,004.20 on Oct. 31. The accrued interest will be returned at the first coupon payment.

Inflation breakeven rate

With the nominal 5-year Treasury note trading at 4.01% at the auction’s close, this TIPS gets an implied inflation breakeven rate of 2.34%. I say implied because of the unusual nature of the October auctions. Maybe a better estimate would be around 2.29%. If anyone can find a more-official number, let me know.

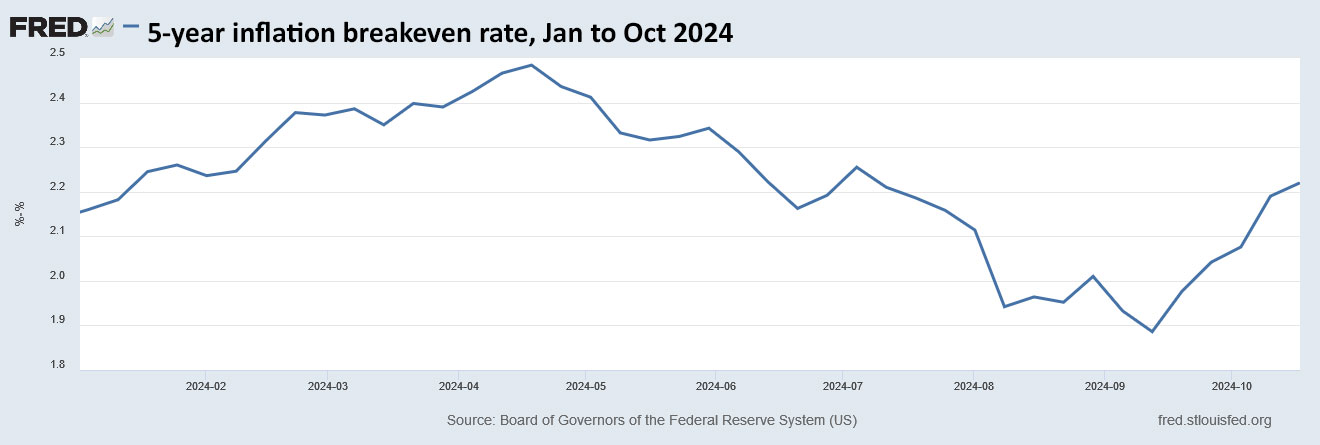

Here is the trend in the 5-year inflation breakeven rate through 2024, showing a recent surge in inflation expectations:

Thoughts

TIPS yields were trending slightly lower on Thursday morning, after three weeks of increases. Today’s auction result of a 1.670% real yield looks attractive, despite the appearance it was below the “market.” That’s just the way this October auction works. But it is below the results of October auctions in 2022 (1.732%) and 2023 (2.440%).

No media service covers TIPS auctions live anymore, but I found this snippet a day later from MarketWatch, via MSN, on Friday:

Treasury’s $24 billion auction of 5-year Treasury Inflation-Protected Securities was weak, with below-average bidding by non-dealers, according to BMO Capital Markets strategist Vail Hartman.

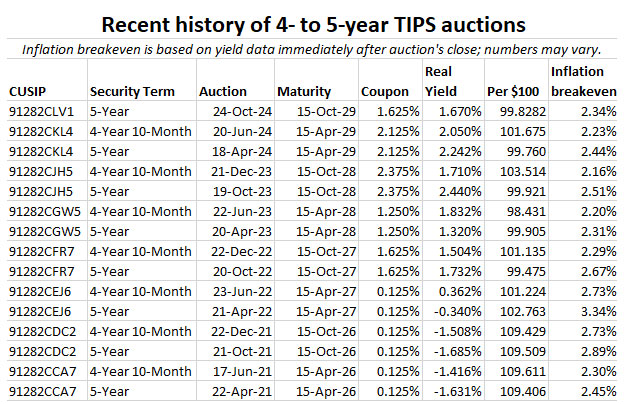

This TIPS will be reopened at auction on December 19. Here are results for recent auctions of this term, showing the transition from real yields deeply negative to inflation in 2021:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Weak demand results in real yield of 2.121% for 5-year TIPS reopening auction | Treasury Inflation-Protected Securities

Pingback: Rise in real yields (once again) makes 5-year TIPS auction look attractive | Treasury Inflation-Protected Securities

Pingback: Real yields seem to have crested the peak. What’s next? | Treasury Inflation-Protected Securities

How is it possible that the CPI is at 2.4 and the breakeven is at 2.3? Does not make a lot of sense to me.

There is a huge disparity between real inflation and breakeven from one year ago to now.

2022 had an annual inflation of 6.5, and the breakeven by the end of the year was 2.26 (lower than now).

Even though I understand breakeven inflation is the expectation of inflation, this would not be a reasonable expectation.

I see more a supply/demand trading type of issue.

When people say that the breakeven rate “forecasts” future inflation, I say: Look back to June 2013, when the 10-year inflation breakeven rate was 1.96%. In reality, inflation averaged 2.7% over the next 10 years. Or look at the 5-year inflation breakeven rate in Jan 2019, when it was 1.50%. Inflation averaged 4.1% over the next 5 years. It is just a measurement of sentiment, and of course it can work in reverse, trending lower than reality at times.

Yes, I get that. My point is that as of right now, I do not feel the sentiment or the expectation should be higher for inflation than at the end of 2022, meaning that the owner of the TIPS in the secondary market is not willing to sell at close to 2% of real yield (which would be a breakeven of 2.2). He thinks he can sell it for 1.9% real yield and that is what is driving the breakeven and the price now. That is why I feel it takes a longer time for TIPS to adjust to changes in the 10-year bond price. The market must be somehow concentrated in a few hands and this guys simply adjust slowly (to their advantage I would think) to changes in price. This is my feeling but not sure how marketmaking works for TIPS.

Thank you for this. I particularly appreciated the clear explanation of coupon rate vs real yield.

David, does the 5yr forward yield % on FRED help to forecast the 5yr return on a TIPS vs 5yr nominal Treasury note?

5-Year, 5-Year Forward Inflation Expectation Rate (T5YIFR) | FRED | St. Louis Fedhttps://fred.stlouisfed.org/series/T5YIFR

I would say no. I don’t track the 5-year forward metrics, but I believe that measurement is trying to measure sentiment about inflation *after* the next five years, meaning inflation in years 6 to 10. The 5-year standard inflation breakeven rate, currently about 2.33%, is the best measurement of potential returns of TIPS vs. nominal. See my TIPS vs. Nominals page where I track maturing TIPS: https://tipswatch.com/tips-vs-nominal-treasurys/

Same here.

My first time buying TIPS on auction. Will see how they peform over the next 5 yrs and compare to the 5 yr T notes that I bought about 4-5 months ago.