By David Enna, Tipswatch.com

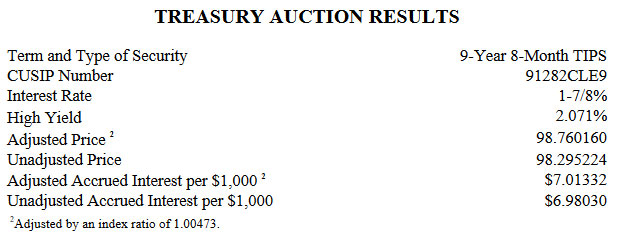

The Treasury’s reopening auction of a 10-year Treasury Inflation-Protected Security — CUSIP 91282CLE9 — generated a real yield to maturity of 2.071%, right in line with where this TIPS was trading this morning on the secondary market.

This TIPS has a 9-year, 8-month term and carries a coupon rate of 1.875%, which was set by the originating auction on July 18. Shortly before the auction’s close it was trading on the secondary market with a real yield of 2.07%, so the result looks on target. But the “when-issued” prediction was 2.05%, so demand might have been a bit weak. The bid-to-cover ratio was 2.35, also a bit weak.

In a short article on the auction, Marketwatch noted it produced “lackluster results.”

However, for investors, a real yield of 2.071% looks like a good result. An earlier reopening for this TIPS, on Sept. 19, got a much lower real yield of 1.592%.

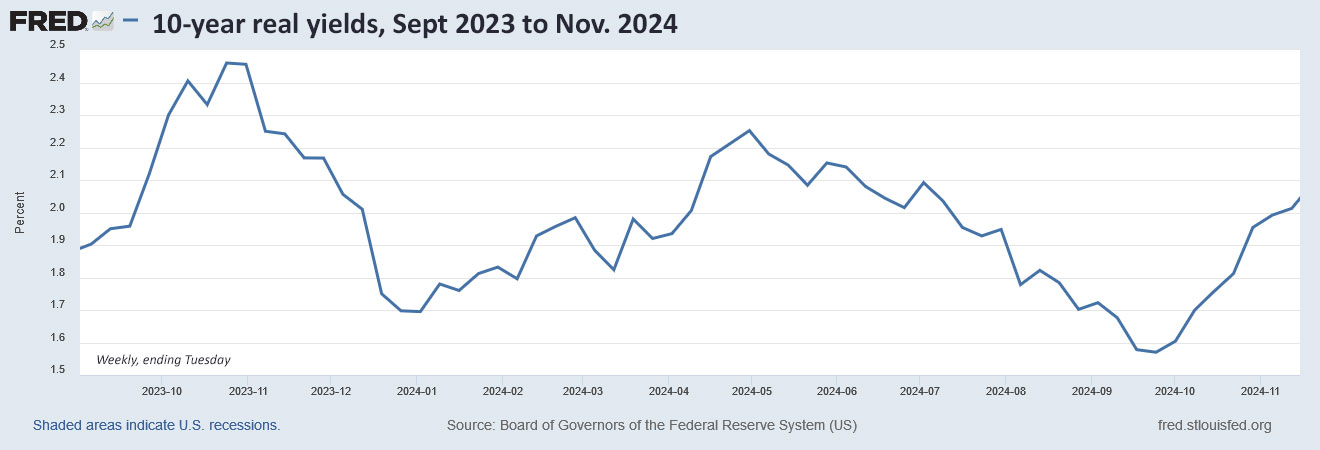

Here is the trend in the 10-year real yield over the last 14 months, showing the peak in October 2023 and the recent surge higher:

Pricing

Because this TIPS auctioned with a real yield higher than its coupon rate, investors got it at a discount, an unadjusted price of 98.295224. In addition, it will carry an inflation index of 1.00473 on the settlement date of Nov. 29. With that information, we can calculate the cost of a $10,000 par investment:

- Par amount: $10,000.

- Principal on settlement date: $10,000 x 1.00473 = $10,047.30

- Cost of investment: $10,047.30 x 0.98295224 = $9,876.02

- + Accrued interest of $70.13

In summary, an investor purchasing $10,000 par of this TIPS paid $9,876.02 for $10,047.30 of principal on the settlement date on Nov. 29. From that point on, the investor will receive annual interest of 1.875% on adjusted principal, which will grow with future inflation.

Inflation breakeven rate

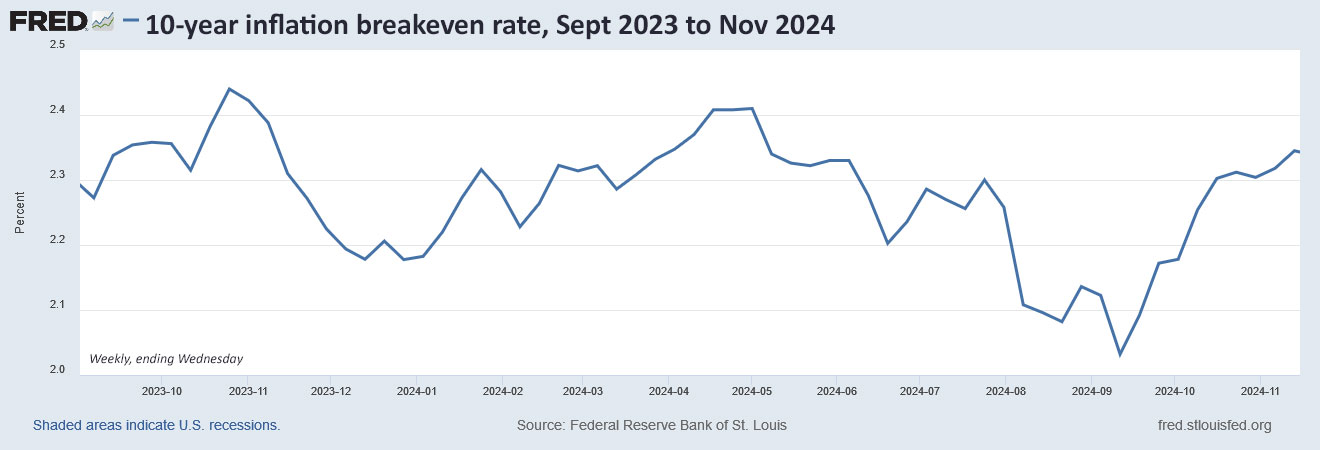

With the 10-year nominal Treasury note yielding 4.42% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.35%, a bit higher than recent results. This reflects growing uncertainty about future inflation at a time of a strong economy, strong stock market and very high U.S. budget deficits.

Here is the trend in the 10-year inflation breakeven rate over the last 14 months, showing the sharp upward trend in the two months leading to the U.S. presidential election:

Reaction to the auction

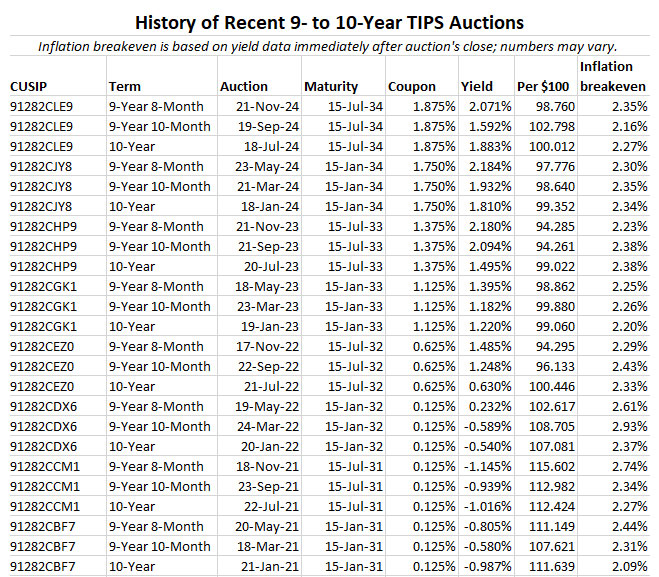

This was a good result for investors, easily clearing the coveted real yield threshold of 2.00%. Since January 2009, there have been 92 TIPS auctions of this term and only four have generated a real yield higher than 2%. Real yields could certainly continue going higher, but for a buy-and-hold investor a yield higher than 2.0% looks like a solid investment.

This was the last TIPS auction of this term for 2024. A new 10-year TIPS will be auctioned on January 23, 2025. Here are results for recent auctions of this term:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

2% above inflation on US Treasury backed dollars is certainly good and safe by long term measures.

Sorry, a little off topic – but, the way real yield is calculated on the secondary market seems nuts to me. To get those 2+% real yields on 1.75% TIPS from January of this year, brokerages are using TIPS prices where the time is “re-winded” to eleven months ago. In reality, the actual today’s price is adjusted for inflation so the purchase price is higher. The “real yield” between today and bond’s maturity date is barely better than what coupon says.

I understand the time difference and future inflation and all that but looking from the perspective of “adjusted price today” vs “100”, almost a 0.25% difference.

Can you elaborate on this? I don’t follow the brokerage pricing issue.

The secondary market price is adjusted for inflation accruals since issue, so you are buying more principal per unit than you would have at issue. Instead of buying $1000 of current (issue date) dollar principal at issue, perhaps you are buying $1020 of current (today) dollar principal on the secondary market nearly a year later. The cost is relatively higher for the same YTM, but that is because your principal is greater.

Inflation factors for the oldest TIPS are around 2. Each unit is about $2000 of current principal instead of the original $1000 when they were issued. If you bought these, you’d be buying fewer units for a given current dollar value than if you bought newer issues with the same maturity date.

I completely agree about buying more principle. It is just the convoluted multi-step way of looking at the instantaneous current “real yield” that drives me crazy. Here is an example to clarify my point:

91282CJY8 matures on 1/15/2034. Lets use 11/29/2024 as the purchase date:

Unadjusted price: 98.609 – 1.92% real yield – (they are using 98.609 and 100 at maturity and the original 1.75% to get this yield)

What we would actually pay today is:

Price 101.15

Now, there are 3 possibilities:

If the inflation keeps going up with the exact same trajectory or higher as it did between 1/15/2024 and 11/29/2024, then yes, we would get something very close to 1.92%, so called “real yield”.

If the CPI “freezes” tomorrow at 101.15, we would only get 1.75% (the original coupon rate). Because the price at redemption will be 101.15. Technically, there is no problem – “real yield of 1.92%” on 11/29/2024 is correct. But, we would not be getting 1.92% on 1/15/2034, the “future yield” on that date will be 1.75%.

If there is extreme deflation, we would then only get 1.61% yield because the price at redemption will be 100. (I realize that this is no longer “real yield” considering that the date and prices keep changing)

So, technically the definitions and calculations are all correct. I just think it is odd to be thinking about “quoted real yield” in terms of prices at auction origin date, when the purchase on the secondary market is done on some other date.

Maybe if the term specifies “real yield right now, based on prices at origin”, nitpicky people like me will be happy, lol.

You can pretty much ignore whatever happened between Jan 15 and Nov 29, because you are buying inflation-adjusted principal. And you are buying that principal at a discounted price of about 98.20. So, if inflation was absolutely zero through the rest of this term, you would earn 1.75% on your adjusted principal, which you bought at a 1.8% discount. Roughly speaking, divide 1.8% by 9 years and you get a 0.2% yield bonus, and if you add 0.2% to 1.75% you get to 1.95%, pretty close to the real yield you are quoting. The real yield is correct, even if inflation is zero.

I bought CUSIP 91282CLE9 at 1.875% in July. I can buy it for $98.453 on the secondary market on the Fidelity portal (yield =2.052%). Maybe I will buy eight more. I am cashing in my equity gains. Money market funds can’t deal with the inflation risk.

Agree that is an excellent option. I bought that same at re-auction and recently on the secondary market also just over 2%. Time will tell but there are several inflationary forces working in favor of increased future inflation. And the underlying 10 year Treasury has a reasonable yield partly from the term premium which is finally above zero..

I bought the eight bonds. Yields have dropped five basis points.

David Enna had written of buying TIPS on the secondary market instead of buying TIPS at auction year-by-year. His plots show that TIPS yields are in a comfortably high range right now.

I don’t have a bond ladder in mind: I am going to buy bonds of various terms to preserve my nest egg. I could not understand David’s buying guide, so I am just going to buy low coupon bonds for now because I don’t need the cash flow.

TIPS are a complex investment, but if held to maturity there really is no risk except for “opportunity costs” for people who tend to worry about past decisions. Right now, with real yields are around this 2.0% level or above, TIPS are attractive.

It is indeed a safe place. Thank you, David and Sean. I guess you could say I’m first call ready but hoping for a longer runway (God willing and the creek don’t rise).

David, for 1 bond I paid $994.61 at auction and I’ll get $7 back in accrued interest with the first payment, taking it to $987. Do I have that right?

This sound right.

Thanks for the analysis! I picked up one on the secondary market just before closing. Higher coupon should help with the “phantom income” tax.

Thanks as always for the quick analysis. Is it typical to lose value on the secondary market so soon after auction? Fidelity says it is -0.0765 or 98.43 at the time of writing (2 pm EST 11/21/24). Fully intend to hold to maturity, but (in a bull market especially) it can make you feel that inertial creepiness you get when you take the fork left and every other hiker is going right.

Separately, I really appreciate you sharing some of your choices in broad strokes. Knowing that this is out of scope (but feeling like this is a “safe place”), can I ask if you follow a similar thought process to select munis? Mish mosh ladder of those myself (in a high tax state w/tax eq. 6% +/-.5) along with TIPs, annuities sprinkled in.

Don’t fret the fluctuations. I am still seeing this TIPS trading this afternoon with a real yield of 2.07%, but it is going to fluctuate, all the time, up and down. If you are holding to maturity, so what? My TIPS purchases maturing in 2034 had real yields at purchase of 1.81%, 1.89%, 2.04% and 2.01%. So your purchase today beat all of those. … I don’t invest in munis at all and so I have no opinion on that investment.

I also have a Muni portfolio constructed over the last 18 months. My results are similar – about 6% tax-equivalent yield using General Obligation munis – half from CA and half from various cities.

One issue I faced was that the Muni yield curve is upward sloping such that the best yields are for durations longer than my anticipated high income. An investor with a longer runway could do better.

I have been advised by several sources to expand my search to include higher quality Revenue bonds like utilities.

One great resource:

https://www.raymondjames.com/wealth-management/advice-products-and-services/investment-solutions/fixed-income/bond-market-commentary-and-analysis

Hope that helps..