By David Enna, Tipswatch.com

My philosophy of investing is pretty simple: Stick to your asset allocation, layer in some inflation protection, and avoid undue risk, especially in your fixed-income holdings.

So for fixed income, I am a fan of low-cost, intermediate-term funds like Vanguard’s Total Bond, paired with holdings of I Bonds, individual TIPS, nominal Treasurys and CDs. Safety is the key. That is my approach. And I take a skeptical approach to anything “new and improved.”

Back in the fall of 2020, I was getting a lot of questions about a new ETF with a tongue-twisting title: the Quadratic Interest Rate Volatility and Inflation Hedge ETF. Everyone knew this fund by its ticker: IVOL.

The ETF’s creator, Nancy Davis of Quadratic Capital, was hailed as an innovator for this fund. Barron’s named her one of its top 200 Women in Finance in March 2020. But for me, IVOL was never particularly attractive. It was very new, with just a year of trading history. It was a fixed-income fund with a 1% expense ratio and a complex hedging strategy I couldn’t understand. Some readers disagreed with me back in August 2020:

The author does not like IVOL because of reasons such as “too new” and “expense ratio.” But you can look at the results and decide for yourself… Since the March 2020 lows for TIPS in general IVOL has out-performed the ETF-TIP.

I look at the results of a fund — yield, price growth, volatility and drawdown. So far so good with IVOL on all four. If a fund is performing well, I have no problem paying a higher expense ratio.

The interesting thing about IVOL is that it holds about 85% of its assets in SCHP, Schwab’s U.S. TIPS ETF, a high-quality full-maturity-spectrum TIPS fund. On top of that, it overlays hedging strategies that seek to benefit from interest rate volatility. Quadratic’s information on the fund includes this summary of its strategy:

IVOL is a fixed income ETF that seeks to hedge relative interest rate movements, whether these movements arise from falling short-term interest rates or rising long-term interest rates, and to benefit from market stress when fixed income volatility increases, while providing the potential for enhanced, inflation-protected income.

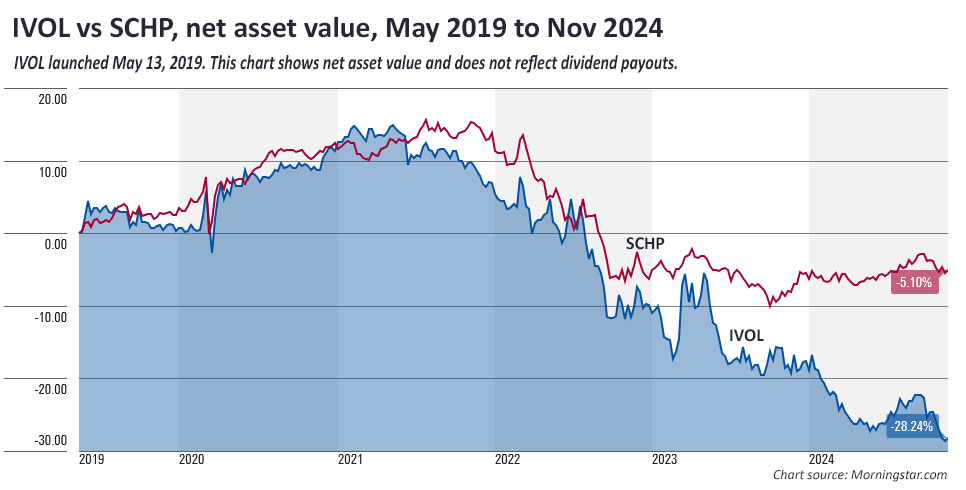

Since IVOL launched in May 2019, we’ve certainly had a lot of interest rate volatility, both up and down. For a time during the early days of the Covid pandemic, IVOL benefited from interest rates falling dramatically. But then in 2022, the Federal Reserve began raising interest rates aggressively.

Rising interest rates aren’t good for any bond fund, but IVOL was especially hard hit in the last two years, as shown in this chart:

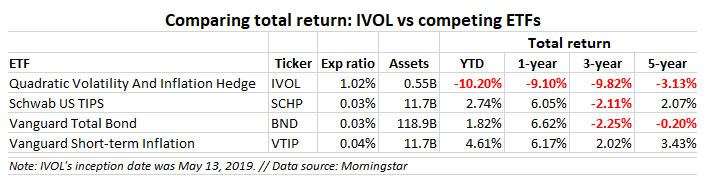

Remember, IVOL holds 85% of its assets in SCHP, but has an expense ratio about 34x higher than SCHP, 1.02% versus 0.03%. Here is a comparison of the total return for IVOL over the last five years versus SCHP, the total bond market ETF (BND) and Vanguard’s short-term TIPS ETF (VTIP).

In a year when bond funds have been rising in total return, IVOL’s total return, including payouts, has declined 10.2% in 2024 and is much worse across 1-, 3- and 5-year periods. My conclusion: IVOL’s hedging strategy didn’t work in a rising interest rate environment.

Why was it so hot four years ago? Because in 2020 it had a total return of 14.6%, versus 10.9% for SCHP. Investors saw that and flooded into the fund. During that time, IVOL’s assets under management surged to $3.5 billion. Today, that is down to $547 million. Morningstar gives the fund a “negative” rating, noting:

Fees are a weakness here. The strategy’s lofty fees are a high hurdle to clear. … Over the past three years, it trailed the category index, the Bloomberg Barclays U.S. Treasury Inflation-Protected Securities Index, by an annualized 7.7 percentage points.

The lesson

It is smart to be dull. I try to keep my investment allocation simple and want safety and predictability in my fixed-income investments. When something “new” and “better” and “smarter” comes along, I am highly skeptical. Let’s see how it performs over time.

IVOL was touted in 2020 as the “great new idea” for inflation protection, but it hasn’t delivered. It was supposed to gain from volatility, but instead did poorly at a time of high volatility. The high expense ratio and untested hedging strategies didn’t work for investors.

At this point, I have no investments in any TIPS funds or ETFs. Over recent years, the one fund I have recommended (if anyone asks) is Vanguard’s Short-Term TIPS, VTIP, which has low volatility and therefore tends to track inflation better. There are no tricks to that fund. It has a 4-star gold rating on Morningstar, which says: “Great inflation protection at a low cost.”

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

“Innovation” in finance is a contradiction of terms.

Good morning, new reader here. Can you please make the bearish case for a CEF selling at a discount to NAV, that uses leverage, if interest rates drop? Thank you and Happy Holidays to all!

I don’t invest in closed-end funds (and have no expertise in them), but they generally do trade at a discount to NAV, sometimes sizable. The leverage could be used in part to continue level payouts over time. (Years ago I invested in an NC municipal CEF and it was under water for years but eventually came back and I sold. And a few years later it was closed.)

Thank you, perhaps others here have experience and expertise in the CEF space in the tips area?

I don’t expect you’ll get much feedback on your CEF question as the people who frequent this site are not CEF types, and that includes me. But I’ll respond to your question anyway based on what I know and assume you probably already know about bond funds in general and leveraged CEFs in particular.

I’d say there is no bearish case to be made in your scenario of falling future interest rates because you are assuming that the Gods of Future Interest Rates will act in your favor – something, however, you cannot know in advance (even if you think you can.) Like all bonds and bond funds, when interest rates drop, the market price goes up, and the CEF will go up more to the degree it is leveraged. What remains uncertain is whether the current discount to NAV will change; but since this can’t be known, a best guess might be that it would remain unchanged, or maybe the discount would lessen as the fund value increases and other active investors jump in. So a win all around for the savvy or lucky buyer who was onboard before interest rates fell. However, if future interest rates were to rise, then your CEF would drop in market value, and more so because of its leverage.

The only thing certain about the future total return of this leveraged CEF over the long term is that it likely will underperform a non-leveraged bond index fund to the degree that it is burdened with higher mgt fees.

David, Thanks for the work you do to inform people on TIPS, it is much appreciated. I have a question you may be able help with. I have read/heard a fair amount about how TIPS did not work in 2022 when inflation took off, dismissing their value/role in a portfolio. Has anyone decoupled, or do you know how to find the data to do so, the difference between the valuation change due to the movement in overall rates and the change in the TIPS real rate. It seems to me that going from (I think) negative to plus 2% real return on the TIPS yield would have accounted for some/most/all of the change and could debunk the discussion that TIPS don’t work in an inflationary environment. Thanks, Corey

>

100% true. I’d say that going from negative real yields of -1.50% to positive real yields of 2.00% was a massive barrier for any TIPS fund to overcome, even as inflation went to 9% for a short time. Back when real yields were deeply negative, TIPS were not attractive, and in fact bonds in general were not attractive. Now real yields are around 1.85% to 2.29%, depending on maturity, and TIPS are attractive, or at the very least, in the safe zone.

In the big runup of yields, TIPS funds did out-perform traditional bond funds because of the inflation adjustments, but it wasn’t by a large margin. For example, in 2022 the TIP ETF had a total return of -12.24%, while the total bond fund was -13.11%. The problem was not with TIPS, it was with the huge runup in real and nominal rates in a very short time.

My 70-80% of fixed income is in 4 week Treasury bills since the days of 5+% yield. I have never been a fan of bond ETFs or MFs of any kind. Also, I don’t use auto-roll beacuse on Schwab, for example, you lose one week of interest, Schwab gives virtually nothing for holding your cash, for every auto-roll adding to 11 weeks or so of no interest in a year. I realize that the Fed is cutting rates and the yield curve is steepning. I am monitoring it and will adjust maturity of my holdings accordingly. I like the fact that I am compunding interest on interest. Yes, it amounts to active management, but creating income requires, relatively speaking, more work than putting money, for example, in 2-3 equity index funds such as VOO and VGT and forget about it. The remainig 20-30% of my fixed income is in I Bonds and TIPS. I have 5 years and my wife has 12 years (since she was born in 1961, her RMDs start at the age of 75) to start RMDs and to build our TIPS ladder the way David has been building his. This blog teaches so much on managing fiixed income. Thanks David!!!

VCRB is a new (inception 12/2023 ) actively managed fixed-income fund that is very similar to BND (inception 04/2007). Both are ETF’s. BND’s expense ratio is 0.03%. VCRB’s is 0.10%, quite small for active management (go Vanguard!). I’m wondering if the additional cost would prove worthwhile in the event of a significant downturn (i.e. insurance)? Also, at least to me, paying for active management for a bond fund seems to make far more sense than doing the same for a stock fund. Note, my wife and I are both retired so safety is a priority.

I had never heard of this new active bond fund, VCRB, so I decided to check it out. At the Vanguard site I looked at the Performance and Portfolio Composition tabs of both VCRB and BND. I don’t see any advantage to holding the slightly more expensive VCRB over BND unless you want to take slightly more risk to earn over time slightly more return. I do see that VCRB has had a higher total return than BND since its recent inception in Dec 2023, but since both funds have the same average maturity (around 8 yrs), the likely explanation for the higher return is that VCRB holds more corporate bonds and fewer US Gov’t bonds relative to BND. If you check the composition of both funds you’ll see that BND holds 68% in US Gov’t bonds while VCRB hold only 51%. And it turns out that over there past year corporate bonds significantly outperformed safer US Gov’t bonds.

So, to your question, my assumption is if there were a significant economic downturn, the slightly less risky BND would outperform the more risky VCRB. If you were looking for a fund that would more likely outperform BND during an economic downturn, I think that would be an even less risky 100% intermediate treasury bond fund such as VGIT. Because it holds safer and therefore lower yielding bonds, it should be expected to modestly underperform in good times and modestly outperform in bad times its more risky cousins.

Thanks for your reply, Barry. I asked ChatGPT the same question: https://chatgpt.com/share/6744c3c1-3984-8009-ab79-fc7c492d3712. It points out the advantages active management may have with regard to safety. In our retirement years, I’m more interested in it than trying to outperform an index. Just trying to determine if the (comparatively smaller) premium paid here is worth it. Of course, we all have insurance policies we hope we’ll never use! Perhaps this is just one more, except in this case it isn’t spelled out or guaranteed.

Wow, a 1% expense ratio for what is primarily a bond fund?!? There is no way IVOL can do well in the long term. I own individual bonds, SCHP, and a little bit of VTIP. If nominal rates were lower, I’d own more VTIP and less SCHP but I think SCHP can appreciate compared to VTIP as rates come down. No way I’d hold IVOL, especially when 85% of it’s holdings are simply SCHP.

At age 47 I hold only a small allocation to I Bonds for inflation protection but nothing else. The majority of my assets reside in the single ETF fund of VT. Could a person hold VTIP indefinitely, forgoing duration matching, in place of manually constructing and managing a TIPS ladder? Where would the optimal placement of VTIP go for tax efficiency?

Can you explain why you advocate for BND over BNDW?

I made my fortune (small, but large enough for me to retire at 48) by the end of last century. All of my “investments” this century have gone into savings bonds, TIPS, and a few CDs

Being over 70 safety is way, way, more critical than making a “good” return. Having anything positive on top of inflation is more than sufficient.

Also, protecting myself against myself as my financial acuity deteriorates (and possibly becomes detrimental) is important.

TIPS (and annuities) do this.

I agree that preservation of capital and getting a return above inflation on safe investments is most important when we retire.

Never invest in a business that you cannot understand. One of Warren Buffet’s key stratgies.

Very timely article about the lure of chasing actively-managed funds that have a breakout year from time to time, especially during Covid in 2020 (think Cathy Wood and her ARKK ETF). In big up years or big down years, sometimes active does outperform passive, however, we all know the statistics that a majority of actively-managed funds do not beat their benchmarks over time, and, oh by the way, will charge you more in expenses for less in returns. So yes, dull is smart! And many actively-managed funds end up being closet indexers too, like this one with SCHP. But, if anyone is absolutely in need of some interest rate hedging, there is an interesting ETF from Simplify, ticker: PFIX, the Simplify Interest Rate Hedge ETF. Another interesting one might be the VanEck IG Floating Rate ETF, FLTR.

I say timely because I was looking at my total fixed income allocations just last night, and trying to decide if individual bonds or ETF’s are the better route for my remaining cash right now. I looked at BND as you suggest, along with Fidelity’s FBND (which performs slightly better over the long-run). I currently have VWOB, VCIT, and maybe 9-10 individual TIPS, Nominals, Agencies, and I-Bonds, but would like to reduce my number of holdings. Any suggestions for how much of your fixed income should be in a core holding like BND, and the rest in other instruments? As always, thanks for sharing all your great info!

I have recently gone through a simplification thought process on my taxable fixed income portfolio. My current portfolio is a 50% muni individual bond ladder AA or better (7 years), 50% Corporate/Agency GSE. I have kept my short term money in rolling 6 month T-bills and CD’s.

Realizing that my heirs would not want to deal with the maintenance, I arrived at 4 investments:

VCSH Corp ETF 50%

VTEI Tax Ex ETF 25%

FMHTX MI Tax Exempt Fund (I live in Michigan) 25%

FCNVX Short Term (replacing T-bills)

As the bonds/bills mature over the next 7 years, I will move them into one of the investments of a similar type.

In my Regular and Roth IRA’s I have 5 and 10 year TIPS. As I get closer to RMD’s I may consider a TIP Ladder or the TIP ladder funds like IBIJ (2030 TIP Maturity and others).

Thanks for sharing your strategy, it certainly seems well thought out and diversified. I have the majority of my fixed income in a traditional IRA, so tax-exempt is not a priority for me, but I do the same as you for my taxable short-term cash with T-Bills on auto-roll at Fidelity. I’ve been trying to replicate a total bond market allocation through the mix I mentioned, but it is getting more difficult to track at times. However, I have noticed a slightly better return with the nuance of more instruments, rather than just an all-in-one fund, but nothing particularly earth-shattering for the effort (maybe .25-.50 nominal basis points better on average).