By David Enna, Tipswatch.com

Update, Thursday 1:35 p.m. ET: Weak demand results in real yield of 2.121% for 5-year TIPS reopening auction

Update, Wednesday 5:17 pm ET: The Federal Reserve’s mixed messaging on inflation (expected to be a bit higher next year) and interest rates (going ahead with some cuts, but fewer) caused a strong market reaction, sending both real and nominal yields higher. This TIPS, CUSIP 91282CLV1, closed Wednesday with a real yield of 2.03%.

This could be a temporary move and could revert lower in the morning. No way to know.

——————-

Just a week ago, I posted an article theorizing that real yields for Treasury Inflation-Protected Securities were beginning to crest, especially for shorter-term issues.

Note to readers: Sometimes I am wrong, especially when trying to pinpoint trends in real yields. In the last week, spurred by a too-high U.S. inflation report and fears of future rate “holds” from the Federal Reserve, both nominal and real yields have jumped higher.

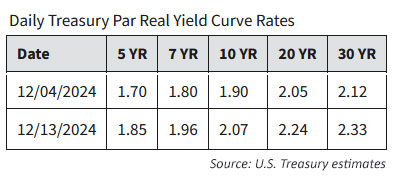

This was even more true for nominal Treasurys. The yield on a 10-year Treasury note jumped from 4.19% on December 4 to 4.40% at the close Friday, an increase of 21 basis points.

All of this is leading up to Thursday’s reopening auction of CUSIP 91282CLV1, creating a 4-year, 10-month TIPS. Its coupon rate was set at 1.625% by the originating auction on October 24 and it closed Friday on the secondary market with a real yield of 1.83% and a price of 99.04.

Definition: The “real yield” of a TIPS is its yield above or below official future U.S. inflation, over the term of the TIPS. So a real yield of 1.83% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.83% for 4 years, 10 months.

One semi-interesting fact about this auction: The Treasury set the size at $22 billion, which is the largest in history for a 5-year reopening. Last December, the auction size was $20 billion. Could these growing auction sizes eventually hold down demand? (Probably not, at this point.)

Here is the trend in the 5-year real yield over the last 14 years, showing that while yields have fallen off highs of October 2023, they remain attractive by the standards of the last decade-plus:

Pricing

If real yields hold at these higher levels, this TIPS reopening should get a price discount of about 1% to accrued principal. It will carry an inflation index of 1.00317 on the settlement date of December 31. All of this means it should end up auctioning at a price very close to, or below, par value.

Here is a look at a potential $10,000 par-value investment, based on Friday’s market close:

- Par value: $10,000

- Actual principal purchased: $10,000 x 1.00317 = $10,031.70

- Cost of investment: $10,031.70 x 0.9904 = $9,935.40

- + Accrued interest: About $34.45

In this scenario, which will change before the auction’s close, an investor would pay $9,935.40 for $10,031.70 of principal and then get inflation accruals for 4 years, 10 months, plus annual coupon payments of 1.625%, distributed in April and October. The cost of the accrued interest will be returned at the first semi-annual coupon payment on April 15.

There is no particular reason for an investor to wait for the Thursday auction to purchase CUSIP 91282CLV1. It could be purchased any time on the secondary market. The auction result could end up better, or worse, but the yield will be uncertain until the auction close. On the secondary market, you can buy when you find the yield attractive.

Inflation breakeven rate

With the 5-year nominal Treasury note closing Friday at 4.25% (pretty attractive, in my opinion) this TIPS currently has a rather-high inflation breakeven rate of 2.42%. However, annual inflation over the last 5 years has averaged 4.2% and over 10 years, 2.9%. So 2.42% doesn’t look unreasonable, and reflects market fears that U.S. inflation is proving to be “sticky” in this range of 2.5% or higher.

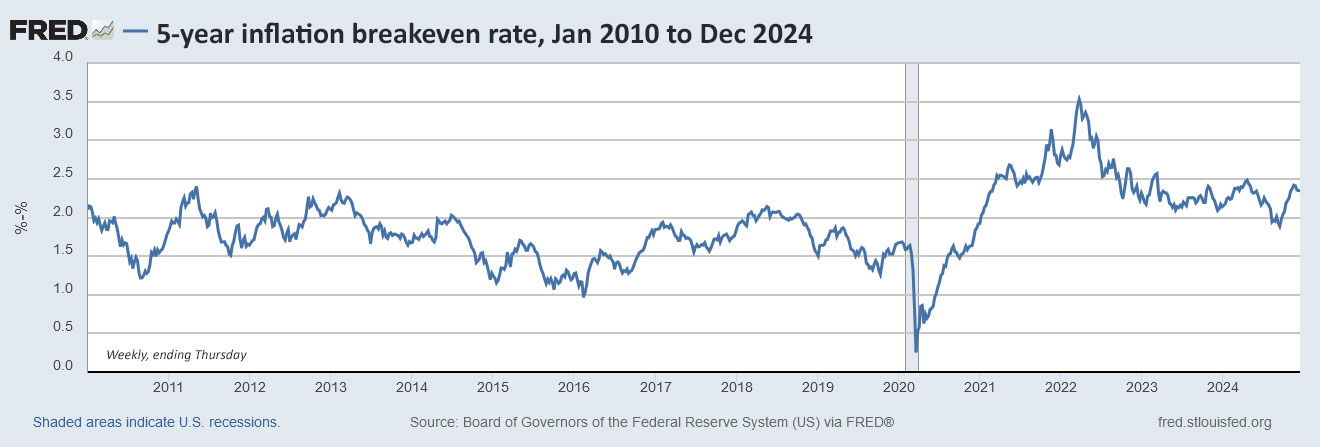

Here is the trend in the 5-year inflation breakeven rate over the last 14 years, showing that inflation expectations have fallen off in the last two years, but remain relatively high by historical standards:

I’ll remind you that the inflation breakeven rate is not a predictor of future inflation. It simply measures market sentiment by comparing nominal and real yields. However, if inflation did remain at 2.42% or higher over the next five years, I think we could expect a continued diet of relatively high Treasury yields. The Fed should not be easing if inflation remains elevated.

Thoughts

I won’t be a buyer this week because the 2029 rung of my TIPS ladder is fully loaded. But I think CUSIP 91282CLV1 looks like an attractive purchase if its real yield holds around 1.80%.

I hear from a lot of readers holding out to purchase TIPS with real yields higher than 2.0%, a number I often call “historically attractive.” Patience may pay off … or it won’t. Real yields are notoriously finicky. A real yield of 1.83% on a 5-year TIPS is attractive, and the maturity date is only 4 years, 10 months away.

On the other hand, if you want to balance off TIPS and I Bonds with some shorter-term nominal investments, a nominal yield of 4.25% on a 5-year Treasury note also looks attractive. I tend to prefer TIPS for terms of two years or longer, however, for the inflation protection over the longer term.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

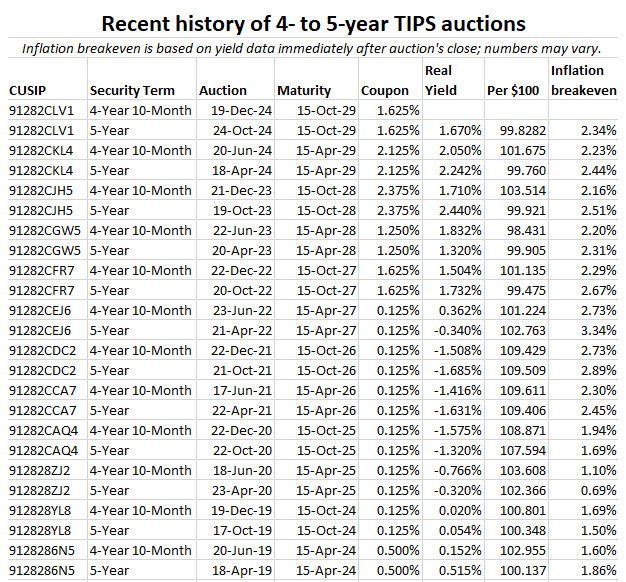

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I was very happy with the 2.121% on today’s (12/19/2024) auction 🙂

Same here. And big thanks to David for providing all the valuable info on this site.

Several TIPS mature in ’29. You’ve probably explained how to determine this already, but notwithstanding 6 months diff in last coupon date, is there any advantage between 91282CKL4, 91282CLV1 (or speaking of the 1999 TIPs party – 912810FH6 which matures in the same year @3.875% ~107.219 ask)?

Separately, is anybody worried about FDIC going away in terms of deposit insurance?

Wishing you and all health and happiness this season!

Those 2029 TIPS are a good example of things to be aware of: wildly different coupon rates, different inflation accruals, different months of maturity. Some sell at a discount (because of a low coupon rate), some at a premium (high coupon rate). The real yields to maturity, however, are fairly similarly grouped around 2.0%. I’d personally prefer the April 2029 issue with a coupon rate of 2.125% and an inflation accrual of only 1.020 and a real yield to maturity of 2.065%. I’d rather have a more straightforward purchase at a price near par and minimal inflation accrual. That isn’t always possible, however.

Keep in mind that shorter-term TIPS maturing in April tend to have what looks like a higher than market real yield, while TIPS maturity in October tend to have a lower than market yield. This is because of the effect of non-seasonally adjusted inflation, which will lag in the closing months of the April issue.

Thanks for the clarity and bonus info. As an aside, I learned about 912810FH6 by creating a ’27-’54 hypothetical on tipsladder.com and selecting “best yield.” It showed up as the ’29 rung, but playing around I noticed if I selected “lowest inflation adjusted principal” 91282CLV1 popped up and the overall return was supposedly 0.3% better. In either case, the return was ~40-ish and mostly principal towards the end, so that got me thinking – why wouldn’t I buy some EE bonds (that double in 20 yrs) for the last 7 yrs instead of TIPS? It looks like you mentioned EE bonds as a (surprisingly) stellar long-term investment in 2020. Granted, it’s only 10k/yr (w/10k spouse gifting for now?) but “crystal ball willing” wouldn’t that be a nice little bonus or did I screw up the math?

@Me Again, EE Bonds did have some appeal when the 20-year Treasury bond was yielding well below 3.5%. Today, not so much. In today’s market, I consider them irrelevant. However, they could pay off with a 2.6% annual interest rate if overall rates decline deeply again. Iffy.

Not sure I understand the appeal of EE bonds now that you mention, 2.60% yield if sold early, and if held to 20Y to get the double in 20 years feature gives an effective 3.53% YTM. And no inflation adjustment. A 20Y treasury would beat that, an agency would be even better but callable. There seem to be lots of other options. Maybe I don’t understand what you meant.

I don’t know how reliable or accurate or precise it is but Fidelity posts an “expected yield” number for Treasury new issues. Today the expected yield for this TIPS went from about 1.85% to 2.02%. Seems like quite a jump.

This was because of confusion over the Federal Reserve’s interest rate decision. Both nominal and real yields surged higher, and the 5-year TIPS reopening at auction on Thursday closed today with a real yield of 2.03%, a remarkable move higher.

I was both a little surprised by the news from the Fed and the reaction to it.

I would just as soon the yield stayed over 2% through the auction, I have ordered some of these TIPS. At 1.85%, they looked good enough. 2% is even better.

Is this too good?

Just purchased 32 par of 91282CBF. Payed $34,740.86. Then multiplied 32x1000x1.21194=38,782.08

So $38,782.08 is current value, provided I hold to maturity and not trade. I am correct? Seems too good to be true.

Thank you for everything you do.

RT

I am assuming this was actually 91282CBF7, which matures Jan 15 2031 and you probably got a real yield to maturity of about 1.9% (good) and you paid a discounted price of about 89.6 (also good). On the negative side, you will be getting an annual coupon rate of only 0.125% until maturity, and that is the reason for the discounted price. The current market is about 1.75% to 1.875%, at least.

yes it was 91282CBF7 indeed

so lousy coupon rate for me. I knew there was a catch 😦

thank you

Isn’t lower coupon rate better if I want to get more of the money when I need it in the future? I would think higher coupon means my interest payments over time are higher so I get more $ before I actually need the money. Is my understanding correct? Thanks.

A lot of investors take this view, but it is still a bit of a toss-up. A higher coupon rate provides some protection against deflation, since it will be paid out even as principal declines. Also, the interest earned could potentially be reinvested in higher yields (or not). Tipsladder.com uses coupon income as part of your annual withdrawal proceeds over the course of the ladder. This is one area where I Bonds have a nice advantage over TIPS, since the interest income continues to compound into the principal balance, year after year.

I bought this TIP last time at 1.65%. I put another order. Let us see what yield we get.

I scheduled a modest, but not insignificant, purchase to my Rollover IRA. But not for my Roth.

I was fleshing out my TIPS holdings with the great rates we saw in November. Now, I am tempted to sell my corporate bonds to buy even more TIPS. I paid $1/bond to buy every one of them.

Jason Zweig wrote an entire book about keeping one’s emotions from affecting one’s financial decisions.

Notice I received states “4-Year 10-Month 1-5/8% Treasury TIPS Auction Announced”. What does the 1-5/8% refer to….a guaranteed interest rate or ?

Thanks

Lynne

That refers to CUSIP 91282CLV1’s coupon rate of 1.625%, which was set by the originating auction. At the auction, the price will probably be discounted to result in an above-inflation yield to maturity that is higher than 1.625%. But the coupon rate will remain 1.625% — the investor will get a discounted price, that coupon rate and future inflation accruals.

In 2008 – real yields went up to 4%, then quickly came down. How did they manage to get them under control so quickly?

In that case, we went through the worse financial panic and resulting recession in U.S. history since the Great Depression, but the primary reason for the surge to a 4% real yield for the 30-year TIPS was a massive selloff in all financial instruments, for just a few days in November 2008. Those few days were a fantastic opportunity for buying TIPS. But it was about a 1-month window.

Been meaning to ask the same question about that 2008 spike. Thanks for the explanation.

Yes, thank you. I suppose everyone just “calmed down” a month later then.

Looking at that FRED chart – it only goes back about 20 years. I guess we will never know what a “fair” real rate should be to loan money to the most stable government on the planet.

If the market was efficient, we probably should see a significant difference between 5-year and 10-year and 30-year TIPS. So far, the difference in real yields between 5yr and 30yr TIPS barely made it above 2% in 2011, and otherwise it has been lower.

One thing to consider is that TIPS have only existed as an investment since 1997, a total of 27 years. In the early years, the real yields were high but this was a new investment and a bit experimental. I started investing in TIPS in 1999 and did get real yields in the 3.5% range at that time. For many years, there longest maturities were 10 years. It is hard to make comparisons, but I agree that the yield curve ought to climb higher for longer maturities.

High yield; to hell with treasury direct!

David, this does look a good time to pick up TIPS. Thinking of getting some more of last February’s 30-year TIPS on the secondary market. I’m new to secondary market purchases. Read your article on this topic. It seems the 30-year TIPS was at 2.315% on market as of 121424 so the last February 2024, 30-year TIPS real yield of 2.200% and coupon of 2.125%, looks good to pick up more? It seems the 30-year breakeven of 2.29% as of 121424 and 30-year nominal market of 4.60% (4.60% – 2.315% = 2.285%) makes it a good buy? I retired in the last few years and value inflation protection. Thanks for your thoughts, David.

Just understand how volatile the 30-year TIPS is. Can you feel confident about holding it maturity, or at least for 30 years, or at least 25? At this point it is selling at about a 4% discount, and the inflation factor is not too bad at 1.02797. I have bought a couple 30-years in the past, and still hold them, but that’s beyond my lifespan today.