By David Enna, Tipswatch.com

This year 2024 brought many surprises. For example:

- Did you think the stock market would soar higher after the Federal Reserve started lowering short-term interest rates? OK, that seemed predictable.

- But then did you foresee that longer-term interest rates would move higher as the Fed cut short-term rates? I had a feeling that could happen.

- And then that the stock market would continue soaring higher even as longer-term rates were rising?

- And that a high-risk, speculative investment like Bitcoin would rise 53% in the 45 days after the November presidential election?

- Or that the incoming Trump administration would at first cause stock-market froth and then trigger investor regret about potential policies, all in a two-month span?

- Or that the Federal Reserve would end the year apparently ready to pause its rate-cutting path into 2025?

The year 2025 is bringing uncertainty. I would not be surprised to see a fairly large sell-off in stock prices early in the year, with investors eager to harvest gains in the new tax year. But I am not a stock market expert and I have no crystal ball. So instead, here is a look back at 2024:

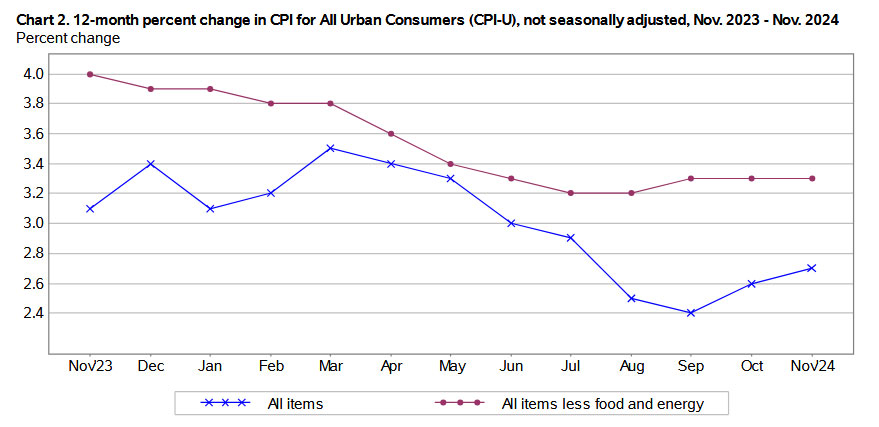

U.S. inflation

In November 2023, annual U.S. inflation stood at 3.1% for all-items and 4.0% for core. Today, as of November 2024, those numbers are 2.7% for all-items and 3.3% for core. That indicates progress. But the troubling thing — and what is clearly worrying the Fed — is that both inflation measures have been rising in recent months.

At its most recent meeting, Fed officials raised their 2025 inflation predictions for the Personal Consumption Expenditures Price Index (PCE) to 2.5% for both all-items (up from the previous estimate of 2.1%) and core (up from 2.2%). And at the same time, it cut interest rates.

PCE tends to track lower than headline CPI, as shown in this chart from the Cleveland Fed. So that means, probably, that official U.S. inflation will rise by a rate higher than 2.5% in 2025 based on the Fed predictions. In other words, we could be seeing 2.7% to 3.0% inflation for many months to come.

In addition, you can add in the potential for higher inflation from Trump administration policy decisions on tariffs and deportations.

Again, the theme is uncertainty.

Treasury Inflation-Protected Securities

The past year was a stellar time for building a ladder of TIPS investments across the full maturity spectrum. Several times over the year, including this week, real yields were close to or above 2.0% across 5-, 10- and 30-year maturities. That offered a unique opportunity to build a ladder quickly and be done. I wrote about this last month.

Even investors in TIPS mutual funds and ETFs did relatively well in 2024, despite the upswing in real yields in recent weeks. The TIP ETF — with the full range of maturities — had a year-to-date total return of 1.48%. The short-term-focused VTIP ETF did better at 4.56%.

Here is a look at the 12 TIPS auctions through the year:

I have highlighted highs and lows for the year, but in my opinion every one of these auctions had a decent result for investors. Outside of the auctions, there were many mid-year and late-year opportunities to purchase TIPS on the secondary market with real yields close to or higher than 2.0%, a historically attractive target if held to maturity.

I would judge 2024 to be an excellent year for TIPS investing, based on the opportunities to snag attractive yields. But note: Real yields could rise higher, especially if inflation continues increasing and U.S. borrowing continues at very high levels. I wrote about this a week ago.

Bloomberg this morning has a detailed article focused on growing pressures in the U.S. Treasury market as the debt level swells. It explains that the primary dealer system may no longer be fully capable of dealing with bond-market disruptions.

“Issuance has gone up almost threefold in the last 10 years and the anticipation is for it to close to double to $50 trillion outstanding in the next 10 years, whereas dealer balance sheets haven’t grown at that magnitude,” said Casey Spezzano, head of US customer sales and trading at primary markets dealer NatWest Markets. … “You’re trying to put more Treasuries through the same pipes, but those pipes aren’t getting any bigger.”

U.S. Series I Savings Bonds

These inflation-protected savings bonds started the year with a fixed rate of 1.3% and a six-month composite rate of 4.28%. Today, the fixed rate for new purchases has fallen just a bit, to 1.2%, but the composite rate is sharply lower at 3.11%.

I am still a fan of and strong advocate for these Nov 2024 – Apr 2025 I Bonds, a unique, super-simple, super-safe investment that will provide tax-deferred returns exceeding inflation for as long as you hold them. My advice is to ignore the composite rate and focus on the 1.2% fixed rate, which is attractive. If inflation continues running at high levels through 2025 and beyond, these savings bonds provide protection in the form of a cash-equivalent savings account that is adjusted for inflation.

At this point, it looks possible the I Bond’s fixed rate could increase at the May 1 reset. For that to happen, using our back-of-the-envelope theory, the 5-year TIPS real yield would need to average at least 1.92% from November to April. That would get you back to 1.3%. At this writing, the 5-year TIPS is yielding 1.99%.

However, because the 5-year TIPS is sensitive to changes in short-term rates, I’d say the 5-year real yield will probably be heading lower.

Next year, changes may be coming to the savings bond program, especially to the much-used “gift-box” loophole for adding to your holdings with a trusted partner. But at this point, we know nothing. The Treasury in the last year has halted issuance of paper I Bonds in lieu of a federal tax refund, and also ended its Payroll Savings Plan for automatic contributions into TreasuryDirect.

This will be something to watch in the coming weeks.

In summary

Uncertainty seems to be my word of the day, maybe for the entire year 2025. And I believe uncertainty causes market disruptions. Things could keep humming along, but it’s probably time for a reality check for over-heated stock and alternative-investment markets.

To quote a famous American: “Be there, will be wild!”

Conservative investors will survive.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David,

Yesterday, in his new Substack, Nobel Prize-winning economist Paul Krugman posted this piece–https://paulkrugman.substack.com/p/the-real-threat-of-fake-numbers–in which he discussed the problems that could arise if Trump has federal agencies create and publicize false statistics. Krugman’s main concern in the piece is Trump’s having the BLS create and publish official inflation numbers that are lower than the actual numbers which are likely to increase if Trump follows through with his economic proposals. In particular, Krugman noted that such a development could hurt owners of TIPS, as well as people receiving Social Security benefits. He made no mention of I-bond holders. I wondered if you’d like to weigh in on all of this.

It’s a legitimate concern and will need to be monitored. Many times in recent years, as Krugman notes, the right-wing GOP has been accusing Democrats of cooking the inflation numbers. I don’t think that has been happening. I think — even if the numbers don’t reflect your personal inflation — they are relatively consistently calculated, with a few adjustments here and there. It would be hard to hide actual inflation from the American people, and very risky to pretend it is lower than it is. The BLS is full of professionals who would blow the whistle if cheating was going on. But … will those people still be there? Financial markets depend on reliable numbers, and Trump knows that. So I doubt this will happen to the extreme.

David, happy new year! I look forward to reading more of your timely analysis and insights throughout 2025.

Since the stroke of midnight, there does not appear to be any restriction on purchasing new I Bonds despite receiving a gift box delivery above the annual purchase limit in 2024.

I looked this morning, too. Same result. I didn’t complete the purchase, though.

I didn’t either. But at least now we have a bit less ambiguity after Treasury kept everyone in the dark for months.

In 2024, I exceeded the 10,000 limit by 4,000 due to gift box delivery, but just made a 400 purchase and it went through with no problem and is out of my bank.

I delivered my IBond purchased last October to my wife. Everything shows up correctly on my wife’s account. I didn’t check to see if I had any IBond purchases available this year since I do not intend to purchase any IBonds.

I have always enjoyed how you typically avoid political discussion and discourage political rants in the comments – hopefully that holds going forward with a new administration and isn’t a one sided policy. I see some slippage over the past few months but maybe it’s just me

If I see a policy I don’t like (either party) I am going to explain why I don’t like it. For example, I criticized Biden’s Inflation Reduction Act as inflationary, and while it might have some benefits, it was inflationary.

HI David,

Do you have any thoughts on the upcoming 10 year TIPS auction on January 23rd? It looks like a good opportunity. I am hoping to convert a portion of my BND ETF holding into this 10 year TIPS. Good idea?

I will be publishing a preview article on that auction on Sunday, Jan. 19. I am nearly 100% likely to be a buyer at that auction, because it is the first TIP issued that will mature in 2035, filling a vacant spot on my ladder. I have been setting aside money for this purchase, but in the past I have used money out of BND to buy TIPS in the tax-deferred account.

Appreciate the EOY roundup David. Would also love to see your twitter posts mirrored to bluesky. That site seems to avoid the army of attractive Russian women that started following me on twitter even though I never post anything. 🙂

Those same fictional women are also after me on Twitter. We are irresistible, I guess. (I block them when I notice.)

Looking ahead to likely Trump policies that will be inflationary – tariffs and deporting much of the workforce in certain areas – I am buying short term TIPS in the secondary market.

TIPS pay on the unadjusted CPI and not the widely reported seasonally adjusted CPI.

It would be useful to know the seasonal adjustments for each month in order to judge which secondary TIPS to buy.

I hope you will publish this.

I spent a couple of hours seeking this on the web and failed.

Thanks

https://www.bls.gov/cpi/seasonal-adjustment/

Keep in mind that after 12 months, non-seasonally-adjusted and seasonally-adjusted inflation will be exactly the same. It balances out. So what you are really after is the month-to-month difference in the two versions of CPI during the year, and that will change a bit every year because it is based on 81 price indexes. Here is how it went month to month in the last year, with non-seasonal running higher Jan to June and then lower from July to Dec. This is the pattern every year:

In this chart, I am using the official rounded CPI-U number for each month (one decimal point) and my own calculation for non-seasonal with two decimal points. So the numbers may not add up to be exactly equal.

Thank you very much for your excellent TIPS insights!

I have a practical question: you mention TIPS ETFs in your article. What is the advantage of buying treasury note/bill ETFs compared to buying treasury notes/bills directly? How are the tax advantages of treasuries accounted for in the ETF?

Many thanks in advance!

I am not a fan of TIPS ETFs, but they are useful for many people because of their simplicity — no 1099-OIDs, for example. These funds are acceptable for someone with an undetermined maturity target or one that matches the duration of the fund. The problem is that if real yields rise sharply just before redemption, the fund is going to lose value. The TIP ETF, for example, had a total return of -8.5% in 2013 and -12.2% in 2022. Individual TIPS in a ladder are ideal for creating a stack of predictable, inflation-adjusted income for 10 to 30 years. Using a tax-deferred account is best.

TIPS funds have a lot of defenders. I get the logic but I prefer the certainty of individual TIPS held to maturity.

When it comes to the overall bond market, however, I use Vanguard’s BND as a core holding.

David – I am curious why you hold BND as a large, core holding in your portfolio vs. laddering nominal treasuries as you do TIPS? The only reason I can think of is that the dollars in BND are part of a balanced portfolio that is periodically rebalanced and has a long investment horizon.

BND is technically an intermediate-term bond fund, with a duration of 8.4 years. It holds 11,315 issues as compared with about 43 for TIP. It is a bit overloaded with U.S. government debt (68%), but then the rest is investment-grade corporate. The expense ratio is super low at 0.03%. It seems like a logical choice for a core holding, balancing off my inflation-protected holdings of individual TIPS and I Bonds. I have it in my traditional IRA, which will allow me to tap into it when I need money for RMDs in the future, instead of selling off TIPS.

David – Yes, I understand that BND is a good fund for the reasons you state, but my question was more about laddering one’s nominal bonds vs using a bond fund. ( I know you can’t ladder a composite bond fund like BND as you can treasuries, but BND’s long term returns are only slightly better and slightly riskier than intermediate treasuries, so in my view it’s about a wash). Since you have expressed a preference for laddering TIPS vs holding a fund, and many of your readers including me share that preference, I was surprised that you plan to take your RMDs from a fund with its uncertain day to day value rather than the certainty of a maturing bonds.

Trying to think this through, I’ve concluded that if one intends to reinvest RMDs back into the same bonds in a taxable account, then a fund is much simpler and just as good as a ladder. But if one intends to spend the RMDs, then, to me, laddering nominal bonds offers the same benefits as laddering TIPS. Does this way of framing it make sense to you?

Actually, BND is simply my back-up fund for providing RMDs. Those will be primarily drawn from maturing TIPS or other maturing Treasurys in each year. I also use that BND fund to draw money — as needed — to buy TIPS at good real yields. It just gives me alternatives.TIPS have qualities of guaranteed real return that you can’t get with nominal Treasurys, and there are a limited number of TIPS, so laddering is ideal for that investment. (Probably doesn’t really answer your question. I do buy nominal bonds in the ladder, but only for less than five years out.)

If you had to do it again, would you hold corporates separately from Treasuries? For my bond side, I have been only investing in corporate ETFs and using I Bonds, CDs, high yield savings accounts, etc. otherwise. The issuer diversification for corporate bonds is essential, but for Treasuries having a ladder or picking individual bonds or maturities to knock off can be done.

My financial guru, Allan Roth, stresses that bonds are for safety, and BND is a fund he has always recommended. I need that fund to supply back-up liquidity in my traditional IRA. Investment-grade corporates aren’t that risky, and BND does have some exposure. I would only do corporates in a fund, however, just as you say.

Uncertainty is definitely the keyword. I also believe stocks are way overvalued. The DOW has doubled since the recovery from COVID (about 19,000 to 42,000 today) and the NASDAQ has almost tripled! I think we’re in an “AI bubble” no different than the “Dot-Com bubble.” Fast advances in technology have given people a sugar rush. Buy low, sell high is the successful way to do it, but It’s pretty high right now to join the party late. Also, with inflation going back up (sticky as a lot of people predicted), they are tapping the brakes on all of the rate cuts that they have already banked on. By no means am I an expert (then again, who is?), but the odds don’t seem like they are worth the risk.

I lived through the internet bubble. I am still carrying losses from the Nortel bankcruptcy and my JDSU (fiber optic) investment was the worst. I know “this time it’s different” are dangerous words. For me staying “conservative” has helped while getting a bit smarter and lucky (so far) with some select AI stocks. Having worked in IT all my life has been mostly a blessing. Overall, no regrets.

I do have a question for David and others. If and when nominal 10 Year Treasury has 5% rate and I am good with holding it to maturity, given the current environment, what will you pick 10-year TIPS or the nominal?

Thanks, as always, for David’s great analysis and contributions by all. Wishing you all and your loved ones Happy, Healthy, Joyful, and Prosperous 2025.

A 10-year Treasury with a 5% nominal yield would be quite tempting. It would also mean that a 10-year TIPS would have a real yield of at least 2.5%, maybe higher. My inclination is to use nominals for up to 5 years, and TIPS for 5 years and up.

A while back, in a comments section on this website–although, in view of the numbers involved, I’m surprised at how little “while back” it has been–I asked if anyone else here was concerned (as I am) that the issuer of I Bonds and TIPS had an accumulated debt of $33 trillion.

That figure is now up to $36 trillion. This is absolutely mind-boggling.

I own TIPS and I Bonds because, where truly inflation-indexed fixed income instruments are concerned, they’re the only game in town. But I keep thinking that we’re all just assuming–hoping?–that the national Treasury would never default on its obligations. Or, to state the issue differently, for a while now I’ve been having the uneasy feeling that TIPS and I Bonds are on their way to becoming, or have already become, “faith-based” holdings. (Yes, I’m aware that they’re described as being backed by the “full faith” of the national treasury–but I’m talking about the “faith” of the buyers, not the faith of the seller.)

Would welcome comments by David or any other like-minded (or not like-minded) readers here.

Seems unlikely that the Treasury would default when it could simply inflate away the debt. Inflation protected securities would be protected unless the Government decided to game the measure of inflation.

I certainly share your concern for the humongous and growing debt. As a former employee at the U.S. Office of Management and Budget (and, back when Jimmy Carter was president, of the Council on Wage and Price Stability), I have been fighting this dragon my whole career. When it comes to the safety of bonds as investments, however, you have to ask: “Compared with what?”

People used to say that Social Security was safe; Congress would never let that fail. Today it isn’t so clear. I have a modest federal pension that I score as safer than Social Security; federal employees will protect their own nest eggs more carefully than those that belong to others. And I believe that federal bonds are even safer than that; if things go south, pension payments will be curtailed before default on the debt. Last week Janet Yellen said that, absent an increase in the debt ceiling, the Treasury will start using “extraordinary measures” to manage federal obligations in mid-January. In the face of a real default (as opposed to just a “ceiling problem”), measures will get extraordinary indeed.

Meanwhile, what alternatives look safer for investors? Certainly not private debt. Bitcoin? A ‘stable’-coin? Gold? There is a case to be made for these things, but in my opinion it comes down to being diversified. If I were forced to pick only one, I would not hesitate: across almost all plausible scenarios, inflation-protected federal bonds are a more reliable store of value than anything else now available.

Bmannix, excellent feedback. Thanks.

I can’t image what our investment balances would look like if the U.S. decided to default on its debt. Things would be in shambles. So I don’t think that will happen, but we might see a few shocks along the way to a more sensible policy of spending vs. revenues.

I do wonder if someone will create sovereign-only dollar denominated foreign bond ETFs or inflation-indexed dollar denominated bond ETFs (I think the UK offers that as well). Currently the UCITS ETFs which are available in the European marketplace are unavailable at most brokers in the US, but it would be great to have the same level of diversification in the foreign stock ETF universe to be in the bond world as well.