By David Enna, Tipswatch.com

The December inflation report issued this morning by the Bureau of Labor Statistics can be viewed only one way: U.S. inflation is not yet under control.

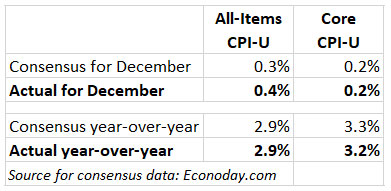

Seasonally adjusted inflation increased 0.4% in December, higher than expectations. Annual inflation increased from 2.7% to 2.9% in December, which matched expectations but isn’t great news. Core inflation, removing food and energy, increased 0.2% for the month and 3.2% for the year, breaking a three-month string at 3.3%. That’s the one bit of positive news.

So officially, U.S. inflation ran at 2.9% for the year 2024, down from 3.4% in 2023.

Gasoline prices reentered the inflation picture in December, rising 4.4% for the month, but fell 3.4% for the year. Fuel oil prices also rose 4.4% for the month. The BLS said energy prices accounted for about 40% of the overall CPI increase. Also from the report:

- Shelter costs showed no sign of abating, rising 0.3% for the month and 4.6% for the year.

- Food at home prices rose 0.3% for the month and 1.8% for the year.

- Apparel prices rose 0.1% for the month and just 1.2% year over year.

- Airline fares rose 3.9% for the month and 7.9% for the year.

- Costs of used cars and trucks rose 1.2% for the month but were down 3.3% for the year.

- New vehicle prices rose 0.5% in December but fell 0.4% for the year.

- Motor vehicle insurance costs rose 0.4% for the month and 11.3% for the year.

Looking for a bright spot? The costs of alcoholic beverages fell 0.3% for the month and rose just 1.4% for the year.

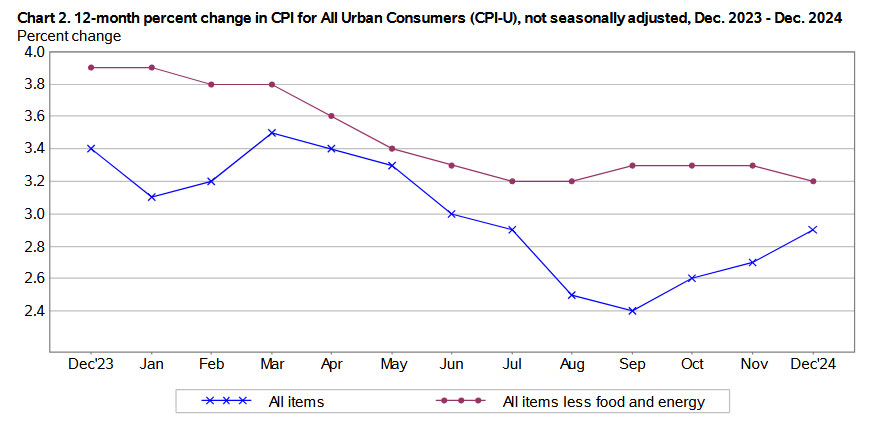

There aren’t a lot of bright spots in this December report, with prices increasing across a broad spectrum of products and services. Here is the trend in annual inflation rates over the last year, showing the clear trend of higher all-items inflation:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For December, the BLS set the inflation index at 315.605, an increase of 0.04% over the November number.

It is normal for non-seasonally adjusted inflation to run lower than official inflation in December. In fact, last month was the first December since 2021 to not record non-seasonally adjusted deflation for the month. The numbers will turn around in January, with non-seasonal running higher than seasonal.

For TIPS. December inflation means that principal balances for all TIPS will increase by 0.04% in February, after falling 0.05% in January. Here are the new February Inflation Indexes for all TIPS.

For I Bonds. The December report is the third of a six-month string that will determine the new variable rate, to be reset as of May 1 and eventually roll into place for all I Bonds. As of December, inflation has increased just 0.1% for the three months, translating to a variable rate of 0.2%.

However, that is pretty meaningless. Non-seasonally adjusted inflation will pick up in January. For example: In 2023, inflation for October to December was -0.34%, but the next three months brought the variable rate up to 2.96%. Here are the data:

What this means for future interest rates

This might not be a “nightmare” inflation report for the Federal Reserve, but it certainly isn’t good news. Annual inflation hit a low of 2.4% in September but now has ticked steadily higher to 2.9%. Core inflation has been steadily above 3.0%, but finally ticked lower in December.

In Bloomberg’s morning report, some analysts are pointing the drop in core inflation has a strong positive. This is from Anna Wong and Stuart Paul of Bloomberg Economics:

We think the Fed will likely view the December CPI report favorably. We still expect officials to hold rates steady in January, but the report bolsters the case for the dot plot’s outlook of 50 basis points of rate cuts this year.

A counter view from Bloomberg’s Molly Smith:

While the easing in the CPI is welcome, Fed officials would need to see a series of subdued readings after months of elevated prints to reassure them that inflation progress has resumed. Lingering price pressures have contributed to a deep selloff in global bond markets and fueled concerns that the Fed eased policy too quickly at the end of last year.

My opinion: For the time being, especially as we enter a period of uncertain government policies, I think the Fed is likely to delay any future cuts in interest rates. Before any change, it will begin sending signals. For now, we are on hold.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The Treasury’s Inflation Table shows a February 1 Inflation Ratio of 1.03003 for the 5 year TIPS dated 10/15/23 (issue date 10/15/23, CUSIP # 91282CJH5). As a buyer, my Unadjusted Price was 99.697130 and the Coupon rate is 2.375%, for a Real Yield of 2.440%. Schwab’s Ask Price on January 17th (for the minimum purchase of $25,000 face amount) was 102.359, with a YTM of only 1.729%. Does that make sense, given that Schwab is making a market in these bonds? Bloomberg shows 98.80 for a real yield of 1.89%, and 4.43% for the 5 year nominal Treasury note, implying a breakeven inflation rate of 2.54% (with 3 years and 9 months to go, does that rate seem realistic?).

Vanguard is showing a real yield to maturity of 1.771% for this TIPS right now. It matures Oct. 15 2028. But … it has a coupon rate of 2.375%, well above the current market yield of 1.756% listed at the Friday close on the Wall Street Journal site. You apparently bought at the original auction with a real yield of 2.440%. Good move! But now the 3-year real yield has moved much lower, so the current price is higher. You can’t compare this TIPS with a 5-year TIPS. This TIPS has its own market, which is currently offering a real yield of around 1.77%. All of this looks correct.

Well this looks disappointing I’ve been enjoying 4-5% on T-BILLS

https://www.morningstar.com/news/marketwatch/20250117524/t-bill-supply-will-turn-negative-soon-without-a-us-debt-limit-deal-bofa

In the most recent episode of the recurring debt limit crisis, some T-bill interest rates (such as for the 8-week, 13-week and 17-week) actually started climbing, while the 4-week yield was falling. Why? Because investors flooded into the shorter-term T-bill, thinking default wouldn’t come within 4 weeks. The 4-week yield actually fell 120 basis points in three weeks, while other T-bills were getting higher yields.

I wrote this on April 23, 2023: https://tipswatch.com/2023/04/23/looming-debt-crisis-is-already-roiling-the-treasury-bill-market/

Prediction: The debt-limit crisis will be resolved, as it always is.

But yes, as a debt-limit crisis approaches, you should see some anomalies in T-bill rates.

I see this as evidence that those who were quick to dump their I Bonds made a premature decision.

I also may have been premature in moving 10% of my IRA into Contrafund, but I still feel confident about 2025 on that.

The trend is not the Fed’s friend; 2.4 to 2.9 in 4 months is not a bump, it’s a trend. Higher for longer rates are not curbing spending or lowering inflation as much anymore either because we are a service-based economy where people have a much harder time cutting back on consumption of stuff like health care and insurance (especially as our country ages and experiences more health & catastrophic events). Service inflation rarely, if ever decelerates. The Fed probably screwed up and has backed themselves into a corner now. Wages have also stabilized and in some cases fell as well, so where is the inflation coming from? Obviously the shortage in housing. In an uncustomary way, cutting rates now might actually lower inflation if that would mean increased supply to the housing market.

I have an untested theory: When the Fed says it expects HIGHER inflation in 2025 (which it did last month), companies see this as an open gate to continue raising prices through the year, even if the increase is unneeded. Consumers now expect higher prices, something the Fed wants to avoid, but has prodded along.

Probably not just the Fed or even mostly the Fed. A lot of inflation isn’t raw hard numbers; policy or even monetary supply – it’s psychological.

UofMich survey inflation expectations just jumped to 3.3% for 2025 and the same 3.3% for long-term. Not that this survey or 1-month of data is gospel, but many times these expectations are somewhat self-fulfilling.

I’m sure the Fed statements are one of many factors which go into expectations and hence into actual future inflation.

Thanks David, and good point. I wasn’t someone who bought into the idea of inflation solely caused by price gouging as the politicians were claiming, but there is definitely some validity to companies exploiting the inflationary environment at certain times to justify their price increases, and thus the vicious cycle continues.

Good hypothesis David since the Fed does take into account consumer sentiment surveys, etc. This week will be a test of your theory with the new Trump tariffs going into effect on Canada, Mexico, and China and how quickly companies will react. I will be buying a car part I need before it is much higher.

It’s so easy to forget with such artificially low interest rates and inflation for a decade after the 2008 Great Recession, and such high inflation when the world reopened with feverish demand and the resulting supply chain issues after the pandemic, that the average inflation rate in the U.S. was 3.30% over the past CENTURY. We are currently experiencing SLIGHTLY BELOW AVERAGE INFLATION on an historical basis, which in and of itself is an accomplishment considering the 2021-2022 spike. We may eventually reach the 2% Fed target rate but unless we have a recession or depression, God forbid, prices are not going to reverse themselves overall — which is what people want but won’t get. What does that mean for investments? It means inflation protection is still a useful component of one’s portfolio and stocks will be driven by profits, both signs of resumed normality.

We did have quite a long spell of low inflation from 2008 to 2020, when annual inflation averaged about 1.6%. Before 2008, all the way back to 1981 (my data starts in 1971), no 10-year period had annual inflation of less than 2.4%. Today’s 10-year inflation breakeven rate is about 2.44%, right in the historic range pre-2008.

Fascinating to see the almost polar opposite takes on the inflation numbers. Market pops this am on the news. Bond up, yields down. Go figure. I’m guessing you’re right the FED’s gonna need to something stable before they cut more.

The market doesn’t agree with you. In fact, it thinks the complete opposite.

The market tends to seize on anything positive, and in this case the drop in core was positive.

Excellent reminder about the wall street cheerleaders.

And thank-you for this excellent summary of DEC 2024 inflation. You are saving us so much time and effort.

I noticed that as well. After hearing the numbers, I went straight to the business channel and saw it was above 600 points pre-market. I was expecting a decline since inflation had actually increased. However, apparently since the YoY Core CPI-U was less than expected (3.2% vs 3.3%), the market got excited. Their thinking is this will somehow justify more rate cuts now. Funny because the All-items CPI-U monthly rate was hotter than expected (0.4% vs 0.3%).

Like David said, I don’t see how this justifies a rally. The bigger thing I guess is that banks are doing much better than expected and the 10 year note is down. With all of the unknown policies about to hit the market, no telling what is going to happen. However, that’s where you gotta jump in sometime to at least have a chance to catch a big investment return. You have a 0% chance to win the lottery if you never buy a ticket.

I noticed the history of October- December as always being either negative or flatlined. The first and only one since 2012 (the earliest year posted on your site) was 2021 and we all know what happened that year. Yikes!

My question pertains to what causes this? Is it because companies are lowering their prices for sales and/or to get rid of that year’s inventory? Just like a new car is going to cost more than an old one. If you buy a 2024 model late in the year, then why not wait for the next one if you’re going to pay that much (or a little more) for a 2025 model? The car hasn’t sold all year and they’ll be happy to just get rid of it at a cheaper price to make room for the newer cars that are more expensive. Same with computers and anything else that depreciates as time goes on. Nobody would buy a computer from two years ago at the same price as a new one today.

Not saying this is the only reason, but I would think it contributes.

Yes, heavy discounting goes on in November and December. That’s the biggest factor. Here is an interesting podcast on that issue: https://inflationguy.podbean.com/e/ep-79-seasonal-adjustment-and-inflation/

Very interesting. Nice to know my hypothesis wasn’t totally crazy lol. I just couldn’t imagine sales discounts not having something to contribute to it. No surprise as to why 2021 was different since we were dealing with COVID. Between the government flooding the markets with stimulus checks and demand being higher than supply. People had more money to spend with the stimulus checks and nothing to do but shop since everything was closed (ie can’t go to the movies; eat out; sports games etc).