The 4-week Treasury yield is sending a message of fear.

By David Enna, Tipswatch.com

Update, April 26: ‘The debt limit drama heats up,’ says Moody’s Analytics in new report

On Thursday afternoon, I happened to be watching CNBC during a long on-air interview with Cathie Wood, CEO and founder of Ark Invest, an investment management firm.

Wood is an interesting person, obviously a high-risk investor whose shoot-for -the-moon style is completely opposite mine. I find a lot of her market commentary is designed to bolster the high-risk stocks her funds already own. She’s a believer. But midway through the interview, she said something that made me jump up and say, “NO!”

Listen to the first two minutes of this clip:

Here is the quote that gave me pause:

I think the markets are leading the Fed and I was struck today to learn that the one-month Treasury bill yield is 140 basis points — 1.4% — below the low end of the Fed funds rate. I remember in ’08 and ’09 the Treasury bill rates were an early indicator of how quickly the Fed was going to ease once it realized how much trouble we were in.

What is really happening here?

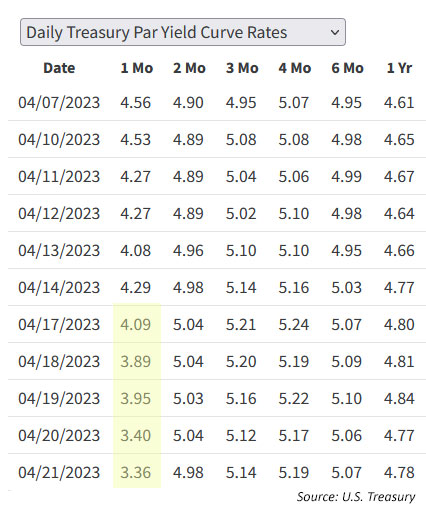

No, the bond market is not anticipating a quick turnaround by the Fed on short-term interest rates. If that were true, you’d see yields falling across all T-bill maturities. But that isn’t happening. Only the 4-week T-bill has seen yields plummet in the last three weeks, as you can see in this chart:

The chart, from the Treasury’s Yields Curve estimates page, shows that the 4-week T-bill’s yield has fallen 120 basis points in three weeks, while the 8-week is up 8 basis points and the 13-week is up 19 basis points. The same is true across the T-bill spectrum — every issue except the 4-week has seen yields rise in April.

Now, why would that happen? The reason is simple: Investors are pouring into the 4-week T-bill, forcing its yield lower, because of the near-certainty of market turmoil coming with the expiration of the U.S. debt ceiling. This is highly likely to reach “crisis” level by June, about 6 weeks from now. From the Washington Post:

If Congress doesn’t increase the limit on how much the Treasury Department can borrow, the federal government will not have enough money to pay all its obligations by as early as June. Such a breach of the debt ceiling — the legal limit on borrowing — would represent an unprecedented breakdown

If you look at the timing of this highly likely crisis, you can see that the 4-week T-bill can be purchased now and mature with a couple weeks to spare. So, in theory, it is much “safer” than the 8-week, which now has a yield 162 basis points higher. Same with the 13-week, which has a yield 178 basis points higher.

The 4-week and 13-week generally follow a similar trend line, but as the debt crisis gets closer, they have diverted:

To be clear: I am not saying that the United State will begin defaulting on its debt in June or August. That would be an utter disaster and I don’t think it will happen. But I also think there will be no resolution to this issue until we approach the brink of calamity. And that is going to cause market uncertainty.

For one thing, the yield on that 4-week T-bill will begin rising dramatically sometime in May, as we approach a potential government shutdown or debt breach.

This has happened before

2011. Back on March 6, 2023, I wrote an article (Debt-limit crisis: Lessons from the 2011 earthquake) looking back on a very similar crisis in mid-2011. This one was the most serious up to this year, but eventually was resolved on August 1. It triggered a frightening stock market collapse and solidified a near-decade of ultra-low Treasury yields. This chart shows the massive moves in Treasurys and the stock market in a single month, August 2011:

The 2011 crisis went to the brink but was resolved. Nevertheless, Standard and Poors lowered its credit rating on U.S. debt from AAA to AA+, a rating that remains in effect today.

But here is the point I wanted to make in this article: The T-bill market began anticipating the approaching crisis, with both the 4-week and 13-week T-bill spiking higher in the days before a potential government shutdown.

Of course, at this time in 2011 the Federal Funds Rate was already as low as it goes, in the range of 0% to 0.25%. So the move higher in the 4-week was only 15 basis points, from 0.01% on July 20 to 0.16% on July 29. But then again, the yield on July 29 was 16 times higher than it was on July 20.

By August 8, two days after the S&P downgrade, the 4-week yield was back down to 0.2%. In other words, the S&P action had zero effect on the U.S. Treasury market. The yield on a 10-year Treasury note was at 2.82% on July 29 and fell to 1.89% on Dec. 30. So when you hear people say, “The 2011 crisis increased U.S. borrowing costs,” just realize this is not true.

2013. A similar debt-ceiling crisis erupted in 2013 after the debt ceiling was technically reached on Dec. 31, 2012. Eventually, the debt ceiling was suspended for a few months, then reinstated. The crisis reached a peak in early October and was resolved on Oct. 16.

The chart shows the extreme, but short-lived, spike in the 4-week T-bill yield as the crisis reached a high point. Again, at the time the Federal Funds Rate was in the range of 0% to 0.25%. The 4-week T-bill yield rose from 0.1% on Sept 9, 2013, to 0.32% on Oct 15, and increase of 32 times.

What happens in a debt-lock?

I don’t think the U.S. is going to default on its debt, but there’s a real possibility we will see a short-term government shutdown and disruption to government payments. No one knows exactly how this would play out.

The Brookings Institution earlier this year issued a paper titled, “How worried should we be if the debt ceiling isn’t lifted?” It starts off with a bang:

“Once again, the debt ceiling is in the news and a cause for concern. If the debt ceiling binds, and the U.S. Treasury does not have the ability to pay its obligations, the negative economic effects would quickly mount and risk triggering a deep recession.”

In speculating on how a debt-lock could be handled, the authors note that the U.S. government created a contingency plan in 2011 at the height of the crisis:

“Under the plan, there would be no default on Treasury securities. Treasury would continue to pay interest on those Treasury securities as it comes due. And, as securities mature, Treasury would pay that principal by auctioning new securities for the same amount (and thus not increasing the overall stock of debt held by the public). Treasury would delay payments for all other obligations until it had at least enough cash to pay a full day’s obligations. In other words, it will delay payments to agencies, contractors, Social Security beneficiaries, and Medicare providers rather than attempting to pick and choose which payments to make that are due on a given day.”

You can read the full contingency plan here.

Also in March, Moody’s Analytics published a paper titled, “Going down the debt limit rabbit hole.” It predicts the actual “X-date” of potential breach is Aug. 18. It notes:

Investors in short-term Treasury securities are coalescing around a similar X-date, demanding higher yields on securities that mature just after the date given worries that a debt limit breach may occur.

Unless the debt limit is increased, suspended, or done away with by then, someone will not get paid in a timely way. The U.S. government will default on its obligations.

In discussing worst-case scenarios, Moody’s notes:

A more worrisome scenario is that the debt limit is breached, and the Treasury prioritizes who gets paid on time and who does not. The department almost certainly would pay investors in Treasury securities first to avoid defaulting on its debt obligations.

But Moody’s also notes the potential political fallout, saying, “Politically it seems a stretch to think that bond investors, who include many foreign investors, would get their money ahead of American seniors, the military, or even the federal government’s electric bill.”

I highly recommend reading through the entire Moody’s report. It presents an unpolitical and unvarnished point of view.

Final thoughts

My main point here was to show that the short-term Treasury market is already being affected by the looming crisis, and things are likely to get a lot more volatile. I don’t have answers to the “What would happen if …” questions readers often ask. We are moving into an uncertain time and the financial markets don’t like uncertainty.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I have i-bonds, but also bought TIPs through one of the well known brokers.

The i-bonds are tracking fine but really confused about the TIPs. I bought TIPs Feb 15. Received interest payments of 0.289% of my holdings. For 2 out of 6 months I would have expected 1/2* 2/6 * 6.89% = 2.3%!? I think I’m missing something in my calculations. Can anyone enlighten me?

If you bought a TIPS in February it was CUSIP 912810TP3 with a coupon rate of 1.50%. The first coupon payment will be August 15, so you haven’t received any interest yet. As of April 24 that TIPS has an inflation index of 1.01075, so your principal balance has grown 1.07% with inflation so far. The only interest you are going to receive until maturity is the coupon rate of 1.5%, paid twice a year (February and August) on the principal balance which will grow with inflation.

TIPS coupon payments are calculated as 0.5 times the interest rate of the TIPS times the inflations index for the TIPS on the date of the interest payment. None of that has anything to do with 6.89%, which is the current annualized combined interest rate for new I Bonds purchased from Nov 2022 through April 2023. Nor does it have anything to do with how many months you have owned the TIPS. When you bought the TIPS you paid the seller the interest they were due for the period from mid Oct 2022 through to your purchase mid Feb 2023. Then you received the full 6 months’ interest on Apr 15th, adjusted by the inflation index as stated above, part of which was money you got back for paying the interest to the seller.

Start here -> https://tipswatch.com/tips-in-depth/

Very key point: you state that you bought TIPS Feb 15 from a well known broker but don’t state what TIPS it was – the CUSIP of it. That would help by telling us whether it was a new TIPS at auction, as David’s post suggests, or an older TIPS from the secondary market, which is the path of the answer I suggested above.

Just went over to TreasuryDirect to confirm my IBond purchase request for tomorrow and saw the following on the login page. It was always a good idea to not buy at the last minute. I seem to recall a similar note due to the mad rush for 9.62% . . . maybe now it’s the new normal.

“Rate Change Deadline: To receive the current 6.89% rate for I Bonds, you must complete your purchase by 11:59 p.m. Eastern Time on Thursday, April 27.”

Things should be OK this year, but people shouldn’t wait until the last minute. My order is set for April 26.

I have seen this problem discussed elsewhere, with varying explanations. Here are the data I use from Treasury News, Treasury Auction Results, 4-week T-bill. The rate is the investment rate. The table is in comma delimited format so you can import it into Excel.

https://www.treasurydirect.gov/auctions/announcements-data-results/announcement-results-press-releases/auction-results/

Date,Tendered,Accepted,Rate

20-Apr,151,51,3.25

13-Apr,186,61,4.11

6-Apr,169,61,4.53

30-Mar,159,61,4.69

23-Mar,153,61,4.23

14-Mar,146,61,4.3

9-Mar,180,76,4.73

2-Mar,191,76,4.68

23-Feb,199,76,4.59

16-Feb,209,76,4.59

9-Feb,197,76,4.6

2-Feb,186,76,4.57

26-Jan,195,76,4.58

Ordinary least squares regression where Rate=f(Accepted) gives an R-squared of .58, with the Accepted variable highly significant. You can see the Accepted variable is a step function with two drops, one from 76 to 61 on Mar 14, and the other from 61 to 51 on Apr 20 (the one everyone is wondering about).

So why? Well, if Treasury is not going to Accept as many as usually Tendered for the 1-month T-bill, then Treasury can pay a lower rate. So why is Treasury decreasing Accepted? Maybe they want to pay lower interest rates.

Something to consider: The “low rate” from competitive bidders for the April 20 4-week auction was 0.0%. For the 8-week on the same day, the low bid was 4.300%. Low bidders automatically get the highest accepted rate. That means big-money bidders are just dropping in a very low bid, knowing they are 100% certain to get the high bid, and don’t care how low that result it. … A week before, the low bid for the 4-week was 3.5% and for the 8-week it was 4.490%.

And the point is: If you have big money pouring in at “whatever” yield, people making a seemingly reasonable bid will get rejected. And so the accepted rate will decline.

So why would this start happening after the end of March?

BTW, I find it difficult to believe big players are really afraid that the US would default on its debt. If the ceiling is not raised, Treasury debt will be the first to be paid, military obligations second. Other programs like social security, medicare, welfare, and other government bureaucracies might have to wait for funds until the ceiling is raised.

I would think that the most likely answer is that the big players are mostly fiduciaries who are obligated to invest prudently. It is speculative to assume that Treasuries will be paid first and even if so, it might not be advisable to invest in such securities in the middle of a political/economic disturbance.

Reality check using Aug 27 data:

Investment rate of 4 week T-bill Aug 27 is 3.91%, up from 3.25% on Aug 20. (Low rate is 2.00% on Aug 27, up from 0% on Aug 20). That is a pretty big jump in the investment rate in one week. It is still well below the 8-week, which was 5.06% on Aug 27, but not insanely lower like on Aug 20. The aberration is interesting, but probably temporary. It would appear that last week’s buyers of the 4-week T-bill made a poor decision.

My view is the 4-week will trend upward in future auctions, but then I am also close to 100% sure Treasury will not default on Treasuries. I am not much interested in those super-short term T-bills. I ladder 3, 4, or 6 month T-bills.

My view has been that the 4-week could end up with the highest yield of the all the T-bills when the “worst” hits the fan in 8 weeks or so.

That would be fine with me. I usually buy the highest yield, as long as the term is under one year. So far this strategy has generally put me only in 3, 4, or 6 month T-bills, which is more or less where I want to be anyway. The circumstances that would lead to the highest yield being the 4-week might not be particularly fine for most people.

The number Tendered is also at a low point on April 20, does that mean anything?

In 2011 and 2013 the 4 week tbill yields ROSE (spiked higher) approaching the debt ceiling. Now they are dropping sharply. I don’t get the connection you’re making. The divergence of the 4 week vs other tbills looks exactly like 2007 before the recession, like Wood said.

It’s because the 4-week is still in a safe period, outside the crisis window. That will change in a few weeks.

In 2011 and 2013 the tbills didn’t start rising until two weeks prior to the debt ceiling being reached. If your reasoning is correct wouldn’t the 4 week have started rising 4 weeks prior?

The reason: The 4-week is still outside the danger zone for the x-date for the debt crisis. So bidders at the 4-week auction know they will get a smooth transaction, with no potential chaos. This isn’t true for the 8-week bills and beyond. I do expect this 4-week yield to begin rising in coming weeks.

Given that today is April 25, both the 4-week and the 8-week T-Bills are both in the “safe zone,” as they would mature before the predicted “X-date” of August 18, according to Moody’s Analytics.

If the threat of future chaos is the reason for the 4-week yield drop, why wouldn’t the 8-week have dropped first, since it is the first one to experience the chaos?

Considering this, the explanation provided earlier may not be directly applicable to the current situation, as both the 4-week and 8-week T-Bills should be considered safe from the debt limit issue, and – if anything – the 8 week is more exposed than the 4-week?

Moody’s has a new report out this week that says the X-date could come as early as June, or possibly July. I will be posting an updated article Wednesday morning.

It’s actually the opposite. T-bills that mature before the chaos (4-Week) are in high demand from institutional and foreign investors. High demand drives bond price up and rates down. Notice the 13-Week and 26-Week auctioned on Monday saw no appreciable decline from their previous offering last week and are both above 5%. They are essentially running based on the Fed rate hikes, not the debt ceiling silliness. You would see the rate drop on the 8-Week if the X-Date was expected to slide into August instead of July.

Debt default gets the headlines, for obvious reasons, but to get a more complete picture of the turmoil in the 4-week bill market, you have to go back to the middle of March. The last day of normalcy was Friday, March 10 (4.81%); over the weekend, the yield dropped 19 bps to 4.62% on Monday, March 13. By Wednesday, March 15 the yield was 4.23%. The timing suggests that the initial catalyst for the dislocation in the 4-week bill market was not concerns about U.S. debt default, but rather the turmoil in the banking sector. As hundreds of billions of dollars fled the banking sector, it went into money market funds, and those funds are heavy buyers of the highest-rated, shortest-maturity instruments, such as 4-week T-bills. Thus the “message of fear,” at least initially, was fear about the safety of bank deposits, coupled with a belated recognition of the opportunity afforded by the attractive yields available in money market funds. This is not to deny that there will be further anomalies in the short-term bill market as we get better estimates of the X-date in the coming weeks, but it was fear about the banking sector that first disrupted the 4-week bill market, and it has been volatile ever since. The 4-week auctions are now so unpredictable, and produce such low yields, that I avoid them completely.

I’ll accept that premise, except that the decline after March 10 was across all short-term maturities. In the next three weeks all the yields went down, but ended March closely aligned. The real change in the 4-week vs 8/13-week began about April 7 and has escalated dramatically since then as the x-date nears:

Date 3-wk 8-wk 13-wk

3/31/2023 4.74 4.79 4.85

3/30/2023 4.74 4.77 4.97

3/29/2023 4.34 4.5 4.8

3/28/2023 4.24 4.39 4.8

3/27/2023 4.22 4.47 4.91

3/24/2023 4.28 4.48 4.74

3/23/2023 4.26 4.48 4.73

3/22/2023 4.16 4.56 4.79

3/21/2023 4.07 4.5 4.78

3/20/2023 4.34 4.56 4.81

3/17/2023 4.31 4.51 4.52

3/16/2023 4.22 4.66 4.74

3/15/2023 4.23 4.56 4.75

3/14/2023 4.47 4.77 4.88

3/13/2023 4.62 4.81 4.87

3/10/2023 4.81 4.91 5.01

As a practical person, my question is: Why spend so much time and energy analyzing all of this if there is nothing we can do about it? Or is there some response or course of action that you recommend, other than diversification? I’ve found that the best advice for me is not to try and time the market – is this an exception? Seems like you are predicting very volatile markets this summer. I guess that is good to know, but it doesn’t seem like an actionable piece of information.

I am a financial journalist, not an adviser, and my area of focus is TIPS, I Bonds, Treasurys and bank CDs. I’m not a stock market expert or forecaster. If I see opportunities in volatility, it will be to lock in safe, attractive yields — nominal or real.

Thanks for your perspective! I really appreciate the effort you put into this; it has helped me a lot.

Almost all guests who come on CNBC, Bloomberg, etc, are promoting their own self serving narratives. Nothing wrong with that as long as we realize to filter out our learnings from their wins and failures. Cathie Wood surprises me with her unbelievable convictions and convincing style. Having spent all my professional life in high tech, her views have virtually no value for me.

I too am old enough to know the truth:

Everybody in the world is full of their own BS. And all of it for one, and only one purpose: to make more money for themselves.

Failed species. I hand over the world to whatever comes after us.

Hypothesis:. If we’re heading to a recession, assuming no default, rates will come down, at least eventually. So buying longer dated bill and short terms notes may be a low risk no-brainer.

Further down the pike, stagflation with yield curve control and steeply negative real rates. Strong argument for I bonds and tips.

I agree, if you push attractive yields out to 1 or 2 years (or more) you can lock in a nice return, no matter the future scenarios. The 1-year Treasury is paying 4.78% and you can find 1-year non-callable CDs paying 5%. For 2-year terms the yield is lower — something to watch in coming weeks.

Agree. So far as purchasing tips, have to do it now while there’s still a real rate available before rates either trend lower or fed pivots, just as you’ve been doing all along. Great work, David.

Questions:

1. So far as the variable rate is concerned, are I bonds superior to TIPS since the variable return for each time period is floored at zero whereas TIPS can have a negative return if periods of deflation occur? Might even outperform despite higher fixed rate on TIPS?

2. If redeeming I bonds early, is the variable return for the last three months prior also forfeited?

1. The fact that the accrued principal of an I Bond can never go down in value is a major advantage over a TIPS, which have accrued principal rise and fall with inflation two months earlier.

2. If you redeem before 5 years, you lose the last three months of the latest composite rate, so you lose the variable return.

The captain of the ship, mentioned in your Barron’s online interview last year, shares your 2-year idea: two-year Treasury Notes attractive at ~4.05%

Again good and informative analysis. Yesterday, I read about the X-Date moving closer than August 18th because the SVB and Signature Bank pulled quite a bit of money fast from the Treasury into the financial system. In other words, expect “brinkmanship and chaos” pick up momentum sooner. Yes, it can represent a buying opportunity if yields go even higher for 8+ weeks Bills. In the mean time, as I said earlier, I will take 5+%. As I see it now, 4-week Bills impacted by the debt ceiling, 8 to 26 weeks influenced by the Feds rate, 1-10 year Notes influenced by somewhat cooling economy or fear of a recession, and the Bonds influenced by controlled inflation – just an observation. There is an another interesting view that I read in this weekend’s Financial Times, the new money put into the system because of the SVB & Signature Bank crises, the Fed may have reversed almost two third of the QT; this may be the reason why the stock market is somewhat calm.

Here’s an update on U.S. Treasurys held by the Federal Reserve:

April 19, 2023 $5.27 trillion

Jan 4, 2023 $5.45 trillion

May 25, 2022 $5.77 trillion

March 11, 2021 $2.52 trillion

Aug 21, 2019 $2.09 trillion

We’ve still got a LOT of quantitative tightening to do.

Indeed, a LOT of QT to do, however, as you know, market reacts to relative change or rate of change more than absolute numbers. It is interesting to oberve market sentiment or change in sentiment at the very first sign of a change. For now, p to 2 year US Treasuries and CDs seem like the sweet spot for a while.

David – Thanks for the fantastic explanation of the drop in the 4 week yield.

I gave up on Wall street gurus back when it was discovered the guests on Louis Rukeyser’s Wall $treet Week were front-running their own recommendations. Wood’s commentary a more subtle form of the same.

From Barron’s today: “On Thursday, ARK lifted its price target for Tesla from $1,533 to $2,000 a share.” The current TSLA price is $153. Her ARK Innovation fund has 10% of its holdings in Tesla.

Okay, forget subtlety.

Thanks David.

200. 100. 237. 165.

In 6 months. When interest rates drop and they will soon. Growth will explode when people naturally exit treasuries.

Pretty sure C. Woods also said BTC to $1m. Perhaps people make outrageous claims to get attention: Woods has banked over $300m in fees.

It makes sense that large corporations and foreign investors would pile into the 4-Week T-Bill which matures before the default date Janet Yellin cited would be in June raising its price and lowering its yield. I expect the same thing to happen to the 8-Week T-Bill when people realize the actual date (as forecast by CBO) is more likely to be July or August. I also do not expect a default but I do expect brinkmanship and chaos, which could cause a sharp rise in interest rates and trigger a buying opportunity in the Treasury market. It’s a little difficult to figure out exactly how that would play out but volatility seems likely in the coming months, in the meantime, I am a buyer of the April I Bond (5.4% annualized for the next 12 months) and the 13-Week, 17-Week, and 26-Week T-Bills also earning more than 5% annualized. I have no concerns about Treasury. They will play out maturing debt as always regardless of what happens.

Like your comments. Will keep in eye out for buying opportunity when there is chaos. Most people think all treasury securities will pay on time if Gov shuts down. Other types of payments may be delayed.

So, Chris, I bought into yesterday’s 13-Week and 26-Week T-Bills and the rates held up extremely well and were almost identical with last week’s auction results for those terms. Still little to no impact on the terms beyond the debt ceiling X-Date which seems to be sometime in July. I’m also in o Wednesday’s 17-Week offering.

I’m really curious to see to what extent the next 4-Week and 8-Week T-Bills will be impacted by all this. Me expecting to see some further erosion in both but we’ll see. The other interesting opportunity may come if the brinkmanship stirs up talk of another credit rating downgrade like we saw in 2011. That will be bad for our country but could cause Treasury rates to rise sharply creating a short-term buying opportunity.