Others may want to wait and watch for higher real yields.

Jan. 23 update: New 10-year TIPS gets real yield of 2.243%, highest for this term in 16 years

By David Enna, Tipswatch.com

I picked up the December issue of Kiplinger Personal Finance from my nightstand last week and began paging through. And chuckling. Why? Because nearly the entire issue was devoted to investing in a new era of declining interest rates.

Some sample headlines and topics:

- How lower interest rates affect your finances.

- Dividend payers are poised to benefit from falling rates.

- At long last, rates are dropping.

- Rate-cut winners and losers.

- Columnist: “I am wary of long-term Treasurys.”

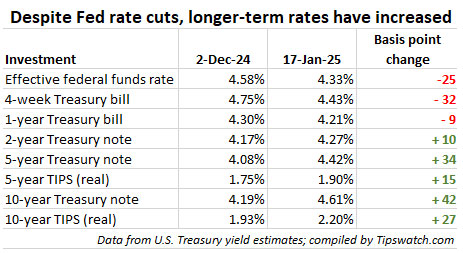

As it turns out, Kiplinger got it wrong. Even though the Federal Reserve continued to cut its federal funds rate by 25 basis points in November and again in December, these cuts had no effect on medium- and longer-term Treasurys. In fact, both nominal and real yields have increased strongly since December 1, 2024.

Let’s give Kiplinger a break, however. I was right with them in expecting to see at least slightly lower medium-term Treasury rates going into 2025. Instead, because of positive economic news and uncertainty about policies of the incoming president, medium- and longer-term rates have been rising.

And this all leads up to Thursday’s auction of a new 10-year Treasury Inflation-Protected Security, CUSIP 91282CML2. This will be the first TIPS in history to mature in 2035, and because of that I have long been targeting a purchase at this auction. I need to fill year 2035 in my TIPS ladder. I am pleased to see the potential real yield hovering around 2.20%, despite slipping a bit last week because of a so-called “soft” December inflation report.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 2.20% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.20% for 10 years.

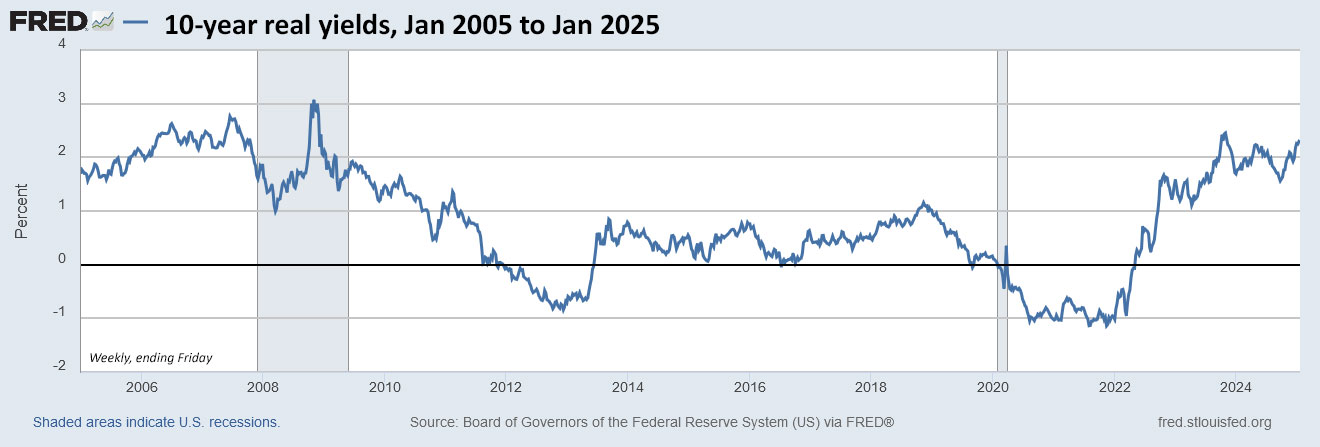

By historical standards, a real yield of 2.20% is attractive. It is actually quite a bit above the historical real return (1.80%) of 10-year Treasurys from 1928 to 2024. Take a look at this chart of the 10-year real yield over the last 20 years:

The lower yields from 2011 to early 2022 were caused by aggressive bond-buying programs of the Federal Reserve, which kept longer-term interest rates suppressed. Now we are in an era of moderate quantitative tightening and yields have returned to more normal levels.

So for me– if rates hold this week — I am going to jump at Thursday’s chance to lock in a 10-year TIPS with a real yield of around 2.20%. A few more things to consider:

- The Treasury is offering $20 billion of this TIPS, the highest ever for an auction of this term. Last year’s January auction was for $18 billion.

- If the real yield to maturity ends up above 2.20%, it would be the highest real yield for any 9- to 10-year TIPS at auction since January 2009.

- If the coupon rate is 2.125% or higher, it would be the highest for this term since January 2009.

Pricing

This is a new TIPS, so its coupon rate will be set at the 1/8th percentage point level below the auctioned real yield (most likely 2.125% or 2.250%). Because of that, this TIPS is going to auction at a slightly discounted price. Plus, its inflation index on the settlement date of Jan. 31 will be 0.99972, providing another very slight discount.

In other words, a purchase of $10,000 par of this TIPS is probably going to cost just a little less than $10,000 or maybe right at $10,000 after you add in a small amount of accrued interest, maybe $10 or so.

Inflation breakeven rate

With the 10-year nominal Treasury note closing Friday at 4.61%, this TIPS currently would have an inflation breakeven rate of 2.41%, higher than any auction of this term since September 2022. However, U.S. inflation has averaged 3.0% over the last 10 years, so the number isn’t unreasonable. (In my opinion, a 10-year nominal Treasury at 5% would start to get interesting.)

Here is the trend in the 10-year inflation breakeven rate over the last 20 years:

That’s a crazy chart, isn’t it? The shaded areas show the strong effect recessions have on inflation expectations. And yet, over the 20 years, the 10-year inflation breakeven rate never quite reached the 3.0% level of the 2014-to-2024 period. Remember: the inflation breakeven rate is a measure of sentiment, not at all an accurate predictor of future inflation.

Buy now … or wait?

Several readers have asked me why I am going to buy CUSIP 91282CML2 at Thursday’s auction (if yields hold reasonably steady). Why not just wait and buy it later on the secondary market? Waiting could definitely work. … Or not.

Waiting is a bet that real yields will continue to rise, and that definitely could happen. … Or not. My philosophy of TIPS investing is buy a yield you like and don’t look back.

Buying at auction assures me of getting the same high yield as the big-money investors, with no bid-ask spread. Also, because this is a new TIPS, you may not see many small-lot sale offers on the secondary market for several weeks.

The negative of an auction is the uncertainty about the actual yield you will receive. The advantage of the secondary market is that you can see exactly the price and real yield you will get. The negative is that you may face a small bid-ask spread. Most of the time, it doesn’t make a huge difference.

So either way is probably fine, auction or secondary market. I am choosing to go with the auction because this is a new TIPS with a good yield and good pricing. Over this week, you can track the Treasury estimate of the 10-year real yield on this page. Financial markets will be closed Monday in honor of Martin Luther King Jr.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

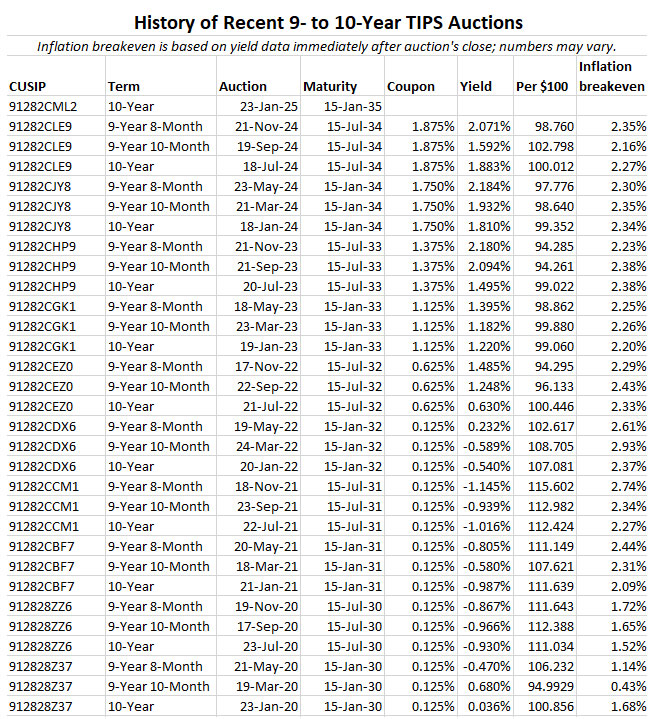

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi, David…

I’m assuming from your comments that you bought the 2035s with new cash.

Did you not overbuy 2034s and 2040s in the past, in order to lock in favorable yields for the gap years by selling them?

In this case, you will probably come out ahead, since yields have shot up so high recently.

But I am curious why you did not take the other approach.

I actually over-bought 2033 and 2034 and to a lesser extent, 2040. But my plan all along was to buy 2035, and if I can pull it off to also buy 2036 through 2039. RMDs could mess up this plan, especially if real yields start declining. My life expectancy is looking good for 2035 to 2039, but who knows after that. I might as well load up in the 10 to 15 year time frame. My ladder extends to 2043, when I will turn 90 (hopefully).

I have backup funds in my traditional IRA to allow future purchases when real yields are attractive.

I purchased different TIPS via Treasury Direct which all pay interest on JAN 15th (and I plan on purchasing today’s CUSIP as well). When the interest was deposited into my bank account, there was no indication what interest was associated with which CUSIP. Other than waiting for my 1099 in January 2026, is there some place on Treasury Direct where I can correlate the interest payments to the appropriate CUSIP? Thanks very much!

When you log into TreasuryDirect, you can view interest payments and other taxable details by clicking on the ManageDirect tab at the top of the page. Then, under the “Manage My Taxes” section, click on the year you want to view. Each item is listed separately.

The new CEO of Schwab Rick Wurster was on CNBC this morning. Becky asked about attractive new opportunities where cash deposits can earn more. He stated it’s a great time to be a fixed income investor. Specifically, if he was a retiree he would be buying TIPS!

David,

I’ve taken your advice on a number of TIPS, but when I received interest on Jan. 15, it seemed like the amount of interest was lower than it should have been. I expected an overall return of about 4%, with about half of that paid on Jan. 15. The two TIPS I received interest on were:UST INFL IDX 1.375/33INFL INDEX DUE 07/15/33:UST INFL IDX 1.75/34INFL INDEX DUE 01/15/34

I have 20 of the first and it paid $142.88 in interest, and I have 10 of the second and it paid $89.83 in interest.

What am I misunderstanding as far as the interest. It seems like they are only yielding closer to 2%.

Thanks,

Brent Fine,Chandler, Az

Hey Brent, Here’s how it works: The inflation adjustment is each month added to your principal amount (or subtracted if there is deflation) and accrues as long as you own the bond. The inflation-adjusted principal then gets paid out upon maturity. Meanwhile, you get paid the coupon interest on accrued principal… in your case 1.375 and 1.75. Said another way, you periodically receive coupon payments, but you get all of the inflation adjustment at the end (upon maturity). If there is more deflation than inflation over the entire term of the bond (unlikely but possible), you are promised the original par value upon maturity. If this layman’s explanation doesn’t satisfy, i’m sure David will chime in.

Thanks, I thought that is how the interest may be made up. If inflation really goes up can you get paid over par at maturity?

It is highly probable (like nearly 100%) that you will receive more than par value at maturity. At maturity you receive:

Par value x inflation index + one final coupon payment.

No TIPS in history has matured with an inflation index of less than 1.0 (it could happen, but is so far is extremely unlikely).

Also note that while the coupon interest rate is stable, the amount paid out will rise as principal rises with inflation. Take a look at this: https://tipswatch.com/tips-in-depth/

Well done, Tahoe!

Thanks for all your help Tahoe and David. I just put in an order for the new TIP through my brokerage at auction. There is no way we won’t have inflation with the amount of debt we’re creating and this continued push to cut taxes more. The only way to solve the debt problem is through reduced spending and revenue increases, and expecting tariffs to make up for the costs of inflation and probably going into a recession by a trade war will only make the problem worse. (my opinion — worked at state level for BLS for 20+ years).

The coupon rate is your cash payout; the other part of the interest is the inflation adjustment that is added into the principal of the bond. That is why it is recommended to own in a tax deferred account, the taxable income will be higher than the cash received (as long as we have CPI inflation). The good news is the coupon rate is paid on the increased value of the bond, so you cash payout will be higher going forward (as long as we have CPI inflation).

I will be a buyer for my partner and me in our respective Traditional IRAs to add to our TIPS ladders. I retired young knowing inflation would likely be one of our greatest financial risks and to hedge that figured four components were essential and address some of the concerns raised above:

A lot of wisdom here. Sounds like a sensible plan. As we get closer to the actual crisis (about 2033) cuts in Social Security benefits become more likely. The time to act is now with a plan for gradually raising the retirement age (slightly) and taxing higher levels of wage income. But that won’t happen, certainly, in the next four years. (Would we really eliminate the tax on Social Security benefits, which I pay and seems fair to me? That money goes back into the trust fund.) This will be a much tougher problem to solve if we wait too long.

David, I’m trying to understand what you mean by buying TIPS to cover RMDs. Can you better explain?

Are you estimating future IRA growth and then calculating an estimated RMD amount X for a given year and then purchasing a TIP that will grow to amount X? Is the idea that your IRA is invested in growth assets and you want to avoid selling assets in a down year? Or is it that you want to hold lots of TIPS into the future but want to have a a TIPS that grows to amount X at maturity for each RMD year so that you avoid selling partial positions?

Thank you for all the great education you provide.

My traditional IRA is almost entirely invested in fixed-income and 70% or so is in the TIPS ladder. This isn’t the growth section of our overall asset allocation. I just tried to set up yearly inflation-adjusted principal amounts for each year that would “just about” cover my potential RMDs, money that will be withdrawn each year and probably spent. The ladder also generates some amount of coupon income, which could also be used to for the RMDs, if needed. In other words, this one account is set up to produce inflation-adjusted income each year.

I was late to understand TIPs, but with David’s constant info flow, I “tipped” into the TIPs world last year in my and my wife’s IRA.

I’m 65 and my wife is 68, both retired, but have enjoyable “post-corporate world” businesses (self-employed) we stay busy with that provides sufficient cash for day-to-day needs. We are not taking out any funds from retirement (IRA or ROTH) and when supplemental cash is needed (trip/big expense), just draw from cash in non-registered accounts.

As I learned about TIPs from David, posts on Bogleheads and videos by others, it was clear that TIPs work well when its solving a need/problem.

So my approach, like David’s strategy, was to link my expected RMD withdrawals from the IRAs for my wife and me. Her’s starts in 2029 & mine in 2032. I used some online calculators to estimate the RMDs and just bought that face amount for each year. So, as I understand, I will have an inflation adjusted amount to fulfill my future RMD, along with some coupon income each year till maturity.

I bought ’29 through ’34 years for my wife and one in ’40. Not keen to buy further out as the up front price just feels “too much”. Instead, now have 3x amount in ’34 (bought more through the year as YTW >2) to “gap” out those open years (’35 – ’39). Will buy the new ’35 10 yr at auction on Thursday (first time at auction as previous purchases on secondary).

Anyway, I feel good to have a plan and hopefully it works out. Regardless, still reading David’s articles and the great comments it attracts.

Thank you for this highly positive feedback.

UPDATE, Tuesday 8:30 a.m.: Treasuries have resumed trading on the secondary market after the holiday weekend and the most recent 10-year TIPS (issued in July 2024) is now trading with a real yield to maturity of about 2.16%, so down a few basis points from last week.

I’ve purchased TIPS bonds both at auction and inthe secondary mkt. The only thing that constrains me from increasing my allocation is the question as to how well the index tracks inflation. Investopedia presents an easy to understand description of some of the difficiencies. Seems that the chance of materially understating actual inflation is not insignificant. That said, a perfect inflation does not exist. The is not to ditch TIPS. Rather, from an asset allocation standpoint, it makes portfolio diversification a necessity.

When you buy a TIPS, you are accepting the terms: Principal adjustments are based on official U.S. inflation. So that’s the deal. Many people feel the official inflation rate is understated. I don’t know, but it is the rate that connects to a TIPS investment. Everybody’s personal rate of inflation is different. The bigger issue would be if the government starts altering “official” inflation to make things seem “better” or to cut other costs, like Social Security benefits. I don’t think that has been happening, so far.

That’s my main concern too. I would not expect this to matter much for this 10Y security but when we are talking about the 30Y auctions, then we are also talking about timeframes long enough where ‘kick the can’ will likely reach its limit. And then the question becomes how the government choses to deal with its deficits and debt load.

My guess is that adding further bias to the CPI methodology will be the most politically opportune way of solving some of these problems. And the target will not so much be TIPS but social security. Lowering the interest cost of TIPS will just be a welcome but minor side effect of that policy. So if I invest in a 30Y TIPS I want to have some higher yield buffer to account for this risk.

Steve G,

You might consider testing out a personal inflation calculator as inflation is highly personal. My colleagues and I studied inflation rates related to medical and non-medical expenditures, and the index is one thing, but how your spending is allocated and priorities is highly personal and potentially flexible. Here is an example calculator-https://cdn-1.umb.edu/editor_uploads/calculator/personal_inflation_calculator.html

But, the risk you’re inflation- hedged income investments address in a worst case is a real risk and the broad index used is likely less important – stagflation periods like my first 18 years of life when the S&P 500, with dividends, returned 0% relative to inflation – https://ofdollarsanddata.com/sp500-calculator/. Hard for my parents to save for five college educations so we were pretty much on our own. If TIPS had been around (introduced in 1977) they would have been a real help.

That’s difficult for many of us to recall due to age and recent experience. For comparison, my son’s college fund returned 4% annually relative to inflation and, since he chose not to go in 2016 it is 6x on the initial investment AFTER adjusting for general inflation (7% annual real return). But, college prices rose even faster so that is a great example of a narrow, highly personalized component of inflation much like my potential long term care bill may be.

TIPS held in a Taxable Brokerage Account vs IRA vs Roth

Is record keeping and taxation for a taxable brokerage account an issue?

I couldn’t find a specific answer in your previous posts. It would appear that you often mention them in a tax deferred account IRA/401k. I did learn this week that I could convert a total individual TIPS Bond at Vanguard from my IRA to my Roth. I forgot to ask if I could do a partial conversion of an individual TIPS bond. It’s my strategy to convert to a Roth prior to starting Social Security and while in a lower tax bracket. Keeping in mind other taxation issues. The Roth funds can continue to grow tax free, but I will remain with a healthy percentage of Index Funds for long term growth. Thank you.

For a TIPS in a taxable account, you pay taxes on both the coupon payments AND the annual inflation accruals, which aren’t actually paid out until you sell the TIPS or it matures. This isn’t a huge deal, but it is the reason people prefer TIPS in a tax-deferred account. Taxable-account TIPS generate a 1099-INT and a 1099-OID each year, two separate IRS categories. A hassle, but again, not a huge deal. (I’ve held a few TIPS in a taxable TreasuryDirect account for years, so I am used to it.)

Delivering a bond (or even bond fund shares) from an traditional IRA account to a Roth in conversion can create a weird problem: What basis will be reported to the IRS? I find this very confusing, so I try to convert to cash before converting or withdrawing from a traditional IRA. Making Roth conversions is probably a good strategy, when you can.

I have delivered several TIPS bonds (not funds) over the years, in kind (not cash), from my traditional IRA to Roth, and the basis reported on the 1099R is the market value at the time of the conversion. So I know right away when I convert what the taxes due will be. In case this is helpful.

Last year I moved some Total Bond Fund (BND) directly from my traditional IRA to a Roth, and the reported value on 1099-R was the cost basis of the shares, not the current market value, which was lower. That really surprised me. It was a small amount, done as an experiment. From now on, I am going to transfer cash.

I am interested in this Cusip at Thursday’s auction. However, I would like to hold it in a tax deferred account. You mentioned I believe that you buy at auction and hold in an IRA account. I have not previously purchased a TIPS at auction but have purchased Treasuries and held in taxable account. How do you buy on TD in a new auction and hold in an IRA account? On TD I see you can link accounts but it appears to be TD accounts, not accounts with other custodians. What am I missing? Thank you!

TreasuryDirect does not allow tax-deferred accounts. However, if you have a tax-deferred account (such as a traditional IRA or Roth IRA) at a brokerage, you would be able to purchase it there, without commission on major sites like Vanguard, Fidelity and Schwab. You would get exactly the same result as on TreasuryDirect, but you would be required to buy in $1,000 increments. The order for a brokerage has to be placed at least by Wednesday or very early Thursday, because the brokerages cut off orders about 3 hours before the auction closes. So the key is: Do you have a tax-deferred account at a brokerage? Also, keep in mind that after the purchase, the brokerage will show the “mark-to-market” value of that TIPS, which can be annoying. If you are holding to maturity, ignore the fluctuations.

Yes, have tax-deferred accounts at brokerages. But have to have funds available in the settlement fund or have adequate time to transfer funds in from another source to buy. Generally don’t hold funds in settlement accounts. Not sure time available to transfer in cash. Will continue to check yields as you suggest, but may still do new one in TD.

If you act Wednesday, you would have plenty of time. The settlement date for the auction is Jan. 31, so you’d have more than a week to arrange the funding. When you place the order your brokerage may warn you don’t have the funds to complete the purchase, but you would probably be able to complete it and move the money in well before Jan. 31.

I am assuming your TD account is linked to a bank and not a brokerage account? You have many options, anyway. You could get the cash into the brokerage account and buy later on the secondary market. But that’s a bit more complicated.

Test comment!

This will be my first auction buy for this 10yr TIPS, compared to previous secondary buys in fashioning a ladder. I had to think through the factors in pricing you mention here, and your FAQ on pricing answered my questions. Thank you.

I’ll be interested to hear your thoughts as we get closer to the 30-year TIPS. My life expectancy should get there, and the odds for my wife are even better.

I will be posting a preview article on that 30-year TIPS auction on the morning of Sunday, Feb. 16. The auction is Feb. 20.

Any educated guess on how the ‘extraordinary measures’ Yellen says will need to be performed this week by the Treasury will effect this TIPS auction?

It has happened several times before. Not good news but also not dire, at this point. The good thing is that this begins the pressure on Congress to settle this issue. Yellen has already left the office of Treasury Secretary. The majority of both GOP and Democrats in Congress do not want a debt-limit super-crisis.

I am 76 now. My TIPS ladder goes out 7 years and my TIPS are about 55% of our fixed income portfolio with another 20% in ibonds (mature in 2031).

Do you have an opinion on how far out a TIPS ladder should extend? Is there a rational rule of thumb one could use?

I’d say it depends on your state of health and if you have a spouse that could out-live you. As I have noted, my ladder extends to age 90. I might make it, might not. This is a personal decision.

Meanwhile – the real yield on the 30-year TIPS is > 2.5%… what about next month’s 30-year TIPS auction? It seems that if one is nearing retirement, that would be a fantastic yield to lock in (provided you get a favorable auction result) – am I correct there?

For the right person, it should be appealing. That new one will mature when I am 101 years old, so it isn’t for me. I buy TIPS to hold to maturity. In the past, I have bought a couple 30-year TIPS, one maturing in 2029 with a real yield of 3.89% and one maturing in 2041 with a real yield of 2.12%. Still holding them in a taxable account at TreasuryDirect. The new 30-year could be attractive to traders because it will be highly volatile and will gain in value if interest rates start declining. That’s a risky strategy.

Is’t locking in money for 30 years a problem? You only get the interest payments. What if you need money before those 30 yrs? What if you die?

This is why a ladder is helpful, because you have maturities each year providing cash flow. I Bonds work well for this also, because they have a potential 30-year term but can be redeemed with no penalty after 5 years. Better flexibility but also a lower fixed rate (1.2%) versus about 2.47% real yield on the 30-year TIPS.

Quick question: Does the size of the auction have any effect?

PS: There’s a typo in the Pricing paragraph.

Up to this point, I don’t think the size of the auctions — which has been steadily increasing — has had an effect on demand. Eventually, it could. Thanks for the tip on the typo.

Thank you for this update. I am building a 20 year tip ladder starting in 2031 thanks to your web site and information. I basically trying to buy $35,000 a year of additional social security startign on my RMD year. I plan to use this auction to fill 2035, 2036, & 2037. The tip ladder generator suggests 91282CLE9 x 89. I assume I at auction I will enter an order for 90. Any tips or feedback would be greatly appreciated. Love this site!

You will probably be able to put in an order for 89, if you wanted. 91282CLE9 matures in July 2034, so this new TIPS would also be a nice gap-year alternative, maturing in Jan 2035. Just keep in mind that real yields could continue climbing. If you commit to holding to maturity, ignore the noise.

Thanks, David! Planning to hedge my bets—buy at auction, then more later if the price is right.

Thanks for this info. When I made my 20-year TIPS ladder last year, I filled in the then “uncovered” years of 2035, ’36, and ’37 with quantities of CUSIP 91282CJY8 to get my interest and income for those rungs. I didn’t really think about how soon 10-year TIPS for those years would be issued. The money is spent so I assume there is no further move to make, but I’ll be watching this new TIPS issue with interest and a bit of FOMO.

This was actually the “recommended” strategy but of course I had to complicate things by setting up money for purchases in 2025 and maybe for future years. The risk is that real yields will decline in the meantime, while you will do fine with good real yields from last year. (I also over-bought, a bit, for 2032, 2033 and 2034. I real like the 10-year timeframe.)

Can you expound on your preference for nominals (for 5 years and under) vs TIPS for longer periods?

Very short-term TIPS (1 year or less) have greater deflation risk than medium- or longer-term TIPS. Outside my traditional IRA, my 1- to 5-year Treasury or CD investments are targeted to meet specific spending goals or to maintain our cash bucket. That doesn’t need inflation protection. All of my TIPS purchases are now in my traditional IRA and the nominals are set up to either 1) fulfill RMDs in near-term years or 2) buy TIPS to mature in years 2036 to 2039. So gradually these will pare down to zero.

I too used 9128CJY8 to cover the gap years in my TIPS ladder. I presume it doesn’t make sense to sell the TIPS matched for 2035 and buy this new issue? How do I decide doing this in general?

No, I don’t think it would make sense to sell one TIPS to buy another TIPS, even if the real yield is now higher. The TIPS you own now has a market-adjusted value so it would be more or less a wash. One other option would be to simply purchase an additional holding in this new TIPS.