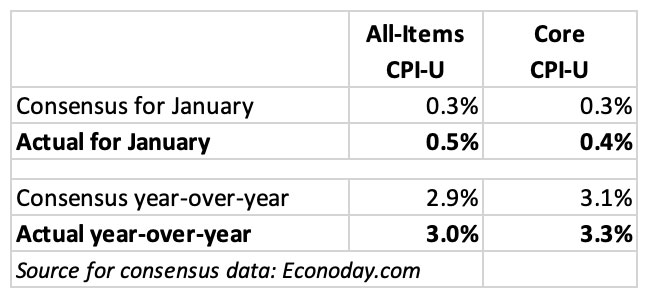

All-items and core inflation both rose much higher than expectations.

By David Enna, Tipswatch.com

The January inflation report, just released by the Bureau of Labor Statistics, demonstrated that U.S. inflation is far from tamed. This was not good news.

There is no silver lining here. Seasonally-adjusted all-items inflation increased 0.5% for the month and 3.0% for the year, both above expectations. Core inflation, which removes food and energy, rose 0.4% for the month and 3.3% for the year, also above expectations. Annual inflation by both measures increased over December levels.

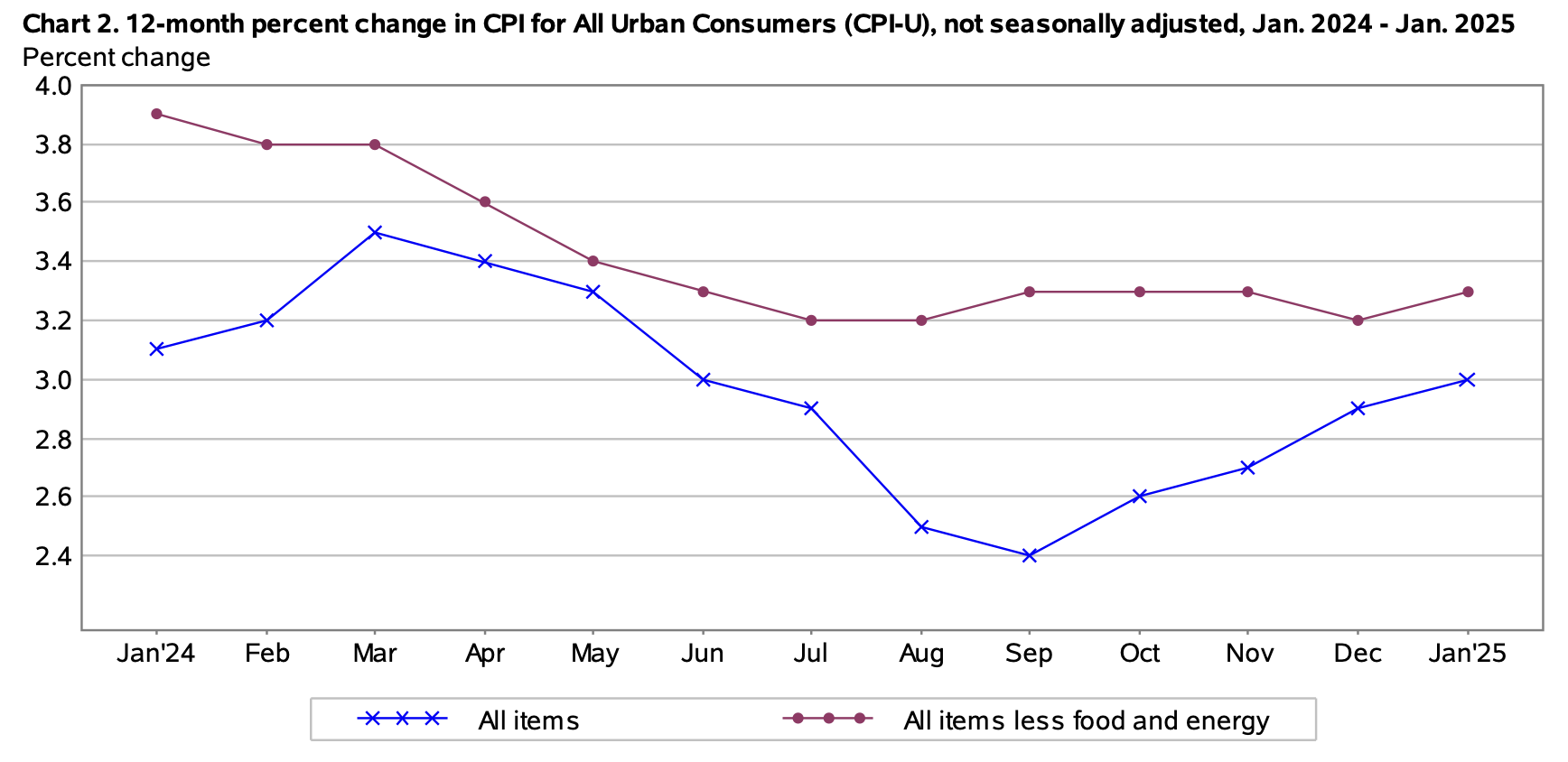

This one graph, tracking the year-over-year trend line, shows it all, with all-items inflation steadily rising higher since fall 2024 and core remaining stubbornly above 3.0%:

The BLS noted that shelter costs increased 0.4% for the month and 4.4% for the year, a major factor in the overall increase. And gasoline prices rose 1.8% for the month, after rising 4.0% in December. Food at home prices increased 0.4% for the month and are now up 2.5% for the year. The price of eggs, for those curious, rose 15.2% for the month. It’s time to switch to breakfast cereal, where prices declined 3.3% for the month.

The BLS said prices were up across all major categories except apparel, which saw costs decline 1.4%.

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which adjusts principal on TIPS and sets future interest rates for I Bonds.

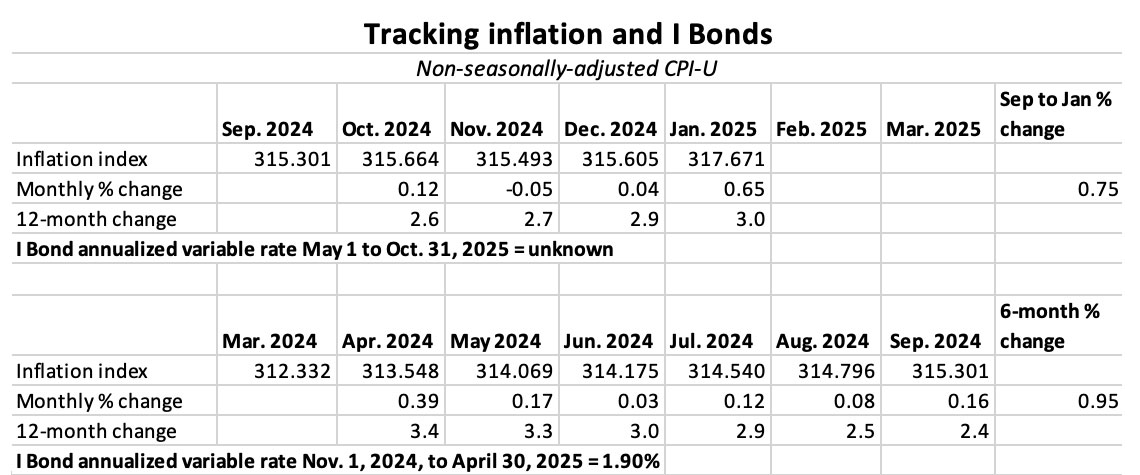

The BLS set the January inflation index at 317.671, a sharp increase of 0.65% for the month. A high number was expected, because non-seasonally adjusted inflation runs higher than adjusted inflation from January to June. But 0.65% was higher than I expected.

For TIPS. The January inflation number means that principal balances for all TIPS will increase 0.65% in March, after rising just 0.04% in February. For the year ending in February, principal balances will have increased 3.0%.

For I Bonds. January is the fourth of a six-month string that will determine the I Bond’s new variable rate, which will be reset on May 1 and eventually roll into effect for all I Bonds. At this point, with two months remaining, inflation has increased 0.75%, which translates to a variable rate of 1.50%. The next two months are likely to push the variable rate up to around 3.0%, or higher. We’ll have to wait and see.

Here are the numbers so far:

What this means for future interest rates

The January surge in inflation (which has been a January trend for several years) supports the Federal Reserve’s decision to hold interest rates at current levels, and probably means no rate-cutting is coming for many months.

This is from Bloomberg this morning:

Seema Shah, chief global strategist at Principal Asset Management, says these numbers are “very uncomfortable” for the Fed. Here’s her view: “If this persists into the next few months, inflation risks may become too heavily weighted to the upside to permit the Fed to cut rates at all this year.”

And this:

The danger is that this elevated inflation reading and the news headlines it produces will add to inflation expectations. They had already been ticking up amid all the discussion of tariff hikes from the Trump administration.

In essence, it would make no sense for the Federal Reserve to make any rate decisions (or even signals) for several months. We are on pause and the potential for rate increases is slightly rising.

I am writing this morning from Santiago, Chile. That is the reason for the abbreviated analysis. And it is time for my vacation to continue!

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David, thank you for this detailed analysis of the January inflation report. It’s clear that the higher-than-expected rise in both all-items and core inflation is concerning, especially with shelter and gasoline prices continuing to increase. Your insights into the impact on TIPS and I Bonds are very helpful for investors looking to navigate these uncertain times. It seems like the Federal Reserve will need to remain cautious with interest rate decisions for the foreseeable future. Enjoy your vacation in Santiago, and thanks again for keeping us informed!

Its almost like all the people slamming the Fed for cutting prematurely (and by so much) were correct!

If Treasury bonds are not secure there would be no future in anything but land.

anyone notice that TreasuryDirect added a 6 week T-BILL to the upcoming auctions I thought they were trying to simplify?

I’m guessing the Presidents Day holiday – Mon 17th – is altering the schedule

Six-week issue is here to stay. “We auction 4-week, 6-week, 8-week, 13-week, 17-week, and 26-week bills every week.” Their updated Tentative Auction Schedule of U.S. Treasury Securities shows the 6-week bill every week going forward.

David, any metrics available on Treasury operations and/or in/outflow of specific Treasury securities given decreasing personnel due to DOGE or lack of confidence in near/future term…ie no “run” in any forecast(s)?

Haven’t heard of any problems yet. (But I am still traveling in remote South America.)

It does seem a little odd. That CUSIP (912797MV6) was previously released as a 26- and 13-week T-Bill. I don’t recall seeing that done with any in the 13-week chain before, but maybe they have. I wonder why now though.

Clarifying my own post a bit, it’s adding the 6-week level that seems to be completely new. 26- to 13-week is a normal progression just as 17- to 8- to 4-week is normal.

I found a note from Treasury when looking at the daily yield curve rates today too:

Effective with the inaugural auction of the new benchmark 6-week Treasury bill on Tuesday, February 18, 2025, Treasury plans to include 6-week bill prices in its input data set for the daily yield curve. Treasury also plans to add a 1.5-month CMT to the Daily Treasury Par Yield Curve Rates and 6-week bill rates to the Daily Treasury Bill Rates that it publishes.

Changes to the published tables and data files to accommodate the additional rates will appear beginning in the evening on February 14, 2025.

They’ve been issuing “42-Day Cash Management Bills” as reopenings of the 26 and 13 week Bills since ~mid 2023. It seems they’ve “graduated” to the more-permanent issuance schedule now that they’re being called “6 Week Bills”

Excellent info. So now the 42-day goes away? I can’t do much research while on Rapa Nui!

Appears so — this past Thursday was the first week they didn’t issue a 42 Day Cash Management Bill. Which makes sense as there’s no need for both a 42 Day CMB and 6 Week Bill! Enjoy your vacation!

I love TIPS as a retirement investment, but I worry about the potential for the CPI numbers to be tampered with for political purposes. It seems to me that small tweaks to the basket of goods and the relative weighting of each could be used to calibrate the number to a desired result.

Are there any effective guardrails in place?

BLS culture focuses on getting accurate estimates out on time. Getting it right is hard enough. Efforts to bend it one way or the other would make the work impossible. Any such efforts would probably be quickly leaked. The only political appointee at BLS is the Commissioner.

BLS has been able to do its work without political interference since the Nixon administration. Nixon had Freddie Malek purge Jews from top BLS management (See Nixon Presidential Library for documentation.)

Another Nixon initiative was to have the monthly jobs numbers reported directly to the White House so Nixon staff could frame the numbers as they saw fit. In response, the Joint Economic Committee of the House and Senate began requiring BLS to report directly each month on the current employment situation.

Recent outside commentary about how housing costs are included in the estimator are taken seriously. Similarly, the MIT Billion Price Project was considered. BLS continuously works to improve the accuracy of their measurements. That is the way they work.

Maybe, but recently Trump and Musk have shown they are not afraid to take a wrecking ball to the workings of the federal government.

I do like tips and i bonds, but I also do not completely trust the numbers, and in my opinion it is foolish to do so.

In my opinion the hard currencies: gold, silver, and now bitcoin and ethereum are truly showing dollar inflation. A mixed portfolio of these currencies is showing something like 20-80 percent dollar inflation per year! averaged over the past 10 years.

Is this a new worry or simply because of the change in administration? This has been a worry and talking point on the right for quite a while, curious if its time for the reversal!

The oft-repeated rule of thumb that “non-seasonally adjusted inflation runs higher than adjusted inflation from January to June” is not quite borne out by data since 2014. If there is a pattern, it’s that lately NSA CPI-U is higher than adjusted CPI-U from about March to October.

Specifically, NSA was higher MAR-SEP 2014 to 2016, and MAR-OCT 2017-2024.

To make things interesting, BLS on Feb 12, 2025 revised all the seasonally adjusted CPI-U figures since JAN 2020, but the pattern holds. https://www.bls.gov/cpi/seasonal-adjustment/

It remains true that total upward and total downward adjustments roughly balance in the long run. From 2014-2024 they differ by less than 4%.

Yes, there is valid reasoning for the treasury to default on your investments. Good grief. If that happens you better have enough food, ammo and gold for years to survive. Because your tips, tbills and ibonds will be the least of your concerns. It will be armageddon.

Where is this nonsense coming from? In all seriousness, I thought we were level headed around here.

My response to those worried about treasury default is similar: yes, it’s a mathematical possibility but if you are worried about it, don’t fret about your investments, start reviewing your ability to repel hordes of zombies.

Prior interpretations are correct.

Argue that US debt securities are a great investment all you want.

Just don’t tell me they’re risk-free. If they ever were, they very certainly aren’t now.

Buyer beware, as the saying goes.

hi GreenAcres, You are of course correct that no investment is 100% risk free. There, i said it. The reason we’re all on this here website is because US Treasury TIPS are the lowest or near-lowest risk way to preserve purchasing power going forward. What else do you propose? Bet the farm on stocks and/or crypto? Good luck. Cash under the mattress? Good luck. Bury goldbars in your backyard? Good luck. If the UST is unable or unwilling to repay domestic holders of TIPS, there will be chaos in the streets, and someone will hit you on the head (or worse) and take the bars when you try to redeem. Here at TIPSwatch (in contrast to most other websites) most readers aren’t interested in arguing about worst-case scenarios about societal collapse; we’re into building the most logical approach(es) to low-risk preservation of purchasing power, assuming cooler heads and the rule of law will prevail, at least for our lifetimes.

Well said, Tahoe

I like inflation protected bonds precisely because the mainstream never mentions them, which must mean there is some value there.

The mainstream, everybody, their dog, and their uncle believes the American stock market rises, forever, to infinity. So far they have been right, but there will be huge repercussions when they are wrong.

The January inflation report was not a disaster for holders of Treasuries (if holding to maturity) and I-bonds. Increased rates means more money for us. Some would say the increase in interest income is offset by the inflation rate, but for me, my expenditures are modest, and an increase in I-bond or Treasury rates is just more more money for me to spend or save.

Perhaps not bad for some individuals now, but this signal points toward potential disaster for the larger scale economy.

Thanks for the report and analysis David. Very helpful, as always. Enjoy your vacation!

Higher CD rates do not come with reduced inflation…thanks Mr. T…keep up the great work!!!

Long-time readers know what to expect when DE gets the travel bug. Buckle up!

Speaking of obvious precautions, I continue to ask myself why would anyone rational buy USG obligations right now?

Has the phrase “risk-free”, never mind the assumption, ever seemed more ridiculous?

Smart people buy Treasuries to hold to maturity. For me that is 3 month T-bills for the time being. Where else can I get a 4.3% annual return, completely liquid, risk-free, with no state income tax on the interest? If you live in a high state income tax state like New York or California, that is important.

Patrick, perhaps Green Acres will return to post again for him/herself, but I take the post above (“Has the phrase ‘risk-free’ . . . ever seemed so ridiculous?”) to mean that, with all the shenanigans going on in the current administration generally, and within the Treasury Department specifically (unelected 20-something Muskrats, as I’ve heard them called, accessing the guts of the Treasury’s Fiscal Service systems), the standard assumption that Treasury securities are a risk-free and sacred public obligation has started to become more questionable.

David, I am not at all worried about the U.S. government defaulting on its debt. If it does, it is the end of the global economy. It will be guns, ammo, and beans time.

Having said that, no investment and indeed nothing in life is completely risk-free. However, US Treasuries are about as close to risk-free as you can get.

I do hope Elon’s nerds don’t make any mistakes like deleting accounts when messing around with Treasury investments. I have screenshots of all my accounts, and Schwab has records of them all too. It would be amusing if the nerds accidentally deleted nearly all of our national debt, but sort of a hassle putting it all back together.

I think the relevant question to go along with this is what else would a rational person do with their dollars instead of buying Treasury Bonds? Does the current apparently higher risk for government debt mean these are now riskier than other US$ options or that risk levels for all US$ investments are now higher than they were before?

Dollar denominated foreign sovereign bonds do exist. There are a few bond funds in this space. https://etfdb.com/etfdb-category/international-government-bonds/

Re: “I am writing this morning from Santiago, Chile. That is the reason for the abbreviated analysis.”

David, your “abbreviated” analyses are better than most of the mainstream press’s “in-depth” analyses. 🙂

Agree.

Well said and agree 100%.