By David Enna, Tipswatch.com

I am writing this on a gorgeous Friday night in Rapa Nui, also known as Easter Island. I am sitting in the open-air lobby of a nice hotel, because everywhere else the Internet is non-existent.

So OK, let’s try to focus on this week’s auction of a new 30-year Treasury Inflation-Protected Security, CUSIP 912810UH9. This is a new TIPS, so its coupon rate and real yield to maturity will be set by the auction results.

At Friday’s market close, the Treasury estimated the real yield of a 30-year TIPS at 2.38%. If that real yield holds through the week, this TIPS would get the highest yield above inflation of any originating or reopening TIPS auction of this term since the Treasury re-started issuing the 30-year TIPS in February 2010.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 2.38% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.38% for 30 years.

Potentially, the coupon rate could be set as high as 2.375%. All of this looks very good.

The problem with this TIPS — for me and many others — is the 30-year term. My investing style is to buy TIPS and hold to maturity. This TIPS will mature February 15, 2055, when I will be 101 years old. it’s not a good choice for me.

The other thing to realize about any 30-year TIPS is that it will be a highly volatile investment, plummeting in value if real yields rise, but also producing a big interim gain if real yield fall.

For example, the 30-year TIPS issued in February 2022 got a real yield of only 0.195% and it is now selling at a price of about 56.33. In other words, it has lost about 43% of its value in only three years. This week’s auction will get a much much better real yield, but it will still be volatile. That’s my warning.

For a 30- to 50-year old investor who could easily hold to maturity, this TIPS is attractive as the top line of a 30-year TIPS ladder. Getting around 2.38% above inflation is going to work out well, even if real yields continue to rise. But only if you can hold to maturity.

Here is the trend in the 30-year real yield over the last 15 years (since the Treasury began to issue 30-year TIPS after a 9-year pause):

Take a look at this graph and you can see the 30-year real yield is now in a desirable place. But it could go higher. It could go lower.

Inflation breakeven rate

With a 30-year nominal Treasury note yielding 4.69% at Friday’s market close, this TIPS currently would have an inflation breakeven rate of 2.31%, which is high but not out of the range of recent results. Over the last 30 years, inflation. has averaged 2.5%.

At some point, a high inflation breakeven rate would make the nominal Treasury attractive, but there is no way I’d be buying 30-year nominal at this point.

Pricing

CUSIP 912810UH9 will carry an inflation index of only 1.00016 on the settlement date of Feb 28. Because its coupon rate will be set slightly below the auctioned real yield, it is likely to have an investment cost very close to par value.

If you order $10,000 of this TIPS, you will be paying a price close to $10,000.

Thoughts

I am not investing in this. But for the right person with the ability to hold to maturity, CUSIP 912810UH9 should end up being an attractive, sensible investment.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

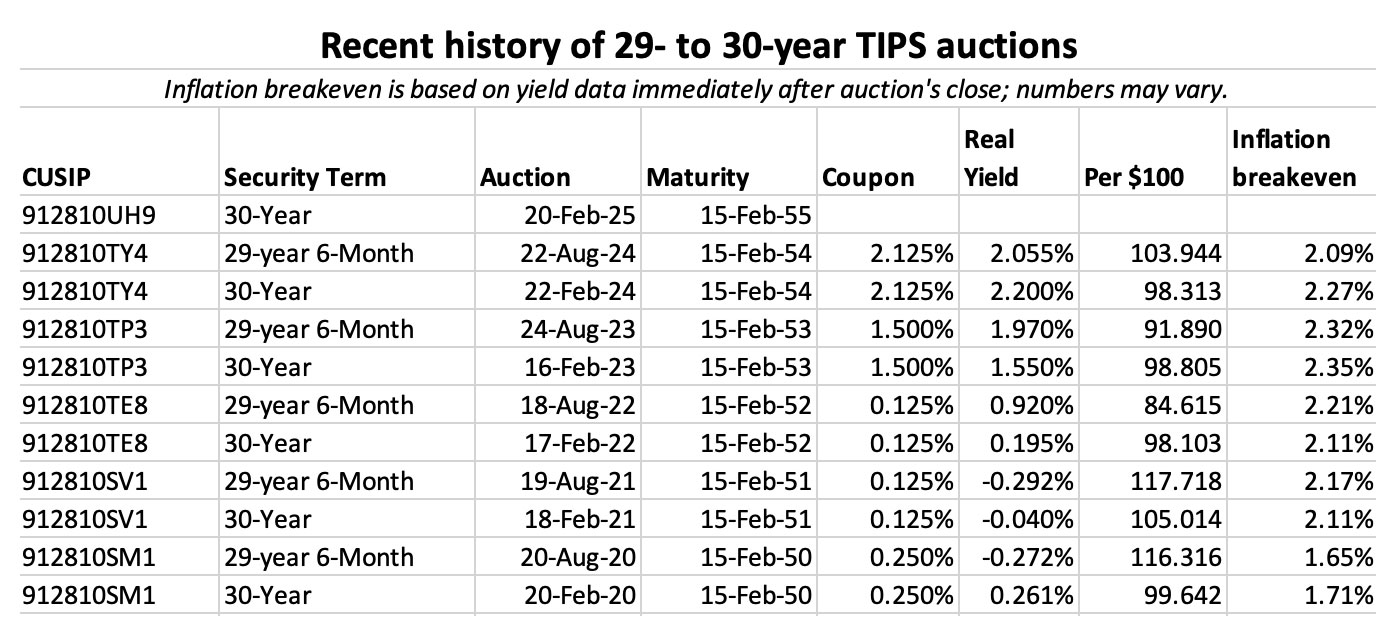

I will be posting the auction results sometime Thursday. Who knows? I am on vacation. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

When you wrote, “At Friday’s market close, the Treasury estimated the real yield of a 30-year TIPS at 2.38%,” where do you find these estimates of the real yield in advance of a TIPS auction? Also, are these estimates updated daily, or only on certain key days leading up to an auction? Thanks!

The Treasury issues yield curve estimates every market day, after the close. You can find the real yield listings here: https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_real_yield_curve&field_tdr_date_value_month=202503

Wednesday evening update: The Treasury’s estimate of the real yield of a 30-year TIPS closed Wednesday at 2.40%. I am getting a “sort of feeling” that Thursday’s auction will get a slightly higher result. (I am often wrong.)

The amount of volatility for a 2.25% coupon bond will be a less than the practically zero coupon (0.125%) 2051/2052 bonds.

If real yields go north of 5% you could see the price drop to around 56. That a stretch, but I think 3% real yields are very possible and that would be a price of 85. 4% real yields would be a price of 69. Perhaps that is a good worst case for planning.

Long duration is definitely a factor one should consider.

Personally, I am looking at “30 year retirement planning” and average life expectancy plus the 10 year “non-spousal beneficiaries withdrawal rules”. This year still makes sense. Next year…we’ll see.

There is a foreign sovereign government inflation protected security ETF, WIP. Currently with only $300 million in assets at a high 0.50% expense ratio. Roughly a third of it is emerging market (Brazil, Chile, Colombia, Mexico, South Africa, Turkey) so may be of too much risk for some. https://www.ssga.com/us/en/intermediary/etfs/spdr-ftse-international-government-inflation-protected-bond-etf-wip

I looked at this years ago and decided, “nope.”

David, excuse the really ignorant question…I’m just starting to learn about TIPS. Anyway, you mentioned that the TIPS will be very volatile, but if we’re holding the bond until maturity to have the funds be available for retirement spending, then does it matter if the bond is volatile along the way to that maturity?

No. That’s the point. Holding to maturity lets you ignore volatility.

“The Federal income tax on the recoupment of some or all of the market discount is deferred until sale or maturity.” – is this the capital gains tax?

I guess I am a little confused how a secondary market purchase would work – 912810TE8 is trading at $56.

I understand the tax on interest portion – that one is easy.

I do not understand how the tax on “increase in principle” is calculated.

An extreme example for clarify –

Purchase TIPS at $56 in 2025. Yields drop in 2026 – the value of that TIPS goes up to $70 – is $14 getting taxed in 2026?

No. There is no tax due on change in market value, until you sell. Taxes will be due on the minimal coupon payment and inflation accruals each year. I am not clear how capital gains vs interest is figured at maturity.

Principal is par value x inflation index. Market value fluctuates with changing real yields.

Just to make this fun, RMDs will be based on market value, not principal value, in a tax-deferred account.

Tnx, interesting – what about 1099-OID – TD seems to be reporting it every year, but sounds like that does not happen on secondary purchases in a taxable account? TIPS can be so confusing.

No. All TIPS in a taxable account will get a 1099-OID, but it could be just a part of the brokerage’s comprehensive tax statement.

My understanding, based on secondary sources as interpreted by someone who is not a tax professional, is that a bond (including TIPS) purchased in the secondary market at a discount from par is referred to as a market discount bond and is taxed in the following manner: “A market discount on a bond is not subject to taxation annually in the U.S., but it is taxable as ordinary interest income in the year that the bond is sold or redeemed. The bond investor can also elect to include amortized market discount annually in income for tax purposes, although this would mean paying tax on it now rather than in the future.” https://www.investopedia.com/terms/m/market-discount.asp But as I said, I am not a tax professional; people facing or expecting this problem should consult one.

That’s my understanding, too, but I have heard conflicting opinions.

Thank you, both,

So, that’s potentially good news about the “market discount on bonds not being taxable till sold”, but what about the OID? – Do any of you hold secondary TIPS in a taxable brokerage account – are they sending you annual OID for TIPS bought on the secondary market?

amChess, if you own any TIPS in a taxable account, you are going to get a 1099-OID. Secondary market makes no difference.

David,

Great picture of you and your wife at Easter Island! This article from recent WSJ may generate some interest in tips.

https://www.wsj.com/finance/investing/inflation-tips-on-how-to-buy-tips-632c8462?st=xHkFg2&reflink=desktopwebshare_permalink

Good article. Jason Zweig contacted me to talk about this topic, but alas, I was in Santiago, Chile + it was inflation day. So we didn’t connect. He did fine without me!

AMA ing to get a message from Easter Island. I’ve been to Chile a few times but on business. Been from Santiago north to Iquique. Reminded me of California.

I was impressed by Santiago. Modern + nice, looked like Charlotte in a lot of ways. Rapa Nui is an incredible destination. Almost entirely undeveloped with a fascinating culture and history.

Ah! That explains it. It is very rare to see an article on TIPS these days without your name and opinions being mentioned. And Thanks for sharing the lovely trip photo. Wishing you a relaxing vacation so we can have more of your wisdom when you get back!

I wish they would use maturities that fit into people’s lives. 30 years is too far out. It would be nice if they had a 2 year, 3 year, and 7 year TIPS along with the 5 and 10.

These are all easily purchased on the secondary market, with a few added complexities

David: I have a slightly different view, it seems to me that CUSIP 91210TE8 (with a maturity date of 2-15-52 and a 0.15% Coupon), could be a more attractive purchase than CUSIP 912810UH9 both for inflation protection and as a bet on a future decline in interest rates–which seems likely to occur once the Federal Reserve has to fight or forestall a new recession by slashing interest rates.

With respect to these objectives, a purchase of CUSIP 912810TE8 seems to me to have three advantages over a purchase of CUSIP 912810UH9.

First, even though the current market price is roughly 56% of the face amount, the holder of CUSIP 912810TE8 will be receiving CPI adjustments on the full principal amount, which is almost 80% more than the market price.

Second, because most of the real return will take the form of market discount, a buyer of CUSIP 912810TE8 gets a lot of the tax-deferral charactics of an I-Bond, i.e., the Federal income tax on the recoupment of some or all of the market discount is deferred until sale or maturity.

Third, if interest rates fall sharply again in the next few years the windfall gain (much of which may be taxable as long-term capital gain) should be a larger % of original investment than would be the case had the investor purchased CUSIP 912810UH9. In this regard, the duration of 26+ for CUSIP 912810TE8 implies that a 2% fall in real interest rates could increase the market price by 50% or more from the current 56% to something close to 90% of the accrued principal.

The main deterrent to the purchase of CUSIP 912810TE8 (as compared to the purchase of CUSIP 912810UH9 would seem to be the necessity to fund out-of-pocket most of the Federal income tax attributable to the CPI adjustments. For me, at least, this is not a deterrent. I do not spend all of my income and I keep 8 to 10% of my assets in Money Market Funds so I can easily fund the Federal taxes due on the CPI adjustments.

In my opinion, these 0.125% TIPS aren’t appropriate in a taxable account. There is near-zero cash flow until maturity, but taxes will be due each year for 28 years. That’s negative cash flow for nearly three decades. In a tax-deferred account, though, they are attractive.

Most TIPS ladder scenarios use the coupon-rate cash flow to provide spending money in early years. The cash flow provides that. If cash flow isn’t an issue, then all is good.

If I were buying a TIPS ladder out to 2055, I would happily buy these 0.125% issues and enjoy the discount.

A better alternative, at least inside an IRA, is to buy a 27 year TIPS, the 1/8% 2052 (or 2051 or 2050).

Buying at 56 gives 178% inflation protection. A good deal in the long run, but an exceptionally good deal for the next 4 years.

”Imputed” interest is reinvested at high rates as well.

These 0.125% coupon TIPS were awful investments at the time, but now are attractive, I agree. Worth noting the 2051 TIPS has a 1.21 inflation index and 2052, 1.13. So you’re buying some unprotected principal, at a nice discount.

I have been reading through your site and just turned 50 and am looking to make this my farthest TIPs to own. Could you expand for the relative novice what you mean by ‘unprotected principal’ and what the significance of the 1.21 and 1.13 would be to someone buying this in a roth ira (i dont have any TIRA); as in are u implying one is better than the other, and relative to the new auction. As of today the ask prices are 56.19 and 55.18 on the WSJ page for the 2051 and 2052 TIPS so both pretty discounted. It seems more than one person has mentioned this 2051/2052 issue in the thread (and passingly in a bogleheads thread i see) so I was interested in hearing more. Thank you!

When a TIPS matures you are guaranteed to get back at least par value, even if we have years of deflation. But when you buy a TIPS with a high inflation accrual, the extra principal is not guaranteed at maturity. This is a very minor risk, unless you are buying a TIPS very close to maturity.

Wow I never considered how a discounted principal would act as a multiplier for inflation protection! Thanks for pointing this out.

Hey David – thanks for the photo.

Meanwhile, the current Administration is showing its generalized disdain and disrespect for tradition, laws, and yes, contracts.

A debt obligation of 30 years? LOL!

At this run rate, the USG won’t last 3 years – if we get past next month’s debt ceiling, that is.

The inability / refusal to reprice US debt given the dumpster fire in D.C. is impressive, but then again denial is a specialty of ours.

https://open.substack.com/pub/paulkrugman/p/lies-damned-lies-and-trumpflation?r=5f1cm&utm_campaign=post&utm_medium=web&showWelcomeOnShare=false

This is from Paul Krugman on Substack. The link I posted will take you to the article:

Lies, Damned Lies and TrumpflationBig worries — and some investment advice

As I have noted before, this issue comes up every day. It’s a potential problem, but we must wait and watch.

Paul Krugman is so blunt. That’s why he left the Times.

I worry this fits into the old TINA (There Is No Alternative) problem. If we’re looking for inflation protection, particularly against the risk of a stock market collapse, then what are our best bets? US agencies being instructed to cook the books on what inflation is will reduce the value of TIPS and I-Bonds, but also any nongovernmental tools that also use CPI or PCE. So in the case of this scenario, what is a better solution that TIPS that also has inflation hedging power if we don’t see this adulteration of government data?

I respect P.Krugman and have learned much from his writing. But here’s the deal: TIPS purchased at positive real yields (YTMs) and held to maturity within my Roth IRAs are super easy to manage (no RMDs, taxes, or reporting hassles), and they promise that my purchasing power will keep up with (and slightly exceed) inflation. Stocks don’t promise that. Gold doesn’t promise that. Crypto doesn’t promise that. Real estate doesn’t promise that. Laying hens don’t promise that. In fact, nothing else promises that.

I go into this with realism and eyes wide open, and the understanding that no investment is 100% risk-free, and i know and accept that promises can be broken. But i sleep really well at night knowing that much of my pile is protected by the promise of maintaining the purchasing power of the money i worked so hard to accumulate.

I will pay attention and monitor the situation, and accept the small risk that the US government may someday break its promise and start to “cook the books” (i.e., lie about actual levels of inflation). If that happens to any significant degree, i’d still feel better than worrying constantly about having my whole pile in equities (or gold or crypto or real estate or nominal bonds or CDs or laying hens) and watching it evaporate overnight in a crash of one sort or another. Until proven otherwise, i am promised a good outcome by what (so far) has been a reliable borrower.