By David Enna, Tipswatch.com

The market for Treasury Inflation-Protected Securities made a bit of history today, with the auction of $9 billion in a new 30-year TIPS getting a real yield of 2.403%, the highest for this term since October 2001.

Of course, we have to recognize that the Treasury stopped issuing 30-year TIPS from October 2001 to February 2010. Since that restart, no 29- to 30-year TIPS auction has received a real yield higher than 2.29%. Until today.

This is CUSIP 912810UH9, and the auction sets its coupon rate at 2.375%, also the highest for this term in 23 years. The auction appears to have come in right on target. The “when-issued” yield prediction — revealed just before the close at 1 p.m. EST — was very close at 2.400%. The bid-to-cover ratio was a solid 2.48.

This is a good result for investors, who will earn 2.403% over official U.S. inflation for the next 30 years. Just a reminder: As recently as March 9, 2022 — less than three years ago — the nominal yield on a 30-year Treasury bond was 2.29%, less than the real yield of today’s result. This is a nice turn for investors seeking safety.

Here is the trend in the 30-year real yield over the last five years, showing the remarkable surge higher after the end of the Federal Reserve’s pandemic-era quantitative easing in March 2022:

Pricing

This is a new TIPS, so investors could be assured that the coupon rate (2.375%) would be set slightly below the real yield of 2.403%. That resulted in a discounted unadjusted price of 99.403433. In addition, this TIPS will have an inflation index of 1.00016 on the settlement date of February 28.

With this information, we can calculate the exact cost of a purchase of $10,000 par value of this TIPS at today’s auction:

- Par value: $10,000.

- Adjusted principal purchased: $10,000 x 1.00016 = $10,001.60

- Cost of investment: $10,001.60 x 0.99403433 =$9,941.93

- + accrued interest of $8.53

In summary, an investor buying $10,000 par of this TIPS at today’s auction paid $9,941.93 for $10,001.60 of principal and will now earn inflation adjustments equal to inflation for 30 years, plus an annual coupon of 2.375% paid on inflation-adjusted principal.

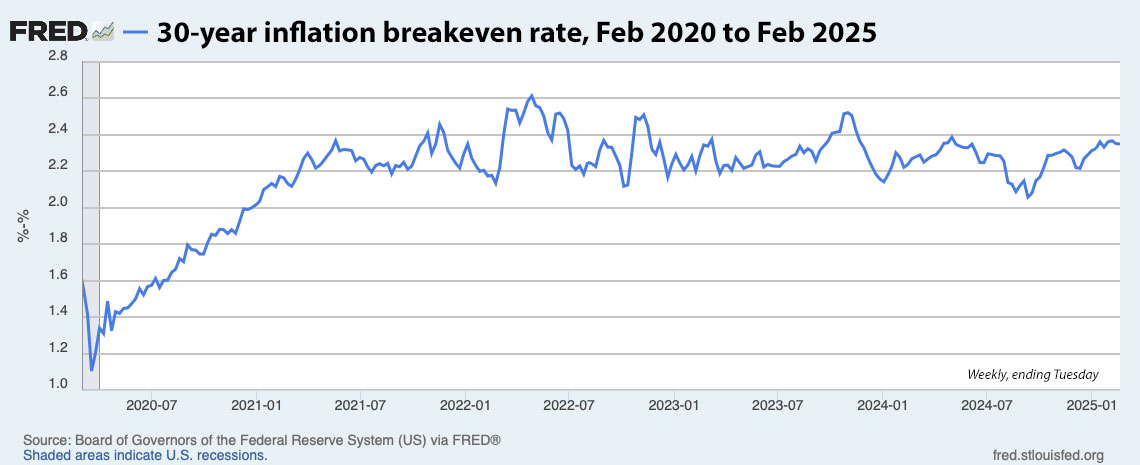

Inflation breakeven rate

At the auction’s close, the 30-year Treasury bond was trading with a nominal yield of 4.74%, meaning this TIPS gets an inflation breakeven rate of 2.34%, a bit high compared to recent trends. This reflects a lack of investor confidence in the Federal Reserve’s ability to put tight controls on future inflation. Inflation over the last 30 years, ending in January, has averaged 2.5%.

Here is the trend in the 30-year inflation breakeven rate over the last five years, showing how inflation expectations have been locked in a narrow pattern (but highish) for the last three years:

Thoughts

This is a very good result for investors who can accept the 30-year time frame and hold to maturity. CUSIP 912810UH9 is the most attractive 30-year TIPS issued in 24 years, in my opinion. But I wasn’t a buyer because the long maturity doesn’t fit into my likely lifespan.

We are heading into uncertain economic times. Both real and nominal yields could be heading higher. Still, getting 2.403% over inflation for 30 years, guaranteed, is attractive and sensible, in my opinion.

Here is a history of TIPS auctions of this term over the last five years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

For those of us that missed the auction, how can we best get in on this TIPS? The secondary market is priced quite a bit higher than the auction ($101.178, 2.329% Yield.) Or is that just the cost of missing out?

The market value and real yield of a TIPS changes constantly during daily trading. As of Friday’s close, this TIPS was trading with a real yield of 2.356%, just under the coupon rate of 2.375%, so it is selling at a small premium as you note. Yes, the auction is over and now the market sets the price and real yield.

According to FRED the real yield on the 5 year TIPS is starting to roll over just a bit. Nowhere near what we saw with last year’s auctions on the 5’s. Curious how well the April auction will go.

I will be posting a preview of that April 17 auction on Sunday, April 13. The 5-year real yield has fallen fairly dramatically since the beginning of the year, from 1.97% to 1.57% at Thursday’s close. While I was in Argentina I swear I saw it hit 1.30% several days recently, but then popped higher. This rate is important because the current trend indicates the I Bond’s fixed rate of 1.2% will be going lower at the May 1 reset.

David, any thoughts on the potential for the Trump Administration to coerce the BLS and BEA into manipulating inflation data downward? The whole reason to invest in I-bonds and TIPS is to protect against the ravaging effects of inflation on purchasing power. Couldn’t Trump put the whole investment thesis at risk?

I won’t speculate. Could it happen? I have to hope it will not happen.

I have trouble making comments so I tried 3 times. The third time it went through but the sender shows as “rainycheerfully5aafc7dae5“. I have no idea who that its. This is from Mary.

Hi David, glad to hear you are enjoying your travels! I have an off-topic question.

I purchased several TIPS at various auctions last year in my taxable brokerage account. I just finished doing my taxes in TurboTax and was checking my returns before I E-File.

On the 1099, I have a question about “Taxable accrued interest paid” which is in a section that says “The following amounts are not reported to the IRS. They are presented here for your reference when preparing your tax return”.

I looked up this topic in TurboTax, and it says I can reduce my taxable interest by this amount. I think I would make the adjustment where it gives you the option to adjust the interest. But my concern is that the accrued interest is not reported to the IRS and I would be reducing the interest reported on the 1099-INT. Could this raise a “red flag”? It would save me $153 on my taxes, but if I have to do an amended return, then it is not worth it to me. I’d rather be done with taxes until next year.

Thank you for any light you can shed on this.

This would apply to TIPS in a taxable account. I am no tax expert, but I think that the accrued interest paid should be deductible. It would only apply to the year of purchase. But I haven’t bought a taxable TIPS in many years, so I don’t know the procedure.

Mary, I’m not sure if this works the same way in all versions of TurboTax, but in the Windows desktop version, from the step-by-step area where you are entering the 1099, you would go to Forms. In the form, scroll down below Box 14 and in the Adjustments to Interest section check Box A, Accrued Interest, and put the amount in the box at the bottom right of that section (“Enter adjustment amount …”). I’ve done accrued interest this way for years on different kinds of bonds (not TIPS) and it’s never been questioned. Hope this helps.

Excellent advice

Thank you Woody and David. I use the online version of TurboTax, but I was able to revisit the 1099-INT and enter the accrued interest. It shows on Schedule B as “Interest Adjustments”. It saved me more than I thought because it also reduced my taxable Social Security!

Mary, in the desktop version you can enter the accrued interest as an adjustment at the time you enter the 1099-INT. After you enter the main information and click the next button, you get a screen that asks if you have one of several uncommon situations. Select the box that says I need to adjust the interest reported and click continue. Enter the amount and select as your reason My accrued interest is included in this 1099. There is an alert that the adjustment will be spread across all types of interest reported for that 1099. That is where it may get trickier for you depending on your particular situation. Read the note and decide for yourself because it talks about creating multiple 1099s out of your one with the different types of interest divided among them. That part may or may not be worth the trouble to you.

Hi Paul, thank you for your response. I use the online version of TurboTax and it lists the Treasury Interest separate from the taxable interest. I selected the Treasury Interest line and checked the box that said something like “I need to adjust this interest”. I put in the adjustment and regenerated and it showed up on Schedule B. It also added a little section to my return that explained the adjustment. Everything looked good, nothing unusual, so I filed the return.

Tremendous yield! I bought at age 54. If I do not make it my beautiful wife, age 51 with perfect health across the board will be able to collect. Trying to figure out last rung on the ladder. Maybe 85 for the wife. Decisions to make.

Thanks for the blog and insight.

Me (also 54), too! Don’t sell us guys short. Making it to 85 is nothing these days!

We have a full 30-year ladder, starts this year, funds essential living costs until age 70 (SSI), then drops by my stated age 70 benefit. My wife’s SSI is insurance against cuts to benefits, or, is irrelevant if I am not as successful at getting to 85 as I hope. The rest of our portfolio will fund everything fun. The plan was to retire end of last year. But, given the market’s highs, I’ve decided not to pull the cord yet… We’ll build up a bigger cushion to reduce sequence of return risks. I don’t mind over-accumulating because we want to leave something to the kids.

David – You end that “We are heading into uncertain economic times.” Do you agree that we are *always* heading into uncertain economic times? If you disagree then I would like to know your opinion as to how or why you believe *now* that we are heading into uncertain economic times but we were not a year ago, 10 years ago, 30 years ago, etc. Isn’t this the entire reason we get compensated for risks taken?

The pandemic certainly created uncertainty. So did 4-decade high inflation. So did unprecedented Fed manipulation of the bond market. And now … potentially harsh tariffs, government cutbacks to employees and services, fast-changing foreign policy. In fact, policy changes come sweeping in with surprises every day. So, yes, I’d say more uncertainty right now than in recent years. We need to see things settle down.

You mentioned compensation for risk. In theory, TIPS are one of the most risk-free investments on Earth. But now they seem to be getting a risk premium, which reflects the market unease about Treasurys.

Add to that the unprecedent level of US debt at 131% of GDP. Think of it this way. If your best friend is $736,000 in debt, makes $100,000 a year and spends $137,000 a year do you think he will be able to repay you any money you lend him in 30 years? Probably not.

Jim B, its funny that you should say all that as a hypothetical. I actually have a friend who is $736,000 in debt, makes $100,000 a year and spends $137,000 a year, but he also has a magic printing machine in his spare room that can legally print an infinite number of $100 bills whenever he wants. He asked me to lend him some money and I’ve been trying to decide what to do.

Correct me if I am wrong, but isn’t part of the increase in the risk premium for TIPS largely based upon quantitative tightening by the Federal Reserve 3 years ago? Isn’t the national debt been exponentially growing for many years now? Didn’t several major wars break out over the last few years?

I believe uncertainty is always in our face; we aren’t heading into uncertain times…. we are always in uncertain times. No one knows what the outcome of all of these wars, negotiations, tariffs, debt limits, cyber attacks, policy changes, etc.

Spending cuts always seem to be the preferred cure for deficits/debt.

Don’t forget that taxation is another option. Marginal tax rates were multiple times higher in the 50s and 60s — a time of great growth and investment.

Minnesota, I am in favor of spending cuts to reduce the deficit, as much as possible. But not in favor of spending cuts to help pay for even larger tax cuts. That’s a sham. Let’s focus on reducing the deficit.

This (link below) is what is giving me nightmares. Half of my retirement savings is in Treasuries. What if DOGE cancels some TIPS claiming “fraud”? That won’t happen, right? Looking for some reassurance.

Trump says US may have less debt than thought because of fraud | Reuters

Apu, I believe Treasurys will continue to be safe investments. But there could be a few hiccups along the way.

Jordan, I agree with your premise, but quantitative easing as the pandemic broke out created a fairly predictable windfall for TIPS investors and the later quantitative tightening created a fairly predictable downfall. Now, there are a lot of very unpredictable factors. Maybe this is “normal” but it doesn’t feel normal yet to me.

David, respectfully I disagree with your statement that the windfall and downfall of TIPS were fairly predictable. All of the major banks, Bank of America, JP Morgan, Wells, etc were wrong for many years on their interest rate direction forecasts. For many years they had forecasted for them to go up and for many years they kept going down. If the entities with the most amount of resources, knowledge, data, inside information, intimacy with the government, etc, cannot predict interest rate direction then how in the world would a single individual? I don’t buy that TIPS recent windfall/downfall were fairly predictable; only in hindsight it was obvious and I would agree that it felt obvious at the time that interest rates would go up but again it took many years for that to happen and even then there was no guarantee that it would happen in our lifetime.

I come back to the world is simply unpredictable and uncertain; always has been, currently is, and always will be. I agree that there is a lot going on right now but there was a lot going on last year, the year before that, the year before that, etc. In the last 5 years we’ve had multiple 20+% draw downs in the stock market in several single calendar years which hints that the economic future was uncertain at those times just as it is right now. We may have a 20+% draw down this year, or we may not; there is no way of knowing and having a hunch or opinion does not change the unlimited flow of data that the world analyzes everyday to make pricing decisions. All we can do is take the risk to obtain the reward. Invest we must! Diversification is key to reduce volatility and risk.

I wish I had the likely lifespan to hold to maturity, but like you David, I don’t. That’s a great real yield! Thanks for your commentary today from Argentina.