The new target-date ETF, ticker IBIL, matures in October 2035.

By David Enna, Tipswatch.com

Blackrock’s iShares division last week launched a unique ETF holding just one bond: CUSIP 91282CML2, a 10-year TIPS that matures in January 2035.

The formal name is the “iShares iBonds Oct 2035 Term TIPS ETF,” going by the ticker IBIL. The goal is simple: To track the performance of U.S. Treasury Inflation-Protected Securities maturing in 2035. Later this year IBIL will add a second TIPS, to be issued in July, and then add two more 5-year TIPS to be issued in April and October 2030.

In 2035, these TIPS will mature and iShares will begin moving proceeds to cash. After October 15, iShares will dissolve the fund and return all proceeds to investors. You can download the prospectus here.

As I have noted before, I’m not a fan of Blackrock using the term iBonds in the fund name, since this can easily cause confusion with U.S. Series I Savings Bonds, usually called I Bonds. But ignoring that fault, IBIL joins a collection of defined-maturity, single-year TIPS funds, which began maturing in October 2024 and now run through 2035 with the addition of IBIL.

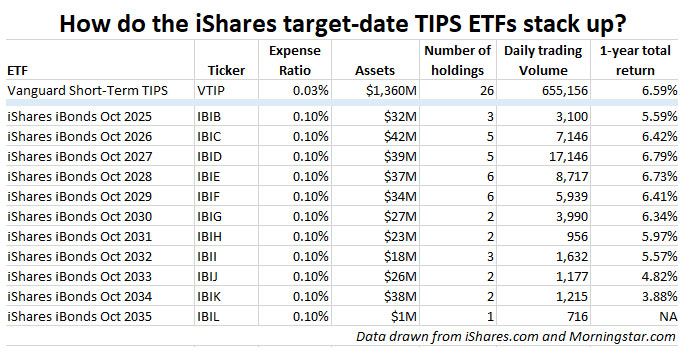

These are useful ETFs, I think, especially for an investor looking to quickly build a diversified TIPS ladder out to 2035. These funds should closely track the performance of the underlying TIPS. Here is a comparison of data for each ETF, along with Vanguard’s Short-Terms TIPS fund for comparison:

The expense ratios for the iShares ETFs are only 0.10%, higher than VTIP’s 0.03% but quite good for such small funds.

Analysis

These funds are designed to be held to maturity and the asset value will rise and fall with market trends through maturity, just like any other bond fund.

Because the expense ratio is just 0.10%, I really have no problem with using these funds as an alternative to buying individual TIPS. You could quickly build a ladder through 2035 in 15 to 30 minutes, assuming the small daily volume doesn’t create issues.

However, the limited span of maturities means these ETFs aren’t the total solution for building an inflation-protected ladder of investments to cover 20 to 30 years.

Is there a required minimum investment?

No. The minimum investment would be the cost of one share (around $25.18 for IBIL on Friday afternoon) plus any possible brokerage commission. There are no limits on redemptions. iShares notes there can be a bid/ask spread on purchases and sales. That seems especially likely for an ETF that trades at such a low volume. The iShares prospectus notes:

When the Fund’s size is small, the Fund may experience low trading

volume and wide bid/ask spreads. In addition, the Fund may face the risk of being delisted if the Fund does not meet certain conditions of the listing exchange.

Traders in individual TIPS face these same bid-ask issues and at times can have trouble buying or selling TIPS in small numbers. This new ETF resolves the small-lot issue, at least. You can buy as little as one share.

Morningstar data indicate the spreads can be fairly small, such as about 0.12% for IBIK and 0.38% for IBIJ. But that compares to 0.06% for the highly-traded VTIP.

The small daily trading volumes could also be a roadblock to a large purchase. For example, if you wanted to buy $40,000 of IBII, maturing in 2032, you would buying about 1,540 shares, very close to the daily trading volume of 1,632. You might have to spread purchases over several days.

Income and inflation accrual distributions

One of the advantages of owning a TIPS to maturity is that inflation accruals continue to build over time, increasing the amount of principal and also increasing the semi-annual coupon payment as the principal increases. An individual TIPS gets the benefit of compounding, even though the coupon is distributed twice a year.

But one of the disadvantages of a TIPS is that if held in a taxable account, those inflation accruals are subject to “phantom” federal income taxes in the current year, even though they are not paid out. Plus, if your account is at TreasuryDirect, you will face the “dreaded 1099-OID,” the cryptic form reporting your taxable accruals.

The ETF plus. These defined-maturity ETFs “fix” the OID issue because inflation accruals will be paid out in the current year, along with the coupon interest. (This is the same way traditional TIPS funds work). That distribution makes these iShares TIPS ETFs more attractive for holding in a taxable account, because it eliminates the phantom income problem.

I assume this also means your broker will provide a single 1099-DIV tax form covering both coupon payments and inflation accruals.

The ETF minus. Distributing the inflation accruals in the current year means that at maturity you will be receiving only the original par value and final coupon payment, since all the inflation accruals would have been distributed.

In essence, this means if you buy IBIL at around $25 a share this week, in 2035 you are going to get back about $25 at maturity, but you will have earned inflation accruals and coupon payments along the way.

To get the full benefits of compounding and true inflation protection you would need to reinvest all inflation-accrual distributions back into these TIPS ETFs or another similar product. That could be a problem because of the very low volume. For example, Vanguard says this on reinvestments in general: “A security’s distributions will not be reinvested if the security has a low average daily trading volume.”

I have gotten feedback from readers saying they have been able to reinvest the dividends in these low-volume funds. Beyond the cost of any bid-ask spread, that is great news. If anyone has further experience with buying these funds and/or reinvesting the dividends, please provide the information in the comments section.

Final thoughts

I won’t be investing in this new ETF, IBIL, because I have already purchased CUSIP 91282CML2 as part of my TIPS ladder, filling the 2035 rung. But I can see the appeal for investors looking for a simpler way to invest in TIPS, especially in a taxable account.

The expense ratio of 0.10% is very good, especially if you can make your trades commission-free. But I do warn against using these ETFs in an assets-under-management account, which could wipe out 1% or more of your annual earnings. And in fact, I suspect these ETFs may have been designed for AUM financial advisers who really don’t understand TIPS (a lot of them don’t).

One other issue is the fact that these funds don’t offer true inflation protection over the long term, since they pay out the inflation accruals in the current year. That is great for people seeking cash flow. But an investor seeking inflation protection would need to figure out a way to reinvest distributions.

In summary, these target-maturity TIPS are good investment for cash flow. Individual TIPS are a better investment for inflation protection over the long term.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Good information. One thing about the inflation accruals for TIPS funds and ETFs, though: They are distributed as dividends. From the Bogleheads wiki:

“Buying through a mutual fund or ETF also makes it easier for tax reporting and reinvesting interest payments. Because a mutual fund or ETF distributes both the interest income and inflation adjustment of an inflation-indexed bond as income distributions, there are some things you need to be aware of:

1 If you want full inflation protection, you need to reinvest inflation adjustment distributions back into the fund.

2 The inflation/deflation principal adjustment causes fund dividend distributions to vary considerably.

https://www.bogleheads.org/wiki/Treasury_Inflation_Protected_Security#Through_a_mutual_fund_or_ETF

hi David,

I’m with you — i’m not buying this fund because i have already built a ladder of individual TIPS that i’ll hold to maturity within Roth IRAs. But here are a couple more things potential buyers may want to consider:

The national debt has become so large that folks such as Ray Dalio say if we don’t pay it down soon, a “financial heart attack” could result in bad things happening such as “restructuring” America’s debt. That would be unprecedented and is considered a small risk to holders of U.S. debt, but it is a risk nevertheless. Investors concerned about that risk may be comforted by the payouts of this ETF, which would somewhat mitigate that risk (depending on what you do with the payouts).

Similarly, there is a small risk to holders of TIPS that the gov’t could intentionally understate the true level of inflation to reduce its payouts to bond holders. (In my mind, the level of this risk has ticked upward given the unprecedented actions of the current Administration. Again, the payouts of this ETF could somewhat mitigate this risk (again depending what you do with the payouts).

I don’t want to overstate what i believe to be small risks, but some persons concerned about those risks may want to consider these points in their due diligence calculations of the risk vs reward of these investments.

…in other words, while most commenters discuss reasons they don’t like the payout feature of this ETF, there can be potential benefits to the payouts, depending on your own personal risk beliefs and calculations.

I know that David has written about these two risks in the past, and like me believes they are small. But others may feel differently, and appreciate that the payouts structure of this ETF could potentially somewhat mitigate those risks.

Please forgive my ignorant question(s). I’m still very new to Tips, but very interested. Anyway, the first paragraph of the article says it’s an ETF with one bond. What’s the motivation to buy an ETF with just one bond (and the 10 bps)? Wouldn’t it be just as easy to buy the Tips bond itself through, say, my Fidelity account? Also, I don’t think I like the idea of having the principal payments paid out over time…I’d prefer to let that principal value build up over the years to truly fight inflation and then receive it at maturity, if I’m understanding things correctly. I see that that was mentioned in the article, but I’m still just trying to reach out and learn. My situation is this…most of our retirement funds are in an IRA (unfortunately), and I’m wanting to have a short Tips ladder for 3 years to act as a social security bridge to age 70 (the bridge to begin 5 years from now), followed by a ladder (or continuing the ladder) for the first 5 or 6 years of retirement for essential expenses. I’d really appreciate any thoughts that you all may have. I respect your knowledge and guidance. Thank you!

The ETF eventually will hold four TIPS to maturity, adding one more later this year and two more in 2030. Some people might see that as “diversification,” but it does muddy up knowing your exact real return over time. If you are comfortable investing in individual TIPS, I think that is the way to go. These ETFs are meant to simplify things for people who want some inflation-protected cash flow and don’t care to understand the complexities of the investment.

Thanks for the quick reply and easing of the mind…

It seems to me that these ETFs mess up one of my primary benefits of TIPS—knowing exactly what my real yield will be if I hold to maturity. The fact that these ETFs can buy TIPS after the date of my investment in the ETF creates the problem. Say I buy into the ETF at formation and it holds a 2035 TIPS with, as of the date of my purchase, a real yield of 2%. Now assume that the ETF later buys a 2035 TIPS at a then real yield of 1%. Those new TIPS will drag down the real yield of the ETF, thereby reducing my real yield below what I expected when I bought in. Am I missing something here?

I’d say that’s correct. Of course, it could work the other way, too, with real yields rising in the future. But people buying individual TIPS are looking for certainty against inflation — the whole point of the investment.

I don’t understand why anyone would buy such a thing. In addition to all the cons mentioned, the ER is a total water of money Owning $50,000 of IBIL with a .1% ER would cost $50 per year, a total of $500 by the time of maturity in 2035. Buying the TIPS itself is just as easy as buying an ETF, and owning the TIPS incurs zero expenses. I mean even if someone is intimidated about buying a TIPS, the ETF expenses should incentivize that person to learn how.

You sold me on buying TIPS at auction and holding to maturity. These I shares TIPS ETF funds are not very attractive in my mind. If you don’t get inflation protection over time because they pay it out, then what’s the point?? You might as well buy another fixed income ETF or individual corporate bond that will have a higher yield.

Great Point. Doesnt this mean Income tax would be easier, no phantom income?

Have you looked into the LifeX ETFs? My impression is that they serve a somewhat different market/purpose than the iShare’s products, but are similar in that they offer a simple protected income solution in ETF form, albeit for much longer time spans (23-40 years for inflation protected. They also have fixed income options for 10 years and up. The inflation protected option strikes me as a sort of TIPS-based annuity product. I’d be interested in hearing your thoughts on them.

I looked at them briefly after financial author Allan Roth wrote about them: https://www.etf.com/sections/advisor-center/allan-roth-lifexs-etf-conversion-1-click-tips-ladder … When first launched, they were limited to a single birth year, sex, could only be purchased through an advisor and had an expense ratio of 1%, too high. Not very attractive. Now they have been converted to ETFs (open to the public) and the expense ratio dropped to 0.25%. It’s all a bit too complicated for me, but these funds are a step in the right direction.

The LIAB fund, which matures in 2048, had a total return of 3.3% over the last year. LIAB has assets of $3.5 million and a daily trading volume of 100 (!). StoneRidge claims the bid-ask spread is 0.2%, but I wonder.

I’d seen that Allan Roth article, but I didn’t quite make the connection because I remembered that product had a 1% ER and it is 0.25% for these ETFs. That’s still a bit high for me, but both of these products might be available to people in their retirement plans whereas direct purchases of TIPs might not. In that case even 0.25% might seem reasonable. Much the same if they allow someone to avoid AUM fees on this portion of their investments.

In terms of understanding what you are buying, I definitely agree they are much more complex than both TIPS and the IShares target date products. I feel like they’d require some degree of blind faith, which is at odds with my desire to provide a secure income stream.

I suppose for some people there’s a tough tradeoff between what they have in retirement accounts (IRA/401k/403b) and in taxable. So the extra costs of this ETF are better than selling assets within the retirement account to buy real TIPS, and then buying those assets in the taxable to return to the asset allocation they want.

But its hard to beat free tax deferred today money with a company match, 401ks. No contest IMHO. Does anyone really do new IRAs now? Not if I were young again.

Absolutely. In my case my IRA is from a previous employers 401k, now in Fidelity. There it’s been easy to slowly convert a total market fund into TIPS under that IRA umbrella, while at the same time I buy into a total market fund with each paycheck into my 401k (plus match as you mention).