The benchmark 5-year real yield continues to fall.

By David Enna, Tipswatch.com

April 11, 2025, update: Welcome to the I Bond ‘buying season’

April 10, 2025, update: I Bond’s variable rate will rise to 2.86% on May 1

Amid all this week’s financial chaos, I am trying to focus on something I more or less understand: Projecting the May 1 fixed-rate reset for the U.S. Series I Savings Bond.

When I last looked at this topic on March 9 the real yield of a 5-year TIPS was trading at 1.57%, which was down 40 basis points from the start of this year. In the past month, the 5-year real yield has continued declining. It closed Wednesday at 1.44% according the Treasury’s daily estimate , but in the midst of tariff paranoia this morning is trading at 1.12%.

I’d expect a bounce higher, but who knows? But even ignoring this morning’s decline, it looks likely that the I Bond’s fixed rate is going to fall from the current 1.2% to 1.1% at the May 1 reset.

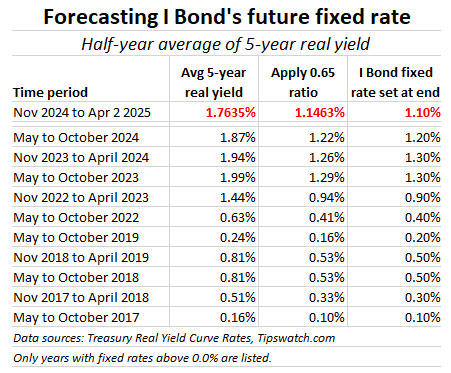

The 5-year real yield is key

The Treasury has never revealed a formula for setting the I Bond’s fixed rate, but it has stated it looks at real yield trends over time. I Bond watchers have observed that over the last decade one formula has accurately predicted the Treasury’s fixed rate decision: Apply a ratio of 0.65 to the average 5-year real yield over the preceding six months. This formula has worked without fail at least since 2017.

This morning I calculated the 5-year real yield data from the date of the last reset on November 1, 2024, to Wednesday’s close. And this week, for the first time, the data show the trend has tilted toward the 1.10% fixed rate.

Note that the I Bond’s fixed rate is always set to the one-tenth decimal point and that means the result of the 0.65 ratio calculation has to be rounded. Now that it has dropped below the 1.15% level, it rounds to 1.10%. And that level is likely to stick with the 5-year real yield plummeting this morning.

Back on March 9 I projected that the average 5-year real yield would need to remain above 1.57% through March and April for the 1.20% fixed rate to carry over to May 1. That is not happening.

Is there a strategy?

As I noted last month, the Trump administration could decide to ditch the long-standing formula for setting the I Bond’s fixed rate. Or it could be swayed by the current low yield of a 5-year TIPS and opt to go lower. Or it could decide to eliminate the savings bond program entirely. (Not likely). So we don’t know.

But from what we do know, it looks like the wisest choice for committed I Bond investors to buy their 2025 allocation late in the month of April, to capture the current 1.20% fixed rate. I ended up completing my 2025 purchases on March 28 because I had available cash and I could see the fixed rate wouldn’t be going any higher.

Are I Bonds still attractive? Absolutely. An I Bond purchased today will earn 1.2% over inflation, while a 5-year TIPS will earn 1.12%. We are back to the strange days when the I Bond has a yield advantage over a TIPS. When that happens, I Bonds are clearly the superior investment because they earn tax-deferred interest, have rock-solid deflation protection and a flexible maturity term.

Next week, on April 10, we will get the March inflation report, the final piece of data needed to set the I Bond’s new variable rate. The official seasonally-adjusted inflation number could be close to zero, but non-seasonally adjusted inflation should be higher, maybe 0.2%. That would give us a new six-month variable rate of 2.80%, up from the current 1.90%.

But that is next week’s news and I will be doing an update on the fixed-rate projection after the March inflation report is revealed.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Very nice work!

I took today’s just-released March ’25 CPI Index (319.799), divided it by the Sept. ’24 Index (315.301), subtracted 1 and multiplied by 100 to get the % increase, then multiplied by 2 to get the I-Bond Annual Inflation Rate that will begin in May:

2.85%

Close. But … The 6-month inflation rate is rounded to the hundredth decimal point, then doubled to create the variable rate. So the result will always have an even number in the hundredth decimal point. In this case, inflation ran at 1.427%, which rounds to 1.43%, and then when doubled equals 2.86%. (FYI, Barron’s makes this same mistake almost every year.)

The fixed rate for I Bonds is projected to decrease from 1.20% to 1.10% starting May 1, 2025. This change is due to declining 5-year real yields, which are a key factor in determining the fixed rate. For those considering I Bonds, purchasing before May 1 locks in the current 1.20% fixed rate.

What would happen to the composite rate if fed starts lowering interest rates down in 6 months or so? Thanks.

It’s impossible to say, since the composite rate is a combination of the fixed rate and inflation-adjusted rate. The fixed rate *could* go down after the Fed cuts rates, but the inflation rate could increase. For example the Fed cut short-term rates 100 basis points last year, but the next fixed rate appears likely to go down only 10 basis points and the variable rate should increase at the May 1 reset.

Thanks you. Much appreciated.

Thanks again! I was waiting for this April Forecast from you. With everything else going on, I did take some time to analyze whether I should buy or not. My biggest concern is that when JPow leaves, the stooges will find a way to fudge inflation numbers. The Snow globe is still shaking & murky. But I am so grateful for your website to get the info that I need.

Finally, I cashed out the 0% I-bonds in our accounts + the Trust account and purchased new I-bonds with the redeemed funds. I like the Tax deferred income with I-Bonds and the 1.2% fixed rate is nothing to sneeze at after years of meh rates. I may end up using these like 5 year tax deferred CD’s. Or, will use these up as required in the retirement years. I feel that inflation will be going up and as long as true numbers are used; Inflation bonds/TIPS are great to hold on to.

So happy that TD allowed us to redeem all the Gift Box bonds (those were at 0%). Again, Thanks to your posts I did that in Oct ’24 at the 1.3% rate. We still have more 0% I-bonds. Considering the option of redeeming it now to buy Gift I-Bonds.

Although I find this all concerning as US Treasuries, I Bonds and TIPS are my investments for the future I am intrigued that real interest rates are falling in a time of such economic uncertainty. I am guessing that this represents the “supply and demand” phenomenon in the market”s “rush to safety”. Although it may be apocalyptic to suggest will investors have an alternative to the US Treasury Market despite it being the largest and most liquid? Will the growing distaste and disillusionment with all things United States of America finally topple the US Treasury Market and the US dollar as the best choice to preserve value?

The first 18 words of your column today are good advice in any financial (or non-financial) analysis. And I believe your prediction of the fixed rate for November has a decent chance of being correct!

I hold I-bonds, TIPs, agencies, CDs. My great fear is that the CPI used to compute payouts on TIPs, on I-bonds, COLA increases on SS, and so many other things will be distorted intentionally. You will not get an accurate measure of inflation, the published numbers will be cooked to make all these expenses lower, and for political advantage, implemented by loyalists now in charge at the Bureau of Labor, and Commerce Dept. Perhaps we will never see inflation over 3% as a reported number no matter what is really happening to prices.

Yes, misreporting of data is a danger. On the other hand, a lot of outside experts carefully track inflation trends and should be able to call this out, if it happens. Any move to fudge US economic numbers would be viewed as extremely negative by global stock and bond markets.

Is there any other bond or treasury note you recommend buying now?

I personally stagger 13- and 26-week T-bills, which still have attractive rates. I try to have one maturing every 4 weeks or so. The 10-year Treasury note is still hanging above 4%, which will probably beat inflation. The 20-year TIPS is still at 2.06% real, which remains attractive for someone who can hold to maturity.

I have no idea where longer-term rates are heading, however. That is a big problem for everyone right now.

Yes, guessing where longer-term rates are heading is never easy and the current environment makes it a lot harder. Current administrration’s focus and desire to keep 10-year treasury rates low coupled with brewing recession fears is one scenario that should keep them low. How actively the administration intervenes in long-term rates manipution is yet to been seen. Japan somewhat successfully did this for a while. On the other hand, if Tariffs are here to stay, they will be inflationary and the Fed will not only stay put but may have to raise rates though only on the short end. With stagflation as the most likely scenario, IMO, 10-year will be range bound between 4 and 4.25% for the rest of this year…but then what do I know, sadly, not much….:(

Spouse and I will buy for gift box for the other the max. this month to start 1 year hold period and capture 1.2 and reset amount for last half of that year. May buy in October for other accounts with funds from final redemption of zero percent fixed ibonds. Wild year for forecasting taxes too

I will be very curious as to the final fixed rate calculation, it appears the current tariff and economy issues will bring it down further, but by how much? Today’s real yield of 1.14% on 5 year TIPS definitely makes iBonds more attractive than TIPS. I will make a decision how much to invest at the TIPS auction in 2 weeks, but I’m not thrilled with the falling real yield. I also may consider iBond gift box purchases to get the current 1.2% fixed iBond rate, but would wait until October if it was likely to be 1.1% and not fall more.

Waiting until October is an option, of course. I will predict with “absolute confidence” that the Nov 1 fixed-rate reset will fall between 0.0% and 4.0%. That is how uncertain things are in 2025.

Thanks, David, for the timely article. I did not expect the 5-year TIPS to plunge this much in just two months. In hindsight I’m very pleased I bought additional 1.3% fixed rate I Bonds through the gift box last fall.

If the fixed rate somehow rises above 2% by the end of this year, it would imply a massive selloff in the bond market. Seems unlikely, but at this point who knows what will happen. I just hope that I Bonds and TIPS will continue to accrue accurate inflation adjustments even if tariffs and trade wars cause a more sustained rise in inflation in the coming years.

Good stuff as always, and thanks for posting today, as one of my first thoughts this morning was “where to deploy some portion of my Treasury stockpile, now that things are beginning to hit, like I’ve been expecting”.

As always, well thought out and timely…thanks!!!…..minor typo just before the table…I think you meant tilted not titled

As always, thank you reader/editor! This is fixed.

Just as an fyi for all, at today’s auction, I got 4.327% for my 8-week T-Bill auction buy, while the 4-week went for 4.313%. I am happy to have, lately, tilted towards the 8-week maturity. Every bread crumb counts towards building a bread….:)))

As I noted last month, the Trump administration could decide to ditch the long-standing formula for setting the I Bond’s fixed rate. Or it could be swayed by the current low yield of a 5-year TIPS and opt to go lower. Or it could decide to eliminate the savings bond program entirely. (Not likely). So we don’t know.

Or they have no idea what an I Bond is or what they are doing.

I agree the I-Bond Fixed rate is likely not even on their radar and given the job cuts not likely they have bandwidth to change anything from what they have done in the past. My tracking of this has suggested 1.1% has been likely for quite a while when it is announced at the end of this month.

Good call, Trump has been quite busy since getting into the office, but hopefully he does not even know what an I-bond is and therefore won’t mess with it.