You can find better real yields by stretching out the maturity date, just a bit.

By David Enna, Tipswatch.com

Important note, April 16: Treasury posted an amended announcement for this Thursday auction, moving up the closing times (probably because of the holiday week):

If you are planning on participating, note the earlier times. If you are buying through a brokerage, I’d recommend placing the purchase order Wednesday evening.

————————————————-

The U.S. Treasury market experienced a disturbing rout last week, with both nominal and real yields soaring on longer-term issues.

And, in fact, the rout hit Treasury Inflation-Protected Securities harder than it did nominal notes and bonds, as noted in a Bloomberg article over the weekend:

Inflation-linked bonds (TIPS) have been the biggest losers in the recent Treasury market selloff, with yields rising more than those on regular Treasury bonds. … The TIPS market is smaller and more prone to dislocation from fundamentals, and a mismatch between supply and demand has exacerbated the current episode.

The article ended with a lovely quote from Michael Pond, head of global inflation market strategy at Barclays Capital: “The TIPS market has a tendency to break.”

Also read: The Treasury market seems to be crumbling. Why?

While that sounds a bit scary, the rout has actually opened nice investment opportunities for buyers of medium- to long-term TIPS. Yields have increased about 40 basis points for 7- to 30- year TIPS since April 1, and those maturities now have real yields solidly above 2%.

Here’s a look at the TIPS yield spectrum over the last two years:

Note that the yield spectrum was tightly bunched over much of the last two years, but has widened dramatically in 2025. Although 5-year real yields have been rising, they remain well below the yields of 10- and 30-year TIPS. The 5-year real yield closed Friday at 1.82%, versus the 10-year at 2.28% and 30-year at 2.68%.

But keep this in mind: In chaotic April 3 trading after “Liberation Day” the 5-year TIPS real yield dropped as low as 1.12% midday, and closed that day at 1.25%. It has since increased 57 basis points. So when (or if) things settle down, where will it be?

Monday evening update: The Treasury’s estimate of the 5-year real yield dropped to 1.67% as of Monday’s close. That is down 16 basis points from Friday’s close.

5-year TIPS auction

That’s the current situation as of Friday’s close. But you can expect more volatility this week, leading up to Thursday’s offering of $25 billion in a new 5-year TIPS, CUSIP 91282CNB3. This will be the largest 5-year TIPS offering in history, up from $23 billion last April. The coupon rate and real yield to maturity will be set by the auction results.

Definition: The “real yield” of a TIPS is its yield above or below official future U.S. inflation, over the term of the TIPS. So a real yield of 1.82% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.82% for 5 years.

You can get an idea of the potential auction yield by 1) looking at the Treasury’s Yields Curve page, which updates at the close of each market day, or 2) looking at Bloomberg’s U.S. Yields page, which updates in real time for secondary market trading of the most recent TIPS for each term.

Saturday, Treasury was estimating a real yield of 1.82% (as of Monday, this dropped to 1.67%) and Bloomberg showed a trading yield of 1.73% (dropped to 1.59% Monday). That’s a pretty big spread. But there is a reason: Bloomberg is showing the real yield of the TIPS issued in October 2024. The October issues always have a lower real yield than the April issues. I tried to explain the reasons here.

So most likely the Treasury estimate is going to be a better indicator. Don’t trust what you see on your trading platform. Vanguard on Saturday was showing an “indicative yield” of 1.728% for an auction order, which clearly is based on the October issue’s trading. The real yield should be higher. But a lot could change in the days leading up to Thursday’s auction.

If this TIPS auctions with a real yield around 1.82%, that result would be in the mid-range of 4- to 5-year auctions over the last two years. However, I have to admit I have no idea where real yields will be heading this week.

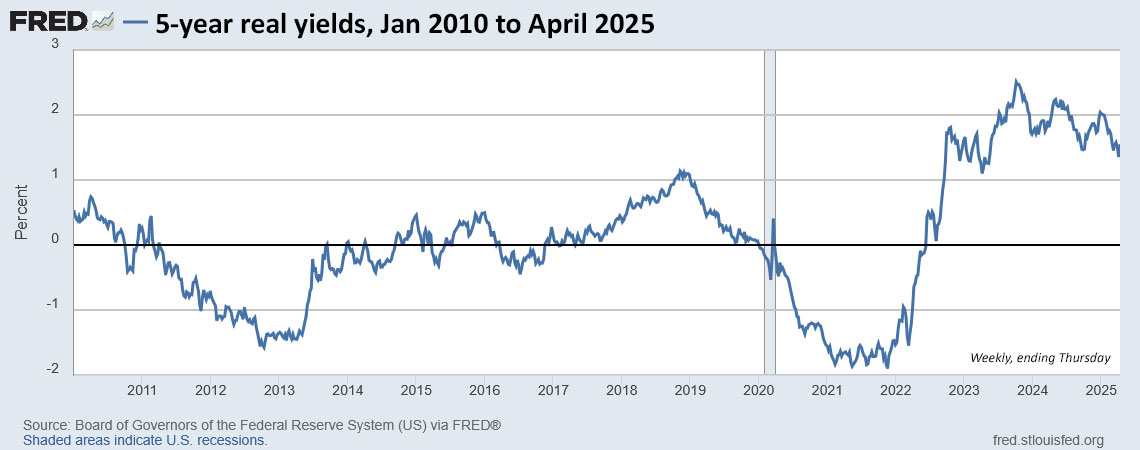

Here is the trend in the 5-year real yield over the last 15 years:

The chart shows how real yields have fallen off from recent highs, but still remain attractive versus the long-term trend. The 5-year real yield tends to be sensitive to potential interest rate cuts by the Federal Reserve, which could explain why the yields have been a bit suppressed versus the overall TIPS market.

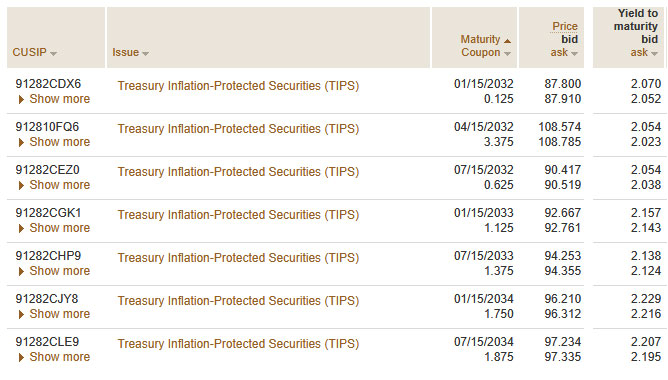

By extending the TIPS maturity out a bit, an investor can find real yields topping 2%. Here are some weekend examples from Vanguard’s trading platform for TIPS maturing from 2032 to 2034:

One advantage of buying on the secondary market is that you can see exactly the real yield and price you will pay at that moment, avoiding the potential volatility leading up to Thursday’s auction.

Inflation breakeven rate

With the 5-year Treasury note closing Friday with a nominal yield of 4.15%, this TIPS currently would have an inflation breakeven rate of 2.33%, close to the result of recent auctions. This means it would outperform the 5-year nominal Treasury if inflation averages more than 2.33% over the next five years. Seems fair. Inflation over the last 5 years, ending in March, has averaged 4.4%.

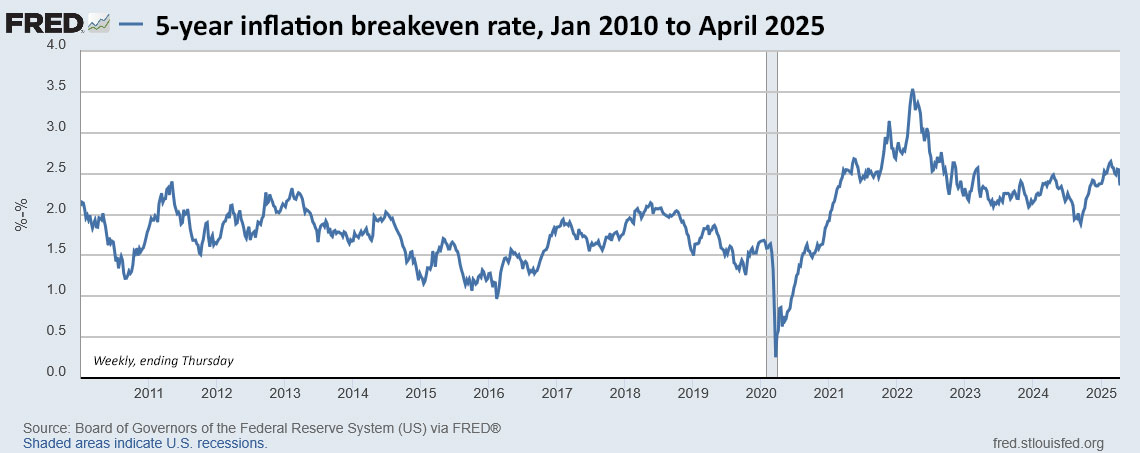

Here is the trend in the 5-year inflation breakeven rate over the last 15 years, showing a fairly stable trend in the 2.0% to 2.5% range in recent years:

Pricing

This is a new TIPS, so the investment price should end up being close to par value. The inflation index on the settlement date of April 30 will be a minimal 1.00222, meaning investors should pay slightly less than par value, based on a coupon rate set slightly below the auctioned real yield.

The alternatives

A 5-year Treasury note yielding a nominal rate of 4.15% is pretty appealing. But given the uncertainties surrounding inflation, I’d prefer a 5-year TIPS with a real yield around 1.82%.

Best-in-nation 5-year bank CDs are currently yielding about 4.5%, also appealing. That stretches the inflation breakeven rate out to about 2.7%. These are worth considering if you are looking for a guaranteed nominal return over five years.

The Series I Savings Bond currently has a fixed rate of 1.2%, well below the 5-year real yield. If you are looking for a cash-equivalent, tax-deferred investment with rock-solid deflation protection, you should invest in the I Bond. TIPS work better for defined inflation-protected cash flow in future years, in a bond ladder.

Final thoughts

I like the 5-year TIPS because … the term is only 5 years. If you are likely to live that long and can hold to maturity, this is a very safe investment that will outperform inflation. If the real yield ends up around 1.80%, that is fine. But you can do a little better by stretching out the maturity, using the secondary market. So it just depends on your needs.

I won’t be a buyer because I have filled the 2030 rung of my TIPS ladder. Right now I am focusing on the new 10-year TIPS to be issued in January 2026, which seems like a lifetime away.

CUSIP 91282CNB3 will be reopened at auction on June 17 and another new 5-year TIPS will be issued in October.

This TIPS auction closes Thursday at 11:30 a.m. ET, which is earlier than normal because of the holiday week. Non-competitive bids at TreasuryDirect must be placed by 11 a.m. Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers will cut off auction orders well before the 11:30 a.m. final deadline.

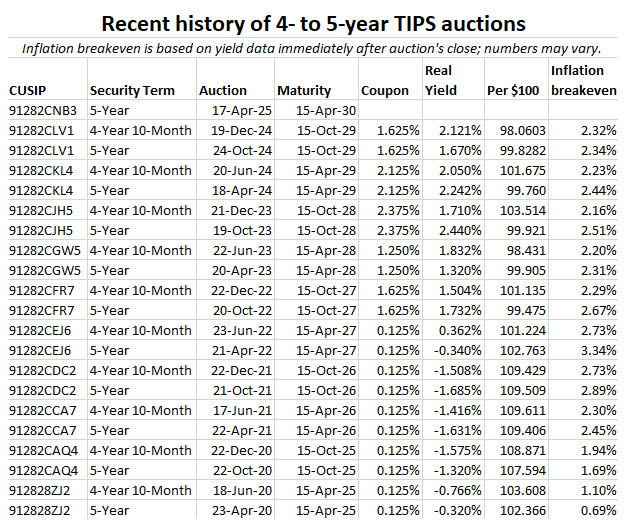

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Inflation Hedging Strategies Every Investor Should Know - Top Wealth Guide - TWG

Hello David,

I decided to try this auction, my first ever TIPS purchase (thanks in large part to your posts here that helped me understand how they work). However, after putting in my order on TreasuryDirect, I saw a comment on another post where you said you don’t recommend buying TIPS on TreasuryDirect. What is the reason for that? Is there a problem I need to watch out for, or should I perhaps even cancel (if possible)? I intend to hold it to maturity. Thanks.

In general, it is better to buy TIPS in a tax-deferred account or at least at a brokerage. If you are holding to maturity for certain, TreasuryDirect is fine. The problem is that you can’t sell a TIPS at TreasuryDirect; you have to transfer it to a brokerage to sell it and that is a tedious process.

OK. I think it should be OK then. I’m not interested in selling before maturity, and barring some complete disaster, it is hard to imagine a circumstance where I would need to.

Thanks again for the great website. I think I first found it years ago when I was getting started with I bonds. I have been intrigued by the idea of TIPS, but didn’t get around to trying to figure them out until relatively recently. They seemed much more complicated, and the potential benefits over I bonds seemed uncertain. Now that I think I have a basic understanding of how they work, I wanted to buy a TIPS or two and see how I like them compared to I bonds.

hey David, first time/long time, love the site keep doing what you’re doing.

had a question, in this post and others you often refer to having “filled the 2036 rung on the ladder etc.” It sounds like you worked hard for years and saved diligently building up a substantial next egg then started using a TIPS ladder to take care of retirement spending needs.

My first question is 1) at what age/amount of savings does it make sense to start doing this? EG what age did you start?

and 2) a big part of your retirement plan seems to be banking on tips working out as an investment. Do you ever wonder what would happen if the USA hit a hyper inflationary (or very significant inflationary) period and did something like a debt restructuring to retire tips early at a fraction of their value or just fixed their interest rate since they would be contributing to a potentially unsustainable debt load? Said another way what if the USA defaults on its debt and gets rid of the inflation protection in tips? As you’ve noted, we’ve seen significant geopolitical shifts and actions by the IS and others that this isn’t as unfathomable as it may have seemed just a few years ago. Do you worry about this possibility? Would this blow your plans to pieces?

thank you

On question 1) I started investing in TIPS in 1998 and I Bonds in 2001 but that wasn’t really a focus. There were some outstanding yields in those early years. I didn’t get serious about building a long-term ladder until real yields rose out the negative depths of the post-Covid era. A TIPS ladder can be built to last 30 years, so it seems to be ideal as a strategy for someone in the age range of 50 to 60. For example, it could be used as a bridge to delay taking Social Security, or in my case, to fund future RMD withdrawals.

On question 2) If the United States defaults on its Treasury debt then all US Dollar investments (stocks, Treasurys, corporate bonds) would get slammed and probably never recover to the glory days of the last four decades. I don’t think that will happen. The debt needs to get addressed, through sizable (but sensible) spending cuts and some possibly painful tax increases, in my opinion. In the meantime, it’s possible Medicare will get transformed into something private and Social Security will be means-tested or benefits simply slashed. Who knows?

The auction closing time has been changed to 11 a.m. ET for noncompetitive bids and 11:30 a.m. ET for competitive bids: Treasury amended announcement

THANK YOU for noticing that and alerting me. I will post a note at the top of the article.

Hello David, I have a question regarding the accrued inflation above the par value that an investor may pay when purchasing TIPS on the secondary market. Does the investor deduct that portion on his/her taxes the way you do with earned interest or do you receive that extra amount at the maturity date or is it dealt with a different way? I just attempted my first secondary market TIPS purchase via Schwab and the Inflation-Adjusted Price isn’t even shown on the main screen of pricing data for the CUSIP. I was told you had to drill down into the hyperlinks to locate that price. Thanks for your insights!

The accrued principal you purchase on the secondary market becomes part of your cost basis for the investment. When you get to the order screen you should see a “cost of investment” listed which will be what you will pay after calculating par value, inflation index and any discount/premium in price.

On Schwab when I click on the CUSIP description on a TIPS bond a popup window opens in a new browser window with all the info including the inflation adjustment.

” If you are likely to live that long….”

Gotta love a realist David I have noticed in the last 12 months the Treasury has been making larger auctions of bills and smaller ones of longer maturities So this huge TIPS auction is a bit of a shocker. Anyone make any sense of it? Beyond me

No. Treasury has been stepping up 5- and 10-year TIPS auctions for several years. But this year it left the 30-year as is.

This one is $25B. The previous one was $24B. The one before was $23B. Mostly each one is $1B higher than the previous one, with a few exceptions where it stayed the same, going back to 2020, from what I checked. So, not a shocker. I really hate phrases like “record-setting” or “largest in history” when it is merely an incremental increase over the previous highest. Most often when applied to things like box office takes or Dow levels or such when it is really just the natural result of inflation, and not any actual notable change in trends. The financial media is especially guilty when recording 500 point drops in the Dow!!!! OMG!!! That amount used to be significant, but now it’s barely more than 1%, which rounds down to almost zero in this current whipsaw market.

Tex, I said it is “the largest 5-year TIPS offering in history” and it is the largest 5-year TIPS offering in history. It’s a fact. Not an exaggeration.

Fair point. I guess I was reading it in the context where one of your readers interpreted it as shocking, when it isn’t. The phrase reminded me of some of the breathless hype on CNBC, but it isn’t in this context. Apologies.

ReaderInCA,

Yes, IMO a 1.2% assumed future inflation rate seems low in light of the Fed attempting to keep it at 2%. I would guess PlanVision is using the recent pre-Covid 10 year inflation rate to guess the future; I think the market has a better understanding of the expected rate as seen in the Treasury’s Par Real Yield Curve Rates https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_real_yield_curve&field_tdr_date_value_month=202504.

As for your second question, yes you get back the bond’s par times the inflation-adjustment based on percentage difference between the reference CPI on the date you bought the TIPS and the reference CPI when you sell / bond matures. In addition, the coupon is also inflation-adjusted.

I like TIPS and Savings I Bonds for the fixed income portion of my portfolio. It takes inflation out of the equation and preserves buying power, even in deflationary environments (you will always receive the bond’s par value no matter how low deflation goes).

The one thing they don’t prevent is a US default; but, like David mentioned, the likelihood is extremely low. I would be more concerned about having enough beans and bullets in that scenario.

I hope that helps.

Thank you very much, Rick. Very helpful!

the problem with buying tips on secondary market, on a brokerage like Fidelity, is the offerings often have high minimums, like 100k.

That can be a problem, especially for newly-issued TIPS. Also, don’t even bother trying to see order information over the weekend, the limits are usually set very high and prices might change by Monday morning anyway.

Same at ETrade. But Schwab almost always has a nice selection with the minimum $1000 usually available.

I haven’t seen that in any of my Fidelity accounts. I can by TIPS in increments of $1,000 including this new issue.

I have seen a $100,000 minimum for high yield money market which is only around 15 bp’s higher than the default money market.

I just bought a bunch of TIPS on Fidelity within my newly rolled-over 401k for much less than 100k each.

Thanks David E for the education on TIPS and the heads up on current deals. Real yields had dipped a fraction below 2.0% when I got to them, but got some decent principle value in there too.

The Fidelity interface, at least, will show you a price with a minimum number (like 200) in the table, but if you click through, you usually find a range of prices for smaller amounts. IIRC they often have a price for 200, 150, 5, and 1 as a minimum (in thousands). The prices get slightly worse as your minimum shrinks.

Pretty much the same on Schwab.com. Click on the name of the particular issue you want in thesearchresults, and in the box that pops up, choose the “market depth” tab. Offers to sell are listed on the right in descending YTM order, so pick the first one you see with a minimum number of bonds at or below the number you want to buy.

Saturday’s Wall Street Journal had an article about this month’s “crazy” equities market. Their advice was: one should be introspective and consider investing in TIPS if they are investing for retirement.

I use Plan Vision too and asked them about this last week. Basically if your plan shows success in the Reports and your rate of return in retirement is 1.8 percent or more than inflation then it doesn’t matter what inflation gets to your plan will continue to be successful. If in pre-retirement the rate of return over inflation would need to be 3.8%.

For their Reports purposes, it doesn’t matter what the actual rate of return or inflation is as long as your rate of return is 1.8 (or 3.8) over inflation.

This is great information, JKGraham. Thanks for sharing. That would mean that the 4% interest rate projected for my entire fixed-income portfolio (all Treasuries) would be woefully inadequate for 20 years if interest rates were higher than 2.2%. Yikes. I’m starting to see why TIPS could be a better choice.

It looks like $25 billion to be auctioned. I’m curious to know if this is significantly more than the previous 5 year TIPS but can’t seem to navigate TreasuryDirect to get that info. Do you happen to know how much went out on the last 5 year? Or, better yet, point out how to find out for myself?

The last 5 year TIPS reopening in December auctioned for $22 billion. You can find all the details of past and upcoming auctions here: https://treasurydirect.gov/auctions/announcements-data-results/announcement-results-press-releases/

Thanks.

My brokerage lists this TIPS as an expected yield of 1.638 which hasn’t budged since it first listed it last week. Seems sketchy in terms of accuracy and updates. Where is the best place to get an accurate picture of what is going on in the auction? I poked around but couldn’t really find anything.

The latest 5-year TIPS, issued in October, is trading this morning with a real yield of 1.60%, so real yields have opened lower this week after last week’s turmoil. The 10-year has dropped to 2.14%.

Try home.treasury.gov. Go to Data, look for Daily Treasury Par Real Yield Curve Rates. See link.

https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_real_yield_curve&field_tdr_date_value=2025

For real time yield changes I use Bloomberg:

https://www.bloomberg.com/markets/rates-bonds/government-bonds/us

There are different sites you can use instead of these.

Thanks, it’s a jungle out there. Fidelity refuses to budge from 1.638, Bloomberg says 1.55, CNBC quotes the October 5-year not this auction, …. sigh.

Thank you so much Dave for that excellent commentary! I have two empty years in both my nominal bond ladder and my TIPS ladder and those are 2030 and 2032. It makes sense to pick up some 2032 maturing TIPS now, while real yields are so attractive. But it still leaves me with a hole in my 2030 ladder which I was hoping to fill this week. Do you think it might be wiser to wait for the 4 Year 10 month follow up in June, or perhaps try the October auction, rather than purchase this week?

I am not a financial adviser, and as I have noted, I have no idea where real yields are heading. This is a hard market to judge. If the Fed does begin to cut short-term interest rates, you could see the 5-year real yield fall. I just took a glance at the TIPS I have maturing in 2030 and they had real yields at purchase of 1.59%, 1.43%, and 2.01% …just for comparison.

Great article! Can I get a link/bookmark to that Fred chart showing 5, 10, and 30-year real yields? I made this one, which seems to work but not quite as nice as the smooth lines above:

https://fred.stlouisfed.org/graph/?g=1I66w

Here it is: https://fred.stlouisfed.org/graph/?graph_id=910716&rn=664

That is the basic version; I alter it a bit every time I use it.

I read those Allan Roth articles, thanks to ReadInCA. I have 67% of my fixed income in TIPS. Yikes, Roth suggests no more than 25%. But he is discussing a 30 year ladder. Mine is just 8 years out and I’m 77 now.

Roth mentions these low probability factors that would negatively affect TIPS: (1) volatility of long dated TIPS, (2) government changes in the CPI, and (3) hyperinflation and the tax implications. I think having a shorter length ladder helps somewhat.

Does my 67% in IRA’s and Roths sound like too much? With the radical government policies shifts we have seen recently, is major CPI fiddling a worry?

For what it’s worth, we are 67% in TIPS for our fixed income in tax-advantaged, as a 10-year ladder, all to be held to maturity. We are also retired, and so inflation protection is important. Our logic in 2/3 TIPS is the asymmetry of the inflation risk. If inflation is lower than “expected”, where nominals would have been a better bet, the loss by TIPS-heavy is small as compared to the other side of the coin, where very high inflation over what is “expected” could produce devastating effects.

I am a retiree that invests in TIPS and I Bonds via Treasury Direct. I make my withdrawals at maturity since you can’t sell directly on Treasury Direct. Treasury Direct also does not price TIPS to market which removes some anxiety. One downside comes at tax time. The inflation adjustment is taxable each year similar to interest you are accruing in a CD but cost basis is rather difficult to figure out but I am hoping that will no longer be an issue with the 2025 tax year with the cost basis of TIPS finally all being reported on the 1099 but last yea, at least, all my 5 year TIPS were.

David,

Thanks as ever for your fabulous post.

Can you comment on the current discussions about whether the yield spike (price drop) is due to market dislocations related to swaps and futures and such, vs. a sudden global fear that the US Treasury may no longer be a risk-free investment? Do you think this is the beginning of the end of the empire, or just a normal periodic market hiccup?

Of course let me know if you’ve posted on this question recently.

Thanks!

My analysis is: “There is a problem here.”

See this: https://tipswatch.com/2025/04/05/howard-marks-the-world-economy-has-been-shaken-like-a-snow-globe/

And this: https://tipswatch.com/2025/04/09/the-treasury-market-is-crumbling-why/

Thank you for replying to my earlier post (copied below for reference). I had seen the posts you linked in your reply. I agree completely and I understand that the answer is “nobody knows.” I also understand the various possible explanations in the second linked post in your reply (though I note the conspicuous absence of the Mar a Lago Accord explanation). But I still am hoping to get a sense of your gut feeling on the fundamental question of whether the US Treasury is meaningfully more likely to default on TIPS today than it was before.

So here is my follow-up question. What probability would you assign to the chance of TIPS purchased today not being paid back as promised by the Treasury? I’m asking for your personal best guess.

Because with last week’s TIPS sell-off, it’s clear that the expected value of the TIPS transaction has changed. Treasury default now seems possible, and above I’ve asked for your personal estimate of the probability that it will happen. But that’s obviously a tail risk. The bigger risk (call it the belly risk, for the belly of the bell curve, rather than the tail) is profound and long-lasting devaluation of the dollar coupled with inflation or stagflation. The probability of this seems very high to me, like 60%. Do you agree?

After all, the devaluation is the explicit intent of the Mar a Lago Accord, which is a pretty compelling explanation for what he’s doing, and inflation is a foreseeable consequence. If this comes to pass, then TIPS remain a good choice for US residents. Today’s TIPS buyers will do okay because even though they will face the pain of inflation, they will also benefit from the security of wealth preservation thanks to the TIPS holdings. The other pain they’ll face is difficulty affording foreign travel due to dollar weakness.

In summary, if the risk of Treasury default has become non-negligible, we really should not be buying TIPS, and instead need to buy gold and ex-US investments that aren’t dollar-denominated. But if we can count on the Treasury fulfilling its promises, then we can continue to buy TIPS, so long as we don’t mind giving up overseas vacations…

.

.

David,

Thanks as ever for your fabulous post.

Can you comment on the current discussions about whether the yield spike (price drop) is due to market dislocations related to swaps and futures and such, vs. a sudden global fear that the US Treasury may no longer be a risk-free investment? Do you think this is the beginning of the end of the empire, or just a normal periodic market hiccup?

Of course let me know if you’ve posted on this question recently.

Thanks!

My personal opinion, for what that is worth, is that the chance of default on TIPS is near zero. But other shenanigans, such as doctoring future inflation numbers, is greater than zero.

Just one perspective which I found interesting, “The Downfall of King Dollar,” from the British magazine New Statesman. The author is a Portuguese (but partly Harvard-educated) economist and writer.

https://www.newstatesman.com/business/economics/2025/04/the-downfall-of-king-dollar

I’ve been reading your column for years, was very invested in I-Bonds and now Treasuries, and I am just now starting to learn about TIPS at age 70 and newly retired. My financial advisor says my portfolio will last 20 years if I’m able to maintain a 4% interest rate across the board on taxable and tax-deferred funds. Bogleheads recommended that I purchase TIPS, not Treasuries, because of the importance of inflation protection. I know this is a newbie question, but if I purchase TIPS, will I still be able to receive the 4% interest rate that I need for my portfolio? And if so, would a good place to start be to purchase this 5-year TIPS on the secondary market? I’d be purchasing in my SEP and/or Roth. Thank you!

TIPS seem way too complicated … and in fact they are complicated. For regular investors (not foreign banks or hedge funds), the most common strategy is to create a ladder of TIPS with a certain amount for each year through your life expectancy. So if you are 60 years old, you could create a 30-year ladder lasting until age 90. With the high real yields we have today, you can build a ladder with a guaranteed, inflation-adjusted withdrawal rate of about 4.7%. See tipsladder.com for more information.

Financial author and adviser Allan Roth has great advice on this topic:

https://www.advisorperspectives.com/articles/2024/10/07/four-easy-steps-build-tips-ladder

https://www.etf.com/sections/advisor-center/allan-roth-i-love-tips-just-dont-go-all

No matter how you choose to do it, the key is to plan to hold to maturity and ignore market fluctuations along the way. Buying in a tax-deferred account is a good move. But understand that I am not a financial adviser.

Thank you very much for the info and the links!

The Allan Roth article is interesting, thank you. I have been thinking more 50% TIPS / 50% Nominal. Do you know if he (or others) had said more along these lines? I suppose another way to look at this might be something like 25% individual TIPS with the plan to hold to maturity, 25% individual nominal with the same plan, and 50% bond funds (with their own volatility and benefits).

Allan Roth did a financial plan for me and my wife in 2019. At the time he was a strong advocate of short- or intermediate-term indexed bond funds, which are nominal bonds. My wife has those funds in her IRA, and I have TIPS in mine, so it does balance out. I like buying individual nominal Treasurys and CDs up to 5 years. Beyond that, I want inflation protection.

fabulous question! I’m sure the author will respond much more thoroughly than I ever could. But my wayman’s way of understanding and we explaining it is that you have the interest rate which in this example for the five year will assume is 1.8%. then, the other half of your income comes from the value of your tip rising with the inflation numbers that come out. So it’s not given to you in interest it’s given to you in a rise and value. (Unfortunately you’re also taxed on that rise in value as if it was income.).

But now that you’ve asked that question I do wonder how retirees navigate withdrawals. I’m guessing that there has to be some principle withdrawal? I myself have a 10-year bond ladder which is made up of about 60% tips and the other 40% bullet shares investment grade defined term etfs, and mygas, as well as some zero coupon and nominal treasuries. It’s a mess, but it works for me!

there is an ETF product offered by a company named LifeX that offers a term trust of tips, and these trusts mature and various years. They appear to mimic annuities, and you can choose whether or not you want inflation protection. Something too investigate if you’re curious.

You might ask your advisor what inflation rate that nominal 4% rate assumes. If that’s assuming 2% inflation and actual inflation turns out to be more like 5% then your 4% return may be insufficient, unless you reduce your spending accordingly. TIPS offer some insurance against that. If inflation averages 5%, this TIPS would return something like 6.8%.

Thank you for the feedback. My advisor is with PlanVision and they use eMoney. From the FAQ:

PlanVision Growth RatesWe set the default growth rates to 5% while working and 3% in retirement for securities. We set cash at 2.5%. Inflation is set at 1.2% for future expenses. We set Real Estate growth at 1%.

So it looks like they’re setting inflation at 1.2%. That seems ridiculously low to me. How about you? The 4% rate is the interest rate of the treasuries I’ve purchased. – So to me it seems like TIPS is like a I-Bond in that you have a low quoted yield, but upon maturity, you get the principal back and also the rate of inflation plus the quoted yield? Is that correct?

ReaderinCA, I don’t know why they would assume that low of inflation, but I suppose inflation affects retired people differently from younger people who are acquiring things more. Also, the growth rates may be somewhat conservative.

Yes, my understanding is the principle adjusts based on inflation and the return is on that adjusted principle. So, a little different mechanism than iBonds, but a similar result.