By David Enna, Tipswatch.com

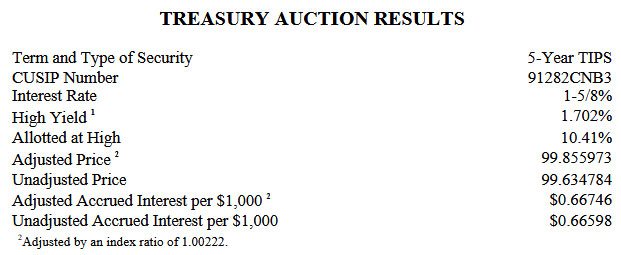

The Treasury’s auction of a new 5-year TIPS, CUSIP 91282CNB3, was a hard one to predict. Real yields have been sliding all over the place in the last week.

You might have seen real yield predictions as low as 1.53%, where the most recent 5-year TIPS was trading this morning. Or as high as 1.62%, the Treasury’s estimate at market close Wednesday. I expected a yield a bit higher than that.

The end result was a real yield of 1.702%, which I would consider a nice result for investors. The “when-issued” yield prediction, revealed just before the auction’s close, was 1.68%. The bid-to-cover ratio was a low-to-middling 2.28. All of this indicates weak investor demand for this auction.

In my preview article, I noted that the Treasury’s 5-year real yield estimate closed at 1.82% on Friday. But I expected volatility this week. And so it goes.

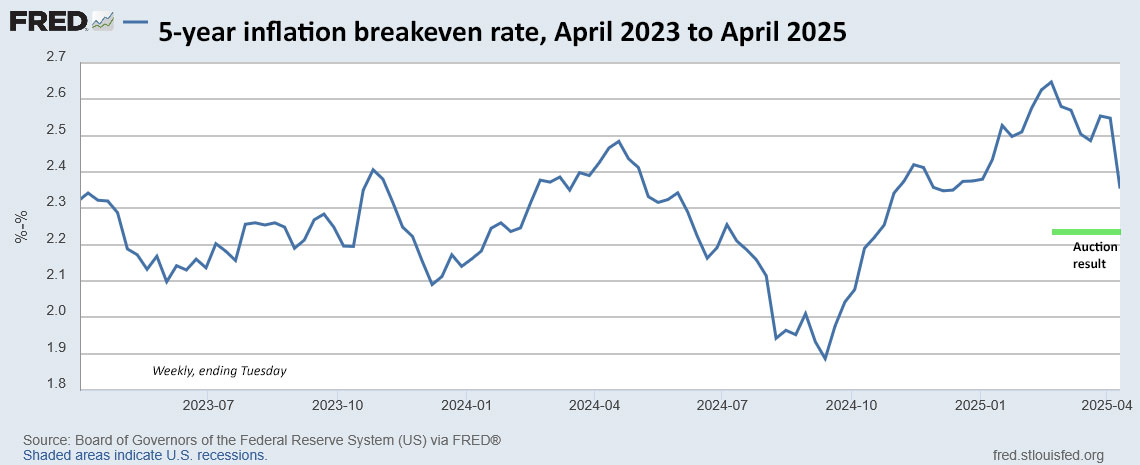

Here is the trend in the 5-year real yield over the last two years. The chart closes with the yield estimate on Tuesday. Note the higher auction result:

Pricing

The auction set the coupon rate for CUSIP 91282CNB3 at 1.625%, same as the October auction of a new 5-year TIPS, issued just days before the November presidential election. That auction got a real yield of 1.670%, lower than today’s result.

Because the coupon rate for this new TIPS was below the real yield of 1.702%, buyers got it at a discounted price of 99.634784. In addition, it will carry an inflation index of 1.00222 on the settlement date of April 30. With that information, we can calculate the exact cost of $10,000 par value at this auction:

- Par value: $10,000

- Principal purchased as of April 30: $10, 022.20

- Cost of investment: $10, 022.20 x 0.99634784 = $9,985.60

- + accrued interest of $6.67

In summary, an investor buying $10,000 par value at this auction paid $9,985.60 and will receive $10,022.20 in principal on the settlement date of April 30.

Inflation breakeven rate

With the 5-year Treasury note trading with a nominal yield of 3.93% at the auction’s close, this TIPS gets a 5-year inflation breakeven rate of 2.23%, a rather low number given our uncertain inflation future. This partly reflects weak demand at this auction, with the real yield rising while the 5-year nominal yield was stable this morning.

Here is the trend in the 5-year inflation breakeven rate over the last 2 years, showing the strong dip in inflation expectations since February:

Thoughts

I knew this 5-year TIPS auction was going to be hard to predict — this is the case with all 5-year TIPS auctions. The October new issue tends to get a real yield lower than “market,” and the April auction in turn tends to get a higher real yield than expected. The reason is the way the non-seasonal inflation affects the final months to maturity of the April issue. Investors expect some deflationary months in the October to December quarter and want a higher real yield as compensation.

So today’s real yield of 1.702% looks good for investors, in my opinion. I was expecting something more in the 1.65% to 1.68% range. It could be that the holiday week and the early auction time contributed to weak demand, resulting in a higher yield.

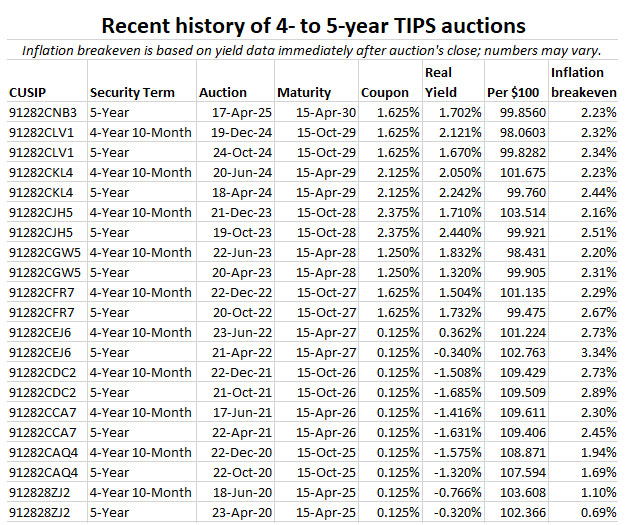

This TIPS will be reopened at auction on June 17 and then another new 5-year TIPS will be auctioned in October. Here is a history of 4- to 5-year TIPS auctions over the last five years, showing that we’ve come a long way from the -1.685% real yield of the October 2021 auction:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’m looking to fill the 2030 step on my TIPS ladder, and I’m wondering what is the best way to compare the three 2030 TIPS that are available. Is it best to compare the total investment cost to the adjusted principal? Using data from yesterday and assuming a $10,000 par value, CUSIP 912828Z37 had an investment cost of $11,652 for adjusted principal of $12,407, a +$754 difference. CUSIP 912828ZZ6 had a +$826 difference, while CUSIP had an investment cost of $40 more than its adjusted principal. I’m not sure how to also factor in real yields and coupon rates in determining the best one to buy. Thanks for all the info on your site!

When comparing TIPS on the secondary market, the most important thing to note is the real yield to maturity, but it is also worth looking at the coupon rate and accrued inflation. As of Thursday’s close:

– The Jan 2030 TIPS has a coupon rate of 0.125%, well below the market, so it has a discounted price, about 93.21. However, that TIPS currently has an inflation index of 1.240, so you’d be buying 24% additional principal at the discounted price. Real yield 1.53%.

– The April 2030 TIPS has a coupon rate of 1.625%, above the market, so it has a slightly premium price of about 100.16. Its inflation index is just 1.002, very close to par value. This TIPS is going to sell at close to par value. Real yield is 1.591%, but this April issue always has a higher real yield because of dangers of deflation in its closing months of Oct to Dec 2039. (This is normal).

– The July 2030 TIPS also has a coupon rate of 0.125%, well below market, so it has a discounted price of about 93.09. But this one has an inflation index of 1.245, meaning you will be buying 24.5% additional principal. Real yield 1.513% So the Jan and July versions are very similar.

Buying inflation-boosted principal is *slightly* risky because future deflation would cause a drop in principal. That isn’t true for the April TIPS, which has a very small boost to principal. There is no right answer for which to buy, but at least this help explain the difference in pricing.

Thanks, yes that does help explain the pricing. Very helpful and appreciated.

The question is whether I understand correctly TIPS US bond 5-year real rate of return was 1.80% and inflation is 2.5%, so I am actually losing 0.7%, do I understand it correctly?

No. If the real yield is 1.8% and the inflation rate is 2.5%, you are earning 4.3%.

Thank you.

I’m having issues with Schwab brokerage and wonder if anyone has info that may help.

I’ve been buying TIPS thru Schwab for decades now, for myself and numerous family, friends and clients. In the past, Schwab always provided the YTM for TIPS purchases in a day-after e-mail confirmation. Starting late February of this year, most and now all of the confirmation e-mails no longer contain YTM. When i first contacted them about this, they said they’d provide the YTM “within a few weeks” if i ask for it. (Ok, that’s a hassle, but could work.)

But after a month, no response. So after NUMEROUS back-and-forth secure messages and several phone calls, they now say they CANNOT provide YTMs per request, and they cannot modify their system to provide YTMs in confirmation emails. I don’t believe it, but they’re basically saying “go away, we can’t help you.”

(Notes: 1. This only affects me for TIPS purchases on the secondary market. YTMs for auctions are easy to find; 2. The Schwab website DOES provide a YTM at time of ordering, but the order is essentially a “bid,” and if you place an order and it’s executed at a better price (happens a lot, in my experience), the YTM changes, and since late Feb 2025 you’re not provided the actual purchase YTM.

Fyi, a couple years ago Schwab also changed its cash management feature so all cash sits idle, earning essentially NOTHING, until you actively move it. Other brokerages, such as Fidelity, have cash sweep features so all “idle” cash is automatically moved to a Treasury money market, earning ~4%.

I wonder if anyone has found a way to extract from the Schwab website the actual YTM for TIPS purchases on the secondary market. But also wanted to let y’all know that, for the above reasons, i’m now (reluctantly, but deliberately) starting to move all of our accounts away from Schwab, and recommending to all my family, friends and clients to choose Fidelity (or some other brokerage) over Schwab. (FYI, i have NO financial or personal interest in any of the brokerages; just interested in putting out the truth to help you make your own decisions.)

I have Fidelity (I don’t have Schwab) and I can confirm that secondary market TIPS purchases from last week show the final yield to maturity on the trade confirmation that is provided by Fidelity the next day after the transaction.

I’m also at Schwab. I haven’t been buying TIPS for a few months; trying to disentangle myself from the US Treasury. But this past week, against my better judgment, I did buy a bit of TIPS in 2 of our accounts (2.15% real yield when CPI is probably headed north of 4% for the next few years was too good to pass up) and noticed the same thing in the confirmation emails, although they do say “call for execution details,” which I haven’t done yet. I remember the same thing happened a year or two ago, where YTM and inflation factors were missing for a month or so. They eventually fixed the problem, but that time they also exhibited Schwab’s odd propensity to have their front-line reps say “It can’t be done” rather than “We’re aware of the problem and working on it.”

But I’m still with them. In 1993, when I had had all our accounts at Fidelity for a decade or so, my father passed away. I bundled up the joint-name stock certificates and certified copies of his death certificate and drove an hour and a half to Fidelity’s nearest office and had the branch manager help me fill out the paperwork to get the shares transferred into my name and deposited into my account. A month later, everything was sent back by Fidelity’s legal office in New York; I had neglected to have my (dead) father endorse the backs of the stock certificates. Back to the sort-of nearby branch, apologies from the branch manager, resubmit with his note explaining that my father (still dead) was not available to endorse (please see enclosed death certificate), everything mailed back to me again a month later…. So that’s why I’ve had all my accounts at Schwab since then. They have their foibles, but so do all large institutions.

David addresses the calculation of the real yield in his TIPS In-Depth section under the heading “Real yield calculation”. With an appropriate iterative calculator such as the Excel YIELD function, you can find the real yield you actually get from any TIPS you purchase whether secondary market or originating auction. Basically the idea is that at the time of purchase, the real yield to maturity is “set in stone”, as David writes, and is calculated just like any other bond. You will use the following values at the time of settlement: unadjusted price you paid, the adjusted principal value, settlement date, maturity date, coupon rate and coupon frequency.

https://tipswatch.com/tips-in-depth/

I have been with Schwab client since 1993 and the most appealing aspect of their platform is 24×7 customer service, which is still much better than Fidelity and Vanguard, where I have accounts as well. Yes, they pay virtually nothing on Cash and they count on investors not have the time to move money to SWVXX or SNAXX, their key money market funds. As you poin out, FIdelity is the better in this regard. So far, I have bought TIPS only at auctions and in my wife and mine IRA accounts, so I have not yet faced the YTM issue. Keep bringing it up with their customer support, have them issue a ticket, and if possible get the ticket number and then keep followingf up. For many years, I wanted Schwab to support software for creating bonds ladder. At a meeting, I spoke with Kathy Jones about it and first she said that the IT budget was limited but eventually they do have ladder building tool now. No platform has all we need….best chander

Fidelity is a great choice, they are one of, if not, the best brokerage account available out there.

When I look at the Fed rates for TIPS (table in home.treasury.gov) I see the rates declining from the beginning of the year. For instance, for the 5 year the number reported for Jan 2 was 1.97% and on April 17 it was 1.69%. Similiarly for the 10 year TIPS those figures were 2.23% and on April 17 they were down to 2.11%.

Now when I look at my TIPS ladder which goes out 2032, each issue’s balance has declined. I would have expected each issue to rise somewhat. Why would this be?

I should add that although I mark those positions to market, I will not be selling until maturity. So this question is just to understand the dynamics of TIPS.

Are you considering the real yield you received at the purchase date for each TIPS? If it was lower than the current market yield, your market value could have decreased.

Sorry, I really got things reversed. I actually had a healthy gain on those TIPS year to date. Helped to mitigate the losses in our equities.

I tend to get interested in TIPS when the rates get up towards 2%. That is what I recall is an average historical real return on intermediate term nominal bonds.

It seems picking up longer term TIPs at a good bit higher rate above inflation are much better for capital preservation over the long run.

Perhaps the “Made in China” label is going to become a status symbol for the rich once the prices on their imported goods double.

This site educated me on TIPS and got me hooked. Got another 15K at this auction in retirement accounts.

I hemmed and hawed and decided yesterday not to buy at this auction. Then I awoke suddenly in the middle of the night and decided to dollar cost average into this issue, so I bought a small amount. I’m hoping to pick up some more at the reopen or perhaps the October new issue to cover future RMDs. 1.70% isn’t what I’d hoped for but it certainly is better than I expected!

I chose to purchase CUSIP 91282CGK1, January 2033, in the secondary market with my 4/15/2025 matured TIPS. I received, according to my calculations, a 1.93% real return. I compared that to about a 4.1% rate on CDs and comparable Treasuries, for a break even rate of just over 2%. In this environment it didn’t take long to add to my TIPS ladder. Even reasonably well rated corporates were paying only 5% or so.

I’m curious what others are doing for income investments in the 5 to 10 year range besides TIPS or to complement your TIPS. I did purchase some $US denominated Royal Bank of Canada bonds at 6% coupon (CUSIP 78014RSD3) at origin which will go to the Secured Overnight Financing Rate (SOFR), now 4.33%, plus 0.75% on 24 Apr 2025. I expect my remaining government agency bonds, all paying > 5.1%, will be called away at the first opportunity. I’ll likely continue with TIPS unless the break even rate exceeds 2.5%.

I’ve been alternating super safe TIPS with riskier baby bonds (exchange traded debt) with staggered maturities for retirement income.

For example, this TIPS maturing April 2030 is flanked by NYMTG (4/1/2030 maturity, 9.125% coupon) and OXLCI (6/30/2030 maturity, 8.75% coupon).

I thought demand might be relatively low for this one. I was a buyer, and I’m happy with the result (although a 2% coupon would have been better, of course…).