By David Enna, Tipswatch.com

Long-time readers of this site know when I go on holiday, bad things happen. There’s consistently a debt crisis overload, a banking crisis, housing collapse, Fed reversals, lavish tariff announcements and roll-backs, etc.

I’ve been touring Scandinavia since May 10. That’s three weeks, but it feels like a lifetime in an era of financial unrest. During that time, I saw very little financial news. Although I could sometimes watch CBNC on board the Viking Vela, my wife usually nixed that channel immediately. Plus, I was dealing with a 6-hour time shift.

So now, knowing little about what happened since May 10, I am going to look at what matters: the actual results.

Our net worth

From May 10 to June 1, our family net worth increased 1.78%. Case closed. This is the only financial measurement that matters, right? Things worked out well, no matter the potential chaos between those dates. But keep in mind that my stock allocation is only 35%. If yours is higher, you did even better.

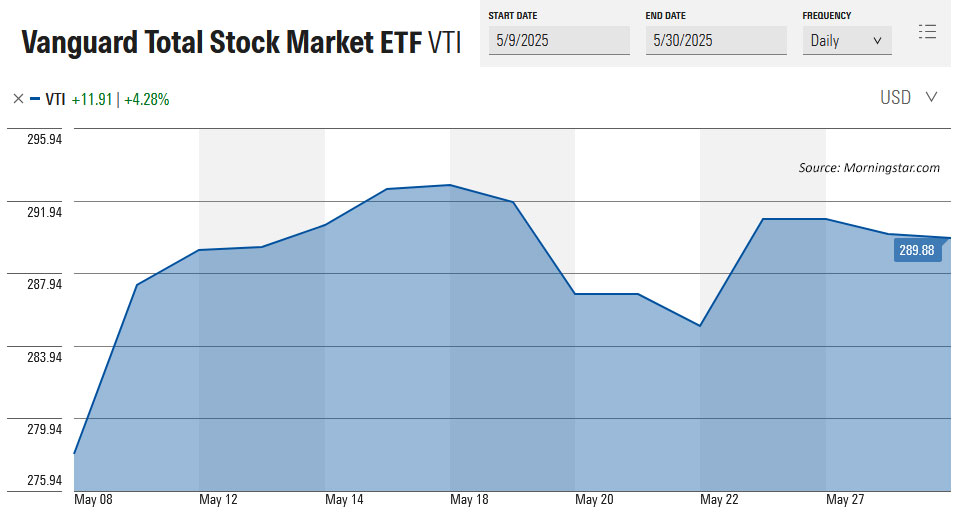

Total U.S. stock market

Using Vanguard’s VTI ETF as the baseline, the net asset value of the total stock market had a positive return of 4.28% from May 10 to May 30. Over the last month, its total return (including dividends) was 6.25%.

Total international stock market

Using Vanguard’s VXUS ETF as the baseline, the net asset value of the total international stock market had a positive return of 3.03% from May 10 to May 30. Its total return over the last month was 4.82%.

Total bond market

Using Vanguard’s BND ETF as a baseline, the net asset value of the U.S. total bond market increased 0.28% from May 10 to May 30, despite fairly large swings in Treasury yields during that period. However, its total return for the full month of May was -0.67%.

Real yields

Throughout 2025, the real yield curve of Treasury Inflation-Protected Securities has been steepening. Longer-term investors are being rewarded with higher yields to compensate for the higher risk of a long-term investment. This is actually a return to “normalcy,” but we haven’t seen it often in the last dozen years.

Based on tax and spending proposals moving through Congress, U.S. deficits appear likely to continue increasing (possibly sharply) over the next five to ten years. The bond market is unhappy — and the result is higher yields, especially for mid- to longer-term Treasury investments. Here is what happened over the last three weeks:

What’s interesting in this chart is that real yields ended May at their lowest level of the three-week period. The shorter end of the curve is much lower, possibly reacting to potential Federal Reserve interest rate cuts later in 2025. But the longer-term end of the curve is holding solidly higher. These are attractive levels, in my opinion, for hold-to-maturity investors. Others disagree, as reflected in this report from Bloomberg this morning:

For DoubleLine Capital, there are two approaches to consider when it comes to 30-year US Treasuries: either avoid them, to the degree they can, or outright short them.

Wary of America’s swelling federal budget gap and growing debt burden, the money manager led by Jeffrey Gundlach is part of a wave of investment firms — including Pacific Investment Management Co. and TCW Group Inc. — that are steering away from the longest-dated US government bonds in favor of shorter maturities that carry less interest-rate risk but still offer a decent yield.

Bob Michele, the global head of fixed income at JPMorgan Asset Management, said last week that the long bond isn’t trading now like the risk-free asset Wall Street always believed it to be, and that the possibility of a reduction or cancelation of the auctions is real.

“I don’t want to be the one to stand in front of the steamroller right now,” Michele said in a Bloomberg Television interview. “I’ll let somebody else help stabilize the long end. I’m concerned that it’s going to get worse before it gets better.”

So, despite the positive news that the stock market brought in the last three weeks, the U.S. Treasury market remains troubled. It is impossible to say where real yields are heading, but higher is a definite possibility if the bond market stages a revolt.

In my headline I used the phrase “good things.” I am not sure that the events of the last three weeks match that phrase, but so far the markets are adapting.

What’s ahead

I’ll try to catch up on financial news, of course. We will get the May inflation report at 8:30 a.m. on June 11, then get a 5-year TIPS reopening auction on June 17 (a Tuesday)!

Eventually the debt-limit debacle will reach crisis mode before it is solved. That could end up creating aberrations in the short-term Treasury market. I will be watching for that.

If you have ideas for new content, or just strong (but not overly political) opinions, let everyone know in the comment sections below.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Welcome home, Dave.

You and TipsWatch readers couldn’t help but have noticed today’s posting from the Bureau of Labor Statistics:

Accurate and uncompromised CPI reporting is the cornerstone of TIPS and I Bond investing. Interested in your take.

Best,

MBS in LA

Here’s some not so good news from The NY Times:

U.S. Is Trimming Back Its Collection of Consumer Price Data

The cutbacks would have “minimal impact,” the government said, but economists warned of reduced confidence in inflation data produced by a struggling statistical system.

Hi, Dave.

I hope you enjoyed your vacation. Welcome back.

Looking at your chart of yields at various maturities from May 9 through May 31st, I read the changes as noise…nothing large enough to generate an opinion.

Regarding an idea for further discussion, perhaps TIPS in taxable vs. tax-deferred accounts. Especially in high income tax states, and maybe even in others. I have been having some thoughts about that which differ from the common wisdom.

Regarding “overly political opinions”, I am fairly sure we all have those. *smile*

Great points!!!…as Churchil said, Americans will always do the right thing, after they have tried everything else….. 🙂

There have been several appearances by Double Line’s Gundlach and Sherman saying they are avoiding the long Treasuries, and even shorting them. They are instead buying “the belly” of the curve. As chanderkhanna1 noted, a hold-to-maturity bond investor is playing a different game. I agree – I wouldn’t know how to short a bond even I wanted to, and I only buy a bond with the intention to hold. The belly of the Treasury curve is the least appealing to me at this moment. Sherman admitted in one interview that they build funds with time horizons of 5 years or so (although I don’t think they close their funds regularly). I infer that there is a cost to them of for example buying a 20 year Treasury at 5%, having it show a significant drop in value for 10+ years if the long rates rises. That cost could be a drop in fund value, with fewer new investors – or worse, an exodus from the fund forcing sale at a loss, not all that different from what happened to SVB.

In addition to long dated TIPS, I have been buying nominal Treasuries (to hedge against lower inflation) and long dated Munis which could continue to pay despite a US delay or outright default. I did also buy a little highly rated corporate debt of intermediate term but am not thrilled with the credit spread. Agency bonds rates are up on the long end again but my personal allocation there is already high and talk of privatization gives me some pause.

I also generally avoid bond funds but do use them to access parts of the credit market inaccessible otherwise. Examples include JAAA and CLOA for AAA bank funds, and DBLIX and DFLEX (two Double Line funds heavy in asset-backed debt. DBLIX isn’t free to buy or sell, and the expense ratio is set to increase in a few months. I bought it last year because it held fewer Treasuries and Agency debt which I much prefer to buy myself and hold in my taxable account).

Thank you for this excellent site and forum.

I will look into the bond funds you buy, thanks!! When it comes to building income with bonds, I don’t want to have a single penny of loss ever. All bond funds have interest rate sensitivity and they are owned by so many others, including institutions. Most of the big players focus on total returns and, yes, they do plenty of hedging. I too only go for the long play with no shorts. My stock side of the portfolio gives me plenty of volatility and stress. I also own the likes of VIG to add to my fixed income dividends and their growth. As it turns out, we have entered an era of high interest rates, unlike the last 2 decades or so. With growing debts all around, we will see how long respectable interest rates last.

Further down this page is a series of comments about the extent of U.S. national debt, and a link to an interview with Harvard economist Laurence Kotlikoff discussing ways to address that debt. But, as David has told us, the site software only allows three comments “deep,” so that at some point it becomes impossible to “Reply” to someone else’s comment.

Where the subject of Social Security is concerned, every time I read interviews with Serious People such as Kotlikoff, I’m reminded of a major option which is staring them in the face but goes unmentioned.

There’s a cap on the amount of salary income subject to the tax which supports Social Security. In 2025, it’s $176,100. Salary of $500,000? $1,761,000? $17,610,000? Not a penny of extra Social Security tax collected.

A study, now 15 years old, U.S. Senate Report 111-187, by the Senate Special Committee on Aging, explored “Social Security Modernization: Options to Address Solvency and Benefit Adequacy.” And among its findings were that the removal of that tax cap, in the absence of any other changes in the Social Security program, would, by itself, solve Social Security’s funding issues for the following 75 years. But this is the one solution that Republicans, and even most Democrats, will not consider.

Since the Social Security tax applies only to wage income, but the wealthy derive a disproportionate share of their own income from real estate and assorted financial instrument speculations, another possibility is to apply the Social Security tax to all “income,” regardless of source, instead of just to wages and salaries. But this, too, is never discussed, by politicians who claim to venerate “work” but nevertheless penalize it in tax terms.

It’s apparently easier to talk about cutting benefits (euphemistically called “reforming entitlements”) for the many rather than raising taxes on the fewer. Given the operation of our campaign finance system and the way it shapes the votes of elected officials, this shouldn’t be surprising.

https://www.govinfo.gov/content/pkg/CRPT-111srpt187/html/CRPT-111srpt187.htm

100% agree. With 10 years to go, simple fixes now could wipe out the problem. Raise the income cap, and phase in a higher full retirement age. Keep the tax on Social Security benefits for higher income people, even though we all hate it. But no one in power is willing to do that combination.

Raising the cap would see more liquidity flowing into DC all right. Then a lot would depend on how they managed it.

“The removal of that tax cap, in the absence of any other changes in the Social Security program, would, by itself, solve Social Security’s funding issues for the following 75 years.”

I think that “in the absence of” phrase is a big deal. If you eliminate the cap on taxation without eliminating the cap on benefits, it makes it pretty obvious that Social Security is a welfare program. It is, and has always been, a welfare program of course, but most people don’t think of it that way.

Remember, we all paid into this “welfare program” for 40 years or more. Kind of unusual for welfare. (I could agree with the monthly payments increasing somewhat — in the future — for the very wealthy who actually contributed in the future, even though they don’t need it. But the payments would need to be taxed as income.)

It might be unusual, but it doesn’t change the fact that by paying higher benefits to lower wage people than to higher wage people (relative to their contributions), and by each successive generation having to support more retirees than the prior generation, it transfers money from the rich to the poor and from the young to the old. It’s a well-disguised welfare program.

The “each successive generation…” part could be reversed if birth rates went back to prior levels. I doubt that’s going to happen, but at least that aspect of the income transfer was probably unintentional.

Thank you very much for your blog. An ask: it would be really helpful to see (near title) the date a blog post is written/published.

The mobile site (for phones) doesn’t show the published date; not sure why and I can’t change that setup. The desktop and iPad version does show the published date on each posting.

Regarding the last few months, I see the bond market getting a mixed message. Inflation was lower than appears many expected while US Treasury debt purchases are likely higher than expected for the recent past and coming future. I’ve commented before that I couldn’t have imagined trillion dollar government deficits (not even debts), debt to GDP ratios well over 100%, plus low inflation and relative interest rates simultaneously. I’m happy with the outcomes of the past few years and particularly the past 5 months given all the market is trying to absorb.

Personally, if I were back in my late 20’s I would find the present market relatively appealing compared to the early 1980’s (stagflation) and 2008 to 2022 (TINA – there is no alternative as implied inflation was <1% and sometimes negative). TIPS would have been nice to have around, especially ones paying 2.5%+. I consider it lucky, not smart, that I experienced a period of extraordinarily low inflation from ages 30 to nearly 60. All data sources that I’m aware of (TIPS, Fed Data Series, Gold Sellers on Late Night TV) generally predicted higher than actual inflation rates until very recently.

As an economist, I concur with JK Galbraith, “The only function of economic forecasting is to make astrology look respectable.” But, that said, I forecast that people who invest a good share of their income portfolio in TIPS until maturity at these rates while minimizing debt as possible will have few regrets. A debt default certainly would be hard to absorb, but if you think that is likely you may want to turn to a “prepper’s guide” for complementary advice.

I’ll continue to re-balance regularly to my 50/50 position and tend to my garden.

I guess my questions are, is it too late to invest in stocks now? And what stocks/sectors to invest in?

This is the eternal question, and it is impossible to answer. On “The Money Guy” podcast — which I recommend — the host often explains that the path of stocks is like a person hiking up a hill with a yo-yo. The yo-yo goes up and down but the steady course is higher. However, we can’t know that for certain. I am a contrarian and generally rebalance into the market after a decline.

I like the Money Guy podcast, too, and particularly emphasized the benefits of dollar cost averaging (buying monthly, for example, into the funds over time). This is often left out of the past market performance and any fund return calculations that I see but more realistic for most people saving for retirement.

It’s easier now to look back than it was in the “heat” of 2000-2002 (dot com) or 2008 (Great Recession), but just putting in my monthly 401k contributions and re-balancing on occasion helps sticking to a plan.

And, if you’re out of the stock market or come into money through inheritance, buyout, …I suggest to friends/family they consider dollar cost averaging the money into the market. It may cost a some return (and regret when you miss years like 2023 or 2024), but you also miss going “all in” just before years like 2022 and 2008.

Has there been any issues with your accepting the I-bond from your gift box this year? I believe you purchased your allotment and then received the gift.

Last year I successfully transferred two sets of gift I-Bonds after purchasing the cap amount in those two accounts. No problem. Then this year I purchased the cap amount in the two accounts, no problem. But we have no definite advice from TreasuryDirect. My suggestion is to purchase the cap amount first (regular way), then do the transfers. The other way around may not work.

Thank you. That is my plan for this year. I have made my 2025 purchase, I will accept the gift bond and see what happens.

Worse case is they return the money, with interest.

On the day you were in the airplane coming home, Jamie Dimon warned of the bond market collapse. “…changes…in the tax system could increase the deficit by an estimated $2.7 trillion to $5.2 trillion over a decade“.

Sorry about the cortisol stimulation. I can’t vouch for the merit of Essa News. Welcome home.JPMorgan’s Jamie Dimon warns of imminent U.S. bond market crisis

$5 trillion is probably a good 10-year estimate, since even this bill includes expiring tax cuts (as did the last one), which will never be allowed to expire because that would be a tax increase.

“I’ve known Jamie for a long time, and for his entire career he’s made predictions like this. Fortunately none of them have come true. That’s why he’s a great banker. He tries to look around the corner.” Scott Bessent, US Treasury secretary

What I want to understand is whether rising treasury yields due to the risk of US debt eventually translates to rising inflation. In other words if we make the assumption that the US will have to pay higher and higher rates to finance the ever growing riskier debt. Is holding TIPS actually a good place to be? It is if they are going to inflate away the debt, but I am not sure it always goes hand in hand, spiraling debt and rising inflation. What is your opinion?

I had posted an article here years ago that governments cannot “effectively inflate away a debt”. Lawrence Kotlikoff had a thesis that we are not so much investing and playing the financial markets as we are putting away money for the time when we are not earning to support ourselves. That’s what got me to TIPS and to this forum. “Spend ‘Til the End”, 2008, with Scott Burns.

Here is a Harvard podcast and article on that topic, from 2023: https://gsas.harvard.edu/news/colloquy-podcast-debt-ceiling-and-beyond-laurence-kotlikoff

As I see it, there are three different narratives in play for the three segments of the Treasury Market: Treasury Bills, especially the shortest end to 2-year, are reacting primarily to the possibilities of Fed rate cuts, Treasury Notes, especially the 10 year, are reacting to the Tarriffs, Inflation, and the economy, while the Treasury Bonds are reacting to the demand for term-premium. Foreign bond investors seeing the US, Europe, Germany in particular, and Japan continuing to add debt demand more term premium.

So far, I have been maximizing my interest income by picking Bills of different maturities. My eyes are on the August 20th, new 20 year nominal bond auction. If I get 5%, I will be super happy and will hold the bonds to maturity. I am 69 now and most likely my wife or daughter will enjoy the principle, I am happy with that. I am all about income and not the total return that Bond Kings talk about. I love I Boonds and TIPS ladders (in our IRA acounts) – both kept to maturity. I don’t like or buy Bond funds and don’t balance our portfolio because we have built our low cost expense ratio portfolio, sort of permanent portfolio, bottoms up and based on expected income and growth needs – with mostly high quality stocks, stock ETFs and Treasuries.

I do extensively read and understand enough about most of the scenarios and risks in the press, IMHO most of it is noise, politics, or entertainment. You can call me naive, but I belive that all of this will also pass and somehow we will muddle through it all. If you are reading up to this line, you are very kind and generous to me…thanks!!!

Chris, it’s more likely that very high interest rates would lead to a recession, which could then tamp down inflation. Or we could get into the dire stagflation scenario, with high inflation and a recession at the same time. We seem to be at an inflection point, sort of like Marvel’s multiverse. Things could develop in many ways.

Now that’s rare, an economic superhero saga metaphor. You’d have to be an Iron Man to figure out the End Game of today’s chaotic tariff policies and budget plans.

Dr. Strange, actually. 😅

Very high interest rates will lead to quantitative easing aka money printing and that may cause inflation to rise.

Or, we borrow ever more (same inflationary effect as money printing) increasing the supply of bonds, and driving interest rates higher.

Balance the budget and both the inflation & interest rate problem will be solved very quickly.

High Tariffs = eliminating the marginal buyer of US Treasuries. High tariffs must be paired with a balanced budget, if not it will lead to default, or lots of money printing & high inflation.

Jason Zweig, in the Long View podcast, opined about Mar Lago accords and the U.S. government renegotiating terms on government debt. He referenced Mar Lago Accord. It is a strange time to imagine a world where the U.S. government reneges on its promises!

Is this even feasible without Congress authorizing this?

I find it very hard to imagine sticking to such a plan for very long even if a President, with or without Congressional approval, tried to not make timely interest and debt payments. It would require a President to refuse to follow a Congressional order for the Treasury to not make payments, or possibly Congressional inaction (e.g., not raising the debt ceiling, not passing a budget or continuing resolution). Even a delay would likely force a tax increase, drastic budget cuts, etc.

To default, I think it would be an especially egregious act without the U.S. actively involved in a war. We did suspend debt payments to Germany and Japan during WW II then restructured them during rebuilding of those countries. I could imagine some countries parsing their US debt holdings if that looked likely.

It would be a very painful market reaction, likely equivalent or worse in my opinion, than a regional or global war in which the US was a direct participant. And, as any corporation or person knows that has defaulted on debt the market punishment can last a long while.

Is it, though?

From May 10 to June 1, our family net worth increased 1.78%. Case closed. This is the only financial measurement that matters, right?

I left it that open-ended intentionally.

At the least, it is an indication that nothing collapsed while I was away.