By David Enna, Tipswatch.com

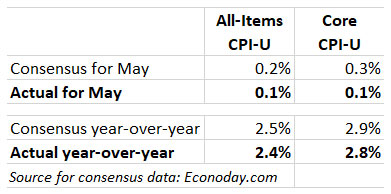

U.S. inflation continued rising at a moderate rate in May, with all-items prices increasing only 0.1% on a seasonally adjusted basis, the Bureau of Labor Statistics reported today. The annual inflation rate for May increased to 2.4%, up from 2.3% in April.

Core inflation, which strips out food and energy, also increased 0.1% and at an annual rate of 2.8%, down from 2.9% for April. All of these results were below economist expectations and should be viewed positively today by financial markets.

May’s result continues a recent string of lower-than-expected inflation reports.

The BLS said shelter costs rose 0.3% in May and were the primary factor in the all-items and core inflation increases. Shelter costs were up 3.9% year over year. Here are other notable items from the report:

- The cost of food at home increased 0.3% for the month and 2.2% year over year.

- Gasoline prices fell 2.6% for the month and are down 12.0% for the year.

- Apparel costs — which could be affected by tariffs in the near future — fell 0.4% for the month.

- Prices for new vehicles fell 0.3% for the month and are up only 0.4% year over year.

- Costs for used cars and trucks also fell 0.5% for the month.

- The cost of motor vehicle insurance rose 0.7% in May and was up 7.0% year over year.

- Airline fares fell 2.7% in May and 7.3% over the last year.

Overall, U.S. prices seems to be showing little effect from U.S. tariffs, which began rolling into effect in May. Overall inflation appears to be being held down, at the moment, by declining gasoline prices and held higher by increasing shelter costs.

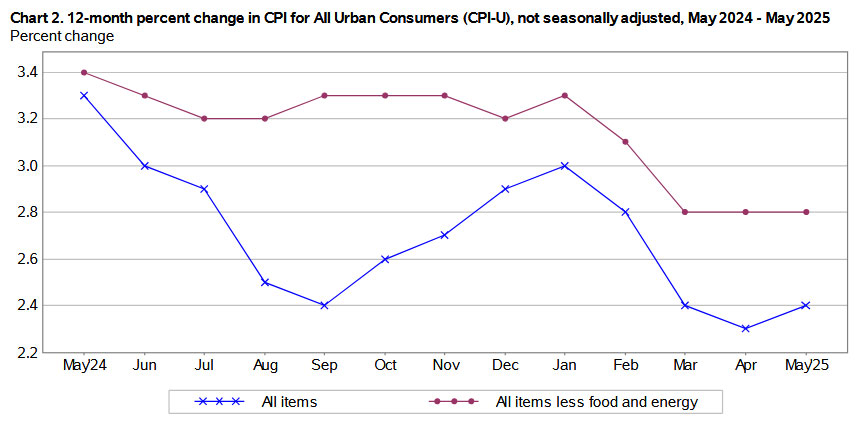

Here is the one-year trend in annual all-items and core inflation, showing the relatively stable pattern over the last three months:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For May, the BLS set the CPI-U inflation index at 321.465, an increase of 0.21% over the April number.

For TIPS. Based on the May inflation number, principal balances for all TIPS will increase 0.21% in July, after increasing 0.31% in April. For the year ending in July, principal balances will have increased 2.4%. Here are the new July inflation indexes for all TIPS.

For I Bonds. The May inflation report is the second in a six-month string that will determine the I Bond’s new variable rate, which will be reset on November 1 based on inflation for April through September. Two months in, inflation has increased 0.52%, which translates to a variable rate of 1.04%. It’s too early to draw any conclusions from that. Here are the data:

What this means for future interest rates

The current string of moderately low inflation reports should be clearing the way for future cuts in short-term interest rates by the Federal Reserve. But the overhanging uncertainty about tariffs is a roadblock to any Fed decision.

Bloomberg’s headline this morning is: “Cool US CPI Boosts Bets on Two Fed Rate Cuts by Year-End.” I’d say we were probably heading that way anyway, and today’s inflation report solidifies that trend. But inflation traders still see inflation picking up later this year to around 3.2%.

Inflation expert Michael Ashton posted this analysis this morning:

While we haven’t seen a major impact from tariffs yet, and my view is that it won’t be a huge impact in any case except for particular items, I am pretty sure we will see something and median and core inflation will see acceleration over the balance of this year and into next year.

Uncertainty remains. While we may see cuts in short-term rates later this year, longer-term Treasury rates could continue rising as the U.S. heads toward higher future deficits and higher borrowing. We are going to see a lot of “crisis talk” in coming weeks as we march toward a massive tax bill and debt-ceiling limit.

* * *

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

You might be proven correct in your assessment of tariffs. But perhaps not. A couple of points:

3. It will show up in the data assuming the data is maintained with the same semi-accuracy as before. There are some questions about that. But assuming it does, there are other variables in play beyond tariffs that could impact inflation and GDP — international conflicts, innovation, energy prices, the tax plan, etc. it’s not always easy to isolate one variable, but the current tariffs are so unprecedented and volatile and far-reaching that it is easier than is usually the case to do so.

I wonder if the data is reliable any longer. It wouldn’t surprise me if the inflation number had to fit the administration’s narrative and political goals. They’re already showing a disregard for facts.

Tariffs are a tax.

It makes sense for Florida to have a very high sales tax rather than an income tax, because it has lots and lots of tourists, so nonresidents pay a material amount of the total sales tax (16% of the total sales tax revenue in the 2021-22 fiscal year), and nonresidents would pay only a trivial portion of a state income tax. Similarly, it makes sense for New Jersey, which has lots and lots of nonresidents driving through the state, to fund its roads with high tolls (it is estimated that 30%-50% of the traffic on the NJ Turnpike is out-of-state residents), rather than gas taxes.

In the same way, tariffs make a lot of sense as a tax because a material portion of the tax is absorbed/paid by manufacturers or wholesalers who are not U.S. people or entities. The “tax” paid by U.S. people/entities would be reflected in the inflation rate (and might be in the coming months). But so far . . . in May 2025, the U.S. collected a record $23 billion in customs duties (tariff revenue), as reported by the Treasury Department. This marks a $17 billion increase over May 2024, when customs receipts were approximately $6 billion. Doing that with declining inflation and accelerating GDP growth (current Atlanta Fed’s GDPNow forecast for Q2 is 3.8%) over a 12-month period would be a positive.

Your Paragraph 1 comments about different states maximizing their tax revenue in ways that are advantageous to them makes sense. Your Paragraph 2 comments about tariffs do not, in my opinion, especially in the way they are being implemented.

Tariffs are indeed a tax increase on consumers, passed down the supply chain from importers to resellers to consumers. While it is true that 100% of tariffs are not likely to be passed along to consumers, and not likely to be passed along to consumers right away, you can bet they will be passed along, in part or in whole, to consumers.

Tariffs are he “wrong” kind of tax on consumers because they are regressive. Our overall tax system already favors the wealthy in numerous ways with lower capital gains rates, deductions, and loopholes; this just compounds the serious issue we have with income inequality in this country.

Tariffs, predictably also cause our trading partners to retaliate, some more than others. That exacerbates the impact of tariffs as a tax. The current administration knows tariffs are regressive, which is why they prefer this type of “hidden” wealth transfer. And politically, they can say they did not raise taxes, when they actually did.

Beyond that, everything about the method of implementation of the current tariff policy has been wrong. The statement that foreign countries pay the tariffs was wrong. The rates presented in the tariff rate chart to justify the amounts were wrong. Tariffing all countries, allies and adversaries alike, trade agreement or not, was wrong. Tariffing penguins on uninhabited islands was wrong. The extent of the tariffs was wrong. Tariffing countries, then pausing them, then resuming them, then saying they would not change, and then pausing them again creates tremendous economic, business, and financial market instability, which was wrong. What we have witnessed has been the textbook way not to impose tariffs.

Is there a legitimate point to be made that foreign markets aren’t as open as they should be to American goods? Yes. Has it actually hurt us over the past century? No, not in the grand scheme of things. Yes, in some cases, we could sell more goods overseas if those markets were open, but America has been, and continues to be, the most prosperous nation in the world and has the greatest economy in the world. The dollar is still the world’s reserve currency. We have done just fine with the post-WWII order of things. Is this way to go about opening foreign markets to American goods? No, I can think of dozens of other ways this could be achieved. Then you add the ridiculous rhetoric we have been hearing for months that insult and disrespect our closest trading partners, like Canada, and the result is Canadian tourism to America and purchasing of American products have fallen off Niagara Falls, and that makes these tariffs even worse.

Actual data: GDP was 2.4% in the 4th Quarter of 2024 before tariffs. GDP was -0.3% in the 1st Quarter of 2025. While the Bureau of Economic Analysis does expect 2nd Quarter GDP to be 3.0%, up from 2.8%, that remains to be seen. America’s economy is resilient, but only for so long.

Lastly, regarding inflation, it has been steadily declining for years as supply chains eased after seizing up during the pandemic reopening, and that trend has continued. Why didn’t inflation spike from tariffs yet? Four reasons:

Tariff chaos (on/off/on/off) creates confusion and a wait and see approach.

We have seen weaker consumer demand and consumer confidence.

The gradual and partial, rather than the immediate and full, pass through of tariff costs.

Business stocked up on inventory before tariffs went into effect (Apple shipping boatloads of iPhones from China just before tariffs kicked in is the perfect example). This won’t last forever.

Good day to you all, my fellow Inflation Analysts! 🙂

We may have touched on this here before, but the term “core inflation” is a term that makes so little sense to me. I get the point that food and energy prices are perceived to be more volatile than other items. But, food and energy seem to be very much a “core” of what humans need.

Should food and energy be lumped together into “high volatility” category to start with? Look at this analysis, for example – food can be volatile and not volatile, depending on what kind of food we are talking about. Price Volatility and Headline Inflation | St. Louis Fed

To me, it would make way more sense to look at either “all items inflation number” or “specific category” inflation number.

This completes my “accepted terminology is nonsense” rant of the day, and it is time to look for a reasonably priced breakfast in Hawaii. “Reasonably priced in Hawaii” – would the correct term be “oxymoron” for this?

I am the unusual person who drives less than 3,000 miles a year, so gas prices aren’t a major factor for me. But I do eat food! I think Fed officials “pretend” not to pay attention to food and energy prices, but they know these are the prices that hit consumers hard and are dangerous politically. Core is a better indication of overall price trends because the volatility is lower.

One theory on energy and food being closely related is about “it takes gas to deliver food to stores” – makes sense, I suppose.

One weird thing about volatility table in the link I sent – apparently fruits and vegetables are high volatility, while food prepared at home is low. I would have thought the other way around, or at least equal. Now I am curious how long is the route for my apples and oranges to get to me.

As a business that relies exclusively on imports from China, my feeling is the rise in prices is just beginning and will continue to head north as long as this tariff game continues. Initially I simply stopped my shipments because we were at 145% now they have dropped them to 30% so I have been allowing some trial shipments. Something to note is 30% is on the total cost of the shipment, so you pay not only on the product but on the freight costs, makes the product cost more like 45% higher. Also major carriers like fedx, ups, dhl are simply charging the 30% on everything. They have a higher diminis rate if under $800 but that seems to be being ignored. That was something the post office was going to have to impose, however the post office is doing nothing, you can’t even send product through the post office anymore as far as I can tell. For example I used Hong Kong post a lot prior, which hands off to USPS. They just stopped offering service to the USA. Claimed it wasn’t worth it. The thing is the Chinese are already hard at work trying to get around these tariffs. Alibaba is a giant logistics company, your package all go on a cargo plane. These things are not being processed individually, somehow Alibaba claims shipments are duty free. I think they are getting around much of the tariffs by bulk loading and under valuing. Things are changing daily. But I promise overall prices are going up if things are not resolved, and made permanent.

Chris, your specific mention of DHL reminded me of previously read news articles reporting that, because of the tariff conditions, DHL was suspending all U.S.-bound shipments valued over $800.

That was in late April. If you’re involved in a U.S. business dealing with foreign product, then, of course, you’ll have a much better idea than I could about whether this DHL decision is still the case, or whether DHL meant it to apply to all customers or only on shipments directly to U.S. retail buyers.

https://www.bbc.com/news/articles/c1jx9ep5l63o

https://www.npr.org/2025/04/21/nx-s1-5371307/dhl-stops-shipping-packages-800-us-customers

https://supplychaindigital.com/supply-chain-risk-management/dhl-halts-high-value-us-shipments-over-trump-tariffs

Fascinating and unique analysis, Chris. Thank you. I may ask you to write a complete article for me, especially if you can compare specific price increases before / after.

I recommend this blog.

“Overall, U.S. prices seems to be showing little effect from U.S. tariffs, which began rolling into effect in May.”

I don’t know about other readers here, but Trump has announced so many different tariffs, then delayed their effective dates, and/or reversed them, and/or announced a reduction in their percentages, and/or announced an increase in their percentages on some specific goods but not others, and/or announced an increase or decrease in their percentages on some specific countries but not others, and/or announced that he’s about to cut a deal with Country X, and/or announced a way that he’s going to punish County X if it “fails” to give him a deal, that . . . I don’t have a clue about what tariffs are actually in effect, let alone how they’d affect any measure of “inflation.”

Reading through your post, I thought you might be engaging in hyperbole, but pausing and rereading your response I can’t pinpoint any non factual statement.

You summed up Trump’s approach perfectly. Disorganized, chaotic and inconsistent.

Yes, planned or realized policy chaos delayed the impact.

But also consider there’s a longer sequence – Supplier to Manufacturer to Distributor to Retailer – which represents a very common pathway for goods in a supply chain, especially in consumer goods.

On April 2nd, I don’t think any participant was truly prepared to increase prices. It’s possible the logical first steps were taken by some Retailers in April – holding off on regularly scheduled promotions or markdowns, or delaying restock orders.

But I’d bet a lot of the price action is yet to come. If it helps, think of your neighborhood Retailer as holding off as long as they can to help you out; but don’t think they’ll be selling things at negative margin after the Supplier’s increases impact the Manufacturer which impacts the Distributor.

Doubtless there will even still be some un-tariffed goods in stock throughout 2025 when you look at apparel, durables and so forth. However, the average consumer will be seeing increases more quickly on imported grocery items. Sucks for everyone who needs groceries, unless you’re rich and greedy, then you might be proud to have the poor footing a tax bill on their grocery basket in a new, hidden way.

“The current string of moderately low inflation reports should be clearing the way for future cuts in short-term interest rates by the Federal Reserve. But the overhanging uncertainty about tariffs is a roadblock to any Fed decision.”

“Bloomberg’s headline this morning is: “Cool US CPI Boosts Bets on Two Fed Rate Cuts by Year-End.” I’d say we were probably heading that way anyway, and today’s inflation report solidifies that trend. But inflation traders still see inflation picking up later this year to around 3.2%.”

If tariff policy is holding the Fed back from lowering interest rates now, and inflation is expected to rise 0.8%: from where it is today by year’s end, why would the Fed cut interest rates?

Inflation expectations are often wrong. But you raise a good point.