A looming debt-limit crisis is causing yield anomalies.

By David Enna, Tipswatch.com

In looking over this week’s auctions of Treasury bills, I noticed something unusual, but also predictable: The looming debt-limit crisis is beginning to send tremors through the short-term Treasury market.

For example, on Thursday I posted these results on X:

It’s unusual to see a 41-basis-point spread between the yields of a 4-week versus 8-week T-bill, on the same auction day. For example, on May 13 the 4-week auctioned at 4.293% while the 8-week was 4.322%, only a 3-basis point spread. That’s normal. A 41-basis-point spread is a strong indication that investors are pouring into the 4-week and shunning the 8-week, which will mature August 26, 2025, potentially in the middle of a Treasury funding crisis.

And then, also Thursday, Treasury issued $60 billion in an unusual 77-day cash management bill, which will mature Sept. 16, potentially beyond the crisis. The usual CMB size recently has been $50 billion and the term has been 14 days, sometimes 42 days. Treasury gave very specific reasoning for the change:

As noted in the May 2025 Quarterly Refunding Statement, until the debt limit is suspended or increased, debt limit-related constraints will lead to greater-than-normal variability in benchmark bill issuance and significant usage of cash management bills (CMBs).

Beginning with a CMB auction announcement on June 24, 2025, Treasury expects to issue a series of CMBs over the next month for up to $250 billion in aggregate. Each of these CMBs will mature on a Tuesday or Thursday in the second half of September. … Treasury expects that issuing these CMBs will at least partially offset the anticipated reduction to the net supply of Treasury bills associated with shrinking 4-, 6-, and 8-week benchmark bill offering sizes.

Technically, the debt-limit crisis has already begun. Since Jan. 21, Treasury has been using extraordinary measures to finance the government. And it has noted, “Treasury is not able at this time to provide an estimate of how long its cash and extraordinary measures may last.”

The expected “X-date,” as it is called, is likely to hit between Aug. 15 and Oct. 3, according to the Bipartisan Policy Center. As Aug. 15 approaches, you can expect to see anomalies popping up in T-bill auctions for issues that will mature during the potential shutdown.

We’ve seen this before

The anomalies will take two forms: 1) sharply lower yields on 4-week T-bills as long as the crisis remains more than 4 weeks away, and 2) sharply higher yields on longer-term T-bills that will mature in the “danger zone.” Eventually, as the X-date gets very close, investors will demand higher yields on the 4-week, too.

In 2023: The chart shows the dramatic disruption of the 4-week T-bill, with yields falling sharply at the same time the 13-week yields were rising. Once the debt limit crisis X-date reached one month away, the 4-week yield soared above the 13-week.

In 2025: At the far right of the chart, you can see the beginning of the predictable pattern: The 4-week yield is falling while the 13-week yield is rising.

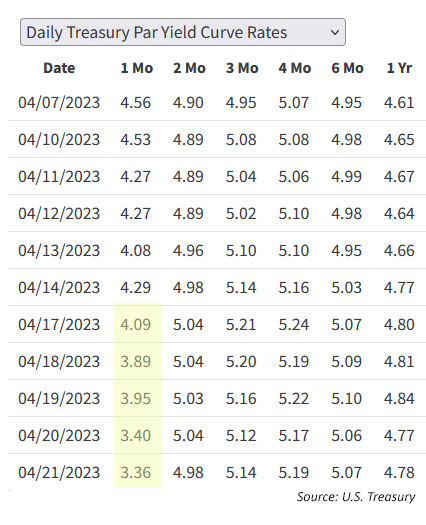

I wrote about this back in April 2023, and included this chart showing the divergence in yields a month-plus before the crisis was resolved:

This chart, from the Treasury’s Yields Curve estimates page, shows that the 4-week T-bill’s yield fell 120 basis points in three weeks, while the 8-week was up 8 basis points and the 13-week up 19 basis points. The same is true across the T-bill spectrum — every issue except the 4-week saw yields rise in April 2023.

This disruption is routine because of the strange way the United States handles its debt limit, forcing a periodic crisis (and eventual resolution). This is a 2023 chart from Moody Analytics:

So far in June 2025, the T-bill disruption is just beginning, but it will step up in coming weeks if the debt limit is not increased:

In a normal market, the 4-week T-bill’s yield should be very close to the effective Federal Funds rate, which currently stands at 4.31%.

This is not a ‘crisis’

The issue could be resolved in the next week, if Senate and House Republicans can get near 100% agreement on President Trump’s “Big Beautiful Bill.”

In most versions of this funding farce, you had Republicans controlling at least one house of Congress, combined with a Democratic president. In only takes a handful of members of Congress to set off the crisis, usually as an attempt to to gain spending-cut concessions. Eventually, a compromise is reached.

In 2017 and 2018, under Trump, the debt limit was increased without much fanfare.

In 2025, you have a Republican Congress and a very powerful Republican president who will demand that the crisis be avoided. (Trump wants the debt limit to be abolished, a stand he shares with Sen. Elizabeth Warren.) Democrats won’t offer to “help out,” but the debt limit has never been an issue for them.

Trump’s Big Beautiful Bill, if passed, would resolve this problem by increasing the federal statutory debt limit by $5.1 trillion. The New York Times noted on June 19:

The national debt is approaching $37 trillion. This week, Senate Republicans unveiled legislation that would raise the debt limit by $5.1 trillion, higher than the $4 trillion increase that House Republicans voted for in their bill last month. Such an increase would likely extend the nation’s ability to borrow into 2028.

An increase of that magnitude would be a record and underscore the ideological flexibility that many Republicans are willing to embrace when they are in power.

In essence, a $5.1 trillion debt-limit increase would push any future crisis out of Trump’s presidency, an idea he supports. (It also provides evidence of large U.S. deficits triggered by this bill over the next few years.) Some Republicans, including Sen. Rand Paul of Kentucky, oppose the lengthy increase. Instead, Paul suggests suspending the debt limit by three months.

The Big Beautiful Bill seems likely to gain approval, as long as nearly every Republican follows the president’s wishes. But when? Trump wants the bill on his desk by July 4, but any snag in House-Senate negotiations could delay final passage. Beyond July 4, the X-date crisis clock will begin ticking.

It would be possible to separate the debt limit issue from the overall spending bill, but that might require concessions to Democrats. If the Big Beautiful Bill stalls (it probably won’t) then emergency action will be needed.

What happens in a debt-lock?

I don’t think the U.S. is going to default on its debt, but there’s a slight possibility we will see a short-term government shutdown and disruption to government payments. No one knows exactly how this would play out.

The Brookings Institution in 2023 issued a paper titled, “How worried should we be if the debt ceiling isn’t lifted?” The authors noted that the U.S. government created a contingency plan in 2011 at the height of a similar crisis:

“Under the plan, there would be no default on Treasury securities. Treasury would continue to pay interest on those Treasury securities as it comes due. And, as securities mature, Treasury would pay that principal by auctioning new securities for the same amount (and thus not increasing the overall stock of debt held by the public). Treasury would delay payments for all other obligations until it had at least enough cash to pay a full day’s obligations. In other words, it will delay payments to agencies, contractors, Social Security beneficiaries, and Medicare providers rather than attempting to pick and choose which payments to make that are due on a given day.”

On Thursday, we saw the Treasury launch a plan to issue $250 billion in longer-term cash management bills in coming weeks. This is a logical strategy, pushing maturities beyond the potential X-date. At the same time it reduced Thursday’s 4- and 8-week auction sizes by $5 billion each.

Most likely, this all gets resolved in the next 5 to 10 days. But as the X-date approaches, we will see worsening disruptions to the T-bill market. People will begin asking: “Is the government going to shut down?” … “Will my T-bill mature and pay out on the predicable date?” … “Is my Social Security benefit payment going to be delayed?” … “Will there be a TIPS auction this month?”

The debt crisis will be resolved, either through the Big Beautiful Bill or through emergency congressional action. As an investor, I would not hesitate to invest in a Treasury T-bill, despite the potential disruption.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Implicit in the OBBB is an assumption that tax cuts and investments needed for the AI will boost the growth of the US easily servicing the new spending.

I wonder what happens to bond yields if the AI sector follows the same timeline as the Internet sector where we suffered through dashed hopes in 2000, expensive wars, and then the Great Financial crisis.

David, Did you see George Will’s column June 25, 2025 in my local newspaper? It raised my US debt, including these early sentences:

“Twenty-five percent of Treasury bonds, about $9 trillion worth, are held by foreigners, who surely have noticed a provision in the One Big Beautiful Bill (1,018 pages). Unless and until it is eliminated, the provision empowers presidents to impose a 20% tax on interest payments to foreigners. The potential applicability of this to particular countries and kinds of income is unclear…

But foreign bond purchasers, watching the U.S. government scrounge for money as it cuts taxes and swells the national debt in trillion- dollar tranches, surely think: What the provision makes possible is possible. Such a significant devaluation of foreign-purchased Treasury bonds would powerfully prod foreign investors to diversify away from Treasurys, which would raise the cost of U.S. borrowing an unpredictable amount.”

Looking forward to your insights.

Column date correction – should be June 28, 2025

For a number of years my wife and I bought new 13- or 26-week T bills at auction every week in our non-retirement Vanguard brokerage account.

Always wishing to maximize simplicity in our finances, i.e., to reduce the time and “life energy” we spend on thinking about and tending to money, we finally decided it was easier to just park all our surplus cash in Vanguard Treasury Money Market Fund. As of this writing, 4.20% SEC 7-day yield, 4.28% compound yield, expense ratio only 0.07%. We might be able to squeeze a few extra basis points of interest rate through auction purchases, but in our view it’s just not worth the bother.

https://investor.vanguard.com/investment-products/mutual-funds/profile/vusxx

I use Fidelity’s Cash Management Account for this purpose (for money likely to be spent within 4 to 6 months). This account is super user-friendly, but its base Treasury money market fund (FZFXX) is paying 3.94% currently, less than Vanguard’s. I also roll over staggered T-bills at TreasuryDirect, paying about 4.30%. I like having that secondary emergency fund slightly out of my reach, so I won’t be tempted to make an impulsive purchase.

Thanks for this explanation. I’ve been buying small amounts of Treasury bills over the last few months, and I noticed the unusual jumps in the 8-week yield in the auctions of June 12 and June 18, and then a similar jump in the 6-week yield in the June 24 auction. Meanwhile the 4-week yield has been steadily declining. It hadn’t occurred to me that these might have to do with the debt limit crisis. Now it makes a little more sense.

Just got some 26 week T-bills that mature 1/2/26. (to push income into 2026). Hope there is not another crisis / close the government which threaten the safety of this t-bill. They have always worked it out. When will the time come when they don’t work it out.

If the US defaults on its debt, it is guns, ammo, and beans time. After death and taxes, the US paying interest on Treasuries is the next surest thing in life. I am not worried. The super-wealthy will not let the global economy collapse, because it would be game over for them. Morgan and his cronies bailed out banks in the 1907 Bank Panic, Roosevelt helped get the economy going again in the 1930s, Buffet bailed out Goldman Sachs in the 2008 financial crisis.

The BBB does nothing to significantly address paying down the debt but increases the debt. Cutting a penny, When we need a $ is voodoo economics. Why is it we spend 10x on military, UDA must really be hated on the world.

Republicans only care about fiscal discipline when there is a Democratic president who they can hammer on the issue. In fact, every Republican president since Reagan (so the last 45 years) has inherited a smaller deficit from his predecessor than the one he left to his successor. Every Democratic president has left a lower deficit to his successor than he inherited from his Republican predecessor.

The reason is simple. They refuse to raise taxes of any kind on anyone to grow revenue into the federal government. That leaves them with only two of the three ways to pay down debt — cut spending and try to increase growth. Americans don’t want government spending on programs they benefit from decreased and doing so would make the Republicans unpopular and threaten their re-election prospects. That leaves economic growth, growing our way out of the deficit, as the only option. That can work, but when there’s a crisis, like the 2008 recession or the Covid pandemic, the whole strategy falls apart.

Notice I have only mentioned the deficit. The debt just continues to grow and grow as long as we run annual deficits, which has happened every year except for the end of the Clinton Administration. That was 26 years ago.

I have long maintained that the Dems ar the party of tax and spend. The Reps also love to spend – they just don’t like taxes.

I’m not so sure the Republicans in the House and Senate will be able to reconcile their differences. One particular flash point is the SALT cap. The House SALT Caucus fought for a $40,000 cap for those making $500,000 or less, and are adamant it remain as is. The Senate Republicans, nine of whom represent the most affected states with high property taxes, intentionally left the cap at its current level of $10,000 which is effectively nI’m-existent necisse of the rise in the standard deduction with inflation since 2017. While it is possible they will negotiate a compromise or the House SALT Caucus will cave, I can envision a standoff here where the Senate bill goes back to the Huse with that $10K cap and it gets voted down, causing chaos. I know it’s hard to predict the future, but any thoughts in that?

I hope it fails. There is too much in the bill and too many competing interests. I would like the Trump tax scheme to continue but not enough to want this bill to pass. So your marginal tax rate will go up 3 points. Cut back on your spending. Some people will get a lot of deductions back too and may fare better. The bill should be broken up into its various components and voted on piecemeal. Vote on the continuing the Trump tax system by itself. And as is, without caps on this and that and exempt income on this and that. The proponents of the bill will say we don’t have time for that. I would say that is the crux of the problem.

I have been willing to accept an extension of the 2017 Trump tax cuts, as is, with no changes. That was inevitable, and even just that move will increase future deficit estimates by trillions because these tax cuts were supposed to expire. Some of the add-ons — such as no tax on tips, no tax on overtime, higher SALT deduction — could be very costly as people re-adjust the way they earn money.

I have a question about the T-Bill chart. It shows a 6/26 rate for the 13-week T-Bill of 4.39%. I was a purchaser of this issue and the auction results show this:

13-Week912797PY706/26/202509/25/20254.195%4.299%

Where does the 4.39% come from in your chart?

That auction was actually June 23 and the investment rate at the auction was 4.299%. June 26 appears to be the settlement date, which is called “maturity date” on the auction results (who knows why?). The Treasury estimates in my chart aren’t based directly on auctions, but on secondary market trading, which is very active.