July 24 update: New 10-year TIPS gets real yield of 1.985% to solid investor demand

By David Enna, Tipswatch.com

On Thursday, July 24, the U.S. Treasury will offer $21 billion in a new 10-year Treasury Inflation-Protected Security, CUSIP 91282CNS6. This is shaping up to be an attractive auction, likely generating a real yield to maturity close to 2%, or higher.

The coupon rate and real yield will be set by the results of the auction, which closes at 1 p.m. EDT. But you can get a fairly accurate idea of the likely real yield by checking the Treasury’s Real Yield Curve estimates, which update at market close each day.

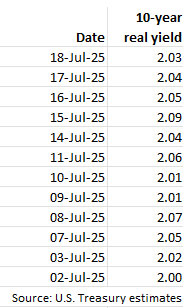

Each day since July 2, the 10-year real yield has closed above the 2.0% level, which is traditionally an attractive milestone. Anything can happen by Thursday’s auction, but a range around 2% seems likely.

This auction size of $21 billion, by the way, is the largest in history for a new or reopened 10-year TIPS. It is up from $20 billion at the most recent originating auction in January, and up from $19 billion last July.

So far, these larger auction sizes haven’t greatly affected demand. The bigger issue seems to be the market’s acceptance of longer-term Treasurys at a time of rising future deficits.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 2.03% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.03% for 10 years.

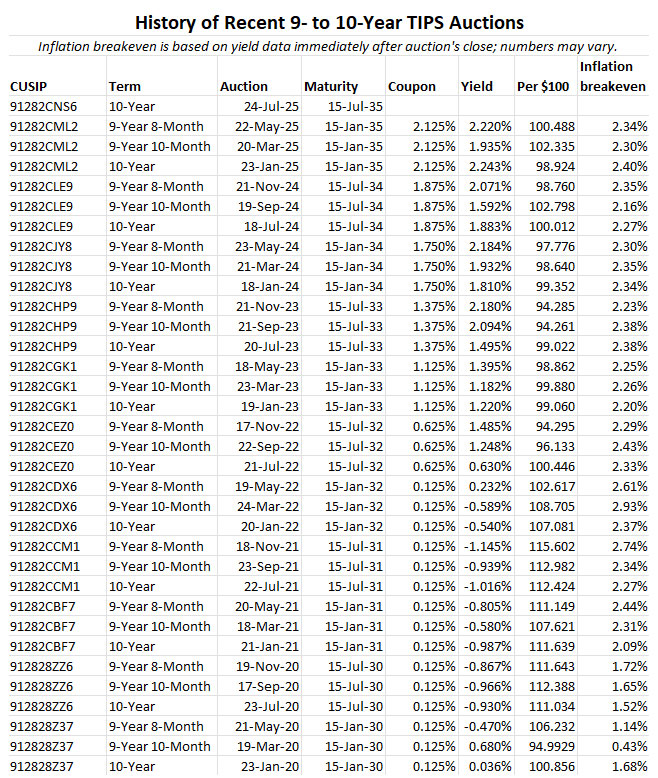

Note that the January auction of a new 10-year TIPS (CUSIP 91282CML2) got a real yield of 2.243%, the highest for this term at auction in 16 years.

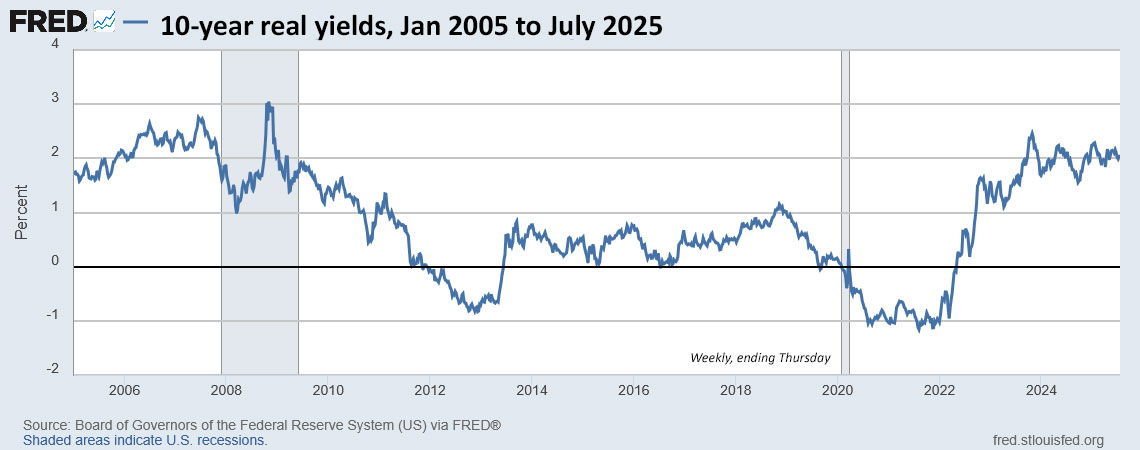

So is a real yield of 2.03% attractive? Yes, in a historical perspective. Real yields could certainly continue climbing higher, but 2% is a solid above-inflation return. Here is the trend in the 10-year real yield over the last 20 years, showing the huge gap from 2011 to 2022 when the 10-year real yield rarely exceeded 1%:

Pricing

Because this is an originating auction, this TIPS should get a price close to, or a bit below, par value. The coupon rate will be set at the 1/8th percentage fraction below the auctioned real yield (for example, 2.00% for a real yield of 2.05%), so the unadjusted price will be slightly discounted. In addition, this TIPS will have a minimal inflation index of 1.00108 on the settlement date of July 31.

In the end, the adjusted price should be close to 100, meaning the investor will be paying par value, or very slightly less or slightly more. Order $10,000 of this TIPS and you will probably have an investment cost of about $10,000.

Inflation breakeven rate

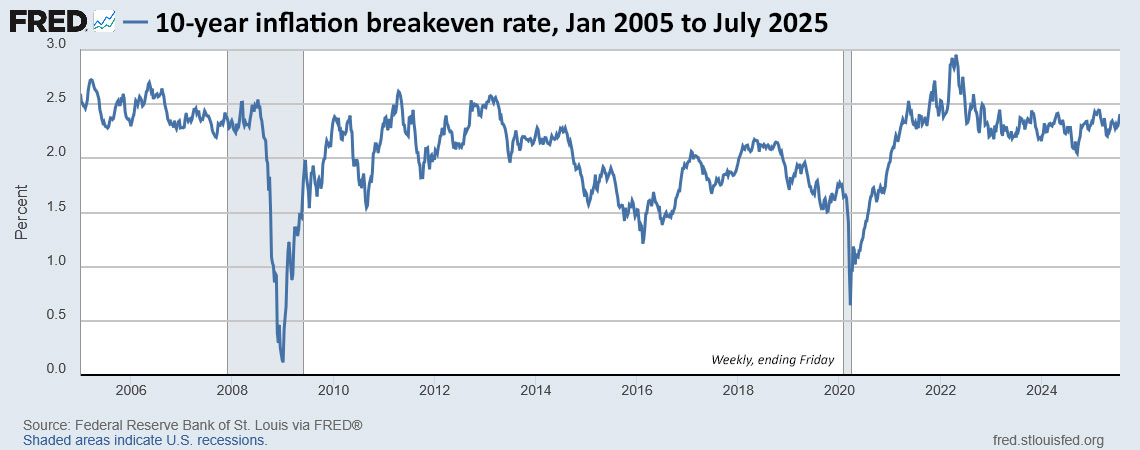

The 10-year Treasury note closed Friday with a nominal yield of 4.44%, setting up an inflation breakeven rate of 2.41%, which is higher than the result of any auction of this term going back to a May 2022 reopening at 2.61%. (But it is still well below the 20-year high of 3.02% hit in April 2022.) A high inflation breakeven rate indicates that a TIPS is “expensive” versus the nominal Treasury.

This rate is likely to change by Thursday, and I wouldn’t be surprised to see it go lower. But the market is facing a lot of uncertainty about future inflation. Here is the trend in the 10-year inflation breakeven rate over the last 20 years, showing the recent trend of breakevens in the range of 2.0% to 2.5%:

Thoughts

This is a new TIPS, so it isn’t available on the secondary market. If you want a TIPS maturing in July 2035, you can either buy at this auction or wait for later opportunities on the secondary market. (Trading in a new TIPS can sometimes be slim in initial weeks.)

I won’t be a buyer because I filled the 2035 rung of my TIPS ladder at the January auction. (The higher real yield was just luck, not a clever strategy.) Now my next purchase will be in January 2026, to fill the 2036 rung.

If the auctioned real yield maintains around 2% or above, the result will be attractive for investors who plan to hold to maturity. Real yields could go higher, but collecting 2% above inflation for 10 years is sound. (And a reminder: Investing in TIPS won’t make you rich; it is a strategy for preserving capital.)

This TIPS auction closes Thursday at 1 p.m. EDT. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi, David.

You mentioned you are not buying any July 2035 maturing TIPS because you have already filled your 2035 allocation.

Is there a reason you would not sell some of your Jan. 2035 TIPS to buy July 2035 TIPS?

I would think the advantage of having more frequent maturing funds in your ladder would outweigh what will probably be pretty trivial bid/ask spreads on the secondary market.

Anitje, long-time readers know I never sell a TIPS. My never-compromised plan is to hold to maturity. For some years, I do have several TIPS per year, but for now I am trying to focus on TIPS maturing in January for the 2036 to 2039 maturities, to make future RMD withdrawals simpler.

But selling to immediately buy one of almost identical maturity is pretty much a wash…just more or less a swap, which is different than just selling. So why do you not do that, to add more flexibility to your ladder (funds maturing more often)? Am I missing something?

As you say, it is pretty a much a wash. So why do it? I am happy with the single January maturity and I appreciate the higher coupon rate.

Nice article as usual. Thanks for it. I bought my 2035 TIPS earlier in Jan. I do have some 91282CJY8 which I had planned to sell when funding the 2035 91282CML2 but I didn’t do it. BTW – Is there a site I can add up all my TIPS and see how much would I get as an income into the future?

You could try https://www.tipsladder.com/build and upload all your existing TIPS holdings as a CSV file.

Upload pre-owned holdings from file with “.csv” extension.

Each line in the file should contain, these separated by commas:

Is that what you were looking for?

The bond desk at Fidelity said that there is a way to purchase foreign TIPS. My contact consulted the the “Capital Markets Team”. One would have to know the CUSIP. It is likely that the minimum order is 200 bonds.Fidelity does offer regular, non inflation adjusted bonds from foreign governments. Those bonds are found under the “show more criteria” features at the bottom under “foreign sovereign debt”. There are 1500 bonds available.It is always a good idea to “diversify”. I have not purchased any of those yet.

Personal opinion: Buy bonds in the currency you will be spending. That simplifies things.

I believe around 2% above inflation is good, but I also worry some more lately about the possibility of deflation.

I’m happy to have some deflation proof money in I-bonds… some getting 1.3% over inflation.

The other thing I like about the I-bonds is the 1.3% fixed rate (or others) is that the additional interest is automatically added to the principle and also becomes deflation proof.

The new TIPS look good to me if things keep going as generally expected.

BTW, Vanguard does NOT post the CUSIP for bonds at auction. I went to their website to buy the CUSIP 91282CNS6 and entered the number. While a bond that looked awfully like that popped up, it did not have a CUSIP, and was greyed out and did not allow me to push the BUY button. A call to Vanguard confirmed that their software does not download the cusip for TIPS at auction. They did confirm that the 10yr TIPS on their bond page was indeed, CUSIP 91282CNS6 but you’ll have to take their word for it. Which I’m sure is true, but no way to do business. Another case about how poorly their brokerage website compares to Fidelity’s and others. And they know it.

This morning I went to Vanguard’s bond-trading page and searched for CUSIP 91282CNS6 and found it. So maybe they had a delay in hooking it up, or your complaint got them to do it.

People can get confused in this process. I have had feedback from people who errantly bought a secondary-market TIPS instead of the auctioned TIPS. This is the way I make an auction order on Vanguard:

1. Go to the main bond trading page.

2. Click on Treasuries in the top line of links.

3. Click on the Auctions radio button.

4. Look for the TIPS in the list. There will only be one, and it will be there only within a week of the auction. Using this process ensures you get to the TIPS being auctioned.

I think we are not on the same page, literally.

Yes, by doing as you say, above, you can find the Tips auction and the upcoming bond offering. But the bond has no CUSIP attached to it, as it does on other sites, e.g. Fidelity. Vanguard admitted to me that this was a software problem. One would like to verify it is the same bond listed on the Treasury site as it does on Fidelity, which does give you the bond’s CUSIP.

The only way to verify that it’s the matching bond is to search for the CUSIP on the Vanguard site. That does, indeed, bring up the bond. But there is no way to purchase that bond from THAT dedicated page, as the purchase button is greyed out. And still is.

Now we’re on the same page, pew, or whatever I hope. Thanks for your reply.

Somehow, I was not able to post a reply to your answer so I am adding this as a new comment.

Thank you for your quick reply. Yes, my estimated portfolio value at 72 in the hypothetical example above is assuming heavy equities allocation.

While fully acknowledging that you are not a financial advisor, I’d like to continue this discussion a bit, if you don’t mind.

In my example above, the $1 Million today is sitting in IRA or 401k already. I understand that one could redirect the future contribution to Roth IRA, but we still have to figure out RMD for this $1M (which will supposedly grow to $2.65M at 72). Did you mean that you started putting aside 4% of your IRA portfolio (say, $40K in this example) once you started building your ladder? So, that means you would need considerable time to fully build out your ladder, correct?

On the other hand, if you allocated $40K for multiple years today (out of the $1M), you could potentially build the ladder beginning at 72 (20 years from now) and end at 82 (30 years from now, which is the latest maturing TIPS available today), correct? That’d be allocating $400K out of $1M today for this ladder. Also, if one allocates 40% of the portfolio to TIPS in this example, then it is unlikely to grow to $2.65 M in 20 years, so one has to keep that in mind, too. I hope you don’t mind so many questions. I just want to understand how people approach this problem when they say they are building TIPS ladder to address their RMD.

Most of my ladder was built after the surge in real yields in late 2023 and into 2024. And it was in a situation like yours with an established traditional IRA. I was at age 70, then, quite a bit older. I filled out the entire ladder in a few months, and now I am just filling the gap years of 2036 to 2039. In your case, you would start your ladder in 2045 and potentially end it in 2055. All of those TIPS are available right now on the secondary market and all have attractive real yields. (Most have very large inflation accruals, which you would need to be willing to accept.) So your plan to allocate $400,000 — $40,000 in par value per year — to the TIPS ladder seems similar to my approach. It would leave you with other investments in the IRA to continue to grow and use for potential RMDs, charitable giving or Roth conversions.

Ok, thank you for sharing your own example. You have now given me some (very good) food for thought!

Maybe if you find time at some point, you could perhaps consider writing an article in future to guide younger audience of this excellent site to start preparing themselves.

David,

How do you decide the amount of money to assign to TIPS ladder for RMP purposes? Let me explain what I mean.

Say, I am a 52 year old (15 years from Full Retirement Age, and 20 years from RMD). Let us further assume that the total value of all tax-deferred account is $1 Million today, and is expected to grow to $2.65 Million when I am 72. According to Schwab RMD calculator, it would mean I need to take $100K out each year once I am 72.

So, do I buy $100K of TIPS now (today) for each year beginning with when I am 72? If so, then I can only buy approximately 10 years worth of TIPS today. But if I do that, my portfolio is unlikely to grow to $2.65 Million when I am 72.

Please set me straight as I am sure I am missing something. Thanks,

If you are 52, I’d say look strongly at investing in Roth accounts as much as you can and bypass this problem. (I wish I could have, but my wife and I both were locked out and had no 401k option, either.) In my case, I took the total amount of my one traditional IRA and set aside 4% of the total to mature each year. In addition, coupon payments will be coming in each year from later maturities. But I gave myself a backup, with side investments in Vanguard Wellington and Vanguard Total Bond in that IRA to provide additional sources to withdraw RMDs. The one thing I don’t want to do is sell future TIPS before maturity to withdraw the RMD.

The prediction of $2.65 million is based on your current investments, which are probably fairly heavy in stocks? You are correct that a TIPS ladder won’t grow that quickly — it is just providing guaranteed, inflation-protected future withdrawals. If you built a 10-year ladder starting today for age 72, you’d be buying 20-year TIPS on the secondary market. Maybe this should just be part of your overall traditional IRA portfolio? I’m not a financial adviser, so I am just tossing out ideas.

You mention that you are 52 and 20 years from RMD. Not sure if you are just approximating, but my understanding is that those born after 1959 start taking RMDs at age 75. You may have 3 more years to work with.

Excellent point, Woody.

Yes, you are right. I stand corrected.

However, I should have clarified that I was using a hypothetical example, not my own situation, per se. My intention was to spark a discussion about the framework that one can use to build their individual ladder for RMD purposes. Specifically, the following:

A lot of questions, I know – lol. This is why I was thinking if David could write a future article about it, that’d be awesome.

Hi David, thanks for another timely post. 1. I am wondering if there is a go-to-place to get graphical representation of the daily real yield. Yes, I do get daily email from the Treasury department with the table/matrix (link) you share with us.

2. On Wednesday, July 23rd, morning, Treasury Department will be announcing potentially a significant increase in the auction of forthcoming Treasury Bill auctions. Scott B has not only continued Janet Y’s policy of more Treasury Bill auctions, but current circumstances seem to demand increasing it further. One of the goals of doing this is to reduce longer term debt and reduce long-term nominal rates. What impact you think it may have, if any, on the 10 year TIPS auction. My guess, the real yield goes lower. Your thoughts?….thanks!!!..I know these tricks can not change the inflation dynamics but they try.

1 For real-time real yields, you can use the Bloomberg U.S. Yields page. That shows current trading on the most recent TIPS (in this case, issued in January). I am looking at that now and it appears real yields are sliding lower this Monday morning (currently at 1.94%).

2 The Treasury has shown a commitment to rising levels of TIPS auctions, except for the 30-year, so that will probably continue. But in theory, reducing other nominal longer-term debt issuance *could* lower auctioned yields. Lower supply = more demand? I think Treasury is attempting to bet that new leadership at the Fed will result in lower interest rates next year. (Could happen, but iffy.)

Thanks

Cynical Me asks, a commitment to rising levels of TIPS auctions because it allows them to kick (part of) the can down the road? They only need to pay the smaller TIPS fixed rate on a semi-annual basis, unlike the greater semi-annual interest they’d pay on a regular bond.

The delayed payments could be a factor. That makes I Bonds even more attractive for the Treasury — a lower real yield and no interest outflow until redemption. The Treasury could also be gambling that inflation will be lower in the future (doubtful?).

Thanks for helping me to understand TIPS, David. I just started last year. Not sure how to figure out what the semiannual coupon could look like (roughly) as we approach the 10 year mark for a $10,000 investment of this new CUSIP at say a 2% real yield if this TIPS stays at or above breakeven. I know we invest in TIPS for the inflation protection on the principal but just trying to get an idea what the coupon might look like near maturity. Thanks

The auctioned coupon rate will likely be 1.875% or 2.0% and that will remain the same for the 10 years until maturity. But the underlying principal will grow with inflation, and that means the actual coupon payout will grow with inflation. So, what will inflation average over the next 10 years? I’d guess in a range of 2.3% to 3.0%. Over the last 10 years inflation has grown 3.1%. The 10-year TIPS that matured July 15 had an inflation index of 1.35402, so the coupon payment at the end was 35% higher.

Comparing the TIPS yield to the S&P earnings yield (2.63%) makes TIPS look even more attractive. I’ve been allocating more to bonds as the Equity Risk Premium drops.

We have sold 40% of our equities since October. Age 65, not going to wait out the next down market in equities.

I get that. My wife and I set a 35% equity position nearly 10 years ago, and we rebalance toward that when needed. Of course, the last 10 years have been mighty for stocks, except for a few months here and there. But if you feel financially secure, lowering your risk level makes a lot of sense.

Currently the farthest out I have ventured with TIPS is to Jan 2033 when I will be 83. If I bought a 10 year TIPS it would mature when I will be 87. Seems quite possible I will be around but is it a good idea?

Is there any rule of thumb or good argument for the longest dated TIPS given one’s age that makes sense?

This is a personal decision. How long do you expect to live? My TIPS ladder goes out to age 90, but I have a wife who is a half-year younger and likely to live to nearly 100. So that makes sense to me.