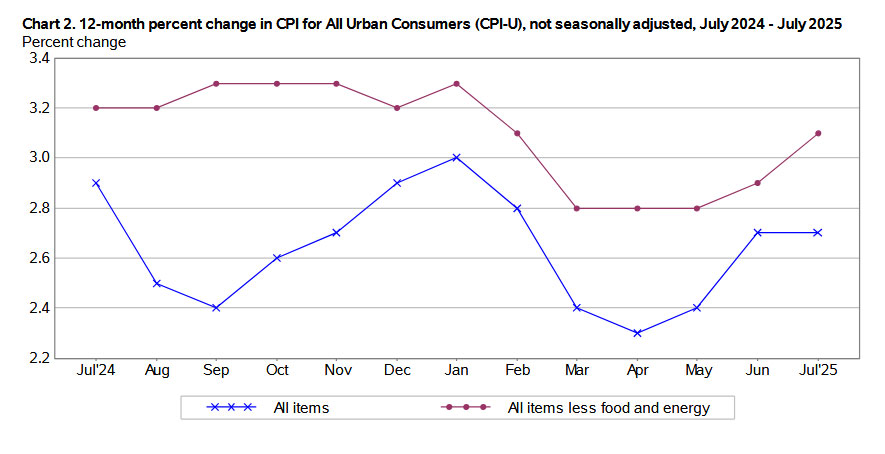

Core inflation, however, rose to 3.1% annually despite moderating shelter costs.

By David Enna, Tipswatch.com

The July inflation report offered a mixed bag of results.

Seasonally adjusted all-items inflation increased 0.2% for the month, as expected, and held steady at 2.7% year over year, less than expected. But core inflation, which removes food and energy, rose 0.3% for the month and 3.1% year over year, higher than expectations.

Core inflation rose above 3.0% for the first time since March 2025 and remains well above the Federal Reserve’s overall target of 2.0% (for a different index).

The Bureau of Labor Statistics noted that shelter costs rose 0.2% in July and were a primary factor in the overall increase in core inflation. A 0.2% increase is moderate and probably acceptable, but shelter costs over the last year were up 3.7%.

In addition, declining gasoline prices have been a huge factor in holding down all-items inflation. The gas index fell 2.2% in July and is now down 9.5% year over year. (Without seasonal adjustment, gas prices were down 0.5% in July). More from the July report:

- Food at home costs declined 0.1% and are up only 2.2% over the last year.

- The meats, poultry, fish, and eggs index rose 0.2% for the month and 5.2% over the last 12 months. The eggs index has increased 16.4% year over year.

- Costs of new vehicles were flat for the month and up only 0.4% year over year.

- Used car and truck prices, however, were up 0.5% for the month (after falling 0.7% in June) and are now up 4.8% for the year.

- Apparel costs were up only 0.1% in July and fell 0.2% year over year.

- Costs of medical care services rose a strong 0.8% for the month and 4.3% for the year.

- The index for dental services increased 2.6% for the month.

- Airline fares increased 4.0% in July but are up only 0.7% year over year.

- Furniture and bedding prices rose 0.9% but prices for appliances fell 0.9%.

From this report, it’s hard to pinpoint much effect from U.S. tariffs, which should eventually cause an uptick in prices for items like new cars, apparel, fruits and vegetables, electronics and home furnishings. The Federal Reserve is going to have some interesting discussions next month.

Here is the annual trend for all-items and core inflation, showing the upward glide of core inflation. Does this present a picture of “inflation under control”? Not quite.

What this means for TIPS and I Bonds

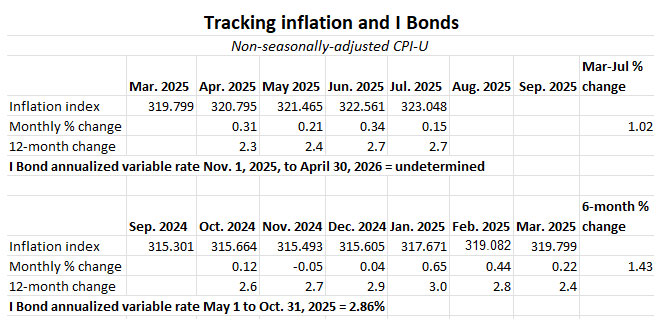

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally-adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For July, the BLS set the inflation index at 323.048, an increase of 0.15% over the June number.

For TIPS. The July inflation report means that principal balances for all TIPS will increase 0.15% in September, after a 0.34% increase in August. Here are the new September inflation indexes for all TIPS.

For I Bonds. The July report is the fourth of a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, to be reset November 1. At this point, through four months, inflation has increased 1.02%, which translates to a variable rate of 2.04%. I’d expect the next two months to bring that number up to about 2.8%, or possibly higher. Here are the data so far:

What this means for the Social Security COLA

The Social Security cost-of-living adjustment is based on an unusual inflation index – CPI-W – and is determined by averaging the indexes for July, August and September and comparing that number to the same average for the year before. For July, the BLS set the CPI-W index at 316.349, an increase of 0.13% over the June number.

With one month complete, here is where we are:

I had been projecting an increase of 2.8% for the 2026 COLA, which isn’t looking very good right now. I was expecting July CPI-W to be a bit higher.

What this means for future interest rates

Most likely, the mixed bag of the July inflation report should allow the Federal Reserve’s Open Market Committee to move forward with a 25-basis-point cut in short-term interest rates at its September meeting. More jobs and inflation data will be coming before that meeting, however.

From today’s live report from Bloomberg:

“Inflation was broadly in line with expectations as tariffs continue to be largely absorbed within profit margins. This gives the Fed the room to respond to the weaker jobs backdrop and cuts interest rates from September.” — James Knightley, chief international economist at ING. …

A 25 basis point cut in September seems to be the base case now. Can the Fed cut rates when inflation is going up? Yes, it can, as long as the tariff inflation is seen as a one-off price adjustment.

Fed officials will have plenty of time to knock down this rate-cut speculation if it isn’t accurate. Most likely they will not, which will indicate a rate-cut is coming.

An interesting side note

The BLS said: “With this release, BLS has replaced survey data collected for the CPI’s wireless telephone services index with secondary source data and non-traditional index methods.” This probably makes sense in a time of budget and staff cuts. More on this topic.

FYI, the cost index for wireless telephone services was flat for July, after a 0.4% decline in June and 0.2% decline in May.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Would you recommend buying the 30 year tips in this reopening auction?

I will be posting an auction preview article on Sunday morning. My thinking on 30-year TIPS is: Can you hold this to maturity? If so, the current real yield of 2.60% is highly attractive (but rates can keep rising). The 30-year isn’t for me — out of my age range, and it will be a highly volatile investment. Hold to maturity and that doesn’t matter.

“We are refusing to cut interest rates because, everyone I know, is forecasting a meaningful increase in inflation from tariffs, next month.”

Powell said this last month June.

So when he says “everyone I know” he must be thinking of experts, no?

That is not a direct quote, but he did say something along those lines. The full quote: https://www.facebook.com/reel/791968413172400/

Thanks!

Powell isn’t wrong in what he says. And he is in an awful pickle.

But here is my ignorant take (can’t be as wrong as the experts!)

I think we focus too much on the cost of the tariffs and not the market shifts once they play out. buyers/suppliers/sellers don’t pay more, end of story. They shop more.

Goldman Sachs just published some research on who is paying the tariffs. So far, they estimate that consumers have absorbed only 22% of the cost of tariffs. Goldman analysts said in the report that U.S. businesses have absorbed about 64% of tariff-related costs. They added that international exporters have taken on about 14% of tariff costs through June, but that rate could increase to 25%.

I made this point in a previous post on Tipswatch — yes, tariffs are a tax on consumers, but SOME of the tax is paid by foreign firms. Goldman expects that portion to settle out at about 25%. In this way, tariffs are similar to New Jersey tolls (significant portion paid by out-of-state drivers) or Florida sales tax (significant portion paid by tourists).

To be clear, this doesn’t mean tariffs are a good idea. But it is not true that tariffs are just a national sales tax or just a tax on U.S. consumers. Not exactly.

Thanks for sharing the Goldman Sachs analysis. It prompted me to read into it further, and a significant projection was left out of your summary which is important for everyone to see to get the full picture:

Goldman Sachs predicts that if recent tariffs follow the pattern of earlier levies, the share borne by U.S. consumers will significantly increase, reaching 67% over time.

Even if you use the lowest tariff amount which has been agreed to in the recent trade agreement frameworks, which is 15%, 67% of 15% is still a 10.05% tariff tax on American consumers. And in many cases, the tariffs are off the charts upwards of 100% and more.

The entire policy is based on a lie told by one man throwing around tariffs irresponsibly and indiscriminately as if they are an economic savior that foreign countries pay the tariffs. Ronald Reagan said it best.

From his April 25, 1987

Radio Address to the Nation on Free and Fair Trade

:

“You see, at first, when someone says, ‘Let’s impose tariffs on foreign imports,’ it looks like they’re doing the patriotic thing by protecting American products and jobs. And sometimes for a short while it works—but only for a short time. What eventually occurs is: … high tariffs inevitably lead to retaliation by foreign countries and the triggering of fierce trade wars… So, soon… markets shrink and collapse; businesses and industries shut down; and millions of people lose their jobs.”

FYI, you updated this link but didn’t change the “updated date”. Social Security COLA | Treasury Inflation-Protected Securities

Thank you for noticing that. It is fixed.

Trump’s pick for BLS commissioner Antoni says he disagrees with Trump, saying he doesn’t believe the BLS intentionally manipulated the jobs data. (That’s from CNN).

I see this as good news… the new BLS head is showing some independence, and gives me hope that he won’t be a total lackey and manipulate the inflation data to please Trump.

Antoni says he would like to suspend the monthly jobs report and go with quarterly reports instead, after revisions are made. This could make sense. I think a key thing to watch will be if he tries to make widespread changes in BLS staffing.

I don’t think we should get rid of monthly jobs report just when the jobs numbers may be falling. I see this as an opportunity to shield the data from Trump’s tariffs.

I don’t trust anyone from Heritage Foundation, authors of the Project 2025. So RFK Jr. convinced Sen. Cassidy to vote for him on the promise to not monkey with vaccines. So much for that.

There should be an non-partisan committee of trusted officials that looks into how to improve the jobs data, which could mean more funding for programs, greater outreach to business to get them to cooperate with the voluntary survey, and other tools to pick up hard-to-reach employment, such as the gig workers.

DOGE imposed mandatory cuts to BLS and then Trump’s proposed budget cuts another 8%. If you don’t put resources into data collection, you can’t expect accurate numbers.

Trump has politicized the BLS and therefore it will now be questioned whether we’re getting accurate data. Never before have we seen this type of outright fabrications without any proof. There must be a thorough vetting of the BLS Commissioner nominee. So far, I’ve seen no one working for Trump willing to stand up to his authoritarian moves who continues to work for the president. We cannot afford to our economic numbers questioned without paying a price in the long run.

I want to add this NY Times article to the mix. BTW, by law BLS is required to publish monthly employment data, according to several reports on news shows today.

https://www.nytimes.com/2025/08/12/business/trump-bls-ej-antoni.html?unlocked_article_code=1.d08.57op.2gs3H-FAY82f&smid=url-share

Any guesstimate on the potential fixed rate component for next reset point based upon historical… 1.1 plus/minus? Important as to locking in the “same as now” or for the Nov 1st and out timeframe for gift boxes and/or…. Thanks

I looked recently at the average since May 1 and the 0.65 ratio of the 5-year TIPS yield was hanging right between 1.0% and 1.1%. The 5-year is currently at 1.37% and if it holds around that level we will probably see a 1.0% fixed rate. I will probably post an update soon on this topic.

If the Fed lowers interest rates multiple times over the next 12 months, I think it makes I Bonds an attractive short term and long term investment. If you purchase in October, you get a return of 3.98%. If your estimate is right, you get a return of 3.9% for the following six months., inclusive of a 1.10% fixed rate. Multiple Fed rates cuts will certainly lower nominal t-bill rates below that amount within that period(how much depends on how many rate cuts we get). Do you see it developing the same way as I do?

I do see it your way, but of course Fed actions are hard to predict. Another thing to look at is that that 5-year TIPS has just a 27-basis-point advantage over the 1.10% fixed rate on the I Bond. That makes the I Bond pretty appealing as a 5-year holding vs. TIPS because of its many advantages.

I stumbled across this guy on YouTube who said the same thing we are saying now back in May.

https://youtu.be/YQpmpiie3nI?si=6UZc0xgc_gGB7UJb

I appreciate when a financial adviser talks up I Bonds.

Interesting that the increase was less than 1/2 of increase in June, yet tariffs are supposed to be increasing inflation. I guess their effect is yet to come.

I would presume some business would eat the cost short term, cut consumer choices, decrease quality and/or quantity to maintain prices. I don’t believe they will have a huge impact on inflation as the money supply hasn’t increased dramatically. I think it will decrease economic freedom and consumer choices.

I think this is essentially correct. In my opinion, tariffs are a terrible idea economically; and implementing them by using “emergency” declarations is very undemocratic.

However, their impact to prices will play out over the next several months; it will be focused on consumer spending like food, apparel, electronics, automobiles; and it will be offset by any economic downturn. In contrast to casual discussion (the price of eggs), all official measures of inflation include significant allocations to healthcare and housing – which may not be impacted to the same extent. Some tariffs are still being invented or changed (e.g. Pharmaceuticals: “In one year, one and a half years maximum, it’s going to go to 150% and then it’s going to go to 250% because we want pharmaceuticals made in our country,” Trump told CNBC in an interview.) as we bear witness to the President’s intentional chaos.

So CPI will be hard to predict – not even factoring in the dismissal of the advisory board and head of the BLS.

I often think that the main factor in interpreting “inflation” is how a person or organization chooses to look at it, almost like a “glass half-full/glass half-empty” situation.

David, in this new posting here, says it’s difficult (so far) to detect much influence from Trump’s tariffs. On the other hand, the current headline on The New York Times, whose report emphasizes the faster-rising “core” inflation number, is “U.S. Inflation Report Shows Effect of President Trump’s Tariffs.”

Neither is “wrong.” I think it just depends on what the observer finds most important or most deserving of attention, i.e., how the issue is framed.

For myself, I’ve never really been able to understand “core” inflation. I mean, I know how it’s defined, but since it’s invariably described as removing the “volatile” (that’s always the word) food and energy sectors, and since I’ve never met anyone who’s able to live without consuming food or energy, I just have difficulty understanding the worth of an “inflation” measure that, focusing on some long-term trend, intentionally excludes real-world costs that real-world regular people actually have every day.

For my purposes, all-items inflation is more relevant because it is the basis (non-seasonally adjusted) of earnings for TIPS and I Bonds. The Fed may “pretend” not to look at all-items inflation or even CPI-U at all, but it definitely feels pressure when food, energy and housing prices are soaring.

great stuff! Keep it up. Just used the tip link! Great idea

You are welcome! Thanks.