Investor demand appeared to be lukewarm.

By David Enna, Tipswatch.com

The U.S. Treasury’s auction offering of $26 billion of a new 5-year Treasury Inflation-Protected Security — CUSIP 91282CPH8 — generated a real yield to maturity of 1.182%, down a whopping 52 basis points from a similar auction in April.

The result looked on target, but demand appeared a bit weak. At the auction’s close, the “when-issued” prediction was for a real yield of 1.17%. The result of 1.182% shows investors were not diving in. However, the bid-to-cover ratio was 2.51, a routine number for this term of TIPS.

Real yields, especially for shorter-maturity TIPS, have been declining as the Federal Reserve rolls out a wave of cuts to short-term interest rates. The next cut could come next week. Here is the trend in the 5-year real yield over the last two years, showing the substantial fall from the October 2023 highs:

The real yield managed to remain 8 basis points above the current fixed rate of the Series I Savings Bond, which has a fixed rate of 1.10% for purchases through the end of this month. For many investors, the I Bond is a more attractive investment at these rates, given the advantages of tax deferral, flexible maturity, and solid deflation protection.

Pricing

This is a new TIPS, which means the coupon rate was set at 1.125%, to the 1/8th percentage point below the real yield of 1.182%. That resulted in an unadjusted price of 99.726133, a slight discount. In addition, this TIPS will carry an inflation index of 1.00148 on the settlement date of Oct. 31. With that information, we can calculate the exact cost of a $10,000 par-value investment:

- Par value: $10,000

- Actual principal purchased: $10,000 x 1.00148 = $10,014.80

- Cost of investment: $10,014.80 x 0.99726133 = $9,987.37

- + accrued interest of $4.95 (to be returned at first coupon payment)

In summary, an investor paid $9,987.37 for $10,014.80 of principal at the settlement date of Oct. 31. From that point on, the investor will earn accruals to principal matching inflation plus an annual coupon rate of 1.125%, applied to inflation-adjusted principal.

Side note for nerds: This is the first time in the history of the 5-year TIPS, dating back to July 1997, that the coupon rate has been set at 1.125%.

Inflation breakeven rate

At the auction’s close, the nominal 5-year Treasury note was trading at 3.59%, setting up an inflation breakeven rate of 2.41% for this TIPS, a bit higher than recent results. This means CUSIP 91282CPH8 will out-perform the nominal 5-year if inflation averages more than 2.41% over the next five years.

That seems like a pretty even bet, but I’ll note that inflation over the last 5 years, ending in August, has averaged 4.5%. I’d prefer the TIPS until we see evidence that inflation is actually declining.

Here is the trend in the 5-year inflation breakeven rate over the last two years:

Thoughts

Although the real yield came in 1 basis point higher than the when-issued prediction, this looks like a fairly routine auction with a fair result. The U.S. Treasury’s 5-year real yield estimate closed Wednesday at 1.24%, but a yield that high never seemed likely, as I explained here. I’d say 1.182% was a good result for investors.

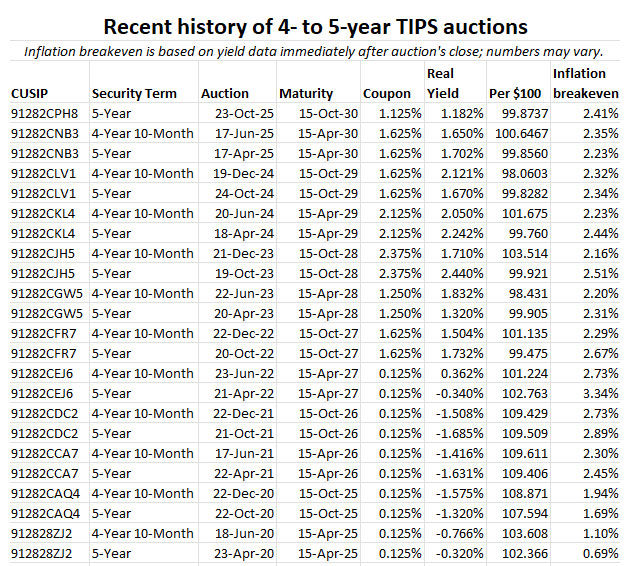

Here are auction results for 4- to 5-year TIPS over the last five years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

From above: “For many investors, the I Bond is a more attractive investment at these rates, given the advantages of tax deferral, flexible maturity, and solid deflation protection.“

I just completed a partial conversion from a Rollover IRA to a Roth IRA. With respect to the Roth IRA, I am looking at next week’s reopening auction having never had a Roth and having never bought any TIPS.

Retired, our circumstances and cashflow are such that we are more concerned with the return of our money than the return on our money, as the saying goes. Our tax-deferred and cash investments are both heavily weighted in T-Bills and I-Bonds and I’m okay with that.

With reference to the above quote from David’s post, in the case of our Roth account I-Bonds are not an option. Further, flexible maturity is not a concern for the 5-year horizon and the amount we are contemplating investing.

However, I suspect I do not fully understand the deflationary scenario.

My take is that we could realize a final yield less than the coupon due to the principal value being reduced in the future. However it would seem that under an extreme deflationary scenario we might actually do quite well given that we would receive our full principal at maturity.

But, I’ve been wrong before and I’m here to learn.

I’m also quite unclear on how the auction being a reopening might affect things, (price paid?), and the associated (perhaps crystal ball) impacts on the TIPs performance at maturity.

I’d appreciate if anyone were willing to expand concerning the deflationary scenario, and how reopening auctions operate.

The equation has changed a bit since this article, with the current I Bond fixed rate falling to 0.9% and the current 5-year TIPS real yield rising to about 1.43%. So the 5-year is looking better by comparison. I have written in the past advising investors to avoid getting fixated on long-term deflation, which is extremely rare: https://tipswatch.com/2024/06/23/dont-over-think-the-potential-threat-of-deflation/

I will be posting a preview article on the Dec. 18 auction on Sunday morning, Dec. 14. Pricing shouldn’t be much of an issue because the higher real yield should result in a discounted price at auction. I consider this 5-year term to be a very safe investment, if you can hold to maturity.

Many, if not all, of your informative posts are followed by some links to other posts such as “Tips in Depth” or “Confused by Tips”. They are still perfectly topical with the arguable exception of “Now is an Ideal Time to Build a TIPS Ladder”. As a longtime reader I know that post dates from 2023 when yields across all maturities were aligning at 2%, but I am thinking a newcomer to your blog might be confused by that title being so prominently displayed.

You raise a good point. I have thought about dropping that link in new TIPS articles. But I will note that that real yields remain above 1.0% for 2028 to 2033, above 1.5% for years 2034 to 2040, and above 2.0% for years 2041 to 2055. So it is still a decent time to build a TIPS ladder.

Hi David,

Interesting development at TreasuryDirect – C of I (Certificate of Indebtedness) might be going away. I received an email from Treasury Direct to redeem my C of I balance as changes might be coming. I use that as staging when I want to combine or break certain investments before reinvesting. You can read the full email they sent me here at treasurydirect’s webpage itself.

https://www.treasurydirect.gov/savings-bonds/emailcofi/

I guess, soon, we won’t be able to use it to hold temporary cash there.

Thanks. I will post an article on this Sunday morning. So much news right now!

Turbotax aggressively opposes any actions that would allow the IRS to make filing tax returns cheaper or easier; maybe this reflects lobbying by Wall Street to make TreasuryDirect less attractive as a competitor to brokerage accounts.

uukj, that could be true. I feel like Treasury is trying to reshape TreasuryDirect to reflect more accurately the reasons people invest there (and also to cut costs). Big-money investors don’t use TreasuryDirect to buy TIPS or bonds. It is the only place to buy savings bonds, however, so that is a unique purpose.

fyi. Gene Ludwig (worth googling the Ludwig Institute), writes the following, summarized from Bloomberg interview:

Ludwig noted that 2023 marked the highest annual TLC increase since 2001. The CPI rose 72.1% over this period, compared to 97.4% for the TLC. In addition, 2023 median weekly earnings for full-time workers as reported by the U.S. Bureau of Labor Statistics rose 5.4% before adjusting for inflation. However, when adjusted using the TLC, earnings fell 3.6%, compared to an increase of 1.3% when adjusted using the CPI.

Thought this might be of interesr to readers.

I have to admit I was baffled by your comment. TLC stands for “true living cost” and here is the complete article you reference: https://www.lisep.org/content/everyday-costs-double-the-pace-of-inflation-according-to-ludwig-institute-report

Inflation is personal to your own spending. No doubt low and middle income have been impacted more, but neither TIPS nor tax brackets or such are indexed to alternative indexes. Accordingly the alternative index is irrelevant except in the context of politics (which may be important but isn’t the focus of this website).

That said, people adjust. They make substitutions, they stop spending on some things. Alternatives appear, like streaming. They can focus on making more, or spending less, or spending more knowledgeably. Change is the only constant, and we all have to adapt.

Correct. My point is that potential purchasers of inflation indexed bonds should be aware that the cpi is not the only inflation measurement, and be aware that over time the cpi may disappoint. There is no perfect inflation hedge out there and the best an imvestor can do is to diversify broadly and hope. That said, I own substantial TIPS and I Bonds within my portfolio.

Your writings are extremely informative. Kudos to you.

Many of us have a gut feel that might be back up by statistics that official inflation understates experienced inflation. Using these numbers, “official” was 2.5% and “real” was 3.15%.

So how can we use these numbers? When building a TIPs ladder, we can build in a slight ramp in the target income, increasing it by 0.65% each year. In my case I was expecting to need CPI + 1% for that layer of my retirement funds. For example Instead of buying TIPs that will produce $10,000 in 2025 dollars in 20 years, I have $12,500 for that year.

If I understand you correctly, then I agree with your point. If your goal is solely to keep even with inflation using TIPS, and you believe the CPI understates inflation, you need a real rate high enough, that together wth the variable rate equals the rate of inflation. If you want to do better, you either need a higher fixed rate, or a diversified portfolio that includes stocks that, over time, appreciate above and beyond the rate of inflation. Is this the point you are making?

Steve: Yes I think we are in agreement. You can make up the difference through real rates of return on the TIPs, or just getting extra long term TIPs. I prefer to have more in the inflation adjusted TIPs, so that the entire layer tracks inflation+. I call it a layer (like a cake) with SSI and TIPs as the foundation covering needs (food, medical, utilities, property tax), then other fixed income bond ladders (paying off the low fixed rate mortgage) and then equities (for the wants).

This is a healthy discussion! I have tracked my expenses forever, and in aggregate, they don’t support significant understatement of inflation – for me. Some expenses go up, others go down, some are new, some go away. But that is me and my spending.

If the understatement is small, the real yield on TIPS and the fixed rate on I bonds solves for any understatement. A positive real yield means your dollars more than keep up with CPI.

TIPS and I Bonds are less wealth builders, than they are wealth maintainers.