By David Enna, Tipswatch.com

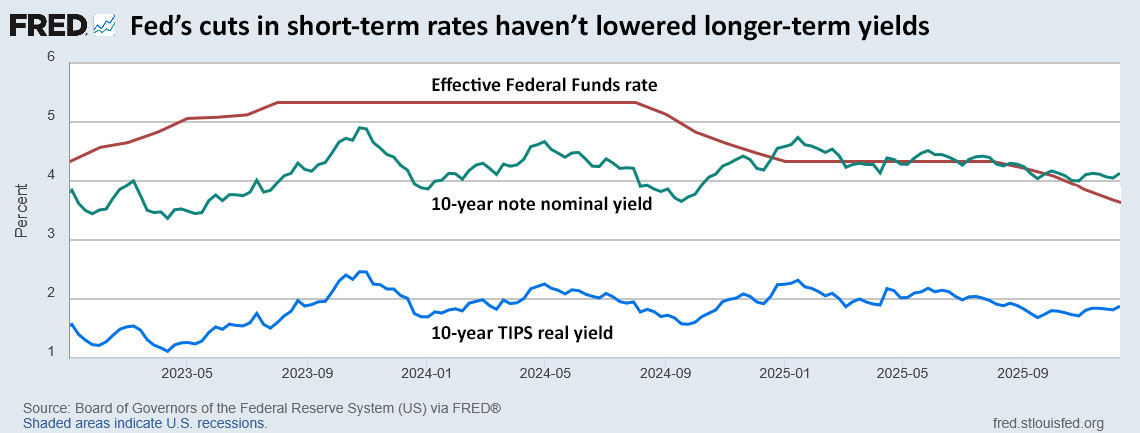

As the Federal Reserve continues on a path toward lower short-term interest rates, the bond market isn’t tagging along. Instead, yields on medium- and longer-term Treasurys have been increasing, not falling.

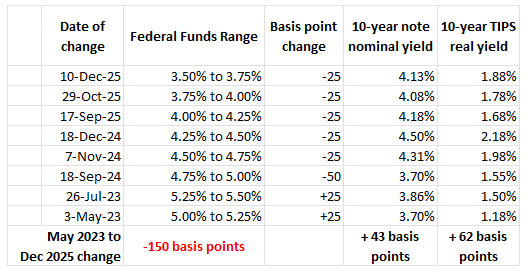

The Fed began its latest phase of rate-cutting on Sept. 17, 2025, and has now cut the federal funds rate by 75 basis points over the last four months. That has brought short-term rates down, but has had no effect in lowering longer-term rates:

Update: In a Thursday auction, one day after the Fed rate cut, the 4-week T-bill got an investment rate of 3.670%, down from 3.742% last week. That 3.67% is probably close to the new short-term T-bill benchmark. On the same day, a reopening auction of a 30-year Treasury bond got a high yield of 4.773%, up from 4.694% last month.

Here is a view of 10-year real and nominal Treasury yields over the last three years, during a time of 1) Fed rate increases, 2) then stability, 3) then cuts. Since September, both real and nominal 10-year real yields have remained relatively stable, even as the Federal Reserve was cutting short-term rates.

And this final chart shows that both 10-year nominal and real yields are up strongly since the Fed ended its rate-increasing cycle in mid-2023. The Federal Funds rate has fallen 150 basis points since May 2023, but both real and nominal 10-year yields are up, fairly dramatically.

Why is this important?

The market yield on the 10-year Treasury note is a key benchmark in the U.S. economy, forming the basis for mortgage rates and business loans. Normally, when the Fed cuts short-term rates, you’d expect to see longer-term yields move in that direction. That isn’t happening in 2025.

Why? One key reason is that the bond market sees U.S. deficits continuing to rise, possibly dramatically, over the next five years or longer. It’s a long-term trend, and it is escalating. When President Trump took office on Jan. 20, the U.S. government debt stood at $36.22 trillion. As of last week, that number was $38.39 trillion, according to the U.S. Treasury’s “Debt to the Penny” reports.

Another factor is inflation expectations. The Federal Reserve yesterday projected PCE inflation (which generally runs lower than headline CPI) to continue at 2.5% through 2026 before falling to 2.1% in 2027 and 2.0% in 2028. That looks like an overly optimistic forecast to me and the bond market seems to agree. The 5-year inflation breakeven rate closed Wednesday at 2.32%.

From a Bloomberg report on Dec. 7:

The bond market’s reaction to the Federal Reserve’s interest-rate cuts has been highly unusual. By some measures, a disconnect like this, with Treasury yields climbing as the central bank lowers rates, hasn’t been seen since the 1990s. …

But one thing is clear: the bond market isn’t buying President Donald Trump’s idea that faster rate cuts will send bond yields sliding down and, in turn, slash the rates on mortgages, credit cards and other types of loans.

Jim Bianco, president of Bianco Research, told Bloomberg the higher yields are a signal that bond traders are worried the Fed is cutting rates even as inflation remains stubbornly above its 2% target and the economy keeps defying recession fears.

“The market is really concerned about the policy,” said Bianco. “The concern is that the Fed has gone too far.” If the Fed continues to cut rates, he said, mortgage rates will go “vertical.”

And of course there is the issue of the Fed’s independence, which hangs over the bond market. Chairman Jay Powell will be gone in May, most likely replaced by Trump’s chief economist, Kevin Hassett, who has advocated for Trump’s policies on tariffs and lower interest rates. At this point, it looks like the Fed’s Open Market Committee is deeply divided over future rate-setting. That looks likely to continue.

The bond market is sending a message: The Fed can control short-term interest rates, but the market determines longer-term rates, unless the Fed launches another round of aggressive quantitative easing. (Opinion: that must not happen.)

So I would expect mid- to longer-term real and nominal yields to remain attractive into 2026, even as yields on savings accounts and money markets begin to fall.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi David, I understand that I-Bonds can be transferred to another person, taxes up to that point being paid by the giftor, and then the recipient is responsible for taxes from that point forward.

I just had what may be a crazy idea, but I’m thinking it might be permitted. My wife and I each have 1998-2001 era I-Bonds in our Treasury Direct accounts listing each other as co-owners. I’m wondering if I could transfer some of the I-Bonds in my account to her account and she could transfer some in her account to my account, pay taxes on say $52,000 in interest this year and another $52,000 next year in order to avoid paying taxes on $135,000 of interest per year beginning in 2028.

Maybe this would be more allowable if we remove our names as co-owners prior to a transfer; maybe it doesn’t matter; or maybe since we file joint returns it wouldn’t be allowed.

What do you think?

Thanks.

I am not a tax expert, so I have no idea of an answer. I would suspect that if you file a joint return, all proceeds would be taxed together in that one return. Could you simply redeem one third in 2026, one third in 2027 and one third in 2028? My wife and I have a large allocation maturing in 2031 and we will redeem them over five years, beginning next year. Read this if you haven’t seen it: https://tipswatch.com/2024/02/04/long-time-i-bond-investors-face-a-tax-time-bomb/

LOL – One thing I have learned in a fairly long life of investing is that no one knows where interest rates are going, and if they say they do, they are frequently wrong.

Prognostication is for sure one of the most ancient human rackets that never goes away and seldom goes as predicted.

I believe your forecast of enduring human credulity has merit.

Loss of global confidence in the US Dollar

I wonder how much the threat / promise of QE/YCC is holding down the long-dated yields currently?

I think it sort of has a similar effect to the infamous “fed put” on the stock market. This is a “fed put” on the Treasury market. I would anticipate that under most conditions, QE/YCC policy will be implemented somewhere in the 5%-6% 10yr yield range, if not before.

Thanks for the post, David, which was very informative, and thanks for all these comments, which I had to read 3 times to sort of comprehend what might be going on now and in the future!

Inflation has really been ok ex-housing, which is more of a lagging indicator. M2 hasn’t gone wild. Cutting rates some in that environment has felt entirely appropriate, though we should go nowhere near to as far as Trump wants.

Don’t love the pivot back to QE though – that can certainly spark inflation again.

An informative hearing yesterday: https://www.hsgac.senate.gov/hearings/the-feds-big-bank-welfare-program-oversight-of-the-feds-iorb-regime/

Bigger driver of debt continues to be Congress (and those of us who vote), but current Fed policy isn’t helping.

I guess that means mortgage rates won’t be decreasing very soon either.

Thanks for the post.

Perhaps they’re going the wrong way. Between 2004 and 2006, the Fed raised the rate 17 times. Long term rates actually declined.

In those years, inflation was running at 4%+ but I don’t think the Fed had yet set a 2% annual goal. The 10-year note yield was typically in the 4.5% range in those years, just barely above the inflation rate.

When President Trump took office on Jan. 20, the U.S. government debt stood at $36.22 trillion. As of last week, that number was $38.39 trillion, according to the U.S. Treasury’s “Debt to the Penny” reports.

Grade F – – – – –

And that’s with taxing American consumers more via unprecedented tariffs passed along down the chain that we were told would be paid by foreign countries. But keep this tax cuts skewed to the wealthiest donors coming and ignore consumer confidence and all the anecdotal evidence of ordinary Americans struggling to make ends meet.

Sorry for the snark, but the schtick is tired and the reality is getting worse — except for the stock market.

We shall see what the yields will be for the upcoming 5 and 10 year Tips reopening auctions.

I am planning on being a buyer for the 10 year Tips bonds on 22 Jan. I’m just not comfortable buying from the secondary market on Vanguard. I don’t understand the lingo of bid, yield and how it will apply to my purchase.

I will have to learn how it all works.

Thank you for providing so much info on TIPS and Series I Savings Bonds.

I will also be buying at the Jan 22 auction, which has been my yearlong plan. I will be posting a preview of the 5-year auction on Sunday morning, and then a preview of the 10-year on Sunday, Jan. 18.

As I am fairly new to secondary market purchases and TIPS in general, I wasn’t sure of the lingo and how purchases worked. I’m very comfortable with secondary market purchases now. I primarily focus on the real yield and can see the exact amount I will pay before clicking “Buy”. Accounting for various costs in a taxable account adds some complexity, but the overall purchase process is simple. Since I plan to hold to maturity, real yield is key for me.

I also plan to buy new 10-year TIPS at January auction, unless real yields change a lot.

Brace yourself, David! It is hard to imagine that we will not have QE3 before the end of Trump’s term. That should make positions in long term bonds (temporarily) quite profitable.

Unfortunately, I also think this is a strong possibility.

Why “unfortunately”?

Mango, QE in the form of large purchases of longer-term bonds is market manipulation, where the Fed is openly competing against investors, so investors don’t get the returns they deserve. It enlarges the money supply, forces yields lower, and can potentially trigger inflation.

It seems we may be there already. Quantitative Tightening (QT) has just been ended and something called “reserve management purchases” (RMP) initiated. As I understand it, this is only at the short end, for Tbills, and is therefore officially contrasted with Quantitative Easing (QE), which is across the rate curve. Not sure what it all means, but it doesn’t sound good. The first linked commentary: “You got to understand what forced this decision: the banking system was showing its cracks. Regional banks were struggling with liquidity. Overnight lending markets, a mess-even Treasury market, where the government borrows money, started acting weird.”

QT is Dead, The Next Wave of the Fed’s Quantitative Easing – The Stillman Exchange

Federal Reserve Unveils T-Bill Buying Spree, Signals New Era for Market Liquidity | FinancialContent

I found this post to be persuasive for the view that QE is not here yet.

https://wolfstreet.com/2025/12/11/why-the-feds-reserve-management-purchases-are-not-qe/

I heard Powell explain that this RMP bond-buying was more about building reserves than attempting to manipulate interest rates. The Fed already has control over short-term rates, so this doesn’t seem like a problem.

Sure sounds like QE to me even if not directed at easing rates.

I’m not convinced by the explanation at wolfstreet.com

Look at the graph posted there, we are still at 3 times the level of 2003-2008.

On December 11th The Federal Reserve’s board of governors voted unanimously to reappoint 11 reserve bank presidents to new five-year terms beginning March 1, 2026 (per WSJ). That includes the governor that has been voting for a 1/2 point cut. I think this takes off the table the worst kind of manipulation that could have resulted in a poorly executed QE3. Imagine if some or all had been replaced with people more inclined toward very low long term rates. It may still happen, but I don’t see a clear path to that in the immediate future.

Thanks for this alert, which is actually big news. It will eliminate the administration’s ability to do wholesale replacements. Here is a nonpartisan announcement: https://www.federalreserve.gov/newsevents/pressreleases/other20251211a.htm

Stephen I. Miran, who preferred to lower the target range for the federal funds rate by 1/2 percentage point at the last two meetings of the Federal Open Market Committee, is NOT a Federal Reserve Bank President. He is a Federal Reserve Board Governor.

The FOMC is made up of 7 Federal Reserve Board Governors, the President of the New York Federal Reserve Bank and 4 other Federal Reserve Bank presidents who serve on a rotating basis.

Governors are appointed by the President and confirmed by the Senate. Federal Reserve Bank Presidents are chosen by the local Federal Reserve Bank board of directors.

Correct. As I said, and to be specific, Governor Miran, voted unanimously with the other Governor’s to reappoint the 11 reserve bank presidents.

It could have gone differently.

Our political system – both sides – cannot make the decisions required to bring down the federal debt. The hope is that we grow economically out of it.

QE3 will come – whether this administration or a future Democratic one – if long term rates continue to rise. We cannot fund the nation with high long-term rates. So the political establishment will print more USD and buy debt to lower rates.

Just look at Japan. We can easily do it.

This was a clever end around the administration. Powell remaining on the Fed Board once his chairmanship ends, if he breaks with past practice, would also help with independence.

Still, SCOTUS has yet to rule on two cases, and there are other means to pressure those who don’t do the administration’s bidding (see Marjorie Taylor Greene; see the recent lawsuit that threats to judges are influencing decisions), so the game isn’t over, it just changes.

Another great article!

The long view and the short view.

Totally agree. Love Mr. Tipswatch! My go to resource.