By David Enna, Tipswatch.com

U.S. Series I Savings Bonds are a unique investment because all interest is rolled into principal until redemption, and in most cases, all the compounded earnings are tax deferred until the I Bond is redeemed or matures.

This is good.

And no I Bond has ever matured. I Bonds were first issued in September 1998, so history’s first I Bond maturity will come in September 2028. These early-issue I Bonds from years 1998 to 2001 had incredible fixed rates of 3.0%+, meaning they have generated fantastic returns over the years, in the range of 6.0% to 6.25% annual interest, compounded.

This is good.

What isn’t good?

A rather large tax bill is coming for investors in these early-year I Bonds. When the I Bonds are redeemed or mature, the entire amount of interest will be subject to federal income taxes in that year. (I Bond interest is not taxed at the state level.) Some people might say, “Nice problem to have,” but break-through amounts of income can trigger a series of harsh tax consequences: higher marginal brackets, Medicare surcharges, phase-out of some deductions, and the 3.8% Net Investment Income Tax.

The amounts can be seriously hefty: When I Bonds were first created in the fall of 1998, the purchase limit was $30,000 per person per year, and the Treasury even allowed credit cards to be used for purchases with no fees. (Air miles!) This means couples could buy $60,000 in I Bonds each year in those early years.

This chart shows how a $10,000 investment has grown for each of these early I Bond issues, from September 1998 to November 2002. Investors who purchased $20,000 in a year would need to double these amounts; if the purchase was $60,000 for a couple, multiply the amounts by 6.

Couples who bought $60,000 in I Bonds in November 1999 have already earned $193,896 in interest and that amount could easily grow by another 30% at maturity in November 2029, figuring annual interest of around 6%. That brings the total interest to $252,065 in 2029. Ouch.

This is an extreme example, but I have heard from many readers who did indeed buy $60,000 a year of I Bonds in the early years. That has been a great investment, but the coming tax bill causes worries.

My own example: 2031 is a problem

Many readers have been encouraging me to write on this tax issue, but I’ll admit I have been ignoring it. I figured the problem was years away, and my wife and I could handle the influx of taxable interest by adjusting other income sources in the years of maturity. I had no intention of redeeming my high-fixed-rate I Bonds … until maturity.

But then I took a closer look.

I knew we had $40,000 in early-year I Bonds with high fixed rates, but I didn’t realize that all of our purchases were in the single year of 2001, meaning they would all mature in 2031. Hmmm … problem.

Let’s look ahead to 2031. Both my wife and I will be collecting Social Security, a pension, possibly an annuity, and drawing RMDs from traditional IRA accounts. This $144,700 of extra income would very probably push us into a higher tax bracket, high Medicare surcharges and trigger the 3.5% Net Investment Income Tax. Plus, it is possible that tax rates will be higher in 2031.

What’s the plan?

Reluctantly, I am going to give up the idea of holding these high-fixed-rate I Bonds until maturity. Now my plan is to redeem one-fifth of the total each year from 2027 to 2031, bringing the interest income to maybe $28,000 a year, an amount we can deal with by adjusting other sources of income (such as IRA withdrawals).

In our case, these are still paper I Bonds, stored in a bank’s safety deposit box. I looked into the box recently and double-checked. There are 40 $1,000 I Bonds, all issued in 2001. Because the denominations are each $1,000 original value, it will be simple to redeem eight a year for five years, 2027 to 2031.

The denomination is important because paper I Bonds have to be redeemed in whole, unlike electronic I Bonds, which can be redeemed in $25 increments. TreasuryDirect says: “You cannot cash part of a paper savings bond. A paper savings bond must be cashed for its entire value.”

My bank (Wells Fargo in Charlotte) still redeems paper savings bonds, but some banks no longer offer that service. TreasuryDirect says, “Banks vary in how much they will cash at one time – or if they cash savings bonds at all.” From a recent New York Times article:

Hoping to cash in a paper savings bond that’s been lying around for a few decades? Set aside a lot of time for disappointment. …

The process is only getting harder. In May, the nation’s largest bank, JPMorgan Chase, began imposing a $500 limit on each savings bond cashed for longtime depositors — that’s total redemption value, so including any interest owed. Wells Fargo and Citi place a $1,000 limit on new customers. U.S. Bank has a five-year waiting period before it will cash a bond for a new customer.

Converting paper to electronic

Because banks are balking at redeeming savings bonds, especially in large dollar amounts, another option would be to act now to convert these paper I Bonds into electronic form. This isn’t simple, of course. My wife recently converted a batch for her mother, and the process was tedious and time-consuming. But it worked.

To do this, you must have a TreasuryDirect account (if you are reading this I am sure you do), and then you will have to create a Conversion Linked Account where the converted I Bonds will reside. This page on TreasuryDirect has answers to a lot of questions on this procedure.

Harry Sit of TheFinanceBuff.com wrote an excellent guide to conversions, which you can read here. He notes:

In the usual government fashion, they don’t make it easy. Treat it as a test for how well you’re able to follow instructions.

Once converted, you can go into TreasuryDirect and adjust the ownership registration, if needed.

You can find another guide to the conversion process in this May 2022 article on the my site: “Ready to convert paper I Bonds into electronic form? Here’s a step-by-step guide.”

It is not a fun process and that is why I am hoping my wife will do it for us: She has experience!

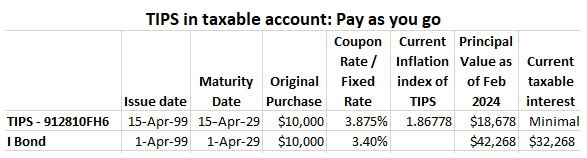

Do TIPS face this same tax problem?

Absolutely not. For example, in April 1999 I bought $10,000 par of a 30-year Treasury Inflation-Protected Security in a taxable account at TreasuryDirect. Let’s look at how it now compares with an I Bond purchased in the same month:

This one chart dramatically shows the difference between investing in a TIPS, which pays out the coupon rate biannually, versus the I Bond, which continuously rolls interest payments into principal all they way to maturity. So even though the TIPS has a higher fixed rate of 3.875%, its current value reflects only inflation of 86.7% over the last 25 years. All the earlier coupon payments — the real yield over inflation — have already been paid out.

Plus, because of the way TIPS are taxed, with inflation accruals getting taxed in the current year, when this TIPS matures on April 15, 2029, there will be only a small amount of tax due — on 3 1/2 months of inflation accruals and the final coupon payment of 1.9375%.

A TIPS held in a taxable account does not create a “tax time bomb.” You pay the taxes as you go. At maturity, taxes are pretty much a non-event.

One more point: The chart demonstrates the benefits of compounded, tax-deferred interest when an I Bond has a very high fixed rate. That April 1999 I Bond is still earning 3.4% above inflation on compounded principal of $42,268. There is no way a TIPS investor could have earned that yield by reinvesting coupon payments in an equally safe investment from 1999 to 2024. For most of that period, real yields have been below 2.25%.

Final thoughts

If you were one of the fortunate investors to have invested in I Bonds in the early era of 1998 to 2001, congratulations. Now you should take a careful look at your investments and the potential tax consequences of holding to maturity. You will be paying taxes, of course, but you may be able to manage the redemptions to minimize effects on your tax bracket, potential Medicare surcharges and the looming Net Investment Income Tax.

You have time to create a plan because the first-ever I Bond maturity won’t occur until September 2028.

• I Bond buying guide for 2024: Be patient

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: How I Bonds Are Taxed: 8 Scenarios You Should Know - Life With Grit

so, dumb question but do you pay tax on the increase in principal value (like one does with a TIPS in a taxable account) ?

eg for your I-bond above March 1, 2031, if you sell it what will the cash-out value be? $57k + $77k , so you pay tax on just the deferred interest or ?

With an I Bond, the investor can defer all taxes until redemption (which the great majority of people do) or pay on the interest earned each year (this is a bit of a do-it-yourself project, keep good records). So yes, all interest earned is eventually taxable, unless you use the I Bond for educational purposes under certain rules.

An additional bit of information that might be helpful . . . it is my understanding that if you hold more than one savings bond you have to treat the interest the same with all of them.

That is, if you defer interest on one bond you have to defer on all of them. You cannot cherry pick which ones to defer and which to accrue — like the Musketeers: All for One and One for All.

My understanding is that there is no increase in principal value; the difference between the purchase price and the ending value is entirely accrued/compounded interest.

That’s not quite correct, but yes the amount above the original investment is taxable. Principal continues growing and is higher for future interest payments.

This article along with a lot of the feedback provides convincing support to NOT get paper bonds with your tax refund. Of course if you already have them then converting to electronic form as soon as possible seems like the best choice.

May I ask, how you made the decision? Consulting someone or running Software for some trade offs?

I inherited some I-bonds. Currently approaching 60, have $800 / month premium tax credits, that it looks like I will lose after 2025, when my I-bond deferred interest would be highest. I could split it up and take 1/3 in 2024 and 2025 , since there is not ACA cliff till 2026 , etc .

I looked at the raw numbers where the I-bonds make 6% interest for 4 years vs the loss of $10k/APTC ,

and don’t see how to make the decision.

I don’t totally understand your situation, but if the I Bond interest would disrupt your ACA health coverage, you’d probably want to redeem and pay the tax in earlier years. I don’t know anything about the ACA rules.

thanks for the reply. ACA has a “cliff” that has been temporarily postponed. Whereby, after a certain amount of Income, one loses all APTC, (advanced premium tax credits), Unless congress does something this cliff will be reinstated for tax year 2026.

So, theorhetically, I have 2024 and 2025 to cash out some I-bonds and not lose the credits, if I do not, then in 2026 , I will have no APTC.

My biggest lump of deferred income will come at age 63 otherwise.

Mostly, I am asking how you crunched the numbers

It’s not a matter of number-crunching for me. My wife and I have a set taxable income goal for each year (based on tax rates and Medicare surcharges). We need to make the I Bond interest fit inside that goal. So spacing out redemptions makes sense.

how does one make that decision? using some particular software?

I’m in the same situation, but also receiving ACA tax credits for another 6 years. Seems complicated enough that I’m inclined to not even try to crunch the numbers.

The author overlooked one other modified option – hold some iBonds till January 2032. If some were bought in November or December 1991, then one or two months of interest are lost. But an extra 5 years of 3% + inflation are gained !

Taxes are due for the year cashed in. So an iBond that matures in 2031 is not taxable that year unless cashed in.

And it is possible that the Treasury will allow a rollover as they once did from Series E to Series HH savings bonds. Holding some iBonds till 2032 expands that opportunity to convert (if the Treasury dies so).

Not sure of your theory here, but I will remind everyone that technically, the IRS says taxes are due in the year the savings bond matures.

It will be good to find an answer because this would mean that an additional penalty for late taxes can be expected for anyone holding a bond past maturity. If that is true, it is unexpected. If the matured bond is not cashed, then it is not income in the year.

If I stick my last 3 monthly paychecks of the year in a drawer and deposit them in January, are they not income in the year received? Asking for a friend.

The IRS says the taxes on an I bond are due when cashed, in before maturity OR at maturity. Seems pretty clear.

Yes. IRS: “Report all interest on any bonds acquired … when the interest is realized upon disposition, redemption, or final maturity, whichever is earliest.”

With regard to cashing of fully matured bonds TD says, “The interest earned is reported to the IRS for the tax year of the redemption.”

It does not seem like it is necessary to pay taxes on matured securities which have not yet been paid.

Your company will report the income to the IRS on Form W-2 in year the check is dated. Deposit the check when received.

Wage income is taxable upon receipt.

I reported less than 1099 income when a check was written on 12-28, mailed 12-29 and received in early January.

In my return, I included a copy of the check & postmarked envelope in my return with a note saying I received it the following year.

No problems.

“The author overlooked one other modified option – hold some iBonds till January 2032. If some were bought in November or December 1991,”

I think there must be a typo in here somewhere. The first I-Bond wasn’t issued until 1998, so none could have been purchased in 1991. They only earn interest for 30 years, so holding longer than that would seem to be of no further benefit, in addition to the possible tax penalties mentioned by others if held into a later tax year than that in which they reach maturity.

Link to IRS website below. They say taxable in the year cashed. Which is consistent with how cash basis taxpayers are treated on other issues.

https://www.irs.gov/faqs/interest-dividends-other-types-of-income/savings-bonds/savings-bonds-1

They say “in General”. Look at Topic number 403 “Interest Received” It says “Savings bond interest – You can elect to include the interest in income each year, but you generally won’t include interest on Series EE and Series I U.S. savings bonds until the earlier of when the bonds mature or when they’re redeemed or disposed of.”

Exactly right! People who hope to circumvent this by not cashing in matured bonds are in for a rude awakening.

Your IRS link is to a FAQ that answers the question, “I cashed some Series E, Series EE, and Series I savings bonds. How do I report the interest?” Therefore the answer is working from the point of a bond that has been cashed in rather than held. It does not address the situation you propose.

Doug, the IRS Publication 550 says, “Report all interest on any bonds acquired … when the interest is realized upon disposition, redemption, or final maturity, whichever is earliest.” … This isn’t even an issue with electronic I Bonds, which are immediately cashed out by TreasuryDirect at maturity, with a 1099 coming the next January. Now, with the paper I Bonds, it *might* be possible to get away with delaying taxes by delaying redemption after maturity. Or, you may owe back taxes and possible penalties.

Pingback: Do You Have An I-Bond Time Bomb? – Get Rich Slick!

Would rolling over your soon to mature or maturing I-bonds into a qualifying 529 education account for your children or grandchildren be another strategy to avoid the tax time bomb?

It seems so, although I have no experience with this. Read: https://www.savingforcollege.com/article/how-to-rollover-us-savings-bonds-into-a-529-plan

With some careful planning to avoid the MAGI limits and possibly scheduling the rollovers across several years this does appear to be an alternative strategy to avoid the tax time bomb. Thanks!

Must be a dependent’s 529 plan. You and your spouse (ordinarily, unusual exceptions) count, but not an adult child nor grandchild who isn’t your IRS tax dependent.

Imagine you retire at 60 because you have enough to do so. You decide you can hold out until 68 or 70 to claim Social Security benefits. So essentially you have no earned income for 8-10 years, you live off of your taxable brokerage account and savings on which you pay a small capital gains tax. You decide to do Roth IRA conversions from your 401k retirement because you will pay 0 or a small amount of income tax because you are in a low tax bracket because , again you have little to no earned income. What if you redeem a portion of your I-bonds during these years and pay little to no tax on the interest because of the tax bracket you are now in? You could even put a portion of it into your Roth IRA and treat your I-bond redemptions as an I-bond to Roth conversion could you not? Thoughts?

Being in a very low tax rate does open up a lot of opportunities. Of course, you would need money to live on, so you would need to withdraw from traditional IRAs or sell taxable assets. I Bonds could be a source of some of that income, since you only pay tax on the interest. Your decision might depend on how large an amount you have in traditional IRAs and 401k. If that number is high, you will want to lower it through withdrawals or Roth conversions before you start RMDs. If you don’t have any regular wage income, you won’t be able to contribute new money to a Roth IRA, however.

If you have paper I bonds, tax is NOT due until the year redeemed. You can hold them after maturity to push them into a new tax year. Publication 550 (Investment Income and Expenses) from the IRS makes that clear. https://www.irs.gov/pub/irs-pdf/p550.pdf See page 7.

“Cash method taxpayers. If you use the cash

method of accounting, as most individual tax-

payers do, you generally report the interest on

U.S. savings bonds when you receive it. But

see Reporting options for cash method taxpay-

ers, later.”

“Series EE and Series I bonds. Interest on

these bonds is payable when you redeem the

bonds. The difference between the purchase

price and the redemption value is taxable inter-

est.”

Both of those make it clear it is when redeemed/when received.

This is consistent with with what Treasury Direct says https://www.treasurydirect.gov/savings-bonds/tax-information-ee-i-bonds/#id-when-must-i-report-the-interest–119999

“For paper savings bonds

The 1099-INT will only come when someone cashes the bond or the bond matures. The interest will be reported under the name and Social Security Number of the person who cashes the bond or who owns it when it matures. The 1099-INT will include all the interest the bond earned over its lifetime. If you are the new owner who gets that 1099-INT, you must prove to the IRS that a portion of the interest was previously reported to a different owner.

For instructions on how to pay tax only on the interest that you owe (the interest the bond has earned since you became the bond owner), see IRS Publication 550.”

Why do you have to pay interest on electronic I bonds at maturity? Because Treasury Direct automatically redeems them and puts the proceeds in a CoI.

No, see Appendix D to Part 359 of Title 31 Subtitle B Chapter II Subchapter A of the Code of Federal Regulations (CFR). “What reporting methods are available for savings bonds?

(a) Reporting methods. You may use either of the following two methods for reporting the increase in the redemption value of the bond for Federal income tax purposes:

(1) Cash basis method. You may defer reporting the increase to the year of final maturity, redemption, or other disposition, whichever is earliest; or

(2) Accrual basis method. You may elect to report the increase each year, in which case the election applies to all Series I bonds that you then own, those subsequently acquired, and to any other obligations purchased on a discount basis, such as savings bonds of Series E or EE.”

Clearly, you can’t push it beyond the year of final maturity. Now, in the case of a dormant or found EE bond a 1099 will be issued the year of redemption, and most people probably never read the CFR and amend the tax return of the year when the bond actually matured. But the CFR is clear on this aspect. https://www.ecfr.gov/current/title-31/subtitle-B/chapter-II/subchapter-A/part-359

I agree with Henry on this one, but it is a confusing issue. Rocky’s link to the TreasuryDirect site includes this sentence: “The 1099-INT will only come when someone cashes the bond or the bond matures.” In other words, the tax is due when the bond matures. The IRS Publication 550 is also clear on this: “Report all interest on any bonds acquired … when the interest is realized upon disposition, redemption, or final maturity, whichever is earliest.”

With electronic I Bonds, there is no issue. The money will be paid out when the bond matures and a 1099-INT will be generated. With the paper I Bonds, however, the IRS has no idea you are holding them past maturity. When you finally cash them, a 1099-INT will be generated and you will owe the tax for that year. The question then is: Will the IRS impose a penalty because you did not report the tax in the year it was due? In many cases, it might not but I can’t find documentation to prove that.

I stand corrected!

That said, I do not believe that is how paper redemptions are handled in practice, and perhaps that is why the IRS guidance is as it is. There are over $39 billion of matured but unredeemed savings bonds. Cashing bonds late has to be a common occurrence. I have seen reference (non-authoritative) that the financial institution issuing the 1099 is to issue it for the tax year it should have been filed or somehow note that it is for a prior year (where on 1099-INT?), not for the tax year redeemed. Do they do that? I don’t know.

Redeeming paper bonds through the Treasury might result in a 1099 noting the prior year. I don’t know.

There are also complications because you can’t amend tax returns after 3 years and there are statutes of limitations on IRS assessments for prior years if not fraud.

The average taxpayer, if they follow the IRS written guidance in Pub 550, is unlikely to be penalized (ask for a waiver as you followed Pub 500). Is the IRS likely to assess for the prior year and not have the income in the current year? Seems unlikely.

This is not saying do this because you can get away with it. The IRS is telling you do to it this way, regardless of the actual law, for reasons known to them. Laws, government website and IRS publications often are inartfully drafted or have requirements that are difficult if not impossible to implement. I suspect the IRS guidance is the practical application of the law.

All that said, Pub 550 guidance might change. Planning to delay is not wise. But in the year of maturity if you find yourself in an edge case with regard to AGI/IRMAA, and the IRS has the same guidance, delaying redemption of a few paper bonds into the next year seems fine.

Slightly aside from the main conversation, but it got me thinking as follows: my wife and I have a 4 year old son. Loading up on the current ibond now in a gift box and then gifting to him over the next (say 5) years would likely allow him to redeem them penalty and tax free (assuming his income is low) over the following 5 years. Am I right?

Technically, you have to redeem for the benefit of the child, although since you are the parent you make that determination, so if you want to raid your son’s I Bonds at age 17 to move into a bigger house that he gets to live in I don’t see why anyone would object. Just be aware of the kiddie tax, the first $1,250 of unearned income is tax free and the second $1,250 is at the child’s tax rate (usually 10%).

You really have to do the math, though, that giving up interest of 7%+ offsets the increase in income tax by delaying, based on the commutative property of multiplication. This is especially the case when there are no risk free investments anywhere paying 2%, let alone 3%, above inflation. If inflation drops to 1% or less the delta for pulling early drops to 3 or 4%, and it’s conceivable that the added interest could bump you up into a higher tax bracket or push you over an IRMAA limit. You might also find competitive nominal interest rates which are just as safe. But I think it’s unlikely when I Bond rates are so high and nominal rates are relatively low.

I bought Ibonds regularly 1998-2001 at 3% to 3.6% real. The interest now amounts to more than $460,000. I earned a lot and am happy to pay taxes on the earnings. I have prepared a schedule redeeming these Ibonds over 2025 to 2031, roughly $80,000 in taxable income each year at current values. I don’t expect to be here in 2031, but my wife probably will be and our son has the redemption schedule. Oh – in the past year I bought $50,000 face value TIPS maturing in each of 2032-2034 to extend inflation protection for my wife after the Ibonds are gone.

I have a similar situation with old bonds and this tax bomb that I’m hoping you or your readers can help with. I bought Series EE and Series I bonds many years ago on the advice of my mother to use as emergency saving. I’ve held them all these years and, like everyone else, they are about to mature. As luck would have it, I have three children who will go to college right as the bonds are maturing so I’m about to have my weight in qualifying educational expenses. However, my understanding is that I can’t use the educational exemption because I was under 24 when I bought the bonds.

Is there any way I can get around this? The TD site says if I gift the bond to my child I owe the tax prior to to gift and they owe post. I can’t roll them into a 529 because they don’t qualify for the exemption. Any ideas?

I was shocked to see this requirement that the purchaser had to be 24 in order to later claim the educational exemption. Series EE bonds that doubled in 20 years or less were an excellent option for a young child, and many parents of young children are younger than 24. I doubt there is a way around it, but the rule should not apply to someone like you who actually was preparing for a child’s education costs.

I wonder what the concern is? That a college age student would purchase a huge amount of bonds, which is impossible, and then redeem early to fund their education? But a parent could do this as well.

I wonder if this regulation is legal? Seems to violate equal protection. I don’t see the rational basis for it.

Thank you both for the reply. The only logic I could think of behind the rule is that you could potentially be claimed on someone else’s taxes as a dependent if you’re under 24. Only, in my case I wasn’t and I have the check stubs to prove that the money came from me. I was a legal adult when I bought them and I’m certainly a legal adult 30 years later. It’s just silly.

On the other hand, you’ve inspired me to go through the painful process of converting the bonds to electronic. I might even help my own elderly mother with her stack.

I think the law makers were considering a generalization that people under 24 attending college are either still dependents (financially) or (and/or) their non earned income will still be below the taxable threshold which for those that also worked can be double the amount of those that do not work if the earned income is low enough. So the interest for a dependent can still be tax free depending upon the other factors. I think they generalized and implied that dependent unearned income would be below the threshold for taxation.

It might be worth it to “refinance” the I Bonds now and pay some income tax now to avoid paying it later, but it would be based on a consideration of your current and future income. Redeem the current I Bonds and repurchase them. You could use the gift box method to prepay for future years of I Bonds with your mother. The real interest rates might be lower than you bought them, but they have never been higher in the last decade or two. The other option, if you are married to the children’s father and he was 24 or older when the bonds were issued, might be to add his name to the bond, such that you are co-owners (technically, he would be secondary owner). Then, if you file jointly, my reading of Publication 972 is that the “owner” has to be older than 24, but that is a requirement of only one of the owners.

For the latter, the spouse had to have been 24 or older before the bonds were issued, you file jointly with the spouse, and your children are dependents on said joint return. The spouse doesn’t actually have to be the child’s father (or be male).

What an interesting idea! Said children are dependents on our joint return and he is slightly older than I. Then he would cash the bonds under his TreasuryDirect account which would add a year or two that they would qualify for the educational exemption. Thank you!

I’ve been considering “refinancing” some of my ‘03 and ‘04 bonds (maturing in ‘33 and ‘34) both to avoid the tax time bomb, and obtain the slightly higher interest rate of the current offering. My heirs can worry about any tax problems this might cause 😉

The 2003 and 2004 I Bonds had fixed rates ranging from 1.00% to 1.60%, but I assume yours are either 1.10% or 1.00%. Those aren’t bad. Maturity is still 9 or 10 years away, so you could hold off. But … your call. As for the heirs, my wife always notes its not a bad thing to inherit $100 even if you have to pay $24 in taxes.

Good points, especially like your wife’s philosophy! Yes they’re mostly 1.1%. At this point in time I could probably treat them like cash reserves except for the tax hit. With that in mind, might just pick up some extra of the current issue and decide later about when to redeem the old ones.

Thanks David for all of your excellent posts. I was also wise enough (make that lucky enough) to buy I-bonds in 2001. My plan is similar to yours to spread the tax gain pain over the last few years prior to 2031. For those charitably inclined, another tactic to employ to lessen (or even eliminate) taxable income with RMDs in the mix is to utilize one of the best tax breaks in existence these days: Qualified Charitable Distributions (QCDs). The QCD is not included in taxable income AND counts towards one’s RMD. The limit in 2024 is $105,000–and will be adjusted for inflation going forward.

In 2015 I realized the approaching problem I had with a slug of EE bonds and some of those early I bonds as my husband was facing the inheritance payout of his mother’s sizeable annuities. We staggered the payouts over the 5 years allowed and then I declared the catch-up amount of interest on all my bonds, all before we had to begin taking RMD’s. In 2022, all the EE bonds matured but it was a non-event taxwise because of what I had already done. I will continue to declare the old I Bonds with the 3% fixed rate at least until the they mature in 7-8 years and I’m watching your advice on disposition of the new ones. Three things: 30 yrs passes fast, Treasury could make the declaration easier if it would post an annual and an accumulated interest amount (tho I have no idea how big a job that would be), and don’t underestimate the final tax implications of 30 yr bond interest on your 75+ year old tax return! Of course, this is a first world problem! Thanks for your work on the column, Dave.

I mentioned this I-bond maturity problem to Mr. Enna a few years ago. My strategy is to cash out some I-bonds at least a few years before maturity. I just have to do the math. Everybody’s situation will be different, depending on the amount of social security income, RMDs, pensions, etc. Unknowable changes in the tax laws will also be a factor. I unintentionally laddered my first I-bond purchases starting in 2001 (my beautiful 3 percenters) and bought more annually right after so that will help. My first I-bonds mature in 2031, so I will start thinking hard about I-bond tax issues in a few years.

Paying taxes at a regular annual basis on I-bond interest defeats the tax-deferred interest attraction of I-bonds. I think it is similar for TIPS (I never owned them). You no longer earn interest on the amount you have been taxed, obviously. Neither options excite me much. I will not complain about making a ton of money in I-bond interest. We all knew at the start that taxes will have to be paid some time. Same with IRAs. You know what they say about death and taxes.

I was somewhat surprised to read that Mr. Enna still has paper I-bonds. I suggest everybody convert to electronic, for the many reasons commenters have mentioned. It is not too difficult, but goes at the speed of all government work.

My bonds are titled as a living trust, also called a revocable trust. I control them while alive. When I pass, the fiduciary gets to mess with them.

Fairly sure the Trump tax cuts will not be renewed after they expire. The government needs to squeeze all it can out of those who have been prudent. And the threshold below which social security benefits aren’t taxed doesn’t rise with inflation.

Len, I suspect there will be a compromise that will retain some tax cuts for lower-income people and some for high-income people and corporations. For example, will the state-and-local tax deduction cap remain at $10,000? Probably not. Will the highest tax rates return to previous levels? Probably not. It would be nice to see the net investment income tax trigger level start to get raised with inflation. Probably will.

A few days ago the House came up with a tax bill which now goes to the Senate, including a last-minute insertion of a provision that, for 2023 only (I.e., retroactively) increases the allowable itemized deduction for taxes from $10,000 to $20,000, for couples filing joint returns only, whose household incomes are not more than $500,000. For those of us affected by this issue who have not filed our 2023 taxes early, we may want to hold off filing until we know the fate of this bill.

More details are available at http://www.itep.org.

Lou, what is comical about this is that I held off paying my 2023 property taxes until Jan 2. 2024, just in case the law changes in 2024. Now instead, it might change for 2023 only. The article you site is very negative on the proposal because it would essentially be a tax cut for the rich.

I was already figuring on possibly redeeming some of my ‘33 maturity I-bonds early, but am now thinking that I may have to start in ‘31, as ‘34 will likely be a problem as well. But that’s a while away and who knows what the tax situation will be then…

Start a business and buy equipment (heavy equipment) to depreciate and write off… give the assets to the kids on your expiration perhaps?

Thanks for the thoughtful heads up. Was hoping to hold my I bonds till at least 5 years but will have to look at the scheduled automatic tax rate increases set to kick in in 2026 when the Trump tax cuts for individuals ends.

The principal amount or the accrued interest for the bond $5k investment in April 2001 looks wrong. I believe the accrued interest is around 14k not 12,028 given a 3.4% fixed rate.

$5,000+12,028 interest = $17,028 not $19,162

$57080 accrued interest on 20k of March 2001 bonds. 57080/4 = $14,270 interest on 5k of March 2001 bonds.

$36084 accrued interest on 15k of October 2001 bonds. 36084/3 = $12,028 interest on 5k of March 2001 bonds.

Yes. The accrued principal checks out as $19,162 and the original investment was $5,000. So interest is $14,162. I will be fixing this. Good catch. Not sure how that happened.

You can report the interest early each year, http://www.treasurydirect.gov/savings-bonds/tax-information-ee-i-bonds/

This is complicated transaction and once you do it with one I Bond, it goes into effect for all of your holdings. And I don’t think it would help at all with an I Bond you’ve held 25 years. It seems most appropriate for I Bonds purchased in a child’s name, where no taxes would be due.

Could you also gift the I Bond to someone with little or no tax liability rather than cash it in and be liable for the taxes?

Can you transfer I-bonds to others as GIFTS in one’s lifetime – is step-up-in-basis / Fair Market Value a possibility for the BASIS of the transferred Principal+Interest amount?

Based on what I understood in IRS website material, looks like FMV applies only to securities traded on open market with buyers and sellers involved in transaction.

I did find this article that gives professional/expert opinion…..anyone have any thoughts asides from this?

https://finance.zacks.com/can-transfer-ownership-savings-bond-godchild-7794.html

I am going to try my best to articulate this as my own understanding in this matter is work in progress…..so forgive any mistakes, please.

For adding minor or major child as co-owner to I-bonds as suggested in article link above, as I understand now based on very little I read so far, if they cash, then it will count towards GIFT TAX amounts/exclusion / ESTATE tax form may need to be filled. If they don’t cash but you cash, then non-issue so far estate / gift tax exclusion amount / estate tax form (i believe it is form 709) filing is concerned.

But as far as who gets to pay interest for bonds co-owned with children (or others?), a lively discussion in this forum https://ttlc.intuit.com/community/taxes/discussion/gifted-ee-savings-bond-with-parent-and-child-as-co-owners-who-pays-the-tax-on-interest/00/2043256

This article too is relevant https://finance.zacks.com/tax-implications-adding-child-joint-account-owner-savings-account-10791.html

Hopefully, if there is any value to this, I request David to shed some light on this in a blog article as he articulates clearly and comprehensively!

Thanks!

No basis step up available for gifts made during lifetime, even in situations where the donor gets a deduction for the fair market value of whatever is gifted. As a general rule, the donee (recipient of gift) gets a basis that is the same as the donor’s basis on the gifting date, and the donor’s holding period for the gifted item(s) becomes the donee’s holding period for purposes of figuring whether a gain or loss on a later sale of the item is long term or short term. Even upon death, no step up is allowed on “income in respect of a decedent” (IRD), meaning income to which a deceased person was entitled immediately before death and on which no income tax has yet been paid. That includes accrued interest, such as on U.S. Savings Bonds for which the owner never elected to tax-report interest annually. IRD also includes traditional IRA account balances not yet withdrawn. This means that, unless the decedent elected during lifetime to report the annual interest earned on Savings Bonds as taxable income, the heir(s) will need to pick up the income when cashing in the bonds (unless they in turn die before the earlier of the date the bonds mature or are redeemed , in which their heirs will pick up the income).

Thanks for taking the time to share on step-up-in-basis – this is very useful clarification that cleared my misunderstanding on the topic.

So what that leaves with is the consideration of adding co-owners instead of selling I-Bonds prior to their eventual maturity with an understanding of tax ramifications if one or other sell prematurely or the bond reaches expiration date.

This may not be a strategy for most alive except for a few who are reaching an age where it becomes a consideration!

Click to access sav4000.pdf

“If the name of a living owner or principal coowner of the bonds is eliminated from the registration, the owner or principal coowner must

include the interest earned and previously unreported on the bonds to the date of the transaction on his or her Federal income tax return for the year of the

reissue. (Both registrants are considered to be coowners when bonds are registered in the form: “A” or “B.”) The principal coowner is the coowner who (1)

purchased the bonds with his or her own funds, or (2) received them as a gift, inheritance, or legacy, or as a result of judicial proceedings, and had them

reissued in coownership form, provided he or she has received no contribution in money or money’s worth for designating the other coowner on the bonds.

If the reissue is a reportable event, the interest earned on the bonds to the date of the reissue will be reported to the Internal Revenue Service (IRS) by a

Federal Reserve Bank or the Bureau of the Fiscal Service under the Tax Equity and Fiscal Responsibility Act of 1982. THE OBLIGATION TO REPORT

THE INTEREST CANNOT BE TRANSFERRED TO SOMEONE ELSE THROUGH A REISSUE TRANSACTION. If you have questions concerning the tax

consequences, consult the IRS, or write to the Commissioner of Internal Revenue, Washington, DC 20224. Unless we are otherwise informed, the firstnamed coowner will be considered the principal coowner for the purpose of this transaction.”

Thanks for sharing!

Wow…….as far as taxes, no stone has been left unturned………everything well thought of! Only the wealthy and their hired hands can find loopholes 🙂

David,

Another aspect for married couples is the tax consequences when one spouse dies – in the following year, the remaining spouse will be in the more constrictive single tax-payer brackets.

Unlike a bond maturity date though, the timing of this event is not as predictable. One needs to at least be aware of this eventual event.

I refer to the 2031 I-Bond time bomb as our big python (meal bulge); he’s still eating and getting bigger. To relieve the pressure (indigestion?), we are whittling down our future RMDs by doing Roth conversions every year to the extent that we can. This also has the benefit of helping out the future remaining spouse, whenever that event occurs. The Tax Man has to get paid sometime.

On a slightly off-topic, but related aspect, I wonder how many people have thought about their tax-deferred accounts and the eventual RMDs they will need to take (yet another ticking time bomb). Some might be surprised at how much they will have to withdraw; without proper advanced planning, they might be put into new taxing situations with overall tax rates higher than when they were working. The whole mantra of 401k’s was that you’d be withdrawing when you are in lower tax brackets; not necessarily!

FYI – the level at which the Net Investment Tax is triggered is NOT adjusted with inflation. With time, everyone will be subject to it (unless the government modifies it).

PS — Another great topic generating terrific discussion.

RMDs and the Medicare IRMAA surcharges are the two important issues most people 10 years away from retirement know little about. RMDs will be a big issue for us because we were locked out of Roth accounts in our earning years. We are doing Roth conversions now, but there is only so much you can do each year without hitting more tax consequences.

Yes, I too have mourned the lack of Roths earlier in our earning years.

You can only do so much planning; good to know of the strategies before the opportunity is lost.

The median 401k for a 65 year old is around $100k, average is $300k, the RMDs aren’t going to be that big a deal. It may mess with Social Security taxation, only because those limits haven’t changed in 40 years, but is unlikely to bump them up into a higher tax bracket. The specter of million plus 401k’s is really a first world problem.

Let’s assume early-year I Bond investors aren’t your “typical American.” They were savvy enough to buy these unknown products nearly 25 years ago and hold them. I’d guess most of these now-retired investors have more than $1 million net worth as a couple, and $2 million is probably closer to average if you include home equity. Is that a “rich person”? It just isn’t. It is what I call “financially secure,” but not rich at the age of 65+.

Median net worth of Americans in their late 60’s and 70’s is $266K. I’m pretty sure all those people close to or below the median would think someone with $1M-$2M as being rich. https://www.cnbc.com/select/average-net-worth-of-americans-ages-65-to-74/#:~:text=The%20most%20recent%20report%20released,and%20early%2070s%20is%20%24266%2C400.

“Let’s look ahead to 2031. Both my wife and I will be collecting Social Security, a pension, possibly an annuity, and drawing RMDs from traditional IRA accounts.”

One small point – Social Security income is not counted toward triggering the Net Investment Tax.

RE: Net Investment Tax — the taxable portion of your Social Security IS part of your MAGI (modified adjusted gross income). BUT those SS earnings are NOT part of the investment earnings that are taxed.

The taxable portion of Social Security benefits is included in AGI, and unless I’m missing something, also in MAGI, in which case I believe it could help trigger NIIT on investment income. If MAGI is over $250,000 for a joint return, then the lesser of the amount over $250k or the amount of the investment income is subject to the 3.8% tax.

Buffethead, I was hoping you were right, but it does appear Social Security income is part of the MAGI for the net investment tax. But it is not considered “investment income” as minnesotaswede points out.

Yes and oops. Sorry for the overly wishful thinking.

Thanks, Dave. I plan to do incremental redemptions to manage tax brackets. The other idea I have is to gift a portion of the older bond to a student, who could use I bond interest for educational expenses. Would that work for those with child or grandchild in school?

This sounds like a valid approach.

I don’t believe I-bonds actually “mature”. You can continue to hold them and they just won’t accrue interest beyond the 30-year “maturity”. You can choose to realize the tax impact well beyond the 30-year “maturity” should it be tax efficient for you to do so.

No. The IRS considers the taxes due in the year the savings bond matures. I know some people delay redeeming paper savings bonds, but it is possible they will face a penalty. And because these amounts are so large, the IRS isn’t likely to ignore them. Read this: https://budgeting.thenest.com/penalty-savings-bond-past-final-maturity-31113.html … For an electronic I Bond on maturity the Treasury will cash out the savings bond and deposit all the money in your connected bank account or the Certificate of Indebtedness account on TreasuryDirect.

Can I convert electronic back to paper?That way I can control when to cash in.

No. But you can easily cash electronic I Bonds, in $25 increments, at TreasuryDirect.

Good point. Let the heirs worry about it. Wonder if they get a stepped up basis?

I Bonds aren’t eligible for a step-up in basis. They’ll pay federal taxes on the untaxed interest since your original purchase when they cash out or when the bonds mature. The bond interest will be taxed as ordinary income, not long-term capital gains.

https://thefinancebuff.com/i-bonds-taxes-simple-default.html#:~:text=I%20Bonds%20aren%27t%20eligible,not%20long%2Dterm%20capital%20gains.

Anyone with substantial savings bond investments would be wise to get a copy of Tom Adams book “Savings Bond Advisor: How US Savings Bond really work — with investment, tax, and estate strategies”.

While this book was last published in 2007 (and only used copies are available) the information is timeless.

On page 122 he states ” The estate can pass the deferred taxes [on to the beneficiary] or it can pay the deferred income taxes . . . through the date of [the] benefactor’s death, on [the] benefactor’s final tax return.”

Bottom line is hope I die before Ibonds mature?

Yes. And I think The Who came to same conclusion…

Hahaha…good one!!

Regarding the Estate paying the tax on I -Bonds. I was thinking the same until I read Harry Sit’s take on it in his Finance Buff blog:

“Your second owner or beneficiary needs to keep the documentation to show how much interest was already added to your final tax return for the bonds they inherited. When they cash out the bonds or when the bonds mature, the 1099 form from TreasuryDirect will still show all the interest since your original purchase. In order to claim the tax exclusion, they’ll have to remember to back out the interest that was already included on your final tax return. See IRS Publication 559 (page 11).

Because it can be many years until they cash out the bonds or when the bonds mature, it’s quite possible they’ll forget and they’ll pay tax again on the whole thing when they have a 1099 form in front of them. I think it’s better to just go with the default and not go out of the way to pay up in the tax year of your death.”

Bottom line is that the Treasury issues the 1099 only when the bond is cashed or matured. High chance of double payment of taxes, knowing my heirs. 🙂

Well done, as usual. I too fall into this fortunate group. My partial solution will be shorter term municipal bonds utilizing one of Vanguard’s bond funds ( municipal bond interest is excluded from the NIL) coupled with some early redemption when the time comes. Some risk with the funds, but the onerous taxation is a certainly.

“Anyone may arrange his affairs so that his taxes shall be as low as possible; he is not bound to choose that pattern which best pays the treasury. There is not even a patriotic duty to increase one’s taxes.”

( Long term federal judge Learned Hand 1872-1961)

Yes, felt smart when I got the 60K/year bonds, less so now. Conversion was not that bad but one question, once the paper bonds have been converted to electronic, does the “must sell the whole bond” limitation apply or can you convert in small increments?

Yes, once converted, I believe you can redeem any amount in $25 increments, because these are now electronic savings bonds. It would be interesting if you could schedule redemptions in advance, like you can with purchases. (As far as I can tell, you can’t.) Then you could set up monthly withdrawals of $1,000+ over several years and create a faux annuity.

In your paragraph “Plus, because of the way TIPS are taxed, with inflation accruals getting taxed in the current year, when this TIPS matures on April 15, 2029, there will be only a small amount of tax due — on 2 1/2 months of inflation accruals and the final coupon payment of 1.9375%.”, I believe it should be “3 1/2 months”.

You are correct, and this is fixed. Thanks for the alert.

Thanks for the reminder. I have 2000 and 2003 vintage I-bonds that I will have to deal with down the road. I did ship off my paper bonds and converted to book entry years ago. You will need a bank signature guarantee to execute the documents. It took a while but it works. It is tough to find a bank to redeem them. Also, finding a safe deposit box is tough these days! Modern banks are not including them in their construction.,

I’ve converted (small amounts of) paper bonds a couple of times in the past few years, and successfully completed the process without running into any signature guarantee requirement.

I agree. I never had to use a bank or any other third party in the conversion process. I just checked Treasury Direct and did not see any new requirements to do so.

Amazing the power of compounding interest twice a year. It stinks to have to cash out early I-bonds only to not make “too much” money, but it’d be silly to make yourself go into another tax bracket and LOSE money. Considering inflation is essentially a tax, it feels like double taxation without representation. Then again, we have no representation regardless of how much we pay 🙄

And despite the high taxes we pay it is insufficient to fund the federal government.

Good analysis of the time bomb. One other thing – if you hit the IIRMA threshold on your Medicare premiums, you may also be paying a surcharge on your monthly Plan D (drug plan) premiums.

Was thinking about the same thing. These taxes (NII and IIRMA) should be exempted for anyone 65 or older. Each one of our dollars is already taxed multiple times before death (where for some it is taxed yet again). We should give all retirees a little break from excessive taxation. This way, our ‘golden year’ dollars are only taxed six or seven times…