By David Enna, Tipswatch.com

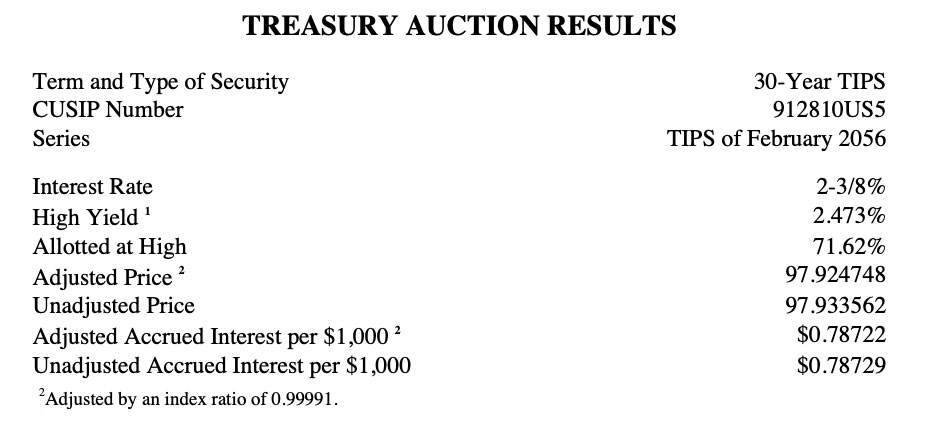

The Treasury’s auction of $9 billion in a new 30-year Treasury Inflation-Protected Security — CUSIP 912810US5 — generated a real yield to maturity of 2.473%, the second-highest yield since the 30-year term was restarted in February 2010.

Demand appeared to be strong. The “when-issued” yield prediction released just before the close was 2.49%, so investor bids were strong enough to lower the real yield. The bid-to-cover ratio was 2.75, also an indication of strong demand.

The auction result set the coupon rate at 2.375%, matching a 16-year high.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 2.473% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.473% for 30 years.

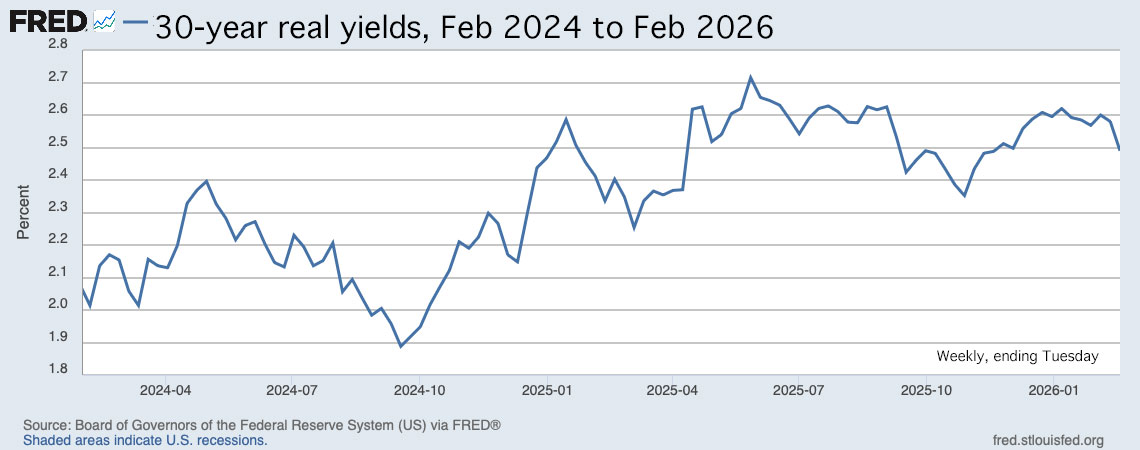

Overall, this looks like a great result for small-scale investors, especially those committed to holding for the full 30-year term. Here is the trend in the 30-year real yield over the last 2 years:

While real yields have dipped a bit in recent weeks, today’s real yield of 2.473% remains historically attractive. This is the first TIPS ever issued to mature in 2056.

Pricing

Because the coupon rate was set below the auction’s real yield, investors got this TIPS at a discounted price of 97.933562. In addition, this TIPS will carry an inflation index of 0.99991 on the settlement date of February 27. With that information, we can calculate the cost of an investment of $10,000 par value:

- Par value: $10,000.

- Principal at settlement date: $10,000 x 0.99991 =$9,999.10.

- Cost of investment: $9,999.10 x 0.97933562 = $9,792.47

- + accrued interest of $7.72

In summary, an investor purchasing $10,000 par value of this TIPS will pay $9,792.47 on the settlement date for $9,999.10 of principal. (The principal is reduced because of slight deflation in the month of December.)

Inflation breakeven rate

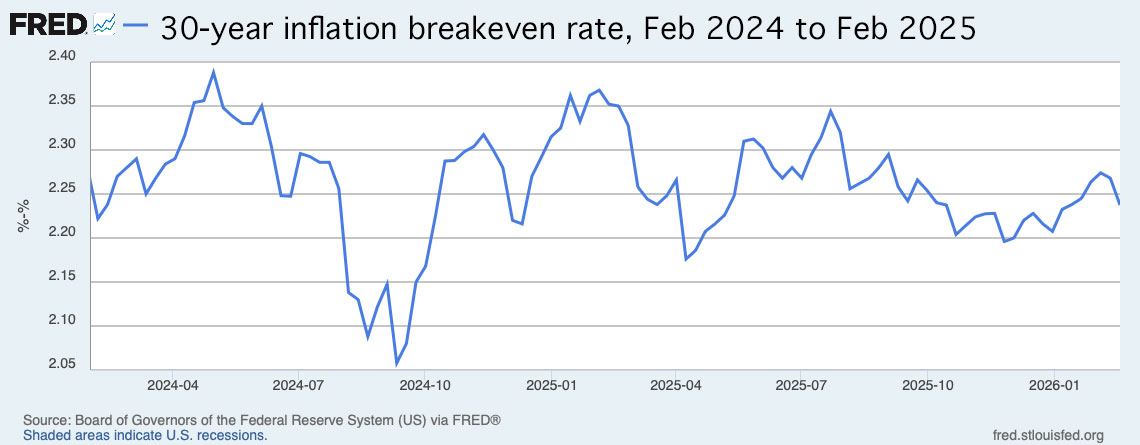

At the exact time of the auction’s close I was asleep in northern Australia (15 hours ahead of EST), but two hours later the 30-year Treasury bond was trading with a nominal yield of 4.70%. We’ll go with that, creating a 30-year inflation breakeven rate of 2.23%, which seems reasonable. This means the TIPS will out-perform a 30-year bond if inflation averages more than 2.23% over the next 30 years.

Here is the trend in the 30-year inflation breakeven rate over the last two years, showing that this auction fell into the mid-range of inflation expectations:

Thoughts

This looks like a solid auction result for both small-scale investors and the Treasury. Demand appeared to be strong, but the real yield remained historically attractive.

It’s impossible to predict (or even troubling to think about) where both real and nominal yields could be heading for longer-term issues. The U.S. debt continues climbing, while at the same time confidence in the Federal Reserve and U.S. dollar is waning.

Real yields could plummet if the U.S. economy sinks and a future Federal Reserve reignites bond-buying quantitative easing. Or, real yields could continue rising. Impossible to say. This TIPS, however, will offer inflation protection for 30 years, along with an attractive coupon rate of 2.375% paid on inflation-adjusted principal.

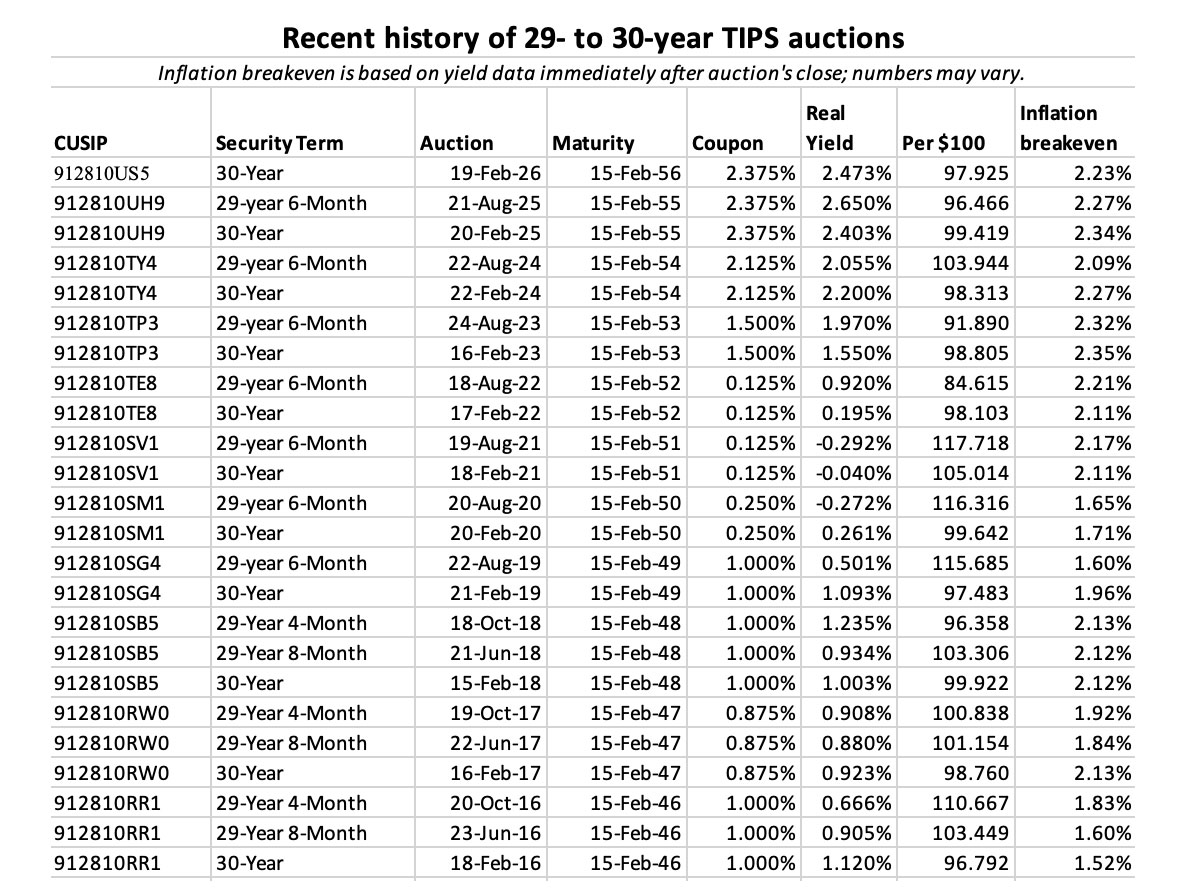

For the right investor, this looks like a solid investment. Here is the auction history for this term over the last 10 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am still a little confused on how it works. If I am 66 and want $20K of income annually for the next 30 years how would I take advantage of this? Thanks!

Looks to me like you would need to purchase roughly about $825K of these TIP bonds in the secondary market at your brokerage.

Thanks!

You can use tipsladder.com to make a very good estimate. I am assuming you want to generate $20,000 year *adjusted for inflation* for all years 2027 through 2056. That is what a TIPS ladder does best. I did a quick estimate and found that the “net cost today” would be $441,495 (depends on a few parameters, but that gives you an idea). That would generate a $20,021 a year in real dollars (meaning dollars adjusted for future inflation). That site can also give you a recommended list of TIPS to purchase to build the ladder.

I was thinking he meant $20,000/year actual cash interest coupon payments today and not counting the inflation adjusted principal value increases nor inflation adjusted payment increases.

I figured $825,000 of 30-year Tip bonds paying today’s ~2.42% cash interest equals about $19,965 in interest payments in the next 12 months.

If this is an annuity question, how much to invest now to get back $20,000/yr and end at 0 after 30 years my calculation is $328,530 has to be invested today assuming 2% inflation and semiannual withdrawals.

It appears to me that purchasing $825k in 30-year Tip bonds you’d get the $20K a year cash payment adjusted biannually by inflation accruals of the principal and then somebody would receive the original $825K principal basis money back in thirty years adjusted by the cumulative years of inflation… maybe more than a couple of million. Who knows the next thirty years inflation rates.

I was interested in understanding what I would need to do to get the 2.473% real yield every year for the next 30. I thought when purchasing via the secondary market every TIPS would be a different real yield but maybe I am wrong. With such along time horizon maybe I should only do the TIPS for the next ten years and use a broad market ETF like VTI for years 11-30 and have some type of strategy to replenish the next ten years every year (exhausting thinking about). I was also wondering how to get the 2.473% for the next ten years. It seems like that is only for 30 years which makes it very hard to use. Thanks!

You might find some useful info over at the BogelHeads.org site in the Outline of financial planning category on their blog too. I find a lot of useful ideas there and here on Dave’s Tips Watch site.

The only way to get the 2.473% real yield (in today’s market) would be to buy the 30-year TIPS, but that’s a complicated investment. (For example, a 5-year TIPS currently has a real yield of just 1.1%.) With the 30-year TIPS, the annual coupon rate of 2.375% would be paid out each year on rising principal, but the inflation accruals would be added to principal and not paid out until 30 years later or when you sell the TIPS. So this one TIPS is not really a practical investment for yearly income, and that explains why a ladder works well — providing current income and inflation-adjusted maturities each year. A 30-year nominal Treasury bond (yielding 4.64% currently) would fill that need better, providing 4.64% principal each year, but with no inflation adjustment.

Would it be possible to create a ladder of sorts that would capture the inflation accruals and redeem the principle annually by buying on the secondary market? For example: In Year 0 you might by 10 bonds. $10,000, 9,000, 8,000 and so on, that are projected to pay back $10,000 each year.

I didn’t but this TIPS auction as but I wanted to say thanks for all the useful info you provide to all of us.

I believe I helped my son buy 30 year TIPS for his IRA last August at a real yield of 2.65%

Was that the all-time high?

The highest since the 30-year term restarted in Feb 2010.

Here is a question. If a 5 year TIPS and a 30 year TIPS were issued on the same day – would they have the same face value for the life of the 5 year bond? I think the answer is ‘yes’ – but they would pay a different dividend. Each would follow the same inflation data.

Yes, if issued at the same par value. The same inflation accruals would apply until the 5-year maturity.

I like the results a lot.

That is guaranteed retirement money throwing off likely ever increasing cash payments for those in the right age group.

If your 45 at the most, than you can hold to maturity and benefit from this investment. For those of us older, it does not make sense to buy a volotile investment that matures long after we will be dead. Be nice if they offered more short maturity TIPS, like maybe a 3 year, 7 year, and 15 year.

So I am in this same age range (a spry 55). I was a buyer as I am builidng a long term to mature from ages 85-90. I just look at it as security for the inevitable end.

I believe you can go into a brokerage account and shop for TIP bonds maturing in however many years you prefer.

If you need to.

For a long time I avoided the secondary market. But once you start building a ladder, it is a necessity and it works well.