By David Enna, Tipswatch.com

I realize that the fixed rate of the U.S. Series I Savings Bond isn’t top of mind for many investors at the moment, given an active war in the Mideast, soaring gas prices, and sharp declines in both the stock and bond markets. But in our little inflation-watching community, it’s a big deal.

Both the I Bond’s permanent fixed rate and inflation-adjusted variable rate will be reset May 1 for purchases from May to October 2026. Before the outbreak of war on Feb. 28 it appeared likely the I Bond’s fixed rate would fall from the current 0.90% to 0.80%. And it also seemed likely the composite rate would fall well below the current 4.03% because of a decline in the variable rate.

The fixed rate is important because it is permanent for the potential 30-year life of the I Bond. It represents the I Bond’s “real yield” above inflation. March’s surge in both prices and interest rates has changed the likely result of the May 1 reset.

(For more on the basics of I Bonds and potential buying strategies, read my Jan. 25 article: “I Bond buying guide for 2026: Wait it out.”)

Although the U.S. Treasury does not reveal its formula for determining the I Bond’s fixed rate, we know Treasury tracks trends in real yields and adjusts accordingly. This forecasting formula has worked for the last decade: Take the average real yield of the 5-year TIPS over the preceding six months and apply a ratio of 0.65.

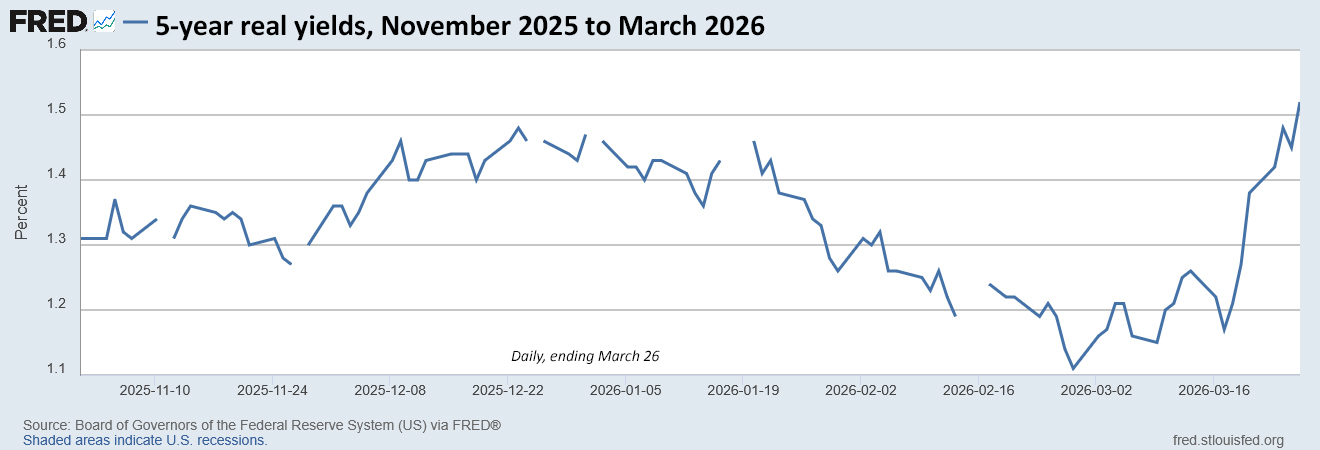

The next rate reset will come May 1, so we are interested in real yields from November 2025 to April 2026.

The before. On Feb. 27, one day before hostilities broke out, the 5-year real yield had fallen to 1.11% and looked likely to continue in a range below 1.20%, which would have dropped the I Bond’s fixed rate to 0.80% at the May 1 reset.

The after. At Friday’s close, the Treasury was estimating the 5-year real yield at 1.50%, up 39 basis points for the month, so far. The current trend — it appears — would have the 5-year real yield solidly above 1.30% in April.

Let’s look at how the equation has changed.

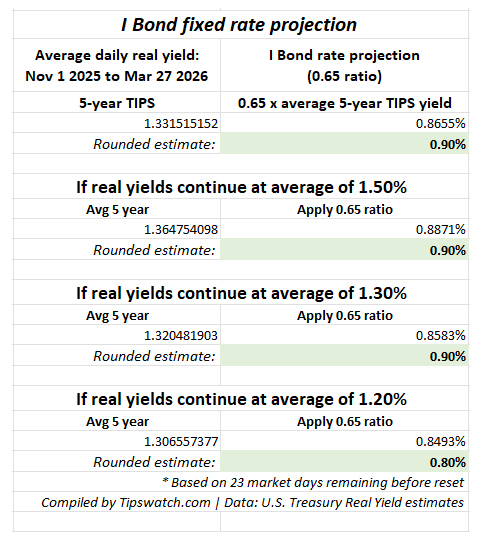

In this chart, the projection is calculated using a 0.65 ratio of the average daily 5-year real yield from November 1, 2025, to March 27, 2026. Using that data, the real yield average is 1.33% and results in an I Bond projection of 0.90%.

1.331515152 x 0.65 = 0.8655%. The I Bond’s fixed rate is always rounded to the tenth decimal point, so the current projection is 0.90%.

That projection holds even if the 5-year real yield drops to the 1.30% range for the 23 remaining market days until the May 1 reset. It would take a fall to an average of 1.20% for those 23 days to cause the projection to fall to 0.80%. That kind of fall is unlikely, even if the Iran hostilities are resolved quickly.

It is even more unlikely that the I Bond’s fixed rate will rise above the current 0.90%, which would require a massive move higher in real yields to balance off five months of accumulated data.

Conclusion. It looks highly likely that the I Bond’s fixed rate will hold at 0.90%.

Qualifications

This projection is based on 10 years of Treasury history in setting the I Bond’s fixed rate. But the Treasury could change course at any time and we should be aware of that. President Trump’s first-term Treasury followed the formula and has continued to do so in his second term.

What about the variable rate?

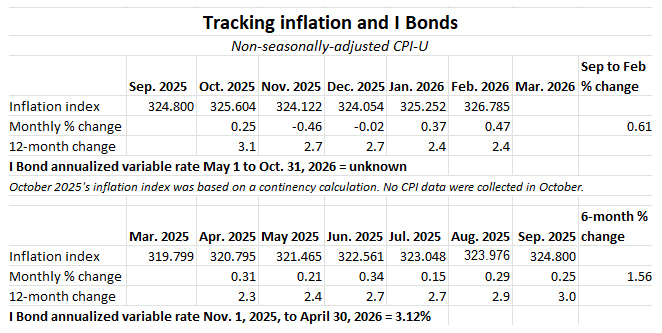

The March inflation report will be issued April 10 at 8:30 a.m. and we will get the final piece needed to know the I Bond’s inflation-adjusted variable rate, which will roll into effect for all I Bonds ever issued, depending on the original month of purchase.

Here are the data so far:

At the end of February — if we assumed moderate inflation in March — we were looking at a potential variable rate of about 2%, well below the current 3.12%.

But soaring gas prices in March — up nearly 40% for the month — are likely to trigger a dramatically higher non-seasonally adjusted inflation rate for that month. The Cleveland Fed’s Nowcasting page is projecting a rate of 0.76% for all-items inflation in March. That is a seasonally adjusted number, so the actual non-seasonally adjusted number for March could be 1.0% or higher.

Conclusion. If we get 1.0% non-seasonally adjusted inflation in March, the variable rate would soar to 3.22% and we would be looking at a composite rate of about 4.2% for six months for purchases from May to October 2026.

Is there a strategy?

Yes. The strategy remains the same as I wrote in January: “Wait it out.” We will get the March inflation number on April 10 and then we will have more than two weeks to contemplate purchasing I Bonds in April, in May, later in the year, or not at all.

If the I Bond’s fixed rate looks likely to hold at 0.9%, and the composite rate will be competitive with the current 4.03%, there will be less incentive to buy I Bonds in April. And in fact, the logical path might be to see how rates develop before the November 1 reset.

An I Bond earns the then-current composite rate for six full months before transitioning to a new variable rate. So a purchase late in May would be financially equivalent to a purchase late in October.

Although real yields are climbing (and could remain elevated) I Bonds remain an attractive inflation-adjusted investment, earning tax-deferred interest, exempt from state income taxes, and with rock-solid deflation protection.

April is going to be an interesting month. I will have more to say on this topic after we see that March inflation report.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David’s fixed rate predictions have been stellar. I hope “the variable rate would soar to 3.22%.” That would give a 6.22% yield on my I-bonds bought in 2001. Who says I-bonds are boring and stodgy? Well, maybe they are now. We will probably never see another 3.0% fixed rate.

Hi David, I’ve been thinking about how TIPS and I Bonds might perform in a stagflation environment. As far as I know, TIPS haven’t really been tested through a prolonged stagflation period (perhaps the brief episode in 2022 is the closest example). Given the current situation—especially with oil prices likely to remain elevated—it seems the risk of stagflation is increasing. My understanding is that TIPS and I Bonds should provide better protection against high inflation compared to nominal bonds. However, I’ve noticed that recently TIPS prices have been moving in sync with nominal bonds, particularly with the rate spikes over the past few days and weeks. That seems counterintuitive if they’re meant to hedge inflation. Could you share your perspective on this? In this environment, would it make more sense to hold TIPS/I Bonds, or to stay in cash/money market fund and wait for potentially higher yields before investing in TIPS?

Best,

Dongchen

Real and nominal yields tend to move together, higher or lower. In the same direction, but not necessarily by the same amount. When the spread gets bigger, it means inflation expectations are rising. (This is the inflation breakeven rate.) When the inflation breakeven rate gets very high, it means TIPS have less of a chance to out-perform the nominal Treasury. But it could happen if future inflation is higher than expected.

Stagflation means a period of very slow economic growth and higher-than-expected inflation. If that means the Fed would be reluctant to raise interest rates at a time of high inflation, then TIPS investments (especially funds and ETFs) should do well. Steady interest rates mean stable bond prices while higher inflation would mean higher inflation accruals. I say funds because a TIPS held to maturity would simply give you the expected return above inflation, whatever inflation is.

So stagflation shouldn’t mean TIPS would be poor-performing investment, as long as future inflation actually is higher than expected.

The wait is over…one of the missing ingredients is the benefit of starting the minimum one year old for maximum flexibility, e.g. Buying nlt end of April provides a known return for 12 months (less always a 3 month penalty)…guaranteed and thus if the Nov reset effective then/April 2027 for those purchases IF going south could permit liquidation in July of 2027 WITH the lower 3 month penalty for July 2027. Otherwise buy for the gift box and deliver this/next year. To wait to May to buy provides no certainty for the second 6 months. And to wait to October suggests…what is your money earning now? Nothing?

2.5% to 2.7%+ Real yield above inflation on 20 to 30-year TIP bonds.

Thom…and your point is? Why would you be looking to move funds to Ibonds if you like your quoted rates for next xx years? The focus is now for changing…I don’t see the relevance of your post in connection with the theme. Thanks anyway

I believe you asked ‘what is your money earning now?’ and I answered… I’m earning a lot more real yield by picking up TIP bonds right now than I-bonds are offered for currently.

If someone is only going to hold any bond just a short time, why not just take money market interest at around the 3.5%+ rate or CDs paying closer to 4% short term?

To me, it seems that David is correct on the ‘wait it out’ idea from what I’ve been reading regarding potential financial impacts of the current global commodity pricing turmoil.

I meant regarding ‘wait it out’ on I-bonds… but to me, TIP bonds right now are a horse of a different color.

I buy i-bonds as long term investments, so I am always most interested in the fixed rate. Looks like I will pass on buying my yearly allotment at the end of April and see how the next fixed rate looks come end of October. I have seen posters on here stating they might pass on any i-bond purchases this year. I would never pass on buying an i-bond with the fixed rates we have been seeing lately. Prior to these last few years it had been many years since we had fixed rates close to or over 1.00%. If inflation does pick up in an extreme manner these i-bonds will be earning a very nice amount of interest. Look to what i-bonds were paying out during covid even with a 0.0% fixed rate. If current events would drive inflation back up to those kinds of levels, it’d be a very nice thing to have i-bonds with a fixed rate close to around 1.00%.

I’ll just point something out to the group– which is why I fail to see the wisdom of obsessing on the most propitious moment and waiting to buy. You can only buy a bond product for what the prevailing interest rate is at that particular moment. Wishing the fixed rate, variable rate, or composite rate to be higher won’t make it so. Wait too long and 2026 passes you by– and we all know that there are limits to annual I bond purchases.

I have been enjoying reading David’s posts from 10 years ago about I-bonds and EE bonds. If you purchased an I-bond in 2015 when the fixed rate was zero, or in 2016 when it was 0.1, you still did better in the following 10 years than any money market fund, broad bond index fund, or long term investment grade bond fund. In fairness, 2022 was one of the worst, if not the worst, bond markets in history, which made I bonds shine in comparison. Junk bonds had superior returns to I-bonds over the last 10 years.

But I think as conservative investments go, I-bonds, by their nature and structure, are a winner compared to the alternatives. Don’t hesitate.

The main point is that the current fixed rate / composite rate combo (4.03%) is available for a full six months for any purchase through the end of April. The next fixed rate / composite rate combo will then be available (for a full six months) for purchase at any time through October. So there is a lot of time to ponder a purchase in May or October. Either one offers the same return, but the 1-year 5-year clock starts ticking earlier if you buy earlier.

I will be buying I Bonds in 2026. The only question is when.

“So there is a lot of time to ponder a purchase in May or October.”

I think you meant to say:

“So there is a lot of time to ponder a purchase in April or October.”

The current I Bond fixed rate / composite rate isn’t had at all. An equivalent 6-month T-Bill (also state tax free) is around 3,7% so the “premium” you get for buying an I Bond instead is about 0.3%.

On the other hand, that comes to a difference of $15 in interest on a $10,000 I Bond,

The real question for long-term buyers is the May 1 fixed rate (which David predicted is likely to remain at 0.9%) vs. the November 1 fixed rate (which is unknowable at this time).

I say in this situation it doesn’t matter all that much because the current fixed rate is just shy of 1% which is solid, and if the fixed rate shoot’s up at the next reset in November, you can always buy it in 2027 before the May 2027 reset,

No one is suggesting hesitating until the year is over and its too late. The rates change twice a year. There’s plenty of time between rate changes in order to make a purchasing decision, and as you are limited to 10k / year it makes sense to try to time your purchase for maximum impact. I usually purchase at the end of April, the End of October and/or the end of either Nov or Dec (if I didn’t make the full 10K worth of purchases earlier) and what the Fix rate is looking to do is a big part of the decision to when of those above times I’ll purchase. For example, if the Fix rate looks to be flat or going down at the May reset, I’ll purchase 5k or 10k in April otherwise I’ll wait till October. If the rate looks to be flat or going down at the Nov Reset, I’ll purchase the rest in October, otherwise I’ll make the purchase in Nov or Dec. I always end up buying the full 10k by years end, the only question is when during the year it happens in order to maximum the return on my investment.

As a likely relative youngin’ here, I’ve accumulated I-Bonds for a while now as a “Build-an-Annuity” to complement Social Security as an income floor, plus be an additional “break-glass” emergency fund if life went very sideways. I’ve plenty of equities to compound another 15 – 22 years before I likely stop working.

I’ll just wait ’til ~10 days before reset to make my decision, as always 🙂 I rely on communities such as this one to help reinforce those decisions.

If the fixed rate remains at 0.90%, there’s no point for me to have already purchased, purchase now, or likely purchase any earlier than October 22nd, 2026.

I try to best maximize my “blended” (across all bonds) fixed rate to best ensure there’s net (of taxes) return 20 – 30 years after purchase. For me, a blended fixed rate of >= 0.60% should achieve that. Right now my blended fixed rate is 0.80%, so I’ve opportunity to increase that to 0.818% or higher with 2026’s purchase.

As a courtesy to the TipsWatch community, you are welcome to use a webpage I wrote for my personal use, to monitor the current Treasury term structure (including 5 and 10 year TIPS)

If you click on the name of a Treasury security in the first column, it opens the page at CNBC that provides data and a chart for that security (in another tab, leaving my page still available)

https://www.bearforum.com/cgi-bin/rrr1.pl

Sample page image (hopefully this will display)

https://www.bearforum.com/Treasuries.jpg

It works and offers more information than you’d find on Bloomberg’s Current Yields page. (I have a watchlist at Bloomberg that works in a similar way.)

Thank you for your kind words, and for taking the time to check it out

I should have mentioned, it takes a while to load because it has to read 12 different webpages to gather the information it presents

So hopefully, anyone who tries to use it will be patient and not give up on it prematurely

I selfishly request you add the 20-year TIPS to the list.

It would be my pleasure to accommodate you

However, the URL for 20 year TIPS at CNBC pulls up no data:

US20YTIPS: undefined undefined (undefined)

I also tried adding the 20 year TIPS from Market Watch, but that doesn’t seem useful.

912810PS15 | United States Treasury 20-Year TIPS 2.375% Jan 15, 2027 Advanced Charts | MarketWatch

It’s certainly not useful enough for me to go to the trouble of mimicking the careful page scraping I do to derive the 2nd, 3rd, and 4th columns of the table for each of the other securities.

I also added the 30 year TIPS from CNBC, which works as expected (i.e. the chart page URL is analagous to all the other securities charts, and the 2nd, 3rd and 4th columns are equally useful)

If you have a better, more useful URL for the 20 year TIPS, please inform. I’ll be cleaning up the program in a day or so to remove the non-functional rows (I’m leaving it this way for the moment for illustrative purposes)

You may or may not support the policies, but there is no denying that two policy choices by the Administrarion, extreme unprecedented tariffs in 2025 and the Iran War in 2026, have directly spiked inflation that was heading towards the Fed’s 2% target. This is ironic given that affordability concerns about high prices that spiked worldwide during the previous administration following the pandemic reopening and supply chain disruptions.

The next CPI report will be a doozy, and the one after that. The fact that the two reports land on either side of the May I Bond reset will serve to smooth out the two rate increase this year.if you believe, as I do, that the impact of $100 per barrel oil prices will filter through the economy and raise prices broadly, then waiting until the October CPI report release might be the way to go. As always, you can hedge your bets and split your purchases between the two — $5,000 now and $5,000 then, or $10,000 now and $10,000 then with your spouse. Either way, anyone looking to minimize the three month penalty and redeem before 5 years with an upcoming low rate period that seemed likely just a month ago will likley not have that opportunity this year at all.

With 30-year TIPS yields hitting 24-year highs (if the chart is correct), I’ve been increasingly looking at tax-opportune times to take the interest hit and cash in old 0% fixed rate I-bonds in favor of the TIPS maturing in 2042 and later. As usual, I was early.

https://www.cnbc.com/quotes/US30YTIP

It’s probably true that the 30-year real yield is at a 25-year high, but that finding is skewed by the fact that no 30-year TIPS were issued from October 2001 to February 2010. The last TIPS issued in October 2001 had a real yield of 3.465%. Then there is a gap to February 2010, when a 30-year TIPS got a real yield of 2.229%, well below today’s market yield. I have also been taking looks at the 2040 to 2043 range, where I could supplement my holdings.

CUSIP 912810FH6 was sold 4/15/1999 (almost 27 years ago) with a 30 year term and a coupon of 3.875%.

CUSIP 912810FQ6 was sold 10/15/2001 (less than 25 years ago) with a 30-1/2 year term and a coupon of 3.375%

Those were the days!

If the March inflation number is 0.76- 1.0% ( as your analysis suggests), that is a massive increase on an annualized basis. I would be happy with a reset composite rate of where it is now. The November reset will be very interesting indeed– like 2022 when it was 9%?

The issue I struggle with is with the abrupt reset upward in interest rates, yields on conventional bonds are increasingly appealing (junk, municipals, corporates, especially at the long end of the curve). Is now the time to be brave, jump in and buy more? Will the future not be as dire as it now seems? Or is there much more pain ahead? The Wall Street types I have been listening to talk about hiding out in cash for awhile, “de-risking” your portfolio.

As far as I-bonds go, I do love that they usually outperform cash investments and that they never decrease in value. I buy the full allotment in January and hold them long term. So I care less about timing– sooner or later I will get that 6 month variable rate. A 0.9% fixed rate is actually pretty good compared to recent years– not the best but much better that the teens and early 20’s when it 0, 0.1, 0.2. And considering the required waiting periods to access your money, I say do it now.

“Qualifications: This projection is based on 10 years of Treasury history in setting the I Bond’s fixed rate. But the Treasury could change course at any time and we should be aware of that. President Trump’s first-term Treasury followed the formula and has continued to do so in his second term.”

Aye, and there’s the rub, because this administration has already done so many things that most people never thought possible, let alone likely. And this is the same president who fired a BLS commissioner for statistics he didn’t like; who has been trying to jawbone the Fed into reducing short-term nominal rates; and who (as we’ve just learned in the past few days) has decided to break a tradition going back to the mid-19th century by putting his own signature on the national currency in place of the Treasurer of the United States.

Fixed income markets crave predictability–and that includes I Bond buyers, small market though we are in the overall picture–so I do hope David’s “formula” continues to hold.

While I take your point, I would guess that I bonds are somewhat niche and not a huge market. It’s hard to imagine someone in the government being interested in changing how the fixed rate is calculated. Not saying it’s impossible, just that there are much bigger fish to fry.

Ben, I 100% agree with you on all logical levels. Assuming logic continues to matter (and in this case, I think it will).

I Bonds are a rounding error – only comprising $86 billion of our $38 trillion in debt. Their balance is down from $89 billion from the year prior. Issuance, including the inflation adjustment, runs less than $6 billion per year.

EE bonds are even smaller at $27 billion.

While that means there is little to gain by changing the fixed rate formula, it also means there is little to lose by changing the formula or eliminating the program completely.

Not saying they will or are even considering such, just that the logic works both ways.

It also occurs to me, reflecting on the history of the savings bond program, that it has been paid the most attention to by Democratic administrations. Designed to help out the little guy, the securities are not marketable and sold in lower denominations. Wall Street is kept out. Large investment firms that sell mutual funds and ETF’s don’t really talk about them.

FDR founded the program in 1935 during the Great Depression. JFK championed them as “Freedom” bonds and created a payroll deduction plan. There’s a famous photo of him holding a savings bond on the Treasury Direct website somewhere I believe. I bonds were started by the Clinton administration, and boy were the fixed rates tasty in those early days!

Republicans have supported savings bonds– notably Eisenhower for the war effort and Gerald Ford bought the first “bicentennial” bond. But most changes I can think of have come under Democratic administrations. Republicans have been more interested in tax cuts and helping out the wealthy, who generally don’t bother with them. But buy enough of them over the years and they can grow to a significant amount.!

Anyway this is all by way of understanding the relative neglect of savings bonds these days. Things may not change at all for awhile.

The photo you’re referring to is at this link (scroll down the page to see it)

https://fiscaldata.treasury.gov/treasury-savings-bonds/

As always, David, thanks for such a clear concise summary of the situation–I will rest easy waiting to April 10–and then perhaps to October!

Given the expected jump in official inflation when the April housing equivalent numbers come in, seems like holding to November makes sense. All of which you’ve written about before of course. For my personal case, TIPS are likely to be the better option than I-Bonds for any new investments.

Having bought I Bonds for many years, my wife and I, like you, have begun to find TIPS attractive and are constructing a ladder, still in-progress and small, but growing.

We do this only within Roth IRAs. To my way of thinking that’s the only truly palatable place to hold TIPS, because (1) if they were held in a taxable situation, we’d have to deal with the taxation-of-“phantom interest” phenomenon; (2) if they were held in a traditional IRA, we’d have to deal with required distributions on a schedule, and in amounts, not of our own choosing, and a portion of the inflation earnings would be given over to income taxes; but (3) in a Roth, no compulsory withdrawals, and 100% of any inflation earnings are ours to keep. As should be obvious, we don’t subscribe to the view that Roth IRAs should “only” to be used, or are “best” to used, just for stocks.

Yikes, having to reply to my own reply.

As should be obvious, we don’t subscribe to the view that Roth IRAs should “only” be used, or are “best” used, just for stocks.

And I do subscribe, although sometimes forgetfully, to the view that it’s always best to proofread oneself before clicking “Reply/Submit.” 🙂

In my case, the best use-case for I-Bonds is as an emergency fund, since TIPS have the higher real rate but can fluctuate in market value. The no-penalty holding period for I-Bonds is closing in on my planned retirement point, and it’s more important for me to build a TIPS bridge from retirement to when I’ll be taking SS. Plus as you note: taxes are important, and I-Bonds can’t be placed inside of any retirement account.

(we’ve all been there for the typos)

I will point out that TipswatchChat is a very careful reader and often points out my typos and wording errors, which I appreciate (and then fix).