I am buying in April. A lot of you will disagree. There is no wrong answer.

By David Enna, Tipswatch.com

Let’s take a moment to ponder what happened in March: The United States went to war in the Mideast, gas prices surged higher, the stock market fell into chaos (briefly) and U.S. inflation took a huge leap higher.

Way down on our list of concerns was: What’s going to happen to Series I Savings Bonds at the May 1 rate reset? On February 27, I would have confidently told you:

- The variable rate was going to fall to about 2.0% from the current 3.12%.

- The fixed rate was going to fall to 0.8% from the current 0.9%.

- And the composite rate would fall (for I Bonds purchased from May to October) to about 2.81%, down from the current 4.03%.

Wrong. Wrong. Wrong.

But before we get into that, let’s look at …

I Bond basics

I Bonds are U.S. government savings bonds designed to protect your savings from inflation. They offer a combination of interest rates that adjust for inflation, making them a popular choice for conservative investors.

- The fixed rate of an I Bond will never change. Purchases through April 30, 2026, will have a fixed rate of 0.90%, which means the return will exceed official U.S. inflation by 0.9% until the I Bond is redeemed or matures in 30 years. The fixed rate will reset on May 1.

- The inflation-adjusted rate (often called the I Bond’s variable rate) changes each six months to reflect the running rate of inflation. That rate is currently 3.12%, annualized, for six months. It will adjust again on May 1, 2026, rolling into effect for all I Bonds, no matter when they were purchased.

- The current composite rate is 4.03% annualized for six months for purchases through April 2026.

I Bonds are an extremely safe and conservative investment. Interest accrues monthly and principal can never decline, even in times of deflation. Investments are limited to $10,000 per person per calendar year for electronic I Bonds held at TreasuryDirect. There is also a “gift box” strategy some investors use to stack purchases for future years.

I Bonds have many positives. For example, earnings are free of state income taxes and federal taxes can be deferred until the I Bond is redeemed or matures. Also, I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

The variable rate

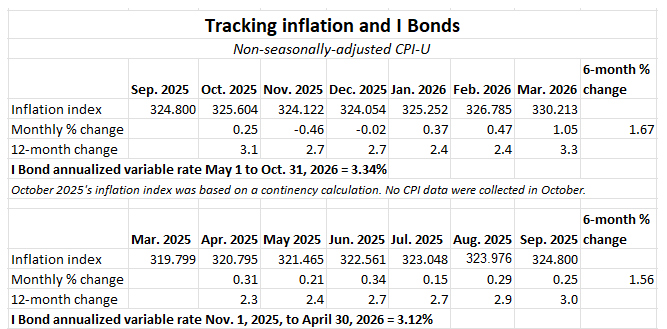

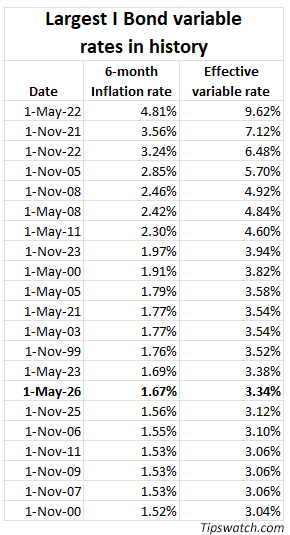

This is set in stone: Because of March’s lofty inflation, the I Bond’s inflation-adjusted variable rate will rise from the current 3.12% to a new rate of 3.34%. This is based on non-seasonally adjusted inflation for the months of October 2025 to March 2026, an increase of 1.67%. The I Bond’s rate-setting formula doubles the six-month inflation rate to create the new variable rate.

All I Bonds, no matter when they were issued, will eventually get the variable rate of 3.34% for six months, with the starting month depending on the original purchase month. From TreasuryDirect:

It’s important to remember that the new variable rate will apply to all I Bonds ever issued (no I Bonds have yet matured). A purchase in April will get that new, higher variable rate starting in October.

Conclusion: The I Bond’s variable rate will rise to 3.34% at the May 1 reset.

The fixed rate

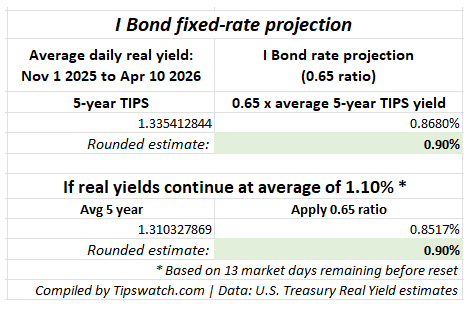

The Treasury has no legal requirement or public formula for setting the I Bond’s fixed rate. The decision is at “the discretion of the Treasury Secretary.” However, we know Treasury tracks trends in real yields and adjusts accordingly. This forecasting formula has worked for the last decade: Take the average real yield of the 5-year TIPS over the preceding six months and apply a ratio of 0.65.

For this reset, we are interested in 5-year real yields from November 2025 to April 2026. There are only 13 market days left before the reset, so we can now get a solid projection:

The formula, which has been accurate for a decade, projects that the fixed rate will remain at the current level, 0.9%. That would be true even if the 5-year real yield — currently at 1.36% — suddenly plummeted to an average of 1.10% for the next 13 market days.

However … This projection is based on 10 years of Treasury history in setting the I Bond’s fixed rate. But the Treasury could change course at any time and we should be aware of that. President Trump’s first-term Treasury followed the formula and has continued to do so in his second term.

Conclusion. It looks highly likely that the I Bond’s fixed rate will hold at 0.90%.

Composite rate

If we assume the fixed rate holds at 0.90% and the variable rate rises to 3.34%, we are looking at a new composite rate of 4.26%, up from the current 4.03%, for I Bonds purchased from May to October 2026. This is based on the formula the Treasury uses to calculate the composite rate:

[Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

If I did my math right, this formula results in the composite rate of 4.26%.

This same annualized composite rate, 4.26%, will apply to I Bonds purchased in April, after six months of earning the current rate of 4.03%.

So we know that an investor purchasing in April will earn 4.03% for six months and then 4.26% for six months, earning a combined rate of 4.16%. An investor purchasing any time from May to October will earn 4.26% for the first six months and then an undetermined rate for the next six months.

Conclusion. The I Bond’s composite rate will rise to 4.26% at the May 1 reset.

The buying decision

Buy now. As I noted at the top, I will buy my full allocation of I Bonds ($10,000 per person per year) later in April. With that decision, I know I will earn 4.16% over the next 12 months, while retaining the permanent 0.90% fixed rate. This is the “sure thing” decision, and I happen to have cash available to make the purchase.

If you are buying in April, I recommend setting the purchase date no later than April 28 on TreasuryDirect to make sure it gets processed ahead of the rate shift.

Buy later. Buying in May would be fine, but most investors who don’t buy in April will hold off investing until at least October 14, when the September inflation report is released and sets the next variable rate, to be reset November 1. At that point investors will also have a very good idea of the next fixed rate.

If you think the fixed rate could be rising in November, it makes sense to wait. Using our standard formula, the 5-year average real yield would need to rise to 1.47% over the next six months to boost the fixed rate to 1.0%. That isn’t unreasonable. So waiting could make sense.

One thing to consider is that the fixed rate announced in November will be available for purchases through April 2027, when the purchase cap resets. Also, realize that a 10-basis-point increase in the fixed rate amounts to $10 a year on a $10,000 investment. It’s not life changing.

Risks of buying now. The fixed rate soars higher in November and you feel miserable about your impatient purchase. (Not likely, but anything can happen.)

Risks of buying later. The biggest risk (also slim) is that the Treasury tosses out its traditional rate-setting formula and drops the I Bond’s fixed rate at the May reset. Another more possible risk, but not as important financially, is that inflation will plummet from April to September and the November variable rate is lower than the current 3.12%.

Short-term investment?

A combined composite rate of 4.16% looks attractive when you compare it to the nominal yields of a 4-week (3.67%) or 1-year (3.70%) T-bill. But remember that you have to hold an I Bond for one year and if you redeem at that point you lose the latest three months of interest.

Not worth it. If you buy late in April and then redeem in April 2027, you will lose the last three months of interest, meaning your total return would be 3.08%. You can do better buying a 1-year T-bill.

Rolling over I Bonds

If you are holding I Bonds with 0.0% fixed rates, you are currently earning a composite rate of 3.12%, and that will rise to 3.34% when the new variable rate kicks in. That’s not bad. There’s no reason to rush to sell these, but if you need to raise cash to purchase 0.90% I Bonds, redeeming and repurchasing makes sense.

I generally encourage people to continue holding I Bonds “until you need the cash.” It’s great to have these savings bonds growing tax-deferred with zero risk.

If you do a roll over, you will owe federal income taxes on the interest earned, and if your withdrawal is more than $10,000 (because of earned interest) you’ll only be able to buy $10,000 in new I Bonds in 2026. Also, time your redemption for early in the month because you earn no interest in the month of redemption.

Gift-box strategy

I don’t think there is a compelling need to “load up” on I Bonds in 2026, but that might change later in the year if the fixed rate surges higher. Although I have used it, I am not a fan of the gift-box strategy, mainly because the Treasury has made no attempt to clarify the rules and in fact has muddied the waters.

Conclusion

When should you purchase? There is no wrong answer. Buying in April or later in the year will likely generate similar financial returns. Getting an I Bond with a fixed rate of 0.90% remains attractive. This is a personal decision, but I still encourage investing in I Bonds as an inflation-adjusted, tax-deferred store of cash.

What are your investment plans? Discuss in the comments section!

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: New Bond Rate Projection I: 4.26% APY (3.36% variable + .9% fixed) - assetsmap

Pingback: New I-Bonds Rate Projection: 4.26% APY (Variable 3.36% + Fixed .9%) - Doctor Of Credit

Hi David,

I’m trying to figure out if I can have my cake and eat it too with some of my 3.0% to 3.6% fixed rate I-Bonds purchased from 1998 to 2001 (i.e., if I can transfer some of them to my wife’s TreasuryDirect account using FS Form 5511, generate a 1099-INT for the accumulated interest between the time they were purchased and the date of the transfer, declare the accumulated interest on our joint income tax returns in 2026 and 2027, but continue earning 6.3+% in my wife’s account). Perhaps complicating the issue is that all of my I-Bonds are registered with my wife as the co-owner.

TreasuryDirect User Guide 264 states: “Whenever a transfer is completed in your account, TreasuryDirect calculates the reportable proceeds amount from the time the Treasury marketable security was issued in your account. All your taxable transactions are available with your online, printable IRS Form 1099 each calendar year.”

31 CFR 363.55 discusses the transfer of savings bonds from one TreasuryDirect account to another.

The second-best option is to redeem $80,000 ($15k purchase price plus $65k interest) this year and next. This will save $13,000 in taxes (12% tax bracket instead of 22% bracket) and help us get the full $12,000 senior tax deduction in 2028, but it will miss out on about $5,000 interest on the $160k withdrawn early (the difference between 6.3% I-Bonds interest and 4% other alternatives).

I’ve gotten mixed messages from Treasury Retail Security Services (844) 284-2676, mostly negative.

If I try this and it doesn’t cause TreasuryDirect to generate a 1099-INT, then we’ll miss out on the $13,000 reduction in taxes by trying to get both that and the extra $5,000 in I-Bond interest.

Do you or anyone on your forum have any experience with this?

Thanks,

William B.

And, in effect, “delivering” Ibonds over $10K per year, i.e. no different than using the gift box to spouse…are the respondents to your inquiry going to be consistent with saying, “no,” b/c of the $10K cap? Hopefully, not! My point being TD has established practical waivers to its purported $10K cap…get over it gang! Have fun with tax day tomorrow. PS What you suggest to me would work but what do i know?

I’ve heard this idea before and I have no idea if you can pull it off to the satisfaction of the IRS. Even a tax attorney might shake their head, and as you note, TreasuryDirect is not helping. My plan is to start redeeming my 2031 I Bonds next year, one-fifth each year. I might even start later this year, depending on how my total AGI is looking.

I’m sure you and I will both be a little sad to redeem some of our 6.3% to 6.9% I-Bonds early (they were paying 13% when inflation was over 9%), but 28 years of that great deal has been a lot of fun—$116k purchase price growing to over $600k.

clearlyc, for what it’s worth, I have used the Form 5511 to transfer I-Bonds from our personal accounts to our Trust account, and the built-up interest stays with the bond after checking the Box a. on page 2 (I am treated as owner in the Trust).

In your case, you might want to read Section 3 on the top of page 3 of the form 5511 where it states, “lf this is a savings bond transaction, I certify that this transfer is either for the purpose of making a gift or is in response to one of these:

final judgment; court order; divorce decree; property settlement agreement; other authorized transfer”

You might be able to transfer them and separate the interest IF you take her off of Co-owner and NOT put you on as Co-owner of the new bonds AND file separate income tax forms.

I also have the dreaded cliff in 2031 and what I am doing is ROTH conversions to end my IRA RMD’s and moving taxable interest to deferred tax I-Bonds.

I’m still picking up some of the 20-30 year TIP bonds along the way right now… earning a real 2.6%+ yield above any inflation.

I recently added to my 2041 TIPS holdings, just to balance out the amounts in the ladder. 2.26% real yield.

My wife and I won’t be buying, although we understand why others will. Our reasons are, uh, quirky, idiosyncratic, private, whatever.

Through a combination of having established multiple TreasuryDirect accounts (individual, individual trust) to increase our I Bond purchases in years when we had both the inclination and surplus cash to do them, and having later discovered the “gift box” option available in the non-trust accounts, we spent several years redeeming all our I Bonds with fixed rates of 0%, 0.2%, etc., and, using the multiple accounts and gift boxes, “recycled” the proceeds into new I Bonds with fixed rates of 1.3% (the majority), 1.2%, and 1.0%.

As a result, we now have no I bonds older than 2023, so the oldest will emerge from the five-year interest penalty period in 2028. Since we’re seniors, all of our holdings have maturity dates way beyond when we expect to still be alive. We’re not inclined to redeem any of them until/unless there’s a specific need, but we could redeem $X a year for the rest of our lives and still not run out.

So we don’t really “need” more I Bonds in general, but the specific “idiosyncratic” part is that, having gone to all this trouble of “recycling” to upgrade the overall fixed rate of the portfolio, we just can’t work up any psychological enthusiasm for new I Bonds with a fixed rate less than 1.0%.

Instead, we’ve started to build a small TIPS ladder in Roth IRAs, no maturity longer than 10 years out. This has the advantage that the TIPS will mature while we’re still likely to be above ground but, unlike the I Bonds, TIPS’ future inflation adjustments and interest earnings will be tax free if/when ever withdrawn from a Roth account.

Our Roths are totally in stock market index funds, but I can see “at some point” building a Roth ladder in my Roth account. That’s the ultimate guarantee of future inflation-protected cash flow with no tax hit. Not ready to do that yet.

Yes, the tax-free aspect of holding TIPS in a Roth is one of the attractions of that location. Others are avoiding the RMDs, i.e., compulsory withdrawals at times not of our own choosing, which would apply if TIPS were held in a traditional IRA, and avoiding the “phantom interest” phenomenon if TIPS are held in a taxable situation outside any retirement account.

I have a pile of I Bonds that mature in 2035, I bought $60K in 2005 with 1% fixed rate. They have been great. I start RMD’s in 2030 so I started redeeming some in 2025 and will continue to do so ahead of the RMD’s to avoid a tax bomb in 2035. It was good timing to have that $6K senior deduction with the liquidation. I agree with David and I am going all in and buying $10K later this month.

I plan on selling some SGOV and buying before the end of the month as well. I had one I Bond I bought five years ago that I unloaded in January because of the low rate and put it in SGOV to make this determination. I would rather keep high yielding I Bonds and have dumped everything under 0.5% at the five year mark.

“A bird in the hand is worth two in the bush.” For me, this applies to an April buy, and since I have the cash I will use my allotment on this month.

Agree with NSS here. What I am doing as well, and will buy my full allotment this month. The lock of over 4% for first 12 months seemed like the right call, and odds fixed rate moving to higher than .9% before November seems unlikely.

David, with limited funds available, do you see a choice between I Bonds and the five year TIPS being auctioned on April 23?

My opinion: If this is money you want to push ahead five years, and can definitely hold for 5 years, then the TIPS makes more sense at about 1.36% real versus 0.90% for the I Bond. The return will be higher, assuming we don’t hit serious deflation, which is highly unlikely. TIPS are best purchased in a tax-deferred account, but that isn’t an absolute.

Fantastic! As I’m still young, I prefer to defer purchases as long as I can. Given I can wait until October (or November) to make a purchase, that’s what I’ll do to best try to maximize my blended fixed rate over my growing I-Bond Portfolio.

Pip pip!

If you are selling before the 5 year period, the best month to sell can often be in April. You will lose Feb, Mar, Apr interests – and these are calculated on a daily tally. This is the shortest 3 month period of the year. For this year it looks like those could also be the lowest interest rate months for 2026, but a lot depends on what month your iBond interest rate changes.

You said, “If you are selling before the 5 year period, the best month to sell can often be in April. You will lose Feb, Mar, Apr interests”.

If you sell before the end of a month, you lose that month plus the 3 prior months interest. The April interest is posted on May 1st, so in your example you would want to sell the 1st of May to lose Feb, Mar & Apr interest.

In years past I might have waited until May just to lock in the higher variable rate sooner or until November, thinking that inflation has to get worse and it would be worth grabbing the higher fixed rate at that time. But these days, long established norms seem to be easily replaced at whim without explanation or consequence. I’d hate to learn next month that Treasury has suddenly changed their usual and accepted practices surrounding I Bonds. My current thinking is to take my allotment before the end of the month.

What is your prediction for ibond rates (fixed and variable) for November and beyond should inflation continue to rise due to ongoing energy shortages.

It’s impossible to say. I would expect a short-term boost in inflation. I could see the annual rate reaching 4% in coming months, but beyond that everything is uncertain.

Did we miss…buy in April 2026 and have the option (also) in selling 15 months later when the 3 month penalty may be minimal or continue to hold?

If you redeem anytime before 5 years, you will lose that last three months of interest. But it is possible to time the move after three months of a low variable rate. So it is possible that would work after 15 months.

This is helpful. Because my wife and I each have Treasury Direct accounts, I think one of us will buy in April and one in May. Time diversification over the long run, isn’t it? Thanks for the advice.

Is there any more clarity from Treasury about their plans for this program?

I rolled over my 0% fixed rate I Bond to 1.3% but I still have another with 0.4% from 1/23. What would you recommend?

Opinion: In this case, it would depend of if you can raise the money easily for a new I Bond purchase. I still have some 0.2%, 0.3% and 0.4% I Bonds that I haven’t rolled over. Your 0.4% version (January 2023) is currently paying 3.53% and will transition to something like 3.76% at the next reset. Not bad in today’s market.

I’m glad you included this cautionary note:

Not worth it. If you buy late in April and then redeem in April 2027, you will lose the last three months of interest, meaning your total return would be 3.08%. You can do better buying a 1-year T-bill.

It illustrates the yield impact of the three month penalty for anyone thinking that today’s I Bond is a short term play. Perhaps it was back a few years ago when Inflation spiked the rate over 9%, but not now.

The real wild card in making this decision is the Iran War and the rise in oil prices above $100 per barrel due to the closing of the Strait of Hormuz. One point worth noting is the timing of the oil inflation happened to coincide with the last month of an I Bond 6-month rate change period. Had it been delayed just ome more month, the likelihood of a much higher rate in the May to October period would have resulted. As it turned out, the spike in inflation will end up smoothing out between the two 6-month periods this year. And as you’ve pointed out, nine of this matters as much as a successful and speedy conclusion to the conflict.

Looking ahead, which is always a crap shoot, it seems likely the impact of constrained oil supplies will continue to spike inflation which will permeate into shipping costs and other industries sensitive to oil prices such as airlines and shipping costs which impact many items including food. I don’t see much risk in buying an I Bond in April. You can always buy the next one in 2027 before April if it is more attractive. So the answer to the question of when to buy might very well be both, buy now and later, not now or later.

Good points, thanks. The I Bond rate-setting periods are designed to include a mix of late-year and early-year months, to smooth out the effect of variations in non-seasonally adjusted inflation. It will be interesting to see what we get in the next six months.

marce, but if the new May 2027 inflation rate goes to zero one would not look at 12 month redemption but as noted before at 15 months (really only 14 since one buys in late April) the apr for 14 months (3months of zero penalty) would be higher?

The odds of a 0% inflation rate are highly unlikely bordering on preposterous, imo.

Good question. So far I have purchased 8,800 I-bonds this year. With the last 1,200, I could just get them now or Maybe wait until October to see if there are any positive surprises. I am thinking they have to have an exit ramp for Iran war, maybe that occurs in the next month and Inflation starts to go down. Even if it goes up, there is no problem buying now, you will eventually get the higher rate. The fixed rate is harder to predict. In 6 months it could go either way. I bought most of the 10K sooner to get the 5 year clock started, that is also relevant to decision. In the end it probably will not make a material difference whether you buy now or Oct / Nov.

David, I really appreciate your insights regarding IBonds. One thing I recently came up against was how selling I bonds can affect your taxes if you also have started your RMD. My first RMD was in 2025 when I turned 73. At the same time I realized that I had a bunch of I Bonds maturing in 2030. They are great, with a relatively high interest rate. I think the purchase price was 20K, while the current value was 100K. So 80K in income. With my pension, Social Security, etc., the RMD was already bringing me close to a different tax bracket (just 24% instead of 22%), it was also bringing me close to a higher IRMAA bracket–right now I pay no IRMAA. Luckily I realized this early enough to figure out a strategy. Sell some of the 2030 I Bonds each year so that by 2030 they are all gone. That should keep me in the same tax bracket and not trigger IRMAA. Hopefully I have figured it correctly.

This is a huge issue as the early-issue I Bonds with very high fixed rates are nearing maturity. I wrote about this in Feb 2024: https://tipswatch.com/2024/02/04/long-time-i-bond-investors-face-a-tax-time-bomb/

I have a load of I Bonds maturing in 2031 and I plan to redeem them (reluctantly) over the five years 2027 to 2031 to space out the tax and IRMAA effect.

I have a similar issue and listened to your story. I have 2030 and 2033 maturities coming up. I began redemption of 25% of the 2030 tranche this year. I also have RMD’s starting in 2030 so I was trying to spread the pain. Thanks!

IRMAA gets an emotional reaction – my Medicare costs a lot more! But in reality, if you look at IRMAA as a tax instead of an insurance premium, it is a very small increase in your tax rate, roughly 1%.

If you were $1 over the 2024 MFJ limit of $218,000 MAGI, you and your spouse are this year paying an additional $2,296 (incl Part D). That is 1.05% of your $218,001 MAGI. Not so bad.

And you could have gone up to $250,000 without triggering the Net Income Investment Tax of 3.8%. Yes, a bit would be taxed at 24% instead of 22%, big woo.

You could have had MAGI of up to $273,999 without triggering the 2nd IRMAA surcharge but $23,999 might incur additional tax of 3.8%, or $912. All told, your tax rate is increased by 1.1% (ignoring 24% vs 22%).

There are additional calculations -the phasing out of the senior deductions in 2025-2028, for example, or keeping income at a level where qualified dividends and long term capital gains incur zero taxes.

It is wise to plan out your taxes as you are doing; your lump sum is big. Just be aware that sometimes minimizing taxes year by year results in paying more taxes overall, and sometimes a lot more.

The only good thing I can say about IRMAA is that is a one-year hit. Sort of like “take your medicine.” For people who don’t see it coming, and have tried to plan for adequate cash flow, and extra $191 a month can be painful. But I have said before I think IRMAA is a fair penalty for wealthier people at a time when Medicare is struggling. My biggest problem is the “cliff” nature of the tax, which makes planning your yearly AGI painstakingly difficult.

Nobody likes to pay extra, but if you have over $200,000 of income (MFJ) so subject to (IRMAA), it is hard to imagine you have a cash flow problem, and if someone does, that is on them.

IRMAA is not recent, it was part of a Medicare overhaul during the W Bush administration. From 2010 to 2020 the brackets weren’t even adjusted for inflation!

The cliff nature is less bothersome to me (see below) than the govt announcing in Nov 2025 what your income needed to be in 2024 to avoid IRMAA surcharges in 2026. Even then, I just put a 2% or so inflation factor on the most recently announced limits to estimate future IRMAA levels.

If not a cliff, then the people would likely complain that their Medicare premium changes with each $1,000 increase in income, and who can plan to that level? Replacing a big cliff with a bunch of small cliffs as it were.

Planning is not really that challenging in most cases, but I know most people don’t do it, or in the face of uncertainty give up rather than making reasonable estimates and allowing sufficient margin for error.

I am all for tax simplification, but it isn’t going to happen.

In the meantime, spreadsheets are our friend!

I realized a couple years ago I would be slightly over the expected first level of IRMAA because of Roth conversions and one surprise capital gain. So at the end of the year I did more Roth conversions to fill up the second level, and now … I am paying 2nd-level IRMAA, for just one year. The IRMAA levels that will be announced in November 2026 apply to the tax return you just filed for 2025. There is no way to know the EXACT levels when you file your taxes.

When taxes give you lemons, make lemonade! Great pivot. You converted roughly an additional $120,000, which will reduce your future RMDs by ~$5,000 per year. It will also remove $120,000 from the possibility of higher tax rates at withdrawal after one spouse dies, or both have died and your heirs are on the 10 year withdrawal path. Excluding any NIIT, your IRMAA added under 1.7% to your tax rate. Not pleasant, but not huge.

It is not always possible, but I have worked my portfolio to try to eliminate surprise capital gains.

I certainly leave a cushion because I don’t know the exact limit. Over the long term, the “unused” amount is immaterial. Really, we will never know if our tax savings strategies worked or not, because we will be dead, assuming we die with some pretax account balances. It is all a guess. We don’t know future tax rates, our dates of death, nor the tax rates of our heirs nor whether they will withdraw the money in a tax efficient manner.

We simply make decisions based on the information we have today, and adjust every year as life and the government throw missiles at us.

Ever since I have had to take RMDs (a few years now), I have offset some or most of that income with QCDs (qualified charitable distributions). Of course, I cannot take itemized deductions for those donations, but I no longer have enough to benefit from itemizing (vs. standard deduction). My RMDs are relatively small anyhow, as I made a number of Traditional IRA to Roth IRA conversions in years when my income was low.

I sure wish I knew about I BONDS in “98” when I was 29 years old $$$

I worked for Lockheed Martin in the ’90s. They practically forced us to buy Ibonds (as a payroll deduction) to please their “client”. I resented it but looking back it was a great investment. High real returns.

What a bonanza they’ve been! I am fortunate to have had the instinct and the money to have purchased large allocations in 1999, 2001, and a lesser amount in 2002. Back then everyone was crazed about dot com start-ups, a bubble which broke. Who knew that a many years-long desert of close to zero interest rates lay ahead? Like others on this blog, I face a federal tax bomb on the near horizon when all those I-bonds mature.

Thanks, David! I’m not buying right now but will consider later this year if the fixed rate rises. I have a ton more bonds than I ever imagined (all TIPS and I-bonds) thanks to your columns. Still have lots of cash, which I have to work to get the best short term rates on.