By David Enna, Tipswatch.com

As U.S. annual inflation rises toward 4%, investor interest in inflation-protected investments is also on the rise, making this week’s reopening auction of a 10-year Treasury Inflation-Protected Security one to watch.

This is CUSIP 91282CPU9, with a term of 9 years, 8 months. It had its originating auction on Jan. 22, when it got a real yield to maturity of 1.949% and a coupon rate of 1.875%. The first reopening auction, on March 19, got a real yield of 1.896%. There is a good possibility this week’s auction will top those yields.

This TIPS trades on the secondary market, and it closed Friday with a real yield to maturity of 2.07%, a jump of about 14 basis points from a week earlier. The U.S. Treasury market is now adjusting to a future with: 1) a lengthy period of high energy prices, 2) the potential for months of climbing U.S. inflation, 3) a growing possibility of Federal Reserve rate increases, and 4) a continual rise in U.S. budget deficits.

Definition: The “real yield to maturity” of a TIPS is its yield above future U.S. inflation, over the term of the TIPS. So a real yield of 2.07% means an investment in this TIPS would provide a return that exceeds official U.S. inflation by 2.07% for 9 years, 8 months.

Many investors assume that when inflation expectations rise, real yields will soar higher. But that is not exactly the case. In a period of rising inflation expectations, the nominal Treasury yield will rise faster than the TIPS yield. Since the beginning of the war with Iran:

- The nominal yield of a 10-year Treasury note has increased 62 basis points.

- The real yield of a 10-year TIPS has increased 38 basis points.

- The inflation breakeven rate has increased 24 basis points.

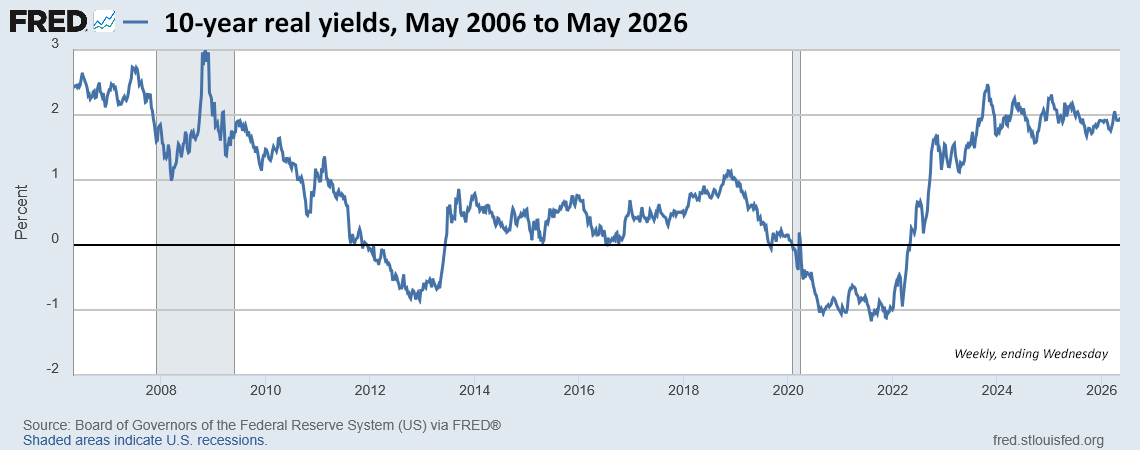

At this point, I’d say it’s impossible to predict where the auction’s real yield will fall, but it looks likely to break through the 2.0% barrier for the first time in a year. Here is the trend in the 10-year real yield over the last 20 years and across two recessions:

The 20-year view is interesting because it reaches back before the period of Federal Reserve activism to force interest rates lower. Before the Great Recession of late 2007 to mid 2009, the 10-year real yield was solidly above 2.0%. In July 2007, a 10-year TIPS auctioned with a real yield of 2.749%. At the time, the 10-year Treasury note was yielding 5.11%, creating an inflation breakeven rate of 2.36%, lower than we are seeing today.

I don’t think we will see a repeat of 2007, but isn’t it possible that the 10-year nominal will rise to 5% and the 10-year TIPS to as high as 2.5%? Maybe, but not at this auction.

Pricing

Because the auctioned real yield is likely to be above the coupon rate of 1.875%, CUSIP 91282CPU9 will almost certainly get a discount on its unadjusted price. (It is currently trading with a price of 98.30.) However, it will carry a fairly sizable inflation index of 1.01522 on the settlement date of May 29. If the real yield holds at the current 2.07% (not likely), this is what the investment cost will look like for a $10,000 par value purchase:

- Par value: $10,000

- Principal purchased on settlement date: $10,000 x 1.01522 = $10,152.20

- Cost of investment = $10,152.20 x 0.9830 = $9,979.61

- + accrued interest of about $70.46.

Again, this is a forecast based on the Friday close. The market will change before Thursday’s auction, but it looks highly like that the cost will remain below par value, even with the extra accrued principal. The accrued interest will be returned at the first coupon payment on July 15.

Inflation breakeven rate

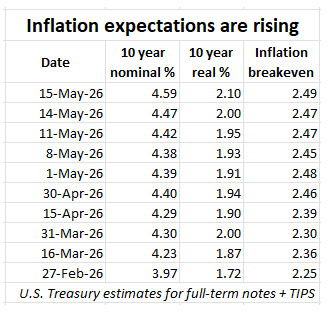

The 10-year Treasury note closed Friday with a nominal yield of 4.59%, which creates an inflation breakeven rate of 2.52% for this TIPS at its current real yield of 2.07% on the secondary market. If that breakeven rate holds, it would be the highest since an auction in May 2022 at 2.61%.

A high inflation breakeven rate indicates a TIPS is more “expensive” versus a Treasury of the same term. At some point, you might shift your focus to the nominal Treasury. Think inflation will average less than 2.52% over the next 10 years? Buy the Treasury note. (FYI, inflation over the last 10 years has averaged 3.4%.)

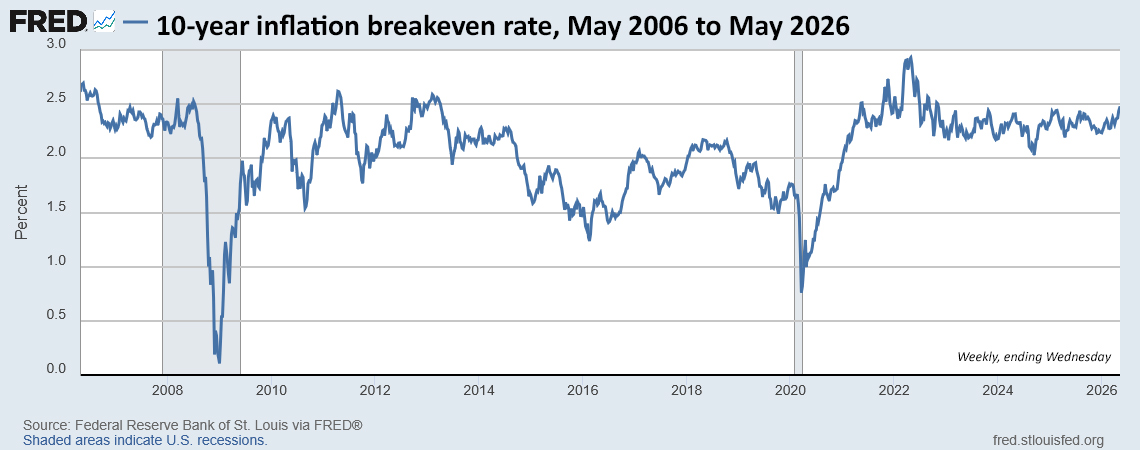

Here is the trend in the 10-year inflation breakeven rate over the last 20 years:

Note the wild dips lower during times of recession. Since early 2022, however, inflation expectations have hovered in a range of 2.2% to 2.5%. We are now at the high end of that range — thanks to a lingering oil-price shock.

Thoughts

I won’t be a buyer at this auction since I bought my full TIPS-ladder allocation for 2036 at the January auction.

There is no overriding reason to wait until the auction to purchase this TIPS, which will be trading on the secondary market all week. If you see a real yield that you like, buy it in a brokerage account.

The advantage of buying at auction, especially through TreasuryDirect, is that even small-lot purchases will get the auction’s high yield. The advantage of the secondary market is that you can see exactly the price and real yield you will be receiving. The negative is that you may face a small bid-ask spread. Most of the time, it doesn’t make a huge difference, but if you see a real yield you like, know that you can probably get it on the secondary market without dealing with the auction’s uncertainty.

This TIPS auction closes Thursday at 1 p.m. ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

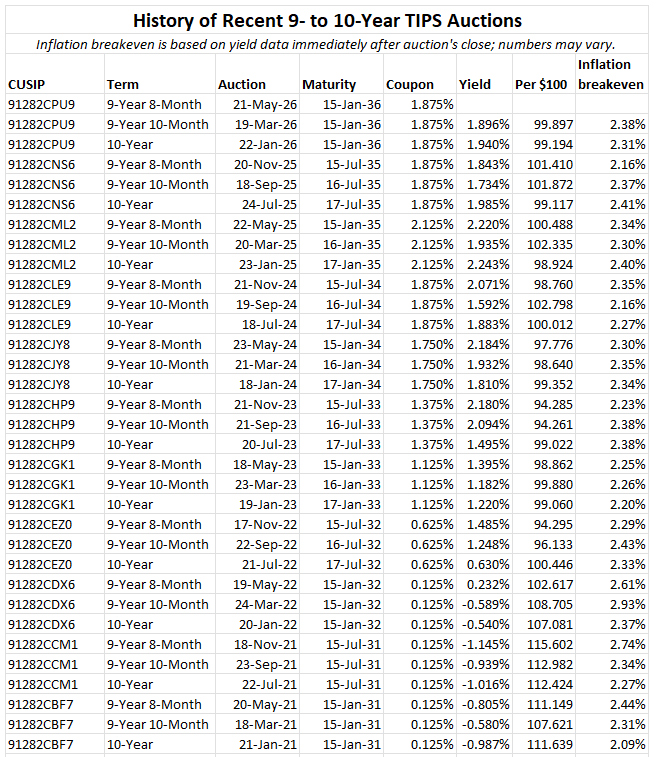

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I would never hold TIP bonds in my emergency fund for any possible near-term needs.

I use the lower yielding money market funds, shorter-term CDs, and I bonds for that forced sale/need cash now type of scenario insurance.

Sorry, this post was supposed to be below responding to Chris B concerns.

I have excess of 91282CJY8 maturing in 2034. Should I sell some and then buy the one maturing in 2036?

In buying to hold TIP bonds you will always see the current market price of your holdings (what you could sell the bond for today) fluctuate sometimes a lot over the months and the years as you wait to collect your guaranteed return at maturity.

I, for myself, do tend to prefer the TIP bonds that yield some amount of ever-growing cash flow in interest payments to reinvest along the way.

I read that the 20-30 year out TIP bonds are trading near a 24-year high on Real yields these days.

Yes, but if you have to sell for any reason and don’t hold to maturity, you could suffer serious losses. With the current environment, long term rates are going up.

How long and how much higher rates you expect for a 20 year bond? What if there is an Iran deal in the next week or two? I am seriously considering 20 year Treasury bonds at Wednesday’s auction. I know no one knows for sure where interest rates may be with inflation, war, potentially new fed chair reducing its balance sheet, all the capital investments in AI infrastructure, inflation expectations going up, and the national debt. Your and views by others are most welcome…thanks!!!

I plan to buy at auction if the real yield holds around 2.05%. For me the ideal 10-year TIPS would have at least a 2% real yield, 2% coupon and unadjusted price below par value. I almost bought last May but got cold feet. After missing two opportunities in 2025, I’ve realized that good enough is what matters in investing.

I bought some of the 10 year TIPS on Friday on the secondary market. I was happy to get over 2% real yield. Inflation is not a good thing, and it’s great to have inflation protection.

I couldn’t wait so I bought 30Y TIPS on Friday at 2.810% Real YTM.

Watching real yields has gotten very addictive recently 🙂

There is no law that says we can’t split a 10 Year Treasury purchase between the standard 10 year bonds and the 10 year TIPS.

Based upon the above article, perhaps it might be best to diversify with 50% of the funds going to the standard 10 years Treasury and 50% going to the 10 year TIPS. Neither looks like a bad choice at this time.

I bought these in January, so not a buyer this week. The 20 year (CUSIP 912810UV8) nominal bond auction this week is interesting though with rates trending at 5%+.

This is just an impression, not based on numbers, but it seems like the bond market in general is more sensitive/reactive than usual lately. Oil is up! Oil is down! Hormuz will reopen! No it won’t! The Iran war is over! The Iran war is just taking a breather before starting up again! There’s going to be even more serious inflation! There’s going to be a recession!

To a certain extent that’s always true, i.e., markets don’t like uncertainty, but nevertheless lately I have the sensation of peering into a financial pinball machine as sentiment ricochets back-and-forth.

If I were buying this 2036 TIPS–which I’m still trying to decide whether to do–I’d be inclined to do it on the secondary market, knowing exactly what I’d be getting, instead of doing the auction and only learning through hindsight whether it was a “really good” or “just so-so” day to be buying. . . . But then, the true “macro” answer to that question will be revealed over the course of the bond’s maturity life.