By David Enna, Tipswatch.com

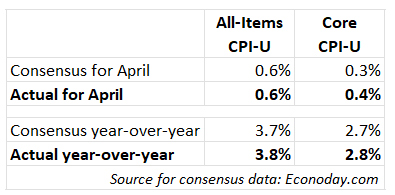

The lingering war in the Mideast, and its oil-price shock, sent U.S. seasonally-adjusted inflation 0.6% higher in April and pushed the annual rate to 3.8%, its highest level since May 2023, the Bureau of Labor Statistics reported today.

Core inflation rose 0.4% for the month and 2.8% for the year — both numbers higher than expectations.

Economists expected an ugly report for April, but this was a bit uglier than forecast. Gasoline costs were a key factor, of course, rising 5.4% in the month after soaring 21.2% in March. Gas prices are now up 28.4% over the last year. The BLS said energy costs accounted for 40% of the all-items increase.

Shelter costs rose 0.6% for the month, a high number that was boosted by April survey data replacing missing data for October 2025. For October, when no data were collected, BLS set shelter inflation at 0.0%, obviously too low. This report begins to bring annual inflation back into line. Did shelter costs truly rise 0.6%? Probably not.

Also in the report:

- Food at home costs increased a disturbing 0.7% in April, after falling 0.2% in March. The annual rate is now 2.9%.

- Costs of fruits and vegetables were up 1.8% for the month and 6.1% for the year.

- Beef prices rose 2.7% for the month.

- Apparel costs rose 0.6% for the month and 4.2% for the year.

- Airline fares were up 2.8% for the month and are now up 20.7% for the year.

- Costs of new vehicles fell 0.2% for the month and are up only 0.2% for the year.

- Costs of used cars and trucks were flat for the month.

- Costs of medical care services were flat but up 3.2% for the year.

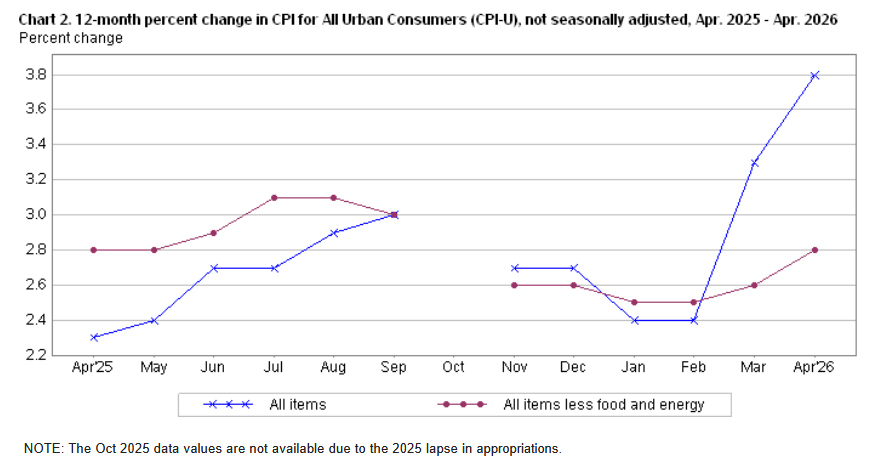

Although gasoline and shelter dominated this April report, there were many signs of inflation creeping across the economy — food, airline fares, household furnishings, apparel, etc. The result is this very scary chart:

Wednesday update: Producer prices

From Reuters: U.S. producer prices increased more than expected in April, posting their biggest gain since early 2022. The Producer Price Index for final demand surged 1.4% last month after an upwardly revised 0.7% advance in March. In the 12 months through April, the PPI jumped 6.0%. That was the largest increase since December 2022.

What this means for TIPS and I Bonds

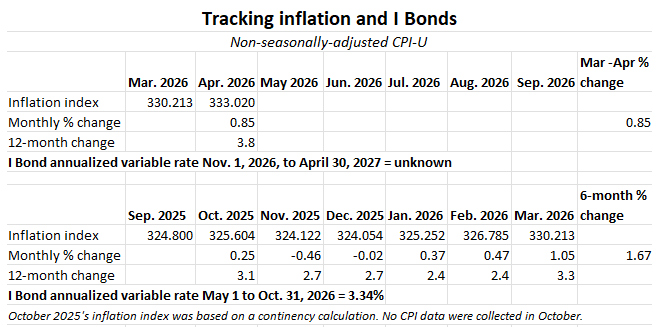

Investors in Treasury Inflation-Protected Securities and Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For April, the BLS set the inflation index at 333.020, an increase of 0.85% over the March number.

For TIPS. The April report means that principal balances for all TIPS will rise 0.85% in June after rising 1.05% in March. These are gaudy numbers, but will be balanced off later in the year when non-seasonally-adjusted inflation runs lower than the seasonally-adjusted version. Here are the new June Inflation Indexes for all TIPS.

For I Bonds. April is the first of a six-month string that will determine the I Bond’s new variable rate, which will be reset November 1. We can’t draw any conclusions from this one-month 0.85% increase, but I can say it is the highest April number over the last 14 years I have been tracking this data.

What this means for future interest rates

We can be certain the Federal Reserve, even under Kevin Warsh’s new leadership, will not be cutting short-term interest rates until this energy shock settles down and we can see the lasting results.

With inflation surging, should the Fed be raising interest rates? Also not likely, especially if the U.S. economy begins slowing down under the weight of energy costs. So I am thinking we are in a period of uneasy stability for short-term rates.

From today’s Bloomberg report:

Even if the current ceasefire holds and the Strait of Hormuz reopens soon, economists anticipate higher costs are likely to persist in the months ahead as oil output normalizes and shipping flows recover. …

The FOMC is likely to be concerned by renewed signs of food inflation accelerating, given the risk that higher gasoline and food prices together will further boost households’ inflation expectations.

And the Wall Street Journal:

The April report is the latest sign that the rate cuts that markets were pricing in at the start of the year are no longer a 2026 story. … Now, the policy debate within the Fed has shifted away from when to cut rates and toward when to start signaling that a rate hike is as likely as a rate cut.

It’s possible we could see inflation begin to stabilize in coming months, while remaining in a range around 4.0%. That is not the set-up for cuts in interest rates. And once again, we can see the value in investing in inflation protection.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I predict the Fed’s next move will be a rate hike, not a cut. And the November I-Bond fixed rate will be > 0.9%. And the 10-year nominal Treasury will be at 5.0% by year’s end.

Good times if you are fixed income investors. Otherwise – yikes.

Hard sell off in the bond market worldwide today. So far this year cash has been a good place to be because rising yields are eating into the coupon wall that bonds have.

Drmattnyc, maybe the market is reacting to the fact that Trump’s trip to China offered no path toward ending the Iran hostilities. Inflation is rising at the same time budget deficits are rising. Not a good picture for the Treasury market. Next week’s 10-year TIPS auction will be interesting. I will be posting an analysis Sunday morning.

I’ve already committed in this auction for some. I just keep building on those bond ladders with the hard-earned capital (profits) that I don’t want to lose.

I’m very curious to see how high nominal bond yields go before they do something to rein it in.

If nominal yields are high but so is inflation, that doesn’t necessarily mean high real yields, right? I’m really foggy on what drives real yields.

I am addressing the real yield issue in my auction preview article, publishing Sunday morning.

I hold a large amount of I bonds and EE bonds but have not as yet redeemed any. I do not use C of I or the gift box. I just received an e mail from TD a few hours ago stating “Dear TD customer,

While tackling spring cleaning, don’t forget to tidy up your digital spaces too– including your Treasury Direct account. Maintain good TD account hygiene by checking your bank information accuracy to ensure that future payments (big ones loom in the next 3-5 years when my I bonds mature) are being sent to the right bank account. If you confirm your bank information is correct, you don’t need to take further action.

The letter then goes on to give instruction on how to check your bank information.Did anyone else get this? More evidence of imminent changes?

Sometimes, when I log in, it asks me to confirm my bank info. Maybe you haven’t done that in a while?

I have $1 in the C of I in two different entity accounts. They’ve been asking me to withdraw that, but there’s no way I’m touching it—I made those deposits to test an alternate bank account connection and got locked out of the accounts when I did. They can keep the dollar or mail me a check.

Anyway, this might be related to them phasing out the C of I and the automated system asking everyone who hasn’t verified their bank info recently to do so. Best guess.

Ben, with only $1 at risk, I think you are making a wise choice. I got the email today advising a check-in on my banking info. So it’s possible the switchover is accelerating.

Anyone else get the email “TreasuryDirect: How Certificates of Indebtedness Can Help Fund Summer Fun”?

What is interesting is I don’t have any C of I. And have never used that feature. I always go direct from bank account. Odd. Possibly another sign of things to come? Glitch in the matrix?

“Why You Should Take Action

Our records show that your account holds unredeemed C of I. C of I is a non-interest-earning Treasury security, so holding funds in C of I limits their growth potential.”

This is good advice from TreasuryDirect, since no one should be holding cash in a zero-interest account. But the upbeat tone is strange. This isn’t new, but I can’t see why you got the email. (I didn’t and don’t use C of I.)

How many meetings do you think were involved in the drafting of that message?

I’ll bet more than one.

For those of you who dislike the treasuryDirect website (clunky, outdated etc) it is going to disappear completely. They are in process of transitioning to a new platform called “mytreasury” that is cloud based and you will even have a phone app. Of course it is taking longer than originally planned and it is also costing more than originally planned. The gift box will disappear, you will still be able to gift I-bonds, but directly. We will see if buying or delivery limits change. They are very slow and careful because they don’t want to interrupt the huge amount of transaction that occur every week.

Interesting information, and seems believable. However, what is your source? (Also, moving to an app-enabled site might have us all begging for a return to the old TreasuryDirect. I’d expect this transition to have some major potholes.)

This is from Claude, backing up your hypothesis: A May 2025 project update indicated that work is continuing to build out the system. So as of today (May 2026), myTreasury is still in development — TreasuryDirect remains the active platform for buying and managing Treasury securities.

The bottom line: myTreasury is the intended successor to TreasuryDirect, but it’s been more than a decade in the making, has faced serious technical setbacks, and there’s no confirmed public launch date yet. If you’re currently using TreasuryDirect, nothing is changing for you in the near term.

If Treasury Direct has been a relatively secure platform, shouldn’t the Treasury proceed cautiously about implementing an unproven cloud based system, particularly with the US government’s track record with losing personal data?

Is Claude the old/new AI? I googled mytreasury and saw the same plus

Claude is Anthropic’s AI. It gave a much more detailed answer but I grabbed a snippet. Claude allows anonymous searching and it seems quite good.

Oh man. I like the treasury direct website. I like old simple stuff that has been well tested and works. I don’t like newfangled cloud services. I’ve had all sorts of trouble with more than one of them.

Good reminder to save account statements and double check everything after the transition.

I am sorry for all the travails of those on this blog of dealing with Treasury Direct. But isn’t it also nice to have an investment vehicle, conservative and quirky as it is, away from the reach of Wall Street and the mutual fund companies? Think of how lucky you were to hold I bonds and EE bonds in 2022 when bond mutual funds were torpedoed by rapidly rising interest rates. TD is the only place to buy I bonds and if you stick to online purchases and redemptions, it’s ok.

It’s more than okay, it works, it’s safe, and it’s secure. When inflation drops, you can even redeem them while minimizing the three month penalty as I did when the rate dropped to 1.90%.

I’ll go further. I also use TD to buy treasuries, mostly t-bills. I select a term that gets me to my next property tax payment so the maturing principal will be there (always reliable) to make those payments while earning state tax-free interest (I live in a high tax state).

The TD site is outdated in its design but completely functional and stable. I believe it is being revamped with all the hoopla about delivering gifts from the gift box. The biggest drawbacks I see are the long wait times due to severe understaffing for special circumstances or PODs. That could be a major issue when those things happen, but normal use works fine. The phone support is decent enough.

I also want to comment on TD phone support. I inadvertently placed an order for $10K TIPS on TD rather than an I-Bond. I only use TD for I-Bonds and had just placed an order for TIPS in my IRA at Fidelity. I called TD frantic that I’d now have to deal with Phantom Income and got a lovely person who walked me through the process of canceling the TIPS order and submitting an order for the I-Bond. She even stayed on the phone to be sure I had entered everything correctly.

TD phone support? Very good, in my experience. I forget why I had to call them (probably a stupid mistake on my part and this was a few years ago) but I had someone on the phone quickly and the problem solved right away.

I haven’t had any issues dealing with Treasury Direct and have called a few times, converted paper bonds multiple times, and multiple estate transfers to multiple parties. My last experience was maybe 4 years ago though.

I wondered about registering new purchases as co-owners, or POD to spouse. From recent postings, it seems for co-owners that transferring bonds requires a form and a wait, whereas single owner with POD can just be transferred online. Given that you can indeed transfer I bonds to your spouse and trigger tax on the accumulated interest without redeeming the bond, seems like single owner POD is the way to go in registration. Triggering the tax at time of transfer is pretty useful for managing future lump sum maturities.

Oil prices feed into the prices of pretty much all sectors of the economy, including core CPI, mainly through higher transportation and energy costs, along with increased manufacturing costs. So when the price of gasoline goes up, you can be pretty sure the price of everything else is going to go up.

For example, the price of food will go up because all food is delivered by trucks. Truckers are paying more for gasoline so they are charging more for deliveries. Grocery stores increase the price of most products to pay the higher cost of deliveries. Your local plumber sees food prices going up, so he starts charging more per hour. Service workers start clamoring for higher wages. It’s the old wage-price spiral.

Inflation impacts people differently. People who do not buy a lot of goods or demand a lot of services are less affected. For me, I am happy that the I-bond variable rate will be going up. BTW, today the 30 year Treasury bond just blew past 5%.

I don’t see how that inflation will be coming down much in the next few months with the current high energy and fertilizer costs extended projections.

Indeed! We’re likely at least 3 months away before the US starts to see the real impact of the disruptions to the oil market, and up to 6 months from seeing the full impact.

My intent to “defer the decision as late as possible” on I-Bonds remains prudent, and I’ll be making this year’s purchase in late October 2026. Next year I’ll wait until late April to determine if I purchase then or again defer to late October for 2027.

I’m still at least five years (possibly ten!) too young to start building the first rungs of my TIPS ladder for early retirement, but these times will be interesting to observe nonetheless. It’ll be interesting to see how TIPS fare versus a low-cost index such as BND over the next few years.

Pip pip!

Last month I pointed out that the I Bond rate would be smoothed out by timing, because the first spike in inflation due to the war occurred during the final month of the May 1 reset, and the second would occur during the first month of the next period. With today’s CPI Report being as bad as expected, or even worse, I decided to ask Chat GPT what the rate would be if the reset period shifted one month forward. In other words, what would the composite rate have been if you lopped off the September CPI and included April. Here’s what it calculated:

Today’s April CPI report showed the NSA CPI-U at 333.020.

So if you hypothetically shifted the calculation window forward one month — effectively using April instead of March — the numbers would look roughly like this:

Actual May 2026 semiannual inflation factor: about 1.66%

Hypothetical factor using April CPI: about 2.58%

Annualized variable rate: about 5.16%–5.18%

Using the current fixed rate of 0.90%, the composite rate formula is:

Where:

F = 0.009

I \approx 0.0258

That produces a hypothetical composite I Bond rate of approximately:

6.1%

instead of the actual 4.26% announced for May–October 2026.

OK, I did the same calculation: The six-month inflation rate was 1.65%. Subtract October’s 0.25% and add April’s 0.85%, and you get 2.25%, which equates to a variable rate of 4.50%. Add in the 0.9% fixed rate and you get a composite rate of 5.42%.

This is why we invest in TIPS and I Bonds. Thanks for your continued efforts to keep us educated.

Edward, thank you for sharing your horror story of interacting with Treasury Direct. Just when I start sniffing around I-bonds again; your story hardens my resolve to not invest in TD again.

Unrelated to this particular post. but i think a good reminder for people who use Treasury Direct. On February 25, 2025, I purchased a 30 year treasury note on the Treasury Direct website no problems it worked as expected. My ignorance was that I didn’t realize that you can not sell securites inside the Treasury Direct account. So I began the process of transfering the security to my brokerage account( discount broker). On July 15, 2025, I initiated a transfer request going through my brokerage account to transfer the security from the Treasury Direct Account to my brokerage account, that took about two weeks to complete. (I went this route because we do not have a Medallion Signature Guarantee in the small town where we live.) I finally got notice that Treasury Direct received the transfer request through an email on August 14, 2025. Then I waited. I called Treasury Direct every few months to check on the status. Once they tried to tell me that there was no request under my name, so I gave them the Transfer Request number, and they were finally able to find it. (Always keep your evidence of the transfer.) I was informed every time I called that it was an extra ordinary request, and that it could take up to 12 months to complete. I finally received notification May 6, 2026 that the transfer had completed and indeed it showed up in my brokerage account on that date. Lessons learned through trial. 🙂

I would caution all who use Treasury Direct to consider whether your purchase could be done in a brokerage account. I know you can’t buy I Bonds via brokerage. I’ve had an account with them for over 25 years, and I am winding down my I-bonds as they approach maturity. Mr. Howard’s example is one of many I’ve read about the trials of using Treasury Direct. Think about how bad this could turn if your heirs had to deal with TD? Best to all!

Thank you for writing about your experience. I Guess your lucky it was done in under 1 year.

I only use TD for I-bonds because brokers will not deal with savings bonds. I buy all my treasuries using my broker. There are no commissions to buy or sell. However, you must buy or sell them in $1,000 increments. I realize TD allows you to buy smaller amounts. However, the TD site is messed up, for many reasons outlined in Tipswatch and in its comments and is best avoided, except for savings bonds because we have no choice.

With the 10 Year TIPS auction opening on May 14th, we shall see what the yield will do. I would wager that it will be over 2% as of now it’s 1.95.

Thank you for your speedy post.

Can you say more on your thought process here? I was wondering if there would be increased demand because of the headline-generating inflation numbers, which then would drive down the real yield.

As it stands now, that 10-year TIPS auction could generate a real yield of 2%, definitely. But there is a lot of volatility and that auction is 9 days away. I will be posting a preview article on that auction Sunday morning.

I think yields will rise from here unless there is a major announcement on the war, otherwise they will drift upwards as the expectation is that inflation will continue to run higher the next few months. So the 10yr at 2% is a ‘real’ possibility and I’ll be a buyer… thanks for all your insights and the articles you put out. I’ve learnt a lot over the years!

The big question I have is will Wednesday’s 30-year bond auction price with a 5 handle. It’s just above 5 this morning.

Results are in: 5.046% high yield. First 5% coupon on a 30-year bond auction since November 2007.