By David Enna, Tipswatch.com

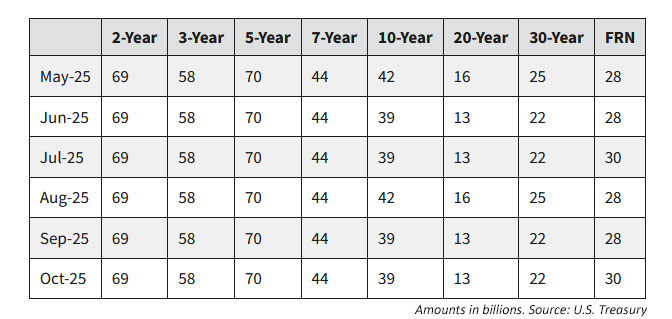

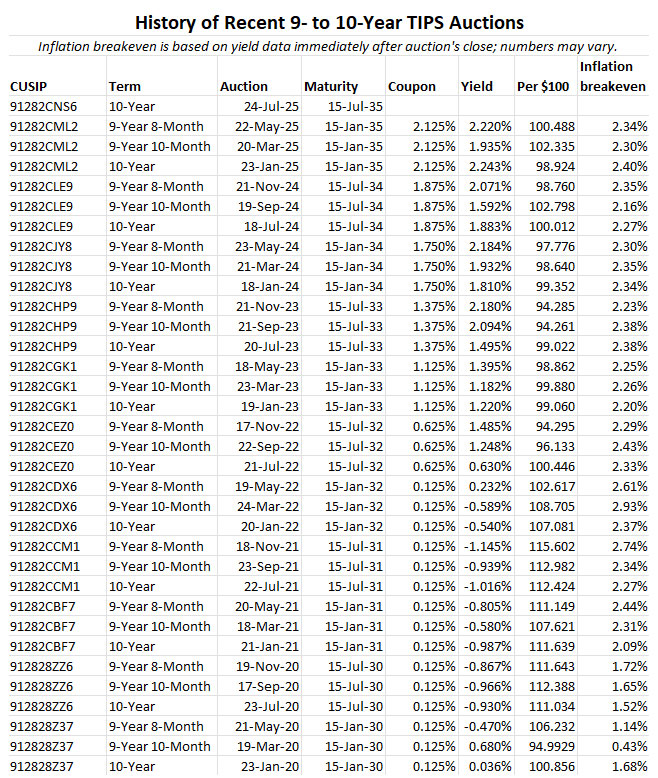

For quite awhile, when I am writing about originating auctions for 5- and 10-year Treasury Inflation-Protected Securities, I note “this new auction is the largest in history for this term.” It has been happening every year since 2021.

The Treasury last week issued its funding plan for the 3rd quarter of 2025, and it is again increasing auction sizes for 5- and 10-year TIPS, while leaving the 30-year auction as is. There will be three TIPS auctions in the 3rd quarter:

- 30-year, August 21. Treasury will offer $8 billion in a reopening auction, the same size as all 30-year reopening auctions over the last five years. In February 2021, the size of the 30-year TIPS originating auction increased from $8 billion to $9 billion and has stayed at that level.

- 10-year, September 18. $19 billion will be offered in a reopening auction, up from $18 billion at the last reopening in May.

- 5-year, October 23. $26 billion will be offered in an originating auction, up from $25 billion at the last originating auction in April.

The chart demonstrates that TIPS issuance is heavily weighted to the 5-year (2 new issues a year and 2 reopenings) and the 10-year (2 new issues a year and 4 reopenings). The 30-year is left with just one originating and one reopening at much smaller amounts.

Treasury offers this reasoning for the steady ramp-up of TIPS auction sizes:

Given the intermediate- to long-term borrowing outlook and the structural balance of supply and demand for TIPS, Treasury believes it would be prudent to continue with incremental increases to TIPS auction sizes this quarter.

Because TIPS are the only tradable Treasury security with a return linked to inflation, they are unique. The Treasury and its primary dealers apparently want to preserve the balance of real vs. nominal investments as the U.S. debt continues to increase. Plus, there are only 3 terms of TIPS (5, 10, 30) versus 14 terms (4-week to 30 years) on the nominal side. The Treasury clearly feels demand is highest for the 5- and 10-year terms for TIPS.

What about nominals?

Treasury says it believes the size of its note, bond and floating rate issues are “well positioned” and no changes will be coming “for the next several quarters.”

T-bills. Treasury didn’t provide specific information on issuance of Treasury bills in the 3rd quarter, but these auctions are likely to increase in size, possibly into 2026. It noted:

Since the $5 trillion increase to the debt limit on July 4, Treasury has increased bill issuance to continue to finance the government and to gradually rebuild the cash balance over time to a level more consistent with its cash balance policy.

This policy reflects a strategic move to shorter-term issues, and maybe a bit of a gamble that longer-term Treasury yields will decline next year.

Treasury anticipates further marginal increases in short-dated Treasury bill auction sizes in the coming days and then maintaining sizes at or near those levels through the end of September. Additional increases to Treasury bill auction sizes are anticipated in October.

At any rate, the U.S. faces steadily higher fiscal deficits in coming years. This is from a July 30 analysis by T.Rowe Price:

The U.S. government will need to issue more Treasury debt to fund its package of tax cut extensions and new spending cuts. Combined with new outlays on defense and immigration enforcement, the Congressional Budget Office estimates that the tax breaks and spending will boost the budget deficit by more than $3 trillion USD over the next 10 years (excluding the effects of any tariff revenue). …

Treasury Secretary Scott Bessent has stated that the Treasury Department will initially issue most of the new supply in the bill market as opposed to coupons. This would take advantage of the low yields on short-maturity debt relative to long-maturity debt and help restrain the government’s total interest costs.

Conclusion

Some investors have expressed fears that the threat of higher inflation would discourage the Treasury from issuing TIPS in the future. There is no evidence that is happening, and in fact TIPS issuance continues to climb. TIPS remain a solid element of U.S. government financing.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing

Certainly looks like a wait and see until mid-October situation for I-Bond purchases.