Back on May 1, I wrote an article about how the new I Bond inflation adjusted variable rate had fallen into the deep negative, -1.60% (annualized). And this meant any Series I Savings Bond with a fixed rate of 1.6% or less would pay 0.0% for six months.

Since then several readers have commented that they aren’t seeing the 0.0% rate in the Savings Bond Wizard. Others have cursed me and told me I have it all wrong, believing that the fixed rate is ‘fixed’ and can never be reduced. Others are just confused.

If you use the Treasury’s Savings Bond Wizard, you are going to see some misleading numbers for awhile, but they aren’t wrong. (I love the Wizard, by the way, it is an excellent tool.) If you have it, open it up today and get the latest update, which provides interest rates through November 2015.

But first, read this …

How is that rate calculated? The Treasury Direct site has a lot of great information on I Bonds, including a very good Rates & Terms page. This chart showing the I Bond rate formula is drawn from that page:

OK, it’s obvious if the fixed rate is 0.0% and the inflation rate is negative, the composite rate is going to drop to 0.0%, the lowest possible. But what if your fixed rate is 3.0%, as it was back in the good old days (May to November 2001)? What will happen to your fixed rate under that formula? Here is the calculation:

OK, it’s obvious if the fixed rate is 0.0% and the inflation rate is negative, the composite rate is going to drop to 0.0%, the lowest possible. But what if your fixed rate is 3.0%, as it was back in the good old days (May to November 2001)? What will happen to your fixed rate under that formula? Here is the calculation:

[0.0300 + (2 x -0.0080) + (0.0300 x -0.0080)]

[0.0300 + -0.0160 + – 0.00024]

0.01376

resulting in a composite rate of 1.38%

So, according to the Treasury formula, your fixed rate will be lowered by the negative inflation rate. It will result in a composite rate of 1.38% for six months.

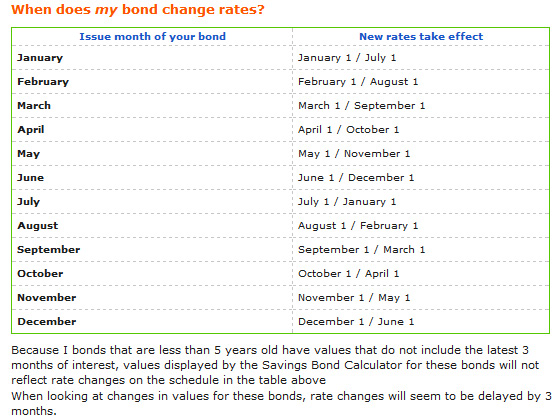

But … my Savings Bond Wizard shows a higher rate! It might, and it isn’t wrong. The I Bond composite rate rolls out across six months, depending on the month when you first bought the I Bond. The Treasury has another nice chart that shows this:

So the Savings Bond Wizard will continue to show a higher rate, based on the last period’s 1.48% variable rate, until the new rate kicks in – depending on the month when you first bought the I Bond. If you bought an I Bond in October 2003, the new rate will begin in October 2015 and continue for six months. If you bought in November 2003, the new rate started May 1 and will continue for six months.

So the Savings Bond Wizard will continue to show a higher rate, based on the last period’s 1.48% variable rate, until the new rate kicks in – depending on the month when you first bought the I Bond. If you bought an I Bond in October 2003, the new rate will begin in October 2015 and continue for six months. If you bought in November 2003, the new rate started May 1 and will continue for six months.

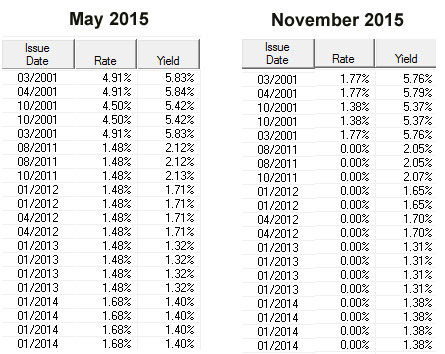

I have updated my Savings Bond Wizard and here is what is it showing for May 2015 and November 2015 for the I Bonds I currently own:

FYI: Rate is the current six-month composite rate, yield is the annualized yield over the lifetime of the I Bond.

That is almost crystal clear, isn’t it? As the new composite rate rolls out over the next six months, all my I Bonds will be affected by the -1.6% variable rate, and the yield – the annualized interest paid over the life of the I Bond – will also decline.

Take a look at the two I Bonds issued in October 2001. They have a fixed rate of 3.0% (nice!) and so they fit the formula that I posted above:

[0.0300 + (2 x -0.0080) + (0.0300 x -0.0080)]

[0.0300 + -0.0160 + – 0.00024]

0.01376

resulting in a composite rate of 1.38%

If you look at the November 2015 rate, it is 1.38%.

And another thing. I am totally, 100% recommending hanging on to all your I Bonds through this six months of reduced returns. Inflation fell at an annual rate of -1.60% from September 2014 to March 2015. Even if you are getting a return of 0.0%, you are beating inflation by 1.6%. You’ll survive.

Because you can buy only $10,000 per person in I Bonds each calendar year (plus the IRS refund trick), they are an asset to hold. I Bonds are part of a strategy of pushing inflation-protected, tax-deferred money into the future. The only reason to sell them is if you need the cash right now.

I hope this helps clear up some of the confusion circling around I Bonds in these strange months of post-deflation 2015.

I plan on selling some SGOV and buying before the end of the month as well. I had one I…