I just noticed that the TIP ETF, which holds a broad range of maturities, is trading at $112.01 today, down 1.1% for the day. The ETF reached $114.14 on Feb. 27, and has since fallen 1.9% in just five trading days.

Part of the reason, at least, is increasing signs of an improving economy. Today’s evidence was news that U.S. nonfarm payrolls grew by a seasonally adjusted 295,000 jobs in February. The economy has now added more than 200,000 jobs for 12 straight months, the longest such streak since 1995, according to the Wall Street Journal. The U.S. unemployment rate fell to 5.5% in February, down from 5.7% in January.

An improving economy raises the possibility that the Federal Reserve will finally relent and begin raising short-term interest rates. Rates have held near zero since 2008.

So far, very weak inflation has allowed the Fed to avoid any move on interest rates. But if the economy continues to improve and the jobless rate continues to fall, wages should begin to increase, and that is a huge first step toward inflation.

While rising inflation would appear to create higher demand for TIPS, higher interest rates in the overall Treasury market would force TIPS yields higher and prices lower.

- The yield on a nominal 10-year Treasury is currently trading today at 2.25%, up 14 basis points for the day and up a rather enormous 57 basis points since Feb. 1. And this yield could easily move higher — it stood at 3.0% on Jan. 1, 2014.

- The real yield to maturity of a 10-year TIPS is currently trading today at 0.41%, up from a close of 0.27% yesterday. That is also 14 basis points, so TIPS and nominal Treasurys seem to be moving in lockstep.

However, a five-day chart comparing TIP with IEI (the intermediate Treasury bond market) and GOVT (the overall Treasury market) shows that TIPS are taking Friday’s news much harder, with yields rising as the ETF price falls (click on image for a larger version):

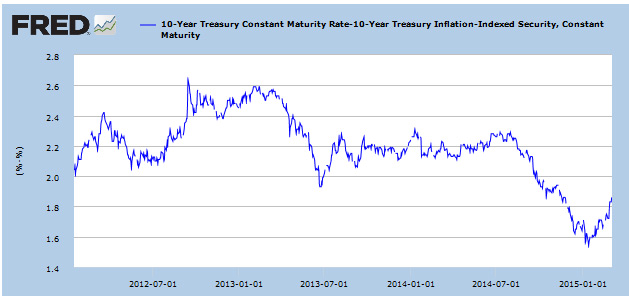

Another factor to watch is the 10-year inflation breakeven rate, which has been rising from extremely low levels. Today’s implied inflation breakeven rate is 1.84%, still low by historical standards but up sharply since the 1.57% posted on Jan. 14. This indicates inflation expectations are rising – and also that TIPS are getting slightly more expensive versus traditional Treasurys. Here is the recent trend in the 10-year inflation breakeven rate:

Another factor to watch is the 10-year inflation breakeven rate, which has been rising from extremely low levels. Today’s implied inflation breakeven rate is 1.84%, still low by historical standards but up sharply since the 1.57% posted on Jan. 14. This indicates inflation expectations are rising – and also that TIPS are getting slightly more expensive versus traditional Treasurys. Here is the recent trend in the 10-year inflation breakeven rate:

This month’s TIPS auction – on Thursday, March 19, will be a reopening of CUSIP 912828H45, a 10-year TIPS that originated on Jan. 22 with a real yield to maturity of 0.315% and a coupon rate of 0.250%. It will be interesting to watch how yields react in the next two weeks leading up to the auction.

This month’s TIPS auction – on Thursday, March 19, will be a reopening of CUSIP 912828H45, a 10-year TIPS that originated on Jan. 22 with a real yield to maturity of 0.315% and a coupon rate of 0.250%. It will be interesting to watch how yields react in the next two weeks leading up to the auction.

My omission--Thank you!