I hate to be negative, but the current trend in the Treasury market has me thinking evil thoughts. Why? Yields on Treasury Inflation-Protected Securities have dropped to levels negative to inflation for maturities all the way up to 9 years. There are 39 TIPS currently trading on the secondary market, and yields are negative on 23 of them.

I hate to be negative, but the current trend in the Treasury market has me thinking evil thoughts. Why? Yields on Treasury Inflation-Protected Securities have dropped to levels negative to inflation for maturities all the way up to 9 years. There are 39 TIPS currently trading on the secondary market, and yields are negative on 23 of them.

This is great if you own TIPS you want to trade or if you are invested in TIPS mutual funds. The value of your holdings has ‘soared’ – as much as Treasurys ever soar – in the brief time since Valentine’s Day. Here’s a chart for that time, comparing the TIP ETF, which holds the full range of TIPS, with the SPY ETF, invested in the S&P 500.

Click on image for larger version

My evil thoughts arise because I’d like to be a net buyer of TIPS, buying more than mature each year as part of a super-safe allocation in my heading-to-retirement portfolio. But right now TIPS are off the table, and I’d certainly shy away from TIPS mutual funds. And I Bonds – another trusty, super-safe investment – are about to enter a six-month period paying zero interest. Bank CDs – paying about 1% for a 1-year CD and 2.25% for a 5-year – might be a more acceptable alternative, although hardly desirable.

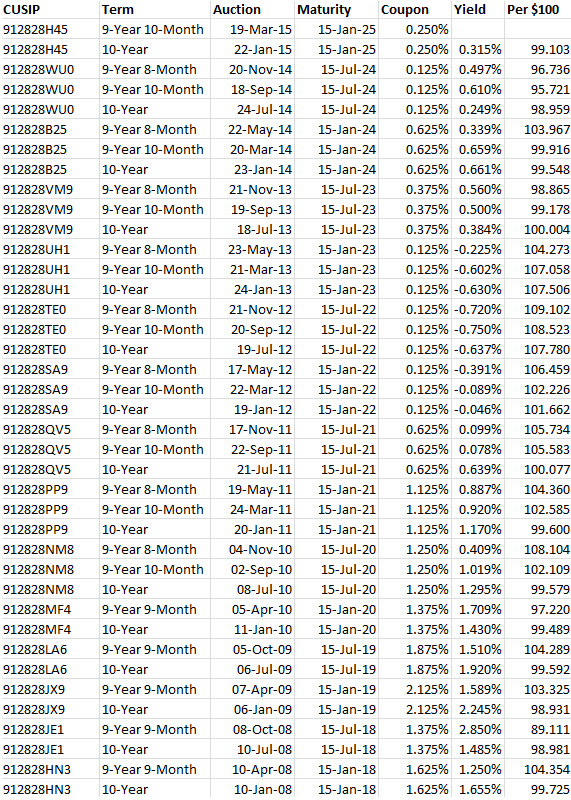

I’ve called TIPS the ‘Energizer Bunny’ investment in the past – they just keep going and going. Look at a 5-year TIPS. Last year’s December reopening auction resulted in a yield of 0.395%, highest in 4 1/2 years. Today, the yield on that same TIPS is -0.505%, down a shocking 90 basis points in five months. And yet the inflation index for that TIPS is .997; there has been less-than-zero inflation since this TIPS was first issued in April 2014.

Here are factors driving TIPS yields down:

- Central banks around the world are trying to inflate their currencies with asset-buying programs, resulting in 10-year bonds in Switzerland paying -0.11%; in Germany, 0.17%; in the Netherlands, 0.33%; in more-risky Portugal, 1.68%. You can get 1.88% in the non-risky United States, and that is where money is flowing.

- A crucial turning point came March 18, when Federal Reserve Chair Janet Yellen gave a decidedly wish-washy view on future short-term interest rate increases in the United States. She said: “Just because we removed the word ‘patient’ doesn’t mean we’re going to be impatient” in raising rates. The market interpreted this – correctly, I think – that the Federal Reserve lacks the courage to begin raising interest rates until inflation is above – possibly well above – its target of 2%.

- Yellen’s comments weakened the dollar, with the Euro gaining about 3% in value since her statement. It also ignited just a touch of inflation fears, which had been dormant after months of mild deflation. This makes TIPS more appealing, even at these low yields.

- If you suspect inflation will rise again to around 2%, TIPS are still the relative ‘bargain’ of the Treasury market. A 10-year TIPS currently has an inflation breakeven rate of about 1.81%. This number usually averages in the 2.0% to 2.2% range, so TIPS remain cheap against nominal Treasurys. That also increases demand.

Just as a rough guideline, I often say that TIPS mutual funds would be appealing to me when the TIP ETF reaches $110. This would happen when the 10-year yield rises to about 0.90%, a long way up from the current 0.07%.

But consider this: The TIP ETF closed at $111.51 on March 13, less than one month ago. Since then it is up 2.7%, and the Energizer Bunny dances on.

Here is that article: https://tipswatch.com/2026/04/05/a-5-year-tips-is-maturing-april-15-how-did-it-do-as-an-investment-2/