The Consumer Price Index for All Urban Consumers (CPI-U) declined 0.4% in December on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 0.8%.

From August until the end of 2014, US prices fell 0.7%. December’s sharp decline was primarily caused by a massive 9.4% drop in the price of gasoline, which is down 21% in the last 12 months. Fuel oil was down 7.4%. Food prices, however, rose 0.3%. The shelter index rose 0.2%, and the index for medical care commodities was up a sharp 1.0%.

What this means for TIPS and I Bonds. Today’s inflation report isn’t welcome news for holders of Treasury Inflation-Protected Securities and I Bonds. Non-seasonally adjusted CPI-U – which fell 0.57% in December – is used to adjust the principal balance of TIPS and set future interest rates for I Bonds. The December inflation index was set at 234.812, below where it stood in March 2014 (236.293). In just three months, from September to December 2014, non-seasonally adjusted CPI has dropped 1.36%.

I have updated my Tracking Inflation and I Bonds page to reflect these new numbers.

This is setting up a problem for I Bonds in 2015. I Bonds purchased through April 30 pay a fixed rate of 0.0% and an inflation-adjusted rate of 1.48% annualized. The next adjustment for the inflation -adjusted rate – on May 1 – will be determined by inflation from September 2014 to March 2015. Three months in, that’s running -1.36%, so it looks highly likely that I Bonds will get an inflation-adjusted rate of 0.0% on May 1, to go along with a fixed rate that may hold at 0.0%. In other words, zero + zero = zero.

What this means: Do not plan on buying your 2015 allocation of I Bonds ($10,000 per person per calendar year) until late in the year, after the Nov. 1 adjustment.

Core inflation. Even when you strip out food and energy, US inflation was unchanged in December and rose 1.6% over the last 12 months. This is well below the Federal Reserve’s target of 2.0% annual inflation, and should allow the Fed to continue holding the line on near-zero short-term interest rates.

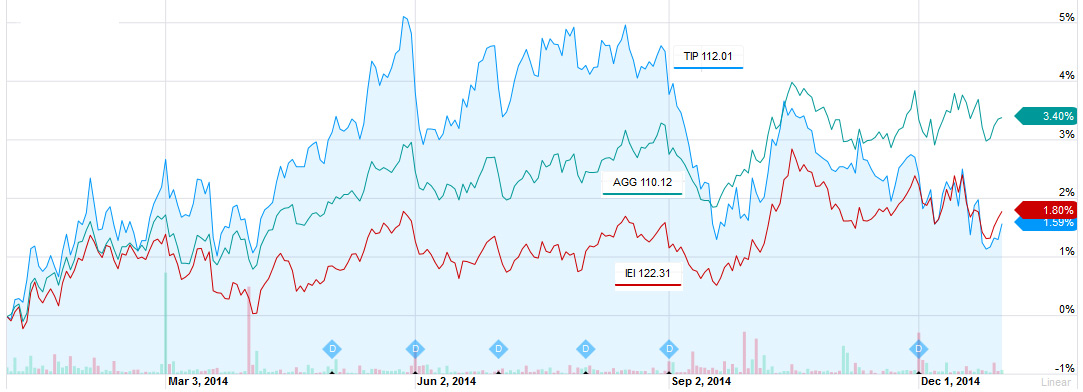

Year in review. CPI-U rose 0.8% in 2014 after a 1.5% increase in 2013. This is the second-smallest December-December increase in the last 50 years, trailing only the 0.1% increase in 2008. The BLS noted it is considerably lower than the 2.1% average annual increase over the last ten years. This chart shows the deflationary trend as gasoline prices fell sharply in the second half of the year:

I wavered a bit when I heard that the fixed rate is likely to remain 0.9% at the May reset,…