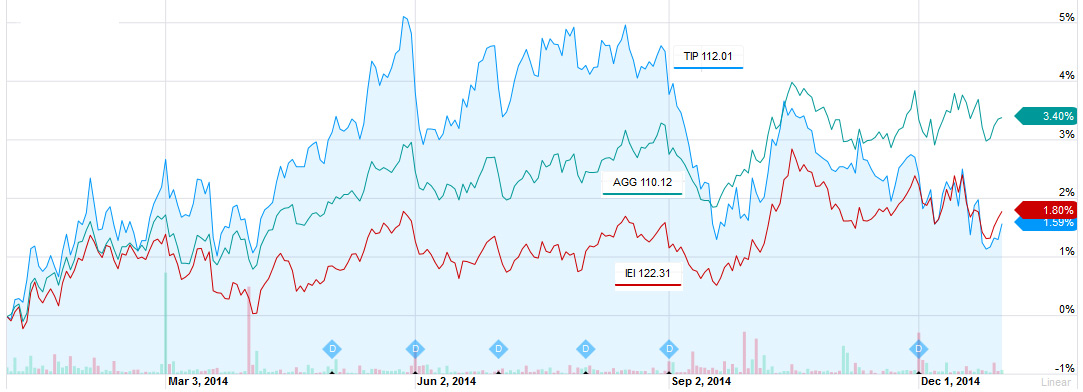

After suffering through a miserable 2013, holders of mutual funds based on Treasury Inflation-Protected Securities enjoyed a rather pleasant 2014. The TIP ETF – a big fund that is diversified through maturity dates – started the year on Jan. 2 at $110.26 and closed Dec. 31 at $112.01. That’s a capital gain of about 1.6% – on top of any interest distributions. (Morningstar reports TIP’s total return as 3.59% for 2014.)

Nevertheless, the TIP ETF underperformed the overall bond market, as shown in this graph comparing the one-year performance of TIP, IEI (intermediate-term Treasurys) and AGG (the overall bond market):

SOURCE: Yahoo Finance / Click on image for larger version

For buy-and-hold investors of TIPS, this year’s auctions included several unique buying opportunities, even though yields on mid- to longer-term TIPS slid throughout the year. Here’s a recap of each of the issues and reopenings:

10-year TIPS, CUSIP 912828B25

- First auctioned: Jan. 23, with a coupon rate of 0.625% and a yield to maturity of 0.661%, plus inflation. This was the highest yield for any 9- or 10-year TIPS at auction since May 2011 and ended up being the highest yield of any of the six auctions for this term in 2014.

- Reopened: March 20, with a yield of 0.659%, just under the initial auction.

- Reopened: May 22, with a yield of 0.339%, a big drop from the initial auction, resulting in an adjusted price of about $103.96 per $100 of value.

30-year TIPS, CUSIP 912810RF7

30-year TIPS, CUSIP 912810RF7

- First auctioned: Feb. 20, with a coupon rate of 1.375% and a yield to maturity of 1.495%, plus inflation. This ended up being the highest yield of the year for this term. This auction set a 30-year inflation breakeven rate of 2.23%.

- Reopened: June 19, with a yield to maturity of 1.116%. Buyers paid an adjusted price of $108.34 for $100 of value – showing the volatility of 30-year issues.

- Reopened: Oct. 23, with a yield to maturity of 0.985% and an adjusted price of $112.17 per $100 of value. The 30-year inflation breakeven rate fell to 2.065% — and has continued falling to 1.92% on Dec. 31.

5-year TIPS, CUSIP 912828C99

5-year TIPS, CUSIP 912828C99

- First auctioned: April 17, with a coupon rate of 0.125% and a yield to maturity of -0.213%, plus inflation. The negative yield resulted in an adjusted price of $101.87 for $100 of value. The 5-year inflation breakeven rate was set at 1.91%.

- Reopened: Aug. 21, with a yield of -0.281%.

- Reopened: Dec. 18, with a yield to maturity of 0.395%. This was the highest yield – and first positive yield – for any 4- to 5-year TIPS since April 2010. The 5-year inflation breakeven rate fell to a remarkable 1.26%. I was a buyer at this auction.

10-year TIPS, CUSIP 912828WU0

10-year TIPS, CUSIP 912828WU0

- First auctioned: July 24, with a coupon rate of 0.125% and a yield to maturity of 0.249%, plus inflation. This was the lowest yield of any 9- to 10-year TIPS auction since May 2013. The 10-year inflation breakeven rate was set at 2.26%.

- Reopened: Sept. 18, with a yield to maturity of 0.610%, a big jump over the initial auction. That dropped the adjusted price to $95.72 per $100 of value and set the inflation breakeven rate down to 2.02%. I was a buyer at this auction.

- Reopened: Nov. 20, with a yield to maturity of 0.497% and an adjusted price of $96.73 per $100 of value. The inflation breakeven rate fell to 1.853% – it closed on Dec. 31 at 1.68%.

Jimbo, at this point I would hold off buying TIPS, even more so on the secondary market, since we are going to see some months of deflation or near deflation. I personally won’t touch my current holdings — that is my style, hold to maturity. But TIPS are actually extremely cheap compared to nominal Treasurys, especially with economic growth chugging along at 3%+. There aren’t any great safe alternatives, either.

After reading a couple of Zvie Bodie’s books in retirement planning, TIPS and iBonds looked like something worth looking into. Your website (and it’s links) expanded significantly on the

information provided in Professor Bodie’s books.

The original goal was to create a ladder of TIPS with maturities ranging from 5 to 10 years. As of the end of 2014, that ladder’s in place with small positions going out to 2024. In addition

to those TIPS, there’s also a ladder of iBonds with equivalent maturities of 2, 3 and 4 years (since they can be cashed-in without penalty within that time horizon).

Since the whole point of TIPS and iBonds is inflation adjusted principle protection, they’ve definitely fit the bill for that. The big question is whether or not it’s worth the bother to make further purchases in 2015.

During the past 12 months, inflation averaged 1.3%. With energy prices expected to decline further, that trailing 12 month rate will probably go even lower over the next 6 months. There’s

a realistic possibility that the 12 month average inflation adjustment may sink to under 1.0%.

In addition to deflation, it appears that the Fed may finally start to raise rates sometime this year. Depending on what happens with the economy, the Fed is targeting 2% as the peak rate for

the foreseeable future. This will add an incremental interest rate risk to bonds.

The only offering that might be worth the bother this year may be the 5 year TIPS. Currently, the 4/15/19 TIPS has had a positive YTM (and has for a while now). At one point recently, the

inflation adjusted price was going for under par on the secondary market.

If that happens again, I may just shift some of my 6 to 10 year TIPS into shorter maturities. It doesn’t make much sense to hold 10 year bonds yielding 0.4% when a 5 year bond is at 0.2%. I’d also like to keep the maturities less than my life expectancy!

About the only bright side to last year was that you could actually make some decent money trading TIPS. It’s doubtful that will continue much longer. But then, the TNX closed below 2.0%

today. That’s back to what it was in May of 2013. The FVX closed below 1.5%. That’s back to what it was in July of 2013.

This just tells you that the world is still in a very dangerous place with regards to financial stability. The Saudi’s move to retain market share in the US by crushing the competition certainly isn’t going to help things much in the coming months.

Hi, John and welcome. What will be really interesting is that the Treasury will issue a new 10-year TIPS this month that will also mature on Jan 15 2025 unless the Treasury does something strange (like making it a 10-year, 2 month TIPS). You will be able to buy that one around par with a yield to maturity of about 0.40%. It should cause a dip in demand for the existing Jan. 15 2025 issue (which started life as a 20-year TIPS). It has a coupon of 2.375% and accrued principal of 25% – wow, that would be expensive. I’ll be writing about this new issue soon.

Hi Dave,

Thanks for the great blog! I’m a first time reader and retiring soon. Currently I have no TIPS but am thinking about building a ladder in my tax-deferred IRA from the secondary market. So I looked at the WSJ / Tullett Prebon link which you mentioned was useful (below) and noodled on buying one of every year available. It surprised me how much these maturities differ, for example Jul 2024 has a low coupon rate (bad) but also a low Accrued Principal (good, according to the deflation risk you described to John R. above). Whereas Jan 2025 only 6 months later is completely the opposite (figures below). Incredible, and seems like an example of the benefit of diversity in maturities for TIPS. As to the degree of deflation risk, a scenario where the price level 10 years from now is lower than it is now doesn’t seem very likely but who knows.

I’ll also take a look at the January auction. I thought getting into TIPS would be pretty simple but it’s more complex than I thought, and more interesting.

Anyway thanks again and keep up the great work!

Maturity Coupon Bid Asked Chg Yield* Accrued Principal

2024 Jul 15 0.125 96.16 96.26 18 0.466 999

2025 Jan 15 2.375 117.21 117.31 19 0.534 1259

http://online.wsj.com/mdc/public/page/2_3020-tips.html?mod=topnav_2_3021

John, it is true that I pretty much exclusively buy TIPS at auction and hold them to maturity. That’s just my investing style — it creates zero commissions, zero fees. I don’t have a problem with buying TIPS on the secondary market, though, especially in tax-deferred accounts. But my style would still be buy and hold to maturity.

That TIPS maturing in January 2010 – five years from now – would be attractive to me with a yield of 0.31%, plus inflation. But … and this is a big problem … realize that you will be buying almost 10% of inflation appreciation with that TIPS. That will raise your purchase price, and normally, that’s not a big problem, you get it back when the TIPS matures. But if inflation continues to run below zero for several months – last month it was -0.54% non-seasonally adjusted – you will see that inflation appreciation erode, lowering the value of your investment. That is why shorter term TIPS have fairly high yields right now — investors are expecting that deflation will erode the principal.

On the other hand, I theorize that gas prices can rise just as quickly as they fall, and it’s possible you could gain back that lost principal very quickly in the next five years.

Thanks for your informative comments. To clarify, I’m not considering buying any debt while interest rates are this low, since that environment is usually much better for stocks. I assume that when a robust economic expansion brings with it a threat of inflation, we’ll see short rates climbing and that will be the time for me to start buying some inflation protection. Equities tend to lose their luster when the 10-year Treasury goes above 5%. For a fascinating look at the dynamics of yield curve vs equity prices, see http://stockcharts.com/freecharts/yieldcurve.php and run the animation. Today’s yield curve looks nothing like ’99 or ’06. But I want to be an intelligent consumer of TIPS when the time comes so I will avidly follow your thoughtful commentary.

I’ve just begun trying to understand how TIPS might work for me over the next decade or so. I think I understand something about how bond markets work: when rates are rising you want to own the 5-year duration because they pay enough yield to make up for the risk of loss of principal should you have to sell before maturity, but when the yield curve inverts it predicts interest rates will be coming down so you want to be in longer-term bonds to take advantage of potential capital gains. I’m not sure if that logic applies to TIPS because of the way their prices react to inflationary expectations. Also, I’ve noticed you talking mostly about buying TIPS from the Treasury at auction and not about buying in the aftermarket, and I wonder why that is. Today, for example, I find CUSIP 912828MF4 issued 1/15/10 and maturing 1/15/20 has a yield to maturity of 0.31. Is this a bad deal?