Ouch. But it’s OK. We’re used to it.

The Federal Reserve’s Open Market Committee on Wednesday issued minutes from its June meeting, with the headline being: ‘Economy is improving, inflation is rising, but Fed stands by ultra-low interest rates well into the future.’

Here’s a summary of key points from the minutes:

- The economy. (G)rowth in economic activity rebounded in the second quarter. Labor market conditions improved, with the unemployment rate declining further.

- Jobs. However, a range of labor market indicators suggests that there remains significant underutilization of labor resources.

- Inflation. Inflation has moved somewhat closer to the Committee’s longer-run objective. Longer-term inflation expectations have remained stable.

- Jobs vs. inflation. The Committee sees the risks to the outlook for economic activity and the labor market as nearly balanced and judges that the likelihood of inflation running persistently below 2 percent has diminished somewhat.

- Tapering continues. Beginning in August, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $10 billion per month rather than $15 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $15 billion per month rather than $20 billion per month.

- The Fed’s massive balance sheet. The Committee’s sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.

- Short-term rates will remain near zero. In determining how long to maintain the current 0 to 1/4 percent target range for the federal funds rate, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. … The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate for a considerable time after the asset purchase program ends, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal.

There are absolutely no surprises in this. The Federal Reserve will soon end its bond-buying quantitative stimulus, and then the clock will start ticking on the end of its near-zero federal funds rate. Will that rate begin rising in mid-2015, as Fed Chair Janet Yellen hinted earlier this year? We don’t know. The Fed says only that these rates will continue near-zero ‘for a considerable time.’

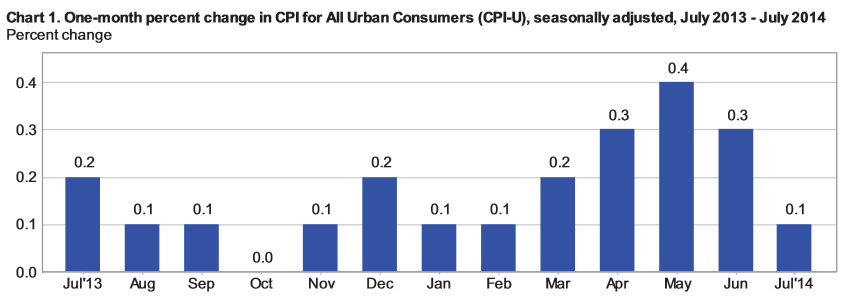

It is important to note that headline inflation is now running at 2.1%, so it has crossed the Fed’s initial target of of 2% (although it uses a different measure). Unemployment has declined to 6.1%, well below the Fed’s initial target of 6.5%.

And yet short-term interest rates remain near zero, and will continue there for a considerable time. That policy, along with the Fed’s balance sheet of reinvesting Treasuries and mortgage securities, will also tend to hold down long-term interest rates. And that means borrowers gain and savers lose. Thrifty Americans looking for safety can find – at best – interest rates that barely beat inflation, or more likely lag severely below it.

The Wall Street Journal today is speculating that the Fed committee is beginning to feel pressure to raise interest rates, at least symbolically:

Some Fed officials are reluctant to wait too long before acting to raise interest rates. Philadelphia Fed President Charles Plosser dissented from a portion of the Fed’s statement because it failed to reflect “considerable economic progress” officials had witnessed.

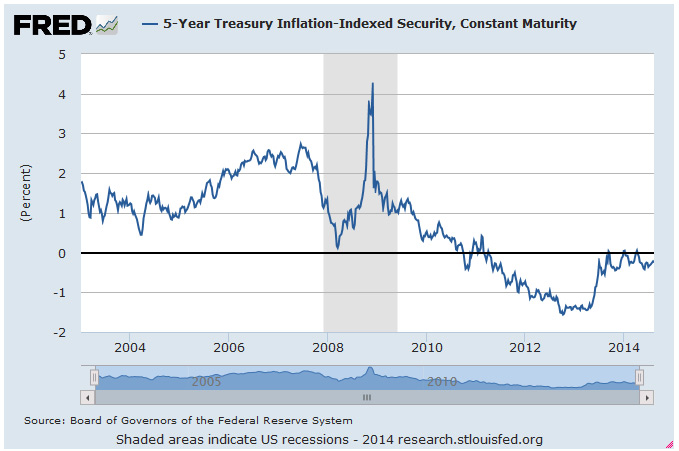

The TIPS market, which has been on a tear this year, took a hit Wednesday, as investors speculated that the easy money can’t last forever (plus, let’s face it, they took profits out of overvalued TIPS). Here’s a five-day chart of the TIP ETF, showing the Wednesday reaction:

Michael Ashton, who writes about inflation in his excellent E-piphany blog, is speculating that the Fed is ‘gearing up to stand down’ and that the stock market will be the primary victim when that happens:

It will certainly be interesting to see how long markets can remain levitated when the Fed’s buying ceases completely. Frankly, I am a bit surprised that these valuation levels have persisted even this long, especially in the face of rising global tensions and rising inflation. …

Ashton also makes the case that the Fed is ill-equipped to 1) recognize or 2) act on rising inflation, and that it will very likely overshoot its target. It’s a great piece of writing, so head over there now to check it out.

It is true that I could have redeemed it when the rate was 1.9%, and maybe could have earned more…