Beautiful Fort Anne, built in 1797 to protect the harbor of Annapolis Royal, Nova Scotia.

I’ve been away on vacation in Nova Scotia the last two weeks, away from a computer and (usually) far from e-mail or business news. So we have some catching up to do … plus there is a 10-year TIPS reissue auction coming up this week … and a new inflation report.

Bump in yields

When I left on August 30, the 10-year TIPS yield stood at 0.68%, plus inflation. Today it is about 0.76%, so it’s seen a bit of a boost. But within those two weeks, on September 5, it high a multi-year high of 0.92%. The inflation breakeven rate for a 10-year TIPS today stands at 2.12%, about where it was two weeks ago.

Today’s inflation report

The U.S. ‘headline’ inflation rate – technically known as the seasonally-adjusted Consumer Price Index for All Urban Consumers (CPI-U) – increased just 0.1% in August and is up a meager 1.5% over the last 12 months. The weak number was primarily caused by a 0.1% drop in the price of gasoline, and a 0.3% decline in energy overall. Food was up just 0.1%. Medical care services, however, were up a sharp 0.7%.

Holders of TIPS and I Bonds care most about the non-seasonally adjusted increase, which is used to adjust the principal on TIPS and set future rates for I Bonds. That increase was also 0.1% in August, and 1.5% over the last 12 months.

‘Core’ inflation, which strips out energy and food, was also up 0.1% in August and up 1.8% over the last 12 months, below the Federal Reserve’s target of 2%.

Today’s inflation report could tip the balance to cause the Federal Reserve to back away from plans to taper its QE3 purchases of Treasuries. That announcement could come Wednesday after a Federal Reserve meeting.

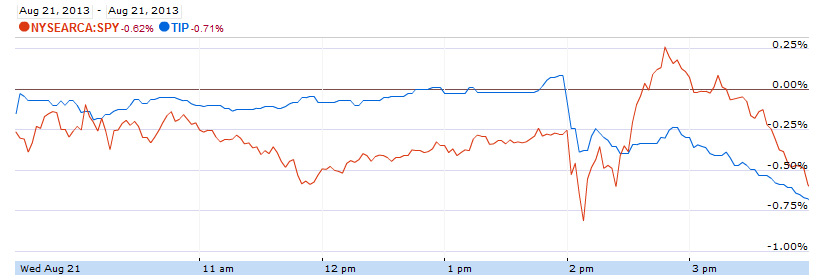

The early reaction to these numbers has TIPS yields falling today, with the 10-year TIPS trading at 0.70%, down 6 basis points from yesterday. The TIP ETF is up about 0.25% in early trading.

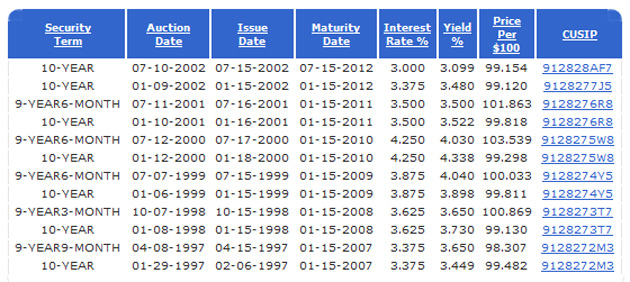

10-year TIPS reissue will auction Thursday

This is a reissue of CUSIP 912828VM9, which first auctioned July 18, 2013, with a coupon rate of 0.375% and a yield to maturity of 0.384%. That means Thursday’s auction will be going off at a discount, about $96.19 for $100 of value. But this TIPS also carries accrued interest (from inflation adjustments) of about 0.3%, which will also factor into the price.

I was a buyer of this TIPS back in July, and it is certainly more attractive now that the yield has risen more than 30 basis points.

Wednesday’s Fed announcement could roil the markets, so keep an eye out for reaction. If the Fed goes ahead and launches tapering, TIPS yields could rise substantially (although I theorize this has already been priced in). If Fed decides to hold off on tapering, expect yields to decline.

More on this later. It’s good to be back.

Unless we see an extended period of deflation (unlikely) your investment should perform about the same as today's auction.